Skip to content

Skip to content

In this blog, we discuss the digitization of the music industry and Spotify’s struggle for profitability as the world’s largest music streaming platform.

The era of piracy

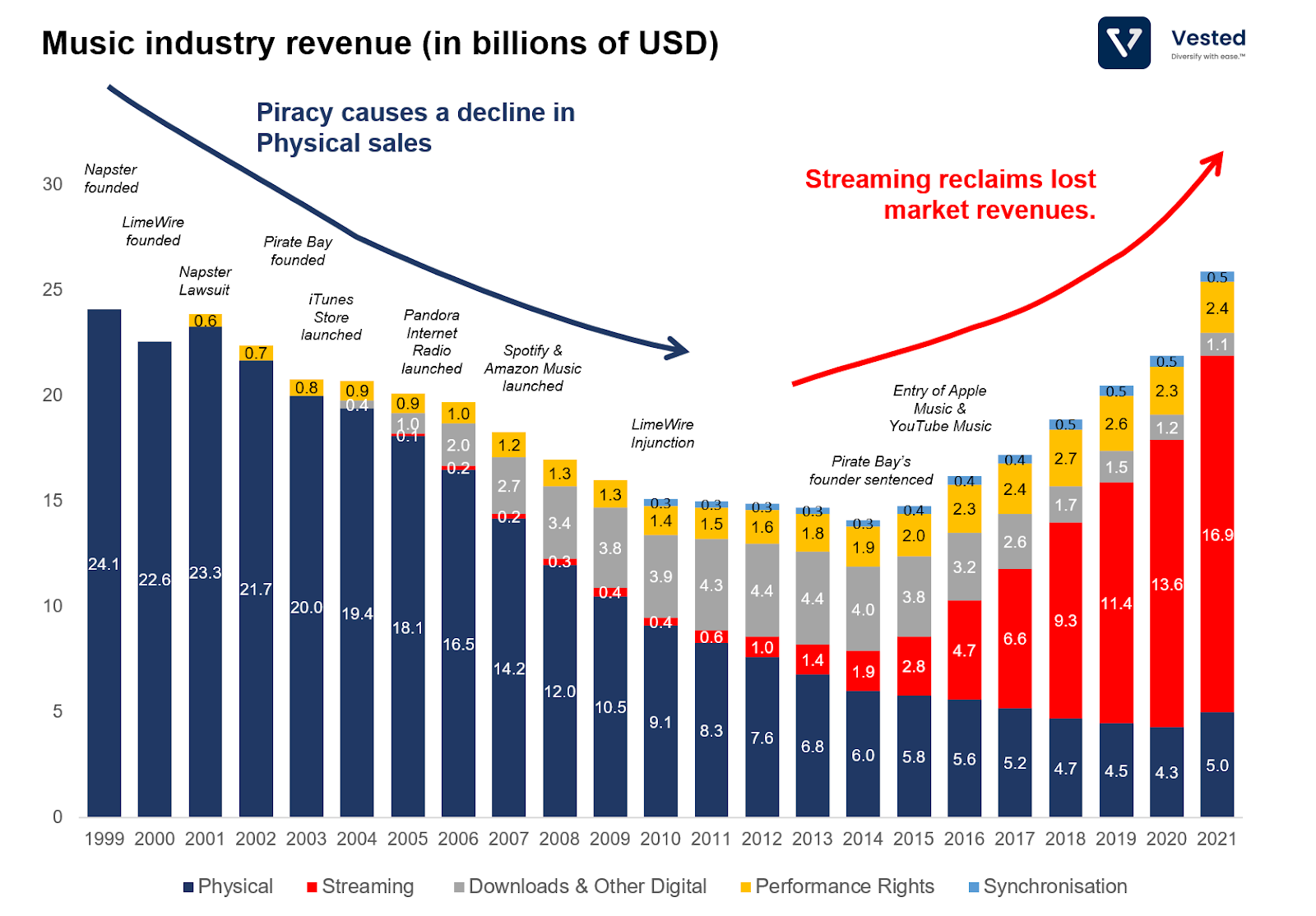

The music industry peaked at the turn of the last century and declined until 2014 (see Figure 1). In the early 2000s, the internet made it simpler for consumers to access and listen to music, reducing the need for physical copies. Meanwhile, websites such as Napster, Limewire, and Pirate Bay enabled peer-to-peer file-sharing, which led to rampant piracy. As a result, the global music business suffered a dip in revenues as customers were less inclined to pay for music.

