Skip to content

Skip to content

For the past decade, Wall Street played second fiddle.

Silicon Valley was where the money, magic, and memes lived. Tech moguls became demigods. Investors couldn’t get enough of cloud, SaaS, AI, and everything in between. Meanwhile, America’s biggest banks were busy scrubbing off the 2008 hangover, navigating new regulations, and rebuilding trust.

But something shifted in 2025.

As markets whipsaw in Trump’s second term, with new tariffs, surprise tax bills, and fiscal fireworks — Wall Street seemingly isn’t just weathering the storm.

It appears to be thriving in it.

The second-quarter earnings season for America’s largest banks may just have revealed a quiet truth: in a world of uncertainty, finance seems to be back in fashion, not with swagger or spectacle, but with a steady reminder that the boring guys may still know how to make money when things get messy.

Let’s unpack why the Street is smiling again — and what that means for the economy.

What Just Happened?

Let’s start with JPMorgan, the heavyweight of American finance.

Yes, its Q2 earnings technically fell 17% from last year. But that’s only because last year included an $8 billion windfall from its Visa shares. Strip that out, and the numbers are far more impressive:

- Net income: $14.9 billion

- Earnings per share: $5.24 (vs. $4.48 expected)

- Revenue: $45.7 billion (vs. $44 billion expected)

What drove the surprise?

Trading and investment banking.

