Skip to content

Skip to content

Picture this: You want to buy a car worth ₹10 lakhs, but you don’t have the money. So the car dealer says, “No problem! I’ll lend you the money to buy the car from me.” Sounds convenient, right? But also a bit… circular?

Well, that’s essentially what’s happening in the AI industry right now, except we’re not talking about ₹10 lakhs. We’re talking about a trillion dollars.

And the craziest part? These deals have already added over $1 trillion to the market capitalizations of the companies involved. Let’s break down this financial merry-go-round.

The OpenAI Spending Spree

OpenAI, the company behind ChatGPT, has been on an tear recently. In 2025 alone, it’s signed deals worth roughly $1 trillion for computing power. Yes, you read that right. A trillion dollars.

To put that in perspective, OpenAI is valued at around $500 billion but generated only about $4.3 billion in revenue in the first half of last year while burning through $2.5 billion. So a company that’s losing money is committing to spending that could power 20 nuclear reactors worth of computing capacity.

But here’s where it gets interesting. These aren’t normal business deals. They’re more like a financial Ouroboros—the mythical snake eating its own tail.

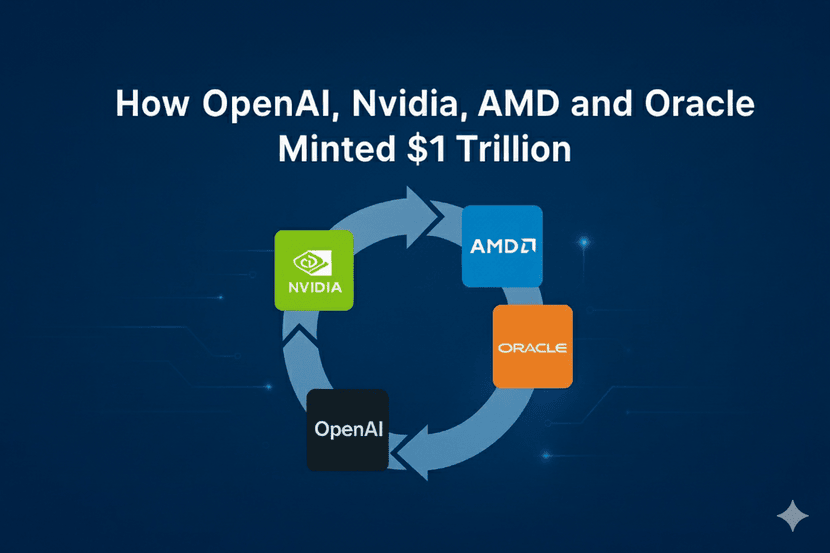

The Nvidia Deal: A Masterclass in Circular Finance

Let’s start with the Nvidia arrangement. OpenAI needs chips—lots of them—to run its AI models. Nvidia makes the best AI chips in the world. Simple buyer-seller relationship, right?

Not quite.

Source: CNBC

Under this deal, OpenAI will pay Nvidia up to $100 billion for chips. But here’s the twist: Nvidia will also invest up to $100 billion in OpenAI over the next decade. So essentially, Nvidia is giving OpenAI money that OpenAI will then use to… buy Nvidia’s chips.

It’s like your local grocery store lending you money every week so you can shop there. Convenient for you, great for their sales numbers, but you have to wonder—is the demand real, or is it just artificially propped up?

When the deal was announced, Nvidia’s already stratospheric valuation climbed even higher. Investors appeared to loved it. After all, it’s a $100 billion chip order! Except, well, Nvidia is also footing the bill for that order.

The AMD Twist

Just when you thought it couldn’t get more circular, OpenAI signed another deal with AMD, Nvidia’s direct competitor. This one might be even more creative.

OpenAI agreed to buy AMD chips worth potentially over $300 billion. In exchange, AMD is giving OpenAI warrants to buy up to 10% of the company for just one cent per share. When the deal was announced, AMD’s shares were trading at around $204.