The industry attempted to curb piracy by issuing legal actions against peer-to-peer file-sharing platforms and by suing university students who participated in such activities. The impact of these efforts was marginal. Instead, salvation for the industry came from the tech sector. Advancements in digital music helped slow the industry-wide revenue decline (see Figure 1 above). The tech sector introduced two key innovations: (i) digital downloads, enabling consumers to unbundle an album and buy one song at a time, and (ii) music streaming.

The pioneer of (i) was, of course, Apple. In 2003, Steve Jobs introduced the iTunes Store, which allowed the a-la-carte purchase of music ($0.99 for a song or $10 for an album). Digital distribution of music is much cheaper than physical distribution, enabling a much lower price point. As you can see, the gray bar (depicting revenue contribution by digital downloads in Figure 1 above) expanded in 2004 and peaked around 2012. Although it helped slow the decline, digital downloads alone could not reverse the downward revenue decline. Fortunately, music streaming came into the picture.

One of the first music streaming services was Spotify, launched in 2006, followed by Amazon, which launched its streaming music service in 2007. Over time, music streaming overtook digital downloads and became the primary revenue driver for the industry (red bar in Figure 1 above).

The industry also saw lower piracy thanks to streaming. Music-related piracy sites saw a 65% decrease in traffic from 2014 – 2021. Consumers inherently do not favor piracy. They favor convenience and low costs, something that music streaming provides:

- Music streaming gives users convenience: Pirating music is not only illegal but is also complicated, time-consuming, and poses cybersecurity risks.

- Music can be free: Thanks to the freemium ad-supported model, people who don’t want to pay for music can still use ad-supported services. This, in turn, acts as a marketing funnel. For example, Spotify reported that over 60% of its premium subscribers initially started with its ad-supported offering.

The difference between music and video streaming

It is common for the music streaming business to be compared to video streaming. In reality, they are quite different, resulting in a significant difference in profit margins.

People consume video and audio differently. For most people, music consumption is more repetitive (they tend to listen to the same music repeatedly). This is why listening to catalogs (any music older than 18 months) make up 72.4% of US music consumption. Because of this emphasis on back catalog consumption, music streaming services must provide an extensive offering of music (both current & back catalog) for their customers.

In contrast, video consumption tends to focus on new releases with minimal repeat consumption (binge-watching Friends is an exception). This difference in consumption is why people are willing to pay for multiple video streaming services. Customers want to maximize content diversity. As such, the video streaming business is very “hit”-driven.

This difference in consumption means that, for video streaming, it’s essential to own new hits. This is why the world’s largest streaming platforms compete to own and develop their 1st party content. When they do so, they own the IP outright, and by removing the middlemen, video streamers can gain operating leverage. In contrast, music consumption is backward-looking. This means that music streamers must license content from music labels. This has a significant impact on profitability.

