Skip to content

Skip to content

Did you know there are 6548 ESOPs across U.S. companies, collectively holding total assets over $1.8 trillion!

In 2025, OpenAI closed a historic $6.6 billion employee share sale at a $500 billion valuation, giving its team one of the largest liquidity events in tech history. While Nvidia, the world’s most valuable company, has around 80% of employees who are now millionaires, thanks to long-term stock options and RSUs.

From tech firms in the U.S. to marketplaces like Urban Company in India, stock-based compensation has become one of the most powerful ways for employees to build wealth.

But behind the glorified stories of ESOPs lies a hard fact: Most employees still don’t fully understand ESOP taxation: what gets taxed, when, and at what rate.

So, if you’ve ever looked at your salary slip to see a new line, “ESOP Perquisite Value” added, and wondered why your tax suddenly spiked? You’re not alone.

In this article, we break down everything from what ESOPs are to explain how ESOP taxability affects your payout, and more.

Introduction to ESOP Taxation

Before diving into taxation, let’s recap the basics.

What is ESOP?

ESOP or Employee Stock Option Plans give employees the right, not obligation, to purchase company shares at a pre-decided exercise price after a vesting period. ESOPs are gradually becoming an important part of compensation for professionals in India and globally. And for good reason:

- They align employee performance with company goals.

- Help retain talent long-term.

- Offer lucrative opportunities beyond basic remuneration.

- Strengthen ownership culture

So, yes, while ESOPs sound like a great catch on your offer letter, ESOP taxation in India is like peeling an onion. You need to understand the rules before exercising or selling shares, or you’ll be seriously crying.

Types of Stock Options & Why Tax Treatment Differs

Taxation rules in India vary by instrument. And since not all equity compensation is tax similarly, here’s a complete breakdown to help you improve your long-term returns:

| Stock Options | Type | When You Get The Shares | Taxation Type |

| |

| ESOPs (Employee Stock Option Plans) | Right to buy company shares at a fixed ESOP exercise price after vesting | Only when exercised | Taxed as salary income as per ESOP taxation rules India | LTCG/STCG based on holding period after exercise | |

| RSUs (Restricted Stock Units) | Shares granted automatically without exercise requirement | On vesting | Salary tax at slab rate, TDS deducted by employer | Capital gains tax applies after sale | |

| ESPPs (Employee Stock Purchase Plans) | Employees buy shares at discount through payroll contribution | At purchase | Discount taxed as salary | Capital gains tax on appreciation from purchase to sale | |

| RSAs (Restricted Stock Awards) | Shares granted upfront but subject to lock-in | Immediately but restricted | FMV taxed as salary when rights fully vest | Gains taxed under capital gains after lock-in | |

| SARs (Stock Appreciation Rights) | No share allocation. Only cash equivalent of price appreciation | NA | Entire amount treated as salary income; slab rate applies | No capital gains as shares not allotted | |

| PEP (Phantom Equity Plan) | Equity-linked bonus settled in cash, values tied to share price | NA | Fully taxable as salary | No capital gains tax |

How ESOPs Are Taxed: A Step-by-Step Guide

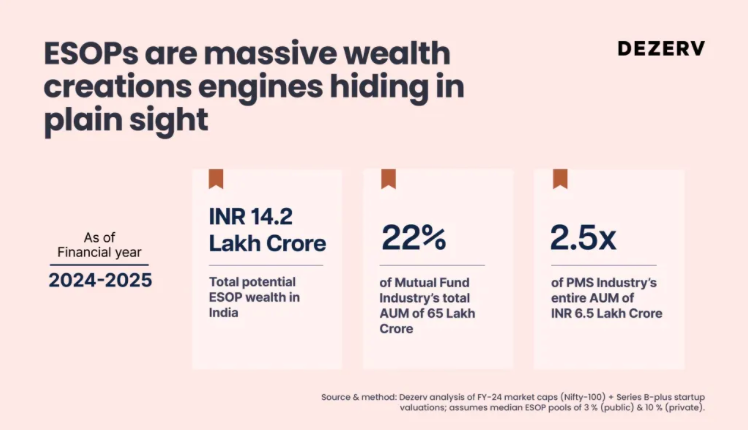

ESOP wealth in India represents ₹14.2 lakh crore, which is equal to 22% of India’s Mutual Fund Industry. So it is safe to say ESOP for employees has become an integral part of compensation today.

Here’s a step-by-step guide to decode tax on ESOP in India.

Stage 1: Tax at Exercise – ESOP Perquisite Tax

When you exercise your ESOPs, you buy shares at the exercise price.

If the Fair Market Value (FMV) is higher, the difference is considered a perquisite (salary benefit).

ESOP Perquisite Tax Formula:

| Perquisite Value = (FMV on Exercise Date – ESOP Exercise Price) × Number of Shares |

This value is added to your salary income and taxed at your income slab rate. When this happens, you owe tax without even selling your shares. Even if the shares are unlisted or illiquid, tax must be paid immediately.