- Fixed income trading revenue surged 14%

- Equities trading jumped 15%

- Investment banking fees rose 7%, defying gloomy predictions

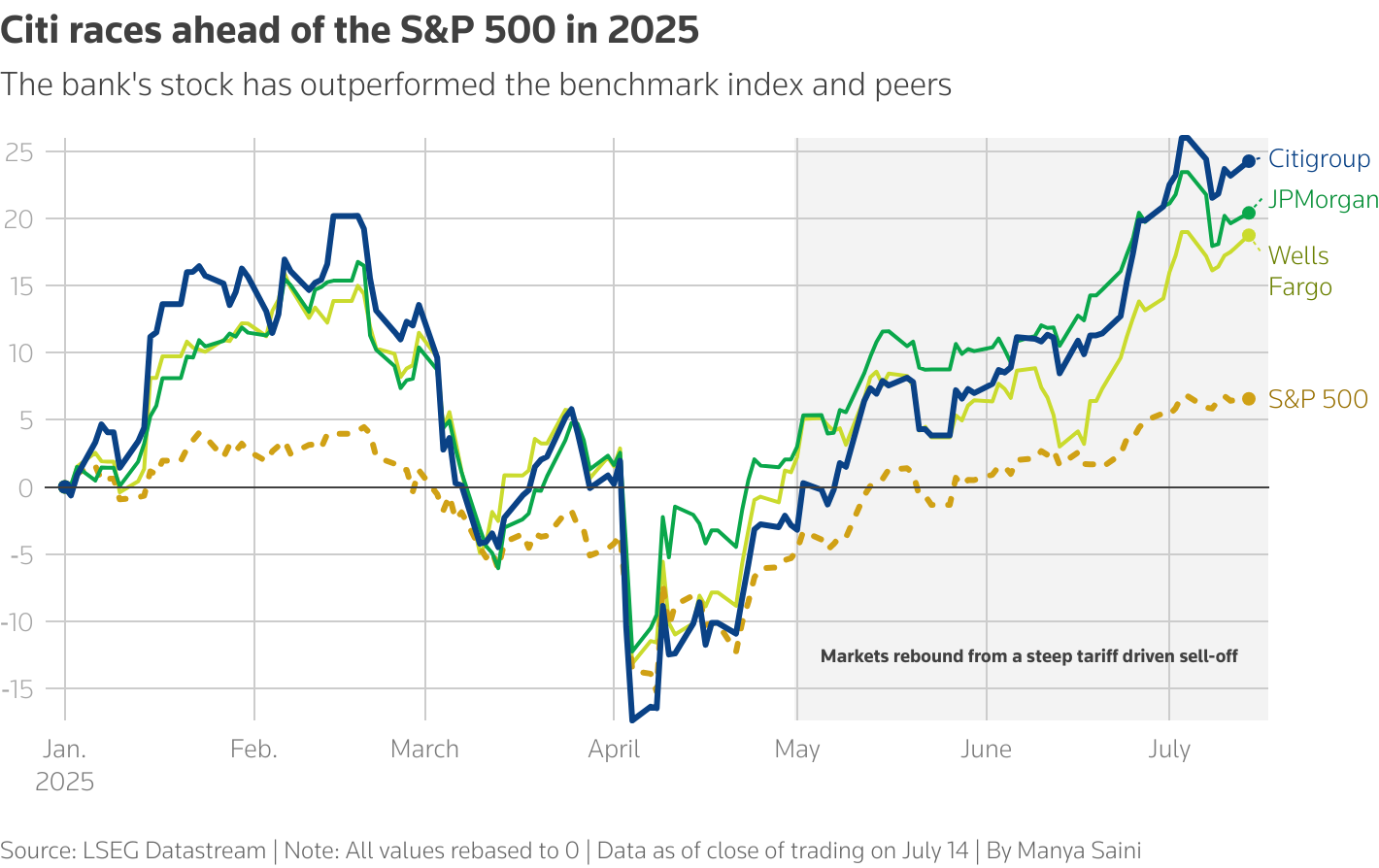

It’s a similar story over at Citigroup, which some consider the underachiever of the Big Four banks. But this quarter, Citi surprised everyone:

- Net income rose 25% to $4.02 billion

- Revenue grew 8% to $21.7 billion

- Trading revenue rose 16%

- M&A advisory fees surged 52%

- And it announced a $4 billion share buyback

Meanwhile, Wells Fargo, freshly freed from a 7-year regulatory asset cap, posted strong numbers too:

- Net income of $5.49 billion (up 12%)

- EPS of $1.60 beat expectations

- Advisory fees rose 9%

All three banks beat expectations. But that’s not the real story.

The real story is that they beat expectations in a quarter filled with chaos.

Why Chaos is Profitable

Let’s back up.

Ever since Trump returned to office, markets have been in turmoil. His sudden “Liberation Day” tariffs in April, followed by a sweeping $3 trillion tax-and-spending bill, seemed to have caught investors off guard.

The U.S. dollar wobbled. Treasury yields spiked. Stocks swung wildly.

For most companies, this kind of uncertainty would be a nightmare. CEOs pause hiring. CFOs freeze spending. Consumers tend to grow cautious.

But for big banks?

This is prime time.

Because volatility = volume.

Every rate shock, tariff tweak, or FX swing is usually trigger for clients to reposition portfolios, hedge risks, issue debt, or seek advice on deals. And banks get paid for all of it — through trading spreads, underwriting fees, and advisory services.

Even JPMorgan — known as the most cautious voice on Wall Street — seemed unusually optimistic this quarter. CEO Jamie Dimon called the U.S. economy “resilient” and noted that tax reform and potential deregulation were tailwinds.

From Fixing to Flexing

Two banks, in particular, appear to be shedding their “work-in-progress” label: Citigroup and Wells Fargo.

Citi has been in restructuring mode for years — exiting underperforming global markets, fixing its compliance systems, and trying to reclaim relevance. But this quarter may have been different.

It seemed confident. Competitive. Capable of chasing — and winning — big-ticket deals.

Fraser confirmed that Citi is now advising on 7 of the 10 largest M&A transactions of the year, including the $21.9 billion Charter-Cox deal and Circle’s IPO.

Wells Fargo, meanwhile, has been stuck under a Federal Reserve-imposed asset cap since 2018 due to its fake accounts scandal. That cap was lifted in June. Now, it’s free to grow again.

CEO Charlie Scharf didn’t mince words:

“We now have the opportunity to grow in ways we could not while the asset cap was in place.”