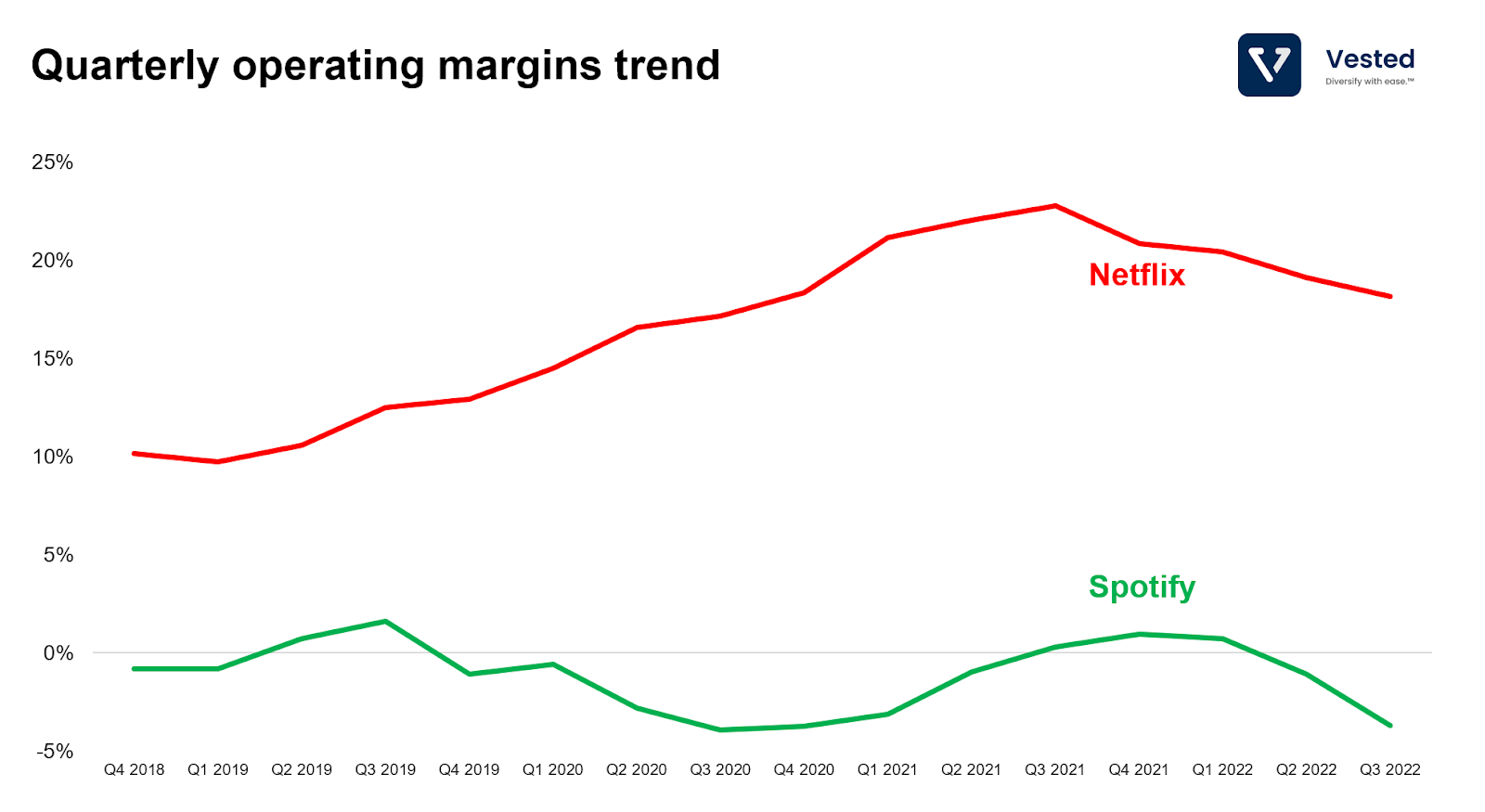

To illustrate this point, we compare the operating margins of the two biggest streamers in these two categories: Spotify and Netflix (see Figure 2 below).

In Figure 2 above, Netflix’s operating margin increased as it began to own more and more of the content it showed on its platform. As Netflix’s subscriber base grew, it spread the fixed cost of content investments to more and more of its subscribers. In contrast, Spotify is not increasing its operating profits. Why is this so?