Stage 2: Tax at Sale – ESOP Capital Gains Tax

When you sell the shares, capital gains tax is levied. Your purchase price for capital gains is not the exercise price. It is the FMV on the date of exercise, because you already paid tax on the perquisite.

Capital Gains Formula:

| Sale Price – FMV on Exercise Date |

Holding Period Rules:

| Holding Period | Type of Gain | Tax Rate | |

| Listed Shares | Less than 12 months | STCG | 20% |

| More than 12 months | LTCG | 12.5% (if gains exceed ₹1.25 lakh) |

*Note for Unlisted Shares: STCG on shares held for less than 24 months is taxed at the listed income-tax slab rate. LTCG on shares held for more than 24 months is taxed at 12.5% without indexation.

TDS on ESOPs: The Employer’s Role and Your Responsibilities

Under the ESOP taxation rules in India, employers must deduct a 30% TDS at exercise.

Employer Responsibilities

- Calculate TDS accurately on the perquisite value under Section 17(2) of the Income Tax Act 1961.

- Deduct TDS and file returns (Form 24Q)

- Issuing Form 16/12BA as proof of tax deduction.

Employee Responsibilities

- Provide accurate income details to the employer.

- Understand tax impact and keep adequate money in hand. If you fall short, exercise a ‘sell-to-cover’ transaction where a portion of the shares is sold to cover taxes due.

- Verify Form 16 with the employer where the TDS deducted is mentioned.

- File ITR with the correct ESOP value to claim TDS as credit.

This is where many employees face liquidity stress because they need cash to pay taxes even before receiving any money from ESOPs.

Special Scenario: ESOP Tax Deferral for Eligible Startups

Usually, when your ESOPs vest and you exercise them, the difference between the Fair Market Value (FMV) and your exercise price becomes taxable immediately as a perquisite under salary.

The challenge? Many employees haven’t sold their shares yet, so they are paying tax on something they haven’t earned in cash. This creates a financial burden.

To boost entrepreneurship and ease this burden for start-up employees, the Government of India introduced a special ESOP tax deferral under Section 80-IAC. Eligible DPIIT- recognised startup employees do not have to immediately pay tax when they exercise ESOPs.

So, when does the ESOP tax finally have to be paid?

You (or your employer via TDS) will pay tax whichever of the following happens first:

- When you decide to sell your ESOP shares.

- Even if you hold shares, tax becomes due after 4 years (48 months).

- If you leave the organisation, tax must still be paid even if you haven’t sold the shares.

For startup employees, ESOPs can unlock substantial wealth, but upfront tax can make exercising unaffordable. This deferral rule gives employees more time to benefit from long-term equity holding.

Cross-Border & NRI ESOP Taxation

ESOP taxation gets more complex in multinational environments. Here’s what you need to know:

Indian Corporate Law allows Indian businesses to offer ESOPs to their employees outside India. So, if you receive US stock options (e.g., Google, Microsoft, Amazon), exercising them will trigger taxation on receipt.

- Same tax treatment as residents

- But additional FEMA and repatriation requirements

- Gains will be taxed in India, subject to exemption under the relevant tax treaty.

- TCS/TDS rules may apply

In a cross-border scenario, the right to ESOP benefits can be earned for services outside India, and the income accrued is outside the country. However, since the shares are of an Indian company, claiming exemption benefits will be under the Double Taxation Avoidance Agreement treaty (DTAA).

- Salary income is taxable in the country of employment, and an exemption is applicable under the ‘Dependent Personal Services’ article.

- A Tax Residency Certificate is necessary to claim the DPS exemption.

- The sale of foreign shares is treated as capital gains tax in India.

- DTAA can offset double taxation. Like India may tax on exercise, while others may tax during the vesting period.

- However, the Foreign Tax Credit (FTC) can be claimed in the country of residence depending on domestic tax laws.

Common ESOP Tax Traps & How to Avoid Them

An ESOP for employees can be a powerful tool for wealth creation. But before you get swept up in the excitement, here are 5 ESOP tax traps and how you can avoid them.

- Exercising Too Early (When FMV is High)

If you rush to exercise ESOPs the moment they vest because it’s the fastest route to ownership, wait. Exercising when the Fair Market Value (FMV) is high immediately triggers perquisite taxation, even if you haven’t earned a rupee from the shares yet. You end up paying a large tax bill before you have any liquidity.

Only exercise early if:

- You have visibility on an exit event (IPO, buyback, secondary sale), or

- The company offers cashless exercise options, reducing out-of-pocket costs.

- Owning Shares but No Liquidity to Pay Taxes

This is one of the most painful real-world ESOP experiences. Employees exercise shares, but the company remains private. The result? You hold valuable equity on paper but have no way to sell, while the tax department still expects payment.

Always check:

- Check your employer’s liquidity history.

- Ask HR whether a cashless exercise is available.

