Skip to content

Skip to content

Remember when tech stocks could do no wrong? When every quarterly earnings report from Apple, Microsoft, or Google felt like a guaranteed market rally? Well, those days might be coming to an end. The so-called “Magnificent 7” – the seven tech titans that have been carrying the entire stock market on their shoulders – are showing signs that their meteoric growth trajectory is finally hitting some turbulence.

The Party’s Still On, But the Music’s Getting Quieter

Don’t get us wrong – these companies are still absolute powerhouses. The Magnificent 7 (Apple, Microsoft, Alphabet, Amazon, Meta, Tesla, and NVIDIA) currently make up a staggering 31% of the entire S&P 500’s market capitalization. That’s nearly one-third of America’s largest companies represented by just seven stocks. It’s a level of market concentration we haven’t seen since the dot-com bubble days.

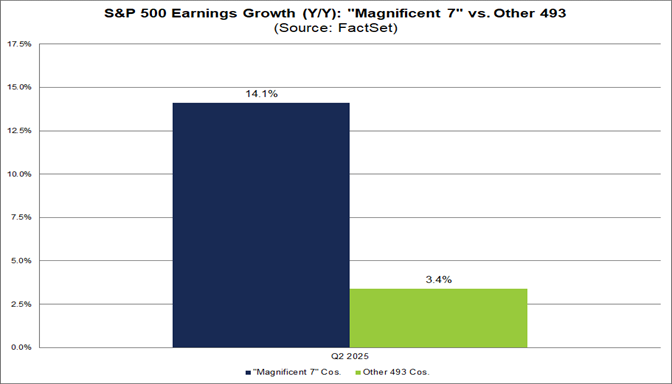

For the second quarter of 2025, these tech giants are still expected to flex their muscles with a collective earnings growth rate of 14.1%. Compare that to the remaining 493 companies in the S&P 500, which are projected to grow at a more modest 3.4%. The overall blended earnings growth rate for the S&P 500 for Q2 2025 sits at 5.6% – and guess who’s doing the heavy lifting?

The top six contributors to year-over-year earnings growth for Q2 tell the story: Warner Bros. Discovery, NVIDIA, Vertex Pharmaceuticals, Microsoft, Broadcom, and Alphabet. Three of these are Magnificent 7 companies, and interestingly, Warner Bros. Discovery and Vertex Pharmaceuticals are only there because they’re benefiting from easy comparisons to weak earnings in the previous year due to one-time charges and expenses.

The Growth Trajectory is Clearly Shifting

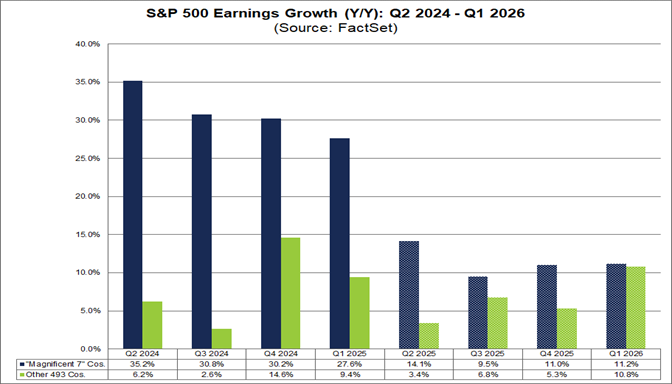

But here’s where the real story emerges from the numbers. Looking ahead to the next three quarters, analysts are painting a picture of role reversal. The Magnificent 7’s earnings growth is expected to decelerate significantly:

- Q3 2025: 9.5% growth

- Q4 2025: 11.0% growth

- Q1 2026: 11.2% growth

Meanwhile, the S&P 493 (everyone else) is projected to actually accelerate:

- Q3 2025: 6.8% growth

- Q4 2025: 5.3% growth

- Q1 2026: 10.8% growth

That final number is particularly striking – by Q1 2026, the rest of the market is expected to nearly match the Magnificent 7’s growth rate. It’s like watching a changing of the guard in slow motion.

The numbers from recent quarters paint this picture vividly. Their aggregate earnings in Q4 2024 reached a record $131.2 billion, growing 31.7% year-over-year – impressive, but still their lowest growth rate since Q1 2023. .

Revenue tells a similar story. The Magnificent 7’s aggregate revenue hit $509.0 billion in Q4, growing 12.8% – the lowest since Q2 2023, though still more than doubling the S&P 500’s 5.2% revenue growth.

Meanwhile, the contribution dynamics are shifting dramatically. In 2024, the Magnificent 7 contributed 52% of total net earnings growth for the S&P 500. By 2025, this is expected to fall to just 33%. Their earnings are projected to rise 17.1% in 2025 (down from 36.8% in 2024), while the S&P 500 excluding the Magnificent 7 is expected to improve from 6.9% last year to 9.2% this year.

The Law of Large Numbers Strikes Again

There’s a mathematical reality that even the most innovative companies can’t escape: the law of large numbers. When you’re already massive, growing at breakneck speed becomes increasingly difficult. It’s the difference between a startup doubling its revenue from $1 million to $2 million versus Apple trying to add another $100 billion to its already enormous revenue base.

The individual stories within the