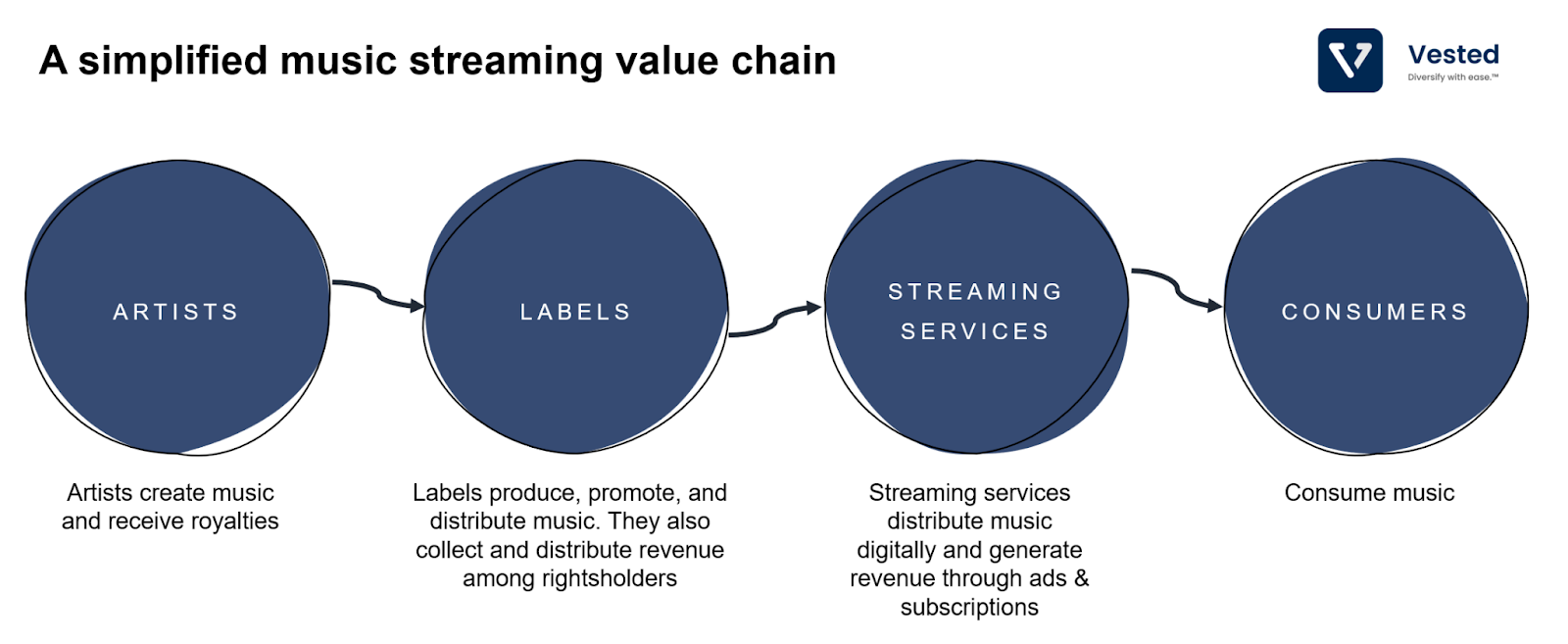

The music value chain

To better understand Spotify’s predicament, let’s look at the streaming music value chain. Here’s a simplified diagram.

