Skip to content

Skip to content

Alphabet, Google’s parent company, has just released its third-quarter earnings, and the results are noteworthy. With strong growth in its cloud segment and continued investment in artificial intelligence (AI), Alphabet is demonstrating resilience in a competitive landscape. Here’s a closer look at what the numbers reveal.

Financial Highlights That Sparkle

Let’s start with the numbers. In Q3, Alphabet posted:

- Earnings Per Share (EPS): $2.12, outshining expectations of $1.85.

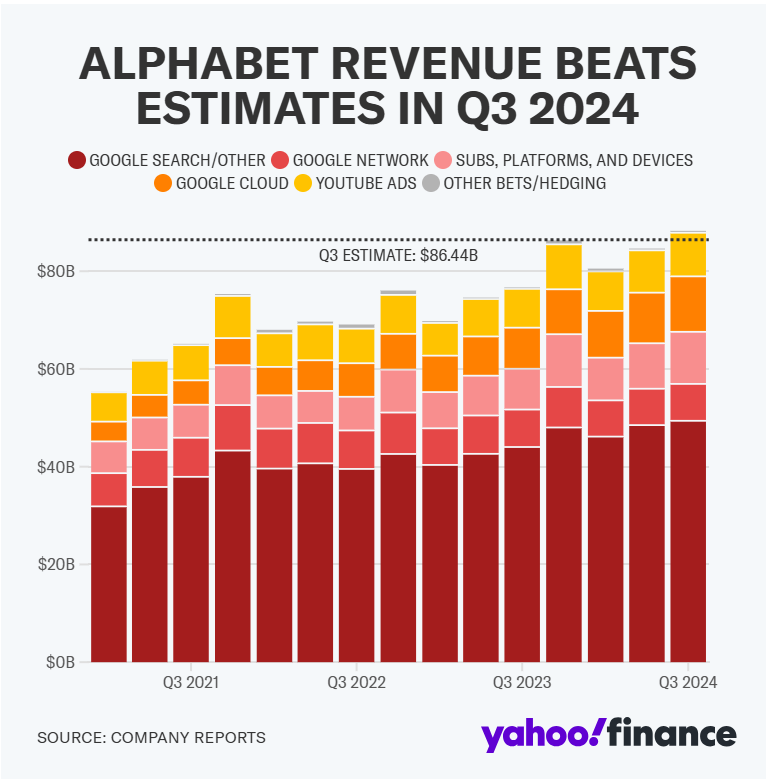

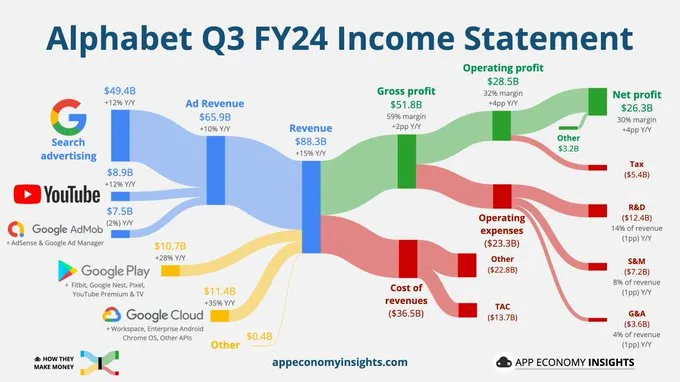

- Revenue: $88.27 billion, exceeding the anticipated $86.30 billion.

- Net Income: A robust increase to $26.3 billion, up from $19.7 billion last year.

But that’s not all. Other key figures include:

- YouTube Advertising Revenue: $8.92 billion, just above expectations of $8.89 billion.

- Google Cloud Revenue: $11.35 billion, surpassing estimates of $10.88 billion.

- Traffic Acquisition Costs (TAC): $13.72 billion, compared to expectations of $13.53 billion.

Source: Yahoo Finance

Investors were quick to react, sending shares up nearly 6% in after-hours trading, reflecting a sense of optimism about Alphabet’s performance.