Think about this structure for a moment. If AMD’s stock price keeps rising, OpenAI can exercise those warrants, sell the shares, and use that money to… you guessed it, buy more AMD chips. It’s a self-funding purchase agreement.

The market’s reaction? AMD’s stock jumped 24% in a single day, adding about $63 billion to its market value. Investors seemed to be euphoric about the massive order. But scratch beneath the surface, and you see OpenAI isn’t exactly writing a traditional check here.

The Oracle Connection

But wait, there’s more! OpenAI also has a deal with Oracle worth around $300 billion for cloud computing services. When that deal was announced, Oracle’s market value jumped by $244 billion in a single day.

And here’s where the web gets really tangled: Oracle is buying chips from Nvidia to build data centers for OpenAI. So OpenAI’s money goes to Oracle, which goes to Nvidia, which invests back in OpenAI. It’s a circular loop that could make an economist’s head spin.

The $1 Trillion Market Cap Magic Trick

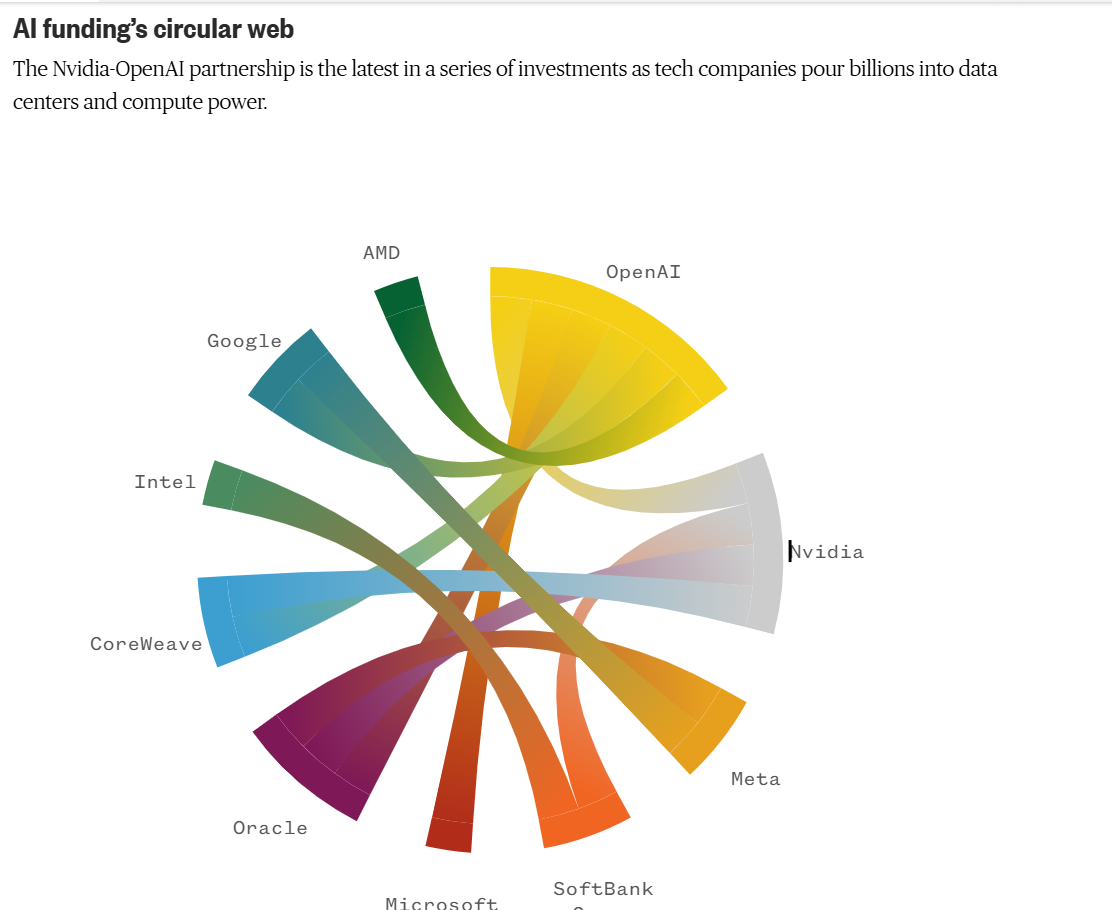

Here’s the truly remarkable part: these deals have collectively added over $1 trillion to the market capitalizations of the companies involved.

AMD gained $63 billion in a day. Oracle jumped $244 billion in a single day. Nvidia’s valuation has soared past $4 trillion in 2025. When you add it all up, these announcements have created paper wealth that dwarfs the actual revenue or profits of most companies involved.

But is it real growth, or is it a mirage created by companies essentially passing money between themselves?

Why Everyone’s Worried About 2000

If you were paying attention during the dot-com bubble, this all might sound eerily familiar. Back in 1999-2000, telecom equipment suppliers used to finance their customers’ purchases through elaborate arrangements. Those customers would then use that financing to buy more equipment, creating the illusion of booming demand.

When reality finally caught up, the Nasdaq crashed 77% between March 2000 and October 2004, wiping out trillions in market value. It took 15 years to reclaim its previous high.

Jim Chanos, a famous short-seller, put it perfectly: “Don’t you think it’s a bit odd that when the narrative is ‘demand for compute is infinite,’ the sellers keep subsidizing the buyers?”

British tech investor James Anderson echoed this concern, saying these deals have “certain rhymes” to the vendor financing schemes of the dot-com era.

The Bull Case: Why This Time Might Be Different

Not everyone is hitting the panic button, though. Bulls argue there are key differences between now and 2000:

First, much of the spending is coming from tech giants like Microsoft, Google, Amazon, and Meta—companies with massive free cash flow and proven business models. They’re not burning through venture capital like the dot-com startups were.

Second, AI adoption is real. ChatGPT now has 800 million weekly users, up from 500 million just months earlier. That’s actual usage, not just hype.

Third, these companies have to spend. Sam Altman, OpenAI’s CEO, says the path to artificial general intelligence requires massive compute power. If they don’t invest now, competitors will.

And crucially, the “Magnificent Seven” tech stocks—Apple, Google, Amazon, Meta, Microsoft, Nvidia, and Tesla—now represent over 35% of the entire S&P 500’s market value, more than $20 trillion. These aren’t speculative startups. They appear to be the backbone of the modern economy.

The Bear Case: Math That Doesn’t Math

But skeptics point out some uncomfortable arithmetic. OpenAI is currently losing about $10 billion a year. It’s committed to spending $1 trillion over the next decade. Even if revenue grows dramatically, can it possibly generate enough profit to service these obligations?

Gil Luria, an analyst at D.A. Davidson, was blunt: “OpenAI is in no position to make any of these commitments.”

There’s also the question of what happens if AI adoption slows down. What if companies realize they’re not getting good returns on their AI investments? An MIT study found that 95% of organizations are getting zero return from their generative AI investments. McKinsey reported that eight out of ten companies see no significant bottom-line impact from AI.

If the AI productivity revolution fails to materialize, or even just gets delayed, the house of cards could tumble quickly.

The Bottom Line

What we’re witnessing might be the largest coordinated investment boom in tech history. Or it might be an elaborate game of musical chairs where everyone’s wealth depends on everyone else continuing to play.

The truth is probably somewhere in between. AI seems to be real, and it might be transformative. But the circular financing structures being used to fund this boom should give investors pause. When sellers have to subsidize buyers, and when deals add hundreds of billions in market value despite questionable unit economics, you have to wonder if we’re building on solid ground or quicksand.

Sam Altman says profitability isn’t in his “top-10 concerns” right now. For investors who’ve watched their portfolios swell by a trillion dollars on the back of these deals, maybe it should be.

Because history appears to have taught us one thing: in financial markets, circular arrangements eventually become vicious cycles. The only question is when.

Image Source – Gemini