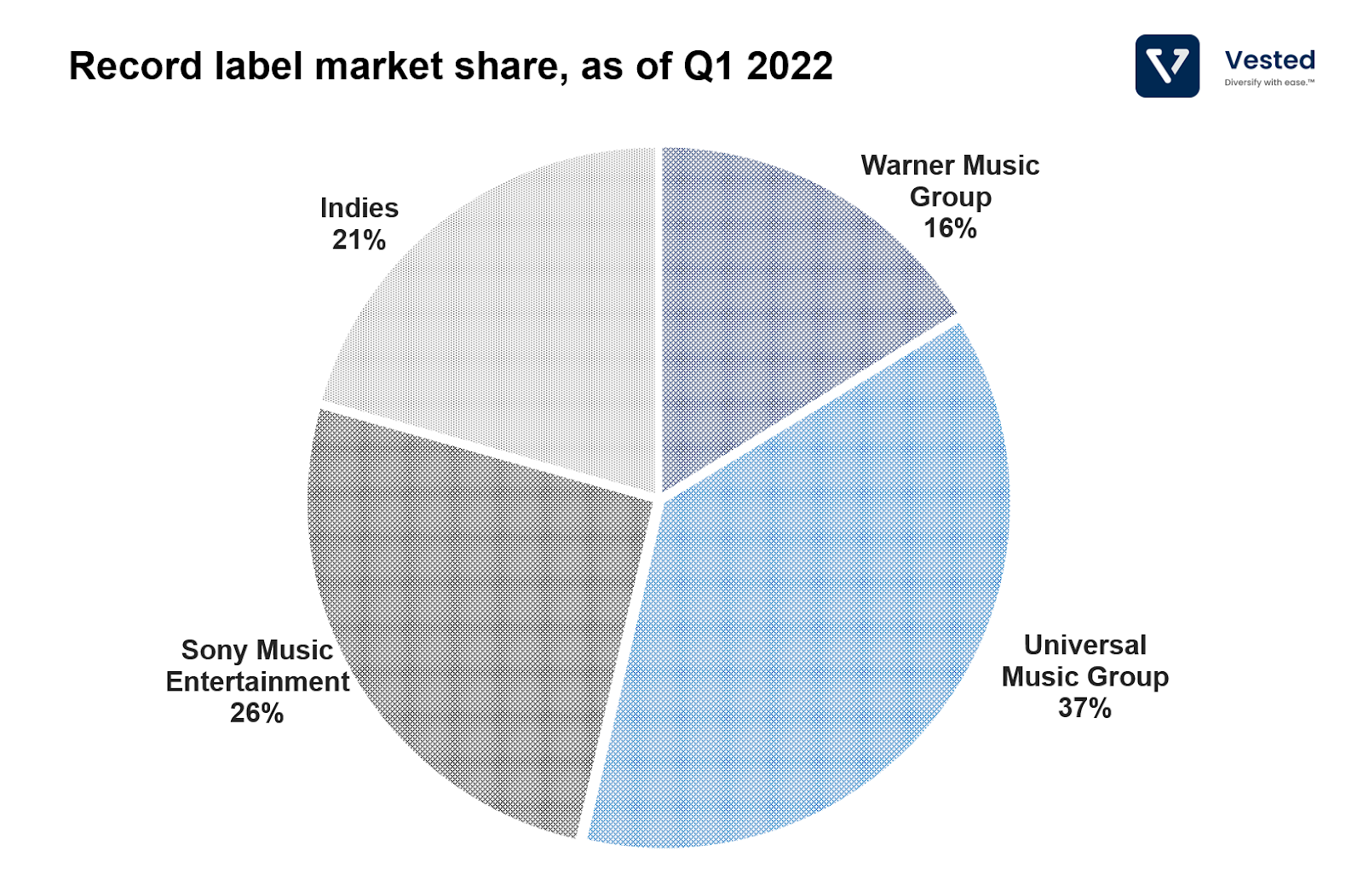

Value chains are important. In a recent article, we discussed that value (and therefore profits) accrue at the point of the value chain where power is concentrated. Despite being a consumer-facing application, music streaming services typically do not have leverage over labels in the music streaming value chain. This is because of the nature of the consumption of music we discussed above. The labels own the rights to the back catalog, and you cannot offer a music streaming service without access to an extensive library of back catalogs. Currently, licensing of back catalog is dominated by three large private labels: Warner Music Group (WMG), Universal Music Group (UMG), and Sony Music.

These three major labels own the rights to a combined share of about 80% of music streams (see Figure 4 above). In other words, they have the strongest position in the value chain and can negotiate better contracts. For example, it was leaked that Spotify’s agreement with Sony Music included a Most Favored Nation clause that allowed Sony to automatically receive increased annual advances if another label negotiated a bigger payout from Spotify. This clause also imposed a cap on how much profit Spotify could make from ad revenue. Although this contract is out-of-date, it demonstrated the extent to which labels hold power over Spotify while negotiating contracts.

