Skip to content

Skip to content

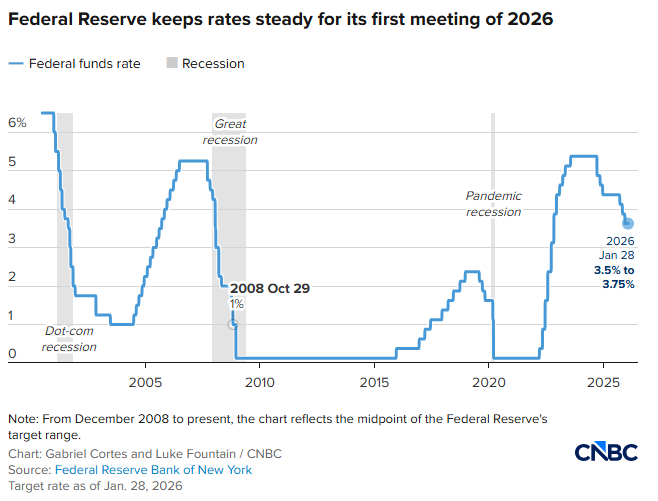

The Federal Reserve just did something interesting. After cutting interest rates three times in a row last fall, they’ve decided to stop. No more cuts. Not now, at least.

On Wednesday, the Fed kept rates steady at 3.5% to 3.75%. And if you’re wondering why this matters, well, it tells us a lot about where the American economy is headed and what’s brewing behind the scenes at the central bank.

The Story So Far

Let’s rewind a bit. Just a few months ago, the Fed was worried. The job market looked shaky. Hiring was slowing down. People were nervous that a recession might be lurking around the corner.

So what did they do? They cut interest rates. Three times in a row, actually. September, October, November. Each time, a quarter of a percentage point came off. The idea was simple: make borrowing cheaper, encourage businesses to hire, keep the economy humming along.

Fast forward to now, and the picture looks different. Fed Chair Jerome Powell stood at his podium Wednesday and delivered what was essentially good news. The economy has improved. The job market is stabilizing. Growth is looking solid. The unemployment rate even dropped to 4.4% in December.

Translation: The emergency is over. Time to take a breather.

But Wait, There’s a Catch

While the Fed voted 10 to 2 to keep rates steady, those two dissenting votes are worth paying attention to. Governors Stephen Miran and Christopher Waller both wanted another rate cut.

Now, Waller is one of four people on President Trump’s shortlist to replace Powell when his term ends in May. And Miran? He’s actually on leave from his day job as a top economic adviser to Trump. See the pattern here?

Trump has been exceptionally vocal about wanting lower interest rates. He believes they’re essential to supercharge the economy. The Justice Department even launched a criminal investigation into Powell earlier this month, though it’s officially about renovations at the Fed’s headquarters. Most people see it as a pressure tactic to influence monetary policy.

Powell, to his credit, hasn’t flinched. When asked about the investigation, he said it’s an attempt to grab control over interest rates through intimidation. He’s defending the Fed’s independence like his professional life depends on it, because, well, it kind of does.

The Inflation Problem

Here’s the uncomfortable truth: inflation is still running hot. The Fed’s favorite inflation gauge ended 2025 at around 3%, a full percentage point above their 2% target. That’s a problem.

Powell tried to spin this positively, saying the story was modestly positive. He pointed out that most of the price increases were in goods, which he blamed on tariffs. We think those will not result in inflation, as opposed to a one time price increase, he explained.

But here’s the thing about inflation. It’s sticky. Once prices go up, they rarely come back down. They might stop rising as fast, but that doesn’t mean your grocery bill gets cheaper. It just means it stops getting more expensive at the same rate.

What This Means for You

If you’re hoping for cheaper mortgages or personal loans anytime soon, don’t hold your breath. The futures markets aren’t expecting any rate cuts until at least June, and by then, Powell will likely be gone, replaced by someone Trump picks.

For businesses, this means borrowing costs stay elevated. That factory expansion you’re planning? The interest on that loan isn’t getting cheaper anytime soon. For savers, though, it’s not all bad news. Your savings accounts and fixed deposits will keep earning decent returns for a while longer.

The stock market? It barely reacted. The S&P 500 stayed flat around 7,000 points. Bond yields held steady at about 4.25%. Markets had already priced this in. They saw it coming from a mile away.

The Balancing Act

What’s fascinating about this moment is what it reveals about the delicate balance the Fed is trying to strike. On one hand, they want to support the economy and keep people employed. On the other, they can’t let inflation run wild.

Right now, they think they’ve found the sweet spot. The economy is growing at a healthy clip. GDP grew 4.4% in the third quarter and is tracking at 5.4% for the final quarter of 2025. Unemployment is low. People are finding jobs.

But inflation hasn’t fully cooperated with the plan. It’s coming down, just not fast enough. And Trump’s tariffs, which he imposed on imported goods last year, are adding to the price pressures, at least in the short term.

The Leadership Drama

Perhaps the most intriguing subplot here is the leadership transition. Powell has just two more meetings left as chair before his term expires in May. When asked if he’d decided whether to stay on as a governor after stepping down as chair, he simply said no and declined to elaborate.

It’s a loaded question. Staying on means potentially serving under someone Trump picks, someone who might have very different views about monetary policy. Leaving means walking away from one of the most influential economic positions in the world.

Powell did offer some advice for his successor: Don’t get pulled into elected politics. It’s advice born from experience. His tenure has been marked by constant battles with Trump over rate policy. The president has called him everything from pathetic to clueless for not cutting rates fast enough.

Powell also attended a Supreme Court hearing last week about Trump’s attempt to fire Fed Governor Lisa Cook. That case is perhaps the most important legal case in the Fed’s 113 year history, he said. The outcome could fundamentally reshape how much control presidents have over the Fed.

What Happens Next?

The Fed’s message is clear: they’re in wait and see mode. They’re not committing to anything. As Powell put it, we’re not trying to articulate a test when to next cut, or whether to cut at the next meeting.

They’ll watch the data. They’ll monitor inflation. They’ll keep an eye on the job market. And when they see enough evidence that it’s safe to cut rates again, or necessary to raise them, they’ll act.

But there’s a political dimension to all this that’s hard to ignore. Once Powell’s replacement takes over, the dynamics could shift dramatically. If Trump appoints someone more sympathetic to his views on monetary policy, we could see a more aggressive push toward lower rates, regardless of what inflation is doing.