And it’s showing up in the numbers. Wells beat estimates, posted strong credit metrics, and it finally looks as if it is getting investor interest again.

But What About the King of Asset Management?

While banks were basking in volatility, BlackRock — the world’s largest asset manager — had a more complicated quarter.

On the surface, it looked strong:

- Assets under management (AUM) hit a record $12.53 trillion

- Net income jumped to $1.88 billion

- Technology revenue rose 26%, thanks to its Preqin acquisition

But despite all that, BlackRock’s stock fell over 5%.

Why?

Because a massive $52 billion outflow from one Asian institutional client spooked the Street. That dragged long-term net inflows down to $46 billion — lower than expected. Performance fees dropped 42%, and retail equity inflows also slowed.

Unlike banks, BlackRock doesn’t profit from market chaos. It earns most of its fees as a percentage of assets under management. When markets swing too hard or clients get nervous, inflows suffer — and so does revenue.

So BlackRock is evolving.

CEO Larry Fink remarked that they are pivoting away from low-fee passive products toward:

- Private markets (which have higher margins)

- Tech platforms like Aladdin

- Retirement solutions that promise stable, recurring revenue

He expects these areas to account for 30%+ of total revenue by 2030, up from 15% today.

It may be a smart strategy — but it also shows that scale alone is no longer enough. Generally, you need pricing power and resilience too.

The Bigger Picture

This earnings season wasn’t just about banks beating forecasts. It was about what kind of world we live in now — and who benefits from it.

For the past decade, many people believed that the tech sector reigned supreme. It was built on:

- Predictable policy

- Low interest rates

- Globalization

- Optimism

But in today’s Trump-era America, the rules seemed to have changed:

- Trade is unpredictable

- Inflation is sticky

- Fiscal deficits are ballooning

- Markets are jittery

And that kind of world? It would play to Wall Street’s strengths.

Banks with strong trading desks, diversified revenues, and solid balance sheets don’t just survive — they monetize the mayhem.

So, What Does This Mean for You?

If you’re an investor, it may be time to rethink old assumptions.

Big banks were often seen as boring, overly regulated, and underperforming. But this quarter proved they can be dynamic, profitable, and well-positioned for a chaotic macro environment.

If you’re a policymaker, this is a cautionary tale. Every surprise policy move — every tariff, tax tweak, or spending spree — has ripple effects. And those ripples could be revenue streams for financial giants.

And if you’re just watching from the sidelines?

Know this:

Wall Street isn’t just surviving Trump 2.0, — it may have learned how to thrive in it.

The Bottom Line

JPMorgan. Citi. Wells Fargo. BlackRock.

Together, they’ve shown that Wall Street isn’t just alive — it’s adaptable. Whether it’s trading volatility, M&A recovery, or pivoting to tech and private markets, finance may have just reclaimed its seat at the economic table.

While tech continues to dominate the headlines, it’s the banks that might just be making sense — and money — out of the madness.

And in a world that’s getting messier by the day, that’s worth paying attention to.

Disclaimer – This article draws from sources such as the Financial Times, Bloomberg, CNBC, Reuters and other reputed media houses. Please note, this blog post is intended for general educational purposes only and does not serve as an offer, recommendation, or solicitation to buy or sell any securities. It may contain forward-looking statements, and actual outcomes can vary due to numerous factors. Past performance of any security does not guarantee future results.This blog is for informational purposes only. Neither the information contained herein, nor any opinion expressed, should be construed or deemed to be construed as solicitation or as offering advice for the purposes of the purchase or sale of any security, investment, or derivatives.The information and opinions contained in the report were considered by VF Securities, Inc.to be valid when published. Any person placing reliance on the blog does so entirely at his or her own risk, and does not accept any liability as a result.Securities markets may be subject to rapid and unexpected price movements, and past performance is not necessarily an indication of future performance. Investors must undertake independent analysis with their own legal, tax, and financial advisors and reach their own conclusions regarding investment in securities markets.Past performance is not a guarantee of future results