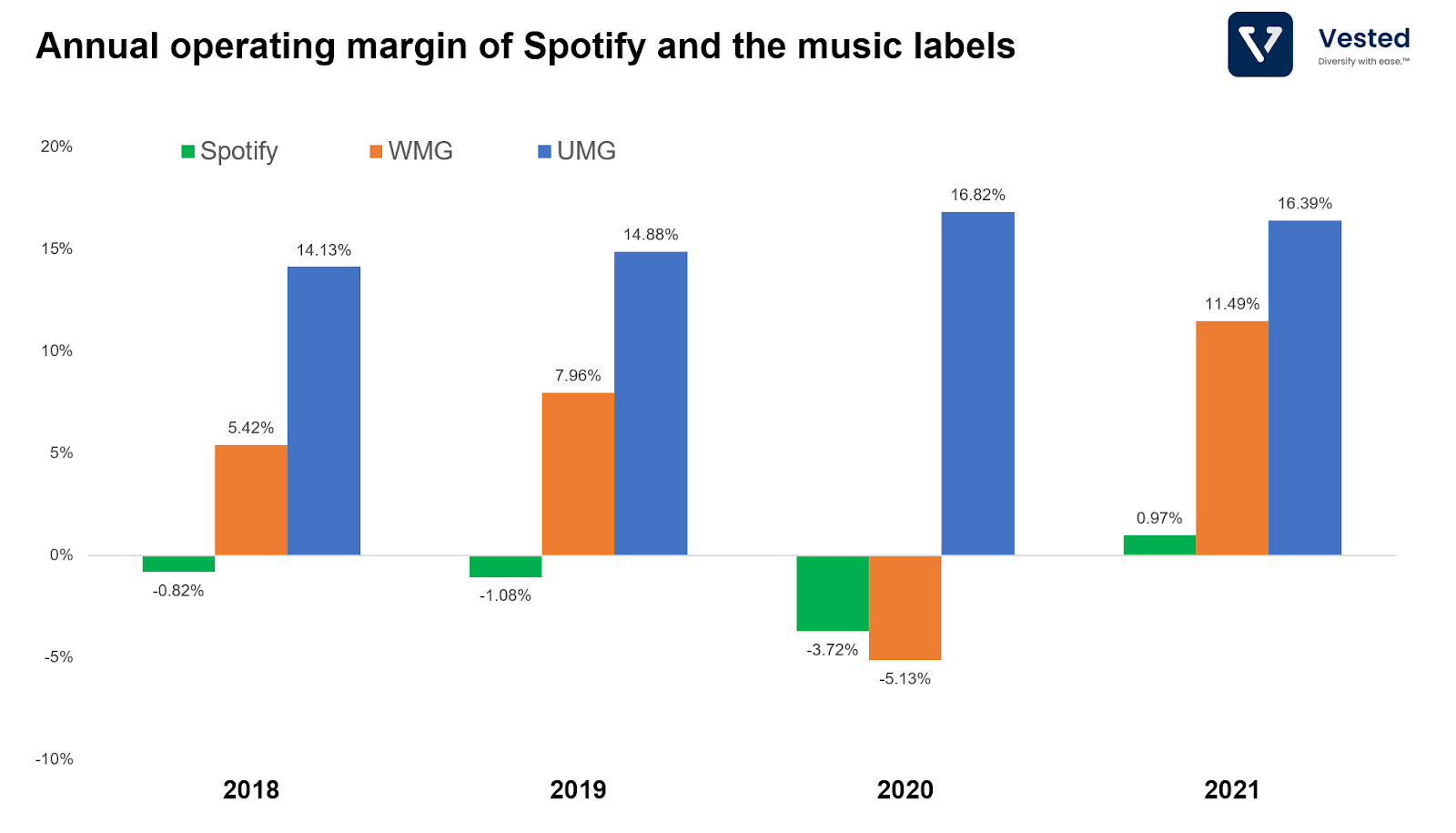

As a result, record labels take the lion’s share of the profits from music streaming. For every $1 of revenue from music streaming that Spotify takes in, $0.70 goes to the rights holders. See Figure 5 below for a comparison between Spotify’s operating margin and the two large labels (WMG and UMG).

As you can see above, Spotify has struggled with profitability (green bar). Operating margins have been historically negative for the company.

Spotify’s way out

To improve its profitability, Spotify embraces the larger mandate of becoming an audio streaming platform (expanding beyond music). The company can adopt other audio products with less stringent licensing agreements, such as podcasts, audiobooks, interactive games, and audio AI.

“From everything I see, I believe that over the next decade, we will be a company that generates $100 billion in revenue annually and achieves a 40% gross margin and a 20% operating margin.” – Daniel Ek (CEO of Spotify)

Podcasts have been a recent focus for the company. With podcasts, Spotify can create and own new shows directly (analogous to Netflix creating its shows). In the past four years, the company has invested over $1 billion in the space (acquiring podcast studios, licensing famous podcasts, buying broadcasting tools, etc.).

Spotify is trying to extract higher margin revenue from podcast ads. To do this, the company has to change the nature of podcast advertising.

Before Spotify, podcast listening was done offline. A typical podcast player on your phone helps you subscribe to an RSS feed and lets you download the audio files to listen to. This means that ad delivery is offline, too (typically, the ad is read by the host, who provides the listeners with coupon codes or unique URLs for tracking). This means the host won’t know if you skip the ads, which you likely do.

In contrast, listening to podcasts on Spotify is an online experience (by default, although premium subscribers can still download and listen offline). With Spotify, the podcast feed is streamed in real-time, and ad insertion is done programmatically. Programmatic ad delivery is important because it makes advertisements work at scale:

- If you’re an advertiser, you no longer have to build relationships with the various podcast creators or create custom URLs and coupon codes. Spotify does this for you.

- If you’re a podcast creator, especially if you’re one with a low number of listens, you can potentially start monetizing via ads inserted by Spotify. You do not have to have a relationship with advertisers. This makes it easier to get started (albeit the magnitude of monetization is probably tiny).

Spotify’s vision is to be the audio version of a self-serve advertising business a’ la Facebook. To do this, Spotify has to do two things: (i) improve podcast ad conversion and (ii) grow podcast listener base.

Improve podcast ad conversion

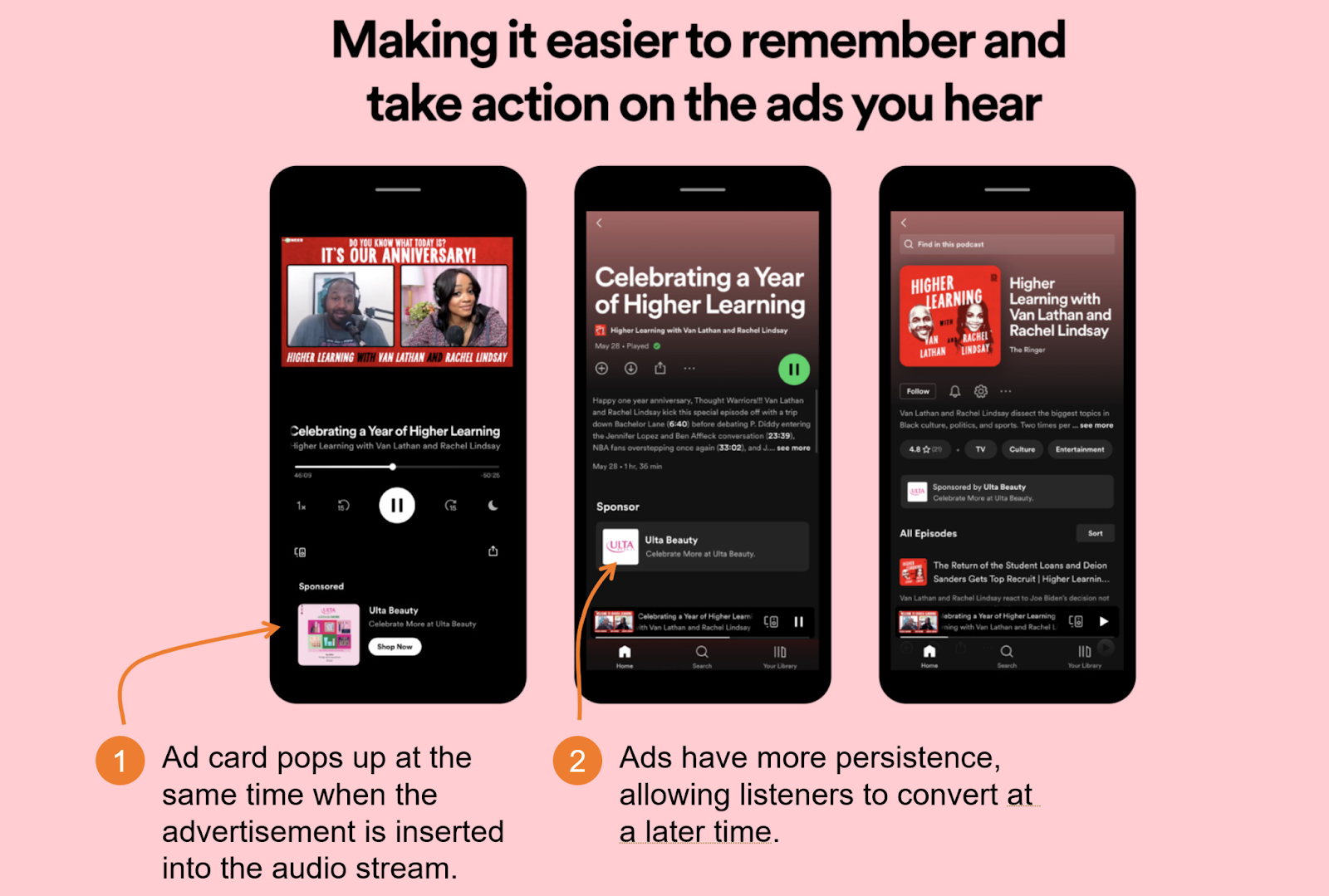

The first thing the company has to do is to improve ad conversion. Inserting ads programmatically helps solve the ad delivery problem. But to bring in more spending on advertising, Spotify has to improve the conversion of ads. Earlier this year, the company introduced a new ad format called “Call-to-Action” (CTA) cards for podcasters. These are visual ads that show up at the same time when the audio ads begin to play. They act as interactive companions for the audio ad, allowing users to bypass promo codes and URLs. These ads can also be persistent, nudging listeners to click on the ad after they listen to the ad (see Figure 6 below).

Grow podcast audience

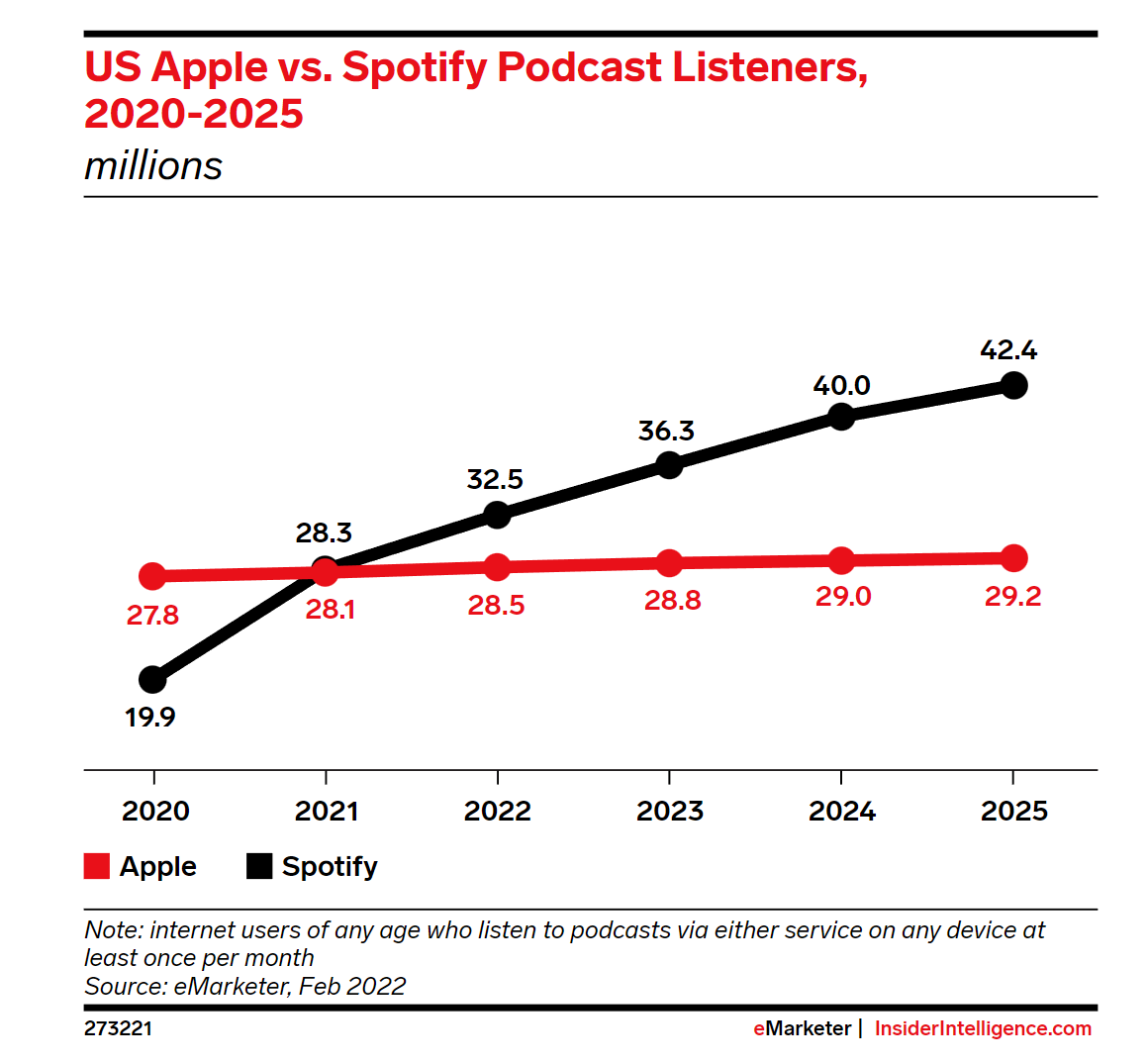

Thanks to the aforementioned investments in the space, in 2021, Spotify overtook Apple Podcasts to become the biggest podcast platform in the US. By 2025, it is projected that Spotify’s lead will widen to 45%, significantly higher than Apple’s (Apple’s growth is projected to be flat). See Figure 7 below.

However, it is not sufficient for Spotify to remain a go-to application for podcasts. The company has to be able to create and own hit shows. On this front, the company still struggles. Popular podcasts tend to be older (seven years or more), preceding Spotify’s podcast initiatives. Newer podcasts are having a hard time gaining popularity. The company’s efforts to create a hit show have so far been lackluster. Recently, the company shifted its strategy, taking a page from TV and Film by hiring podcast hosts with large social media followers.

Spotify has a long way to go on podcasts. It projects that podcasts can be gross margin positive in one to two years and be more profitable than music streaming in three to five years. In the meantime, Spotify hopes that investors continue to be patient as it works towards this goal. Unfortunately, in this environment of higher interest rates, investors’ patience is in short supply. As of this writing, Spotify has lost 68% of its value on the NYSE (compared to -31.6% for the Nasdaq).