Cloud Business Takes Center Stage

Alphabet’s overall revenue grew by 15% year-over-year. Yet, the true star of the show was its Google Cloud segment, which experienced a staggering 35% growth. Bringing in $11.35 billion, this marks the fastest growth in eight quarters. Companies are investing heavily in cloud services, which are crucial for powering AI technologies.

Despite this success, Google Cloud still trails behind heavyweights like Microsoft Azure and Amazon Web Services (AWS). The competition is fierce, and Alphabet will need to keep pushing forward.

Advertising Revenue Faces New Challenges

Advertising remains the heart of Alphabet’s revenue engine, contributing $65.85 billion in Q3, up from $59.65 billion a year earlier. While this reflects a 10% increase, it’s worth noting that growth has slowed compared to the previous quarter.

Google’s dominance in the digital ad market is under threat. Rivals like Amazon and TikTok are gaining ground, and advertisers are diversifying their strategies. Additionally, Alphabet is facing regulatory scrutiny, with the U.S. government considering a breakup of Google due to antitrust concerns. The European Union is also investigating Google’s market practices, adding to the pressure.

In response, Google is innovating with AI Overviews, which summarize information from multiple sources to provide concise answers to user queries. As competition heats up, this could be a crucial move to retain user engagement.

Data from eMarketer suggests that Google’s share of U.S. search advertising revenue could dip below 50% next year—marking a significant shift after nearly two decades of dominance. In contrast, Amazon’s share is projected to rise to 24%.

YouTube’s Continued Growth

YouTube remains a vital part of Alphabet’s ecosystem. The platform reported a 12% increase in revenue to $8.9 billion for the quarter. Over the past year, YouTube surpassed $50 billion in ad and subscription sales, thanks to strategic expansions into sports and partnerships with organizations like the NFL.

Heavy Investments for the Future

Alphabet’s capital expenditures rose dramatically to $13.1 billion, a 62% increase from the previous year. CFO Anat Ashkenazi indicated that these investments are primarily aimed at enhancing infrastructure—think servers, chips, data centers, and networking equipment. This trend is expected to continue into Q4, with total expenditures anticipated to exceed $50 billion for the year.

While Alphabet’s earnings are robust, challenges lurk on the horizon. AI-powered chatbots like ChatGPT and Anthropic’s Claude are reshaping user expectations and competing for search traffic. Google is responding by enhancing its AI Overviews, utilizing its Gemini models to provide direct answers rather than merely presenting links. Pichai noted that these features are gaining traction, especially for complex queries.

Navigating Regulatory Waters

Amidst this impressive performance, Alphabet faces the ongoing threat of regulatory scrutiny. The recent antitrust case highlights concerns over the company’s competitive practices, raising the possibility of significant structural changes within the business. Moreover, investigations into the Play app store and ad tech operations add layers of complexity to the competitive landscape.

Conclusion: A Balancing Act

In conclusion, Alphabet’s Q3 earnings reveal a company that is thriving despite external pressures. The cloud segment and YouTube’s growth are strong indicators of a robust business model. However, the challenges posed by competition, regulatory scrutiny, and evolving technology demand that Alphabet remains agile and innovative.

As the tech landscape continues to shift, Alphabet’s ability to adapt and invest wisely will determine its long-term success. The next few quarters will be critical as the company navigates this dynamic environment.

Disclaimer: This article draws from sources such as the Financial Times, Bloomberg, and other reputed media houses. Please note that this blog post is intended for general educational purposes only and does not serve as an offer, recommendation, or solicitation to buy or sell any securities. It may contain forward-looking statements, and actual outcomes can vary due to numerous factors. Past performance of any security does not guarantee future results. This blog is for informational purposes only. Neither the information contained herein nor any opinion expressed should be construed or deemed to be construed as solicitation or as offering advice for the purposes of the purchase or sale of any security, investment, or derivatives. The information and opinions contained in the report were considered by VF Securities, Inc. to be valid when published. Any person placing reliance on the blog does so entirely at his or her own risk and does not accept any liability as a result. Securities markets may be subject to rapid and unexpected price movements, and past performance is not necessarily an indication of future performance. Investors must undertake independent analysis with their own legal, tax, and financial advisors and reach their own conclusions regarding investment in securities markets.