- Cost of Acquisition

Did you know that FMV at the time of exercise becomes your cost of acquisition? This cost directly affects your capital gains tax when you sell. An incorrect FMV certificate may add to your tax burden.

What you should do:

- Maintain FMV certificates

- Keep every vesting, exercise document, contract, and payment proof.

- Surcharge + Cess

If you’re a high-income earner, remember to add two important additional taxes! Surcharge (up to 37%) and 4% health & education cess. Calculating your tax based on your slab rate may lead to a huge discrepancy.

So before exercising or selling ESOPs, calculate:

- Base tax

- Applicable surcharge

- Cess

- Residency Status

If your ESOPs come from a global company or you work cross-border, taxation may apply in more than one country. Residency laws determine where your ESOP income is taxed, and misreporting can lead to double taxation.

What you should do:

- Refer to DTAA (Double Tax Avoidance Agreement) if applicable.

- Consult a tax expert before exercising cross-border equity.

How to Legally Reduce Tax on ESOPs in India

ESOPs can significantly add to your wealth, but taxes can take a huge part away, too. So here are some smart ESOP tax hacks you need to know in 2025:

1.Time Your Sale

You qualify for Long Term Capital Gains when you hold your ESOPs for 12 months. In India, LTCG is taxed at 12.5% as compared to 20% for STCG.

2. Tax Deferral Benefit

If you are an employee of a recognised startup under Section 80-IAC, you can use the tax deferral benefit to your advantage. This reduces immediate financial burden, allowing you to plan long-term payments.

3. Invest Capital Gains in Residential Property

Under Section 54F, you are eligible to reinvest gains from the sale of your ESOPs in a residential property. While it may not completely eliminate ESOP capital gains tax, it can reduce your financial burden, depending on current tax laws.

4. Invest in Capital Gain Bonds

If your ESOP gains qualify as LTCG, you can invest in 54EC Bonds such as NHAI or REC within 6 months. Your investment will have a 5-year lock-in period.

5. Sales Over Fiscal Years

You can manage your ESOP taxability by gradually selling shares over the years. This helps reduce your capital gains in a single year from crossing the exemption levels. Additionally, if you have other investment losses from stock trading or ETFs in a year, you can set them off against ESOP capital gains to reduce your overall tax burden.

How to Report ESOP Income in Your ITR

Reporting ESOPs while filing your Income Tax Return (ITR) can seem confusing because tax on ESOP in India is levied at two different stages. First, as salary income (when you exercise your options) and later as capital gains (when you sell the shares). Here’s a clear breakdown of how to file it correctly:

- ESOP Related Documents

Before you begin filing, keep the following details ready:

- Grant & Exercise Dates

- Exercise Price

- Fair Market Value (FMV) on Exercise Date

- Sale Price & Sale Date

- Broker Statements & Contract Notes

- Report ESOP Perquisite Under Salary Income

When you exercise your ESOPs, the difference between FMV and Exercise Price becomes taxable as salary.

You must report this under Income from Salary → Perquisites (ESOPs). This amount will also reflect in your Form 16and Form 26AS if your employer has deducted TDS.

- Report ESOP Sale Proceeds Under Capital Gains

If you sell the shares after exercising, the gain from that sale must be reported separately. You will file this under Schedule – Capital Gains in your ITR form.

- Verify Details

Open Form 26AS / AIS / TIS to ensure that:

- ESOP perquisite value matches the salary entry

- TDS deducted by the employer is correctly reflected

- No mismatch exists in reported transaction values.

- File & Submit Your ITR

Once salary income and capital gains are correctly entered, submit the ITR.

Conclusion

ESOPs can create wealth, but only when you understand how they’re taxed.

ESOP perquisite tax, capital gains on sale, FMV valuation, slab rates; each decision affects how much you actually take home. A smart approach to exercising, selling, and planning deductions can mean the difference between compounding wealth and losing it to tax outflows.

By carefully understanding ESOP taxation rules in India, you can make more informed financial choices for your future.

Frequently Asked Questions

What is ESOP?

ESOP stands for Employee Stock Option Plan, a benefit that allows employees to purchase company shares at a predetermined price.

How is ESOP taxed in India?

ESOPs in India are taxed at two stages:

- Perquisite tax at exercise (salary income)

- Capital gains tax at sale

What is ESOP perquisite tax?

Tax on FMV minus exercise price, taxed as salary is also known as ESOP perquisite tax.

What is ESOP capital gains tax?

Tax on gains after the sale of shares is capital gains. If you hold them for less than 12 months, they are known as short term capital gains taxed at 20%. Holding them for more than 12 months qualifies you for long term capital gains, which is taxed at 12.5%, if gains exceed ₹1.25 lakh.

Can ESOP tax be deferred?

Yes it can. Employees of DPIIT-recognised startups can defer ESOP tax for 4 years or until sale/resignation. Since it is calculated from the end of the relevant assessment year, you can benefit from a deferral period of 5 years from your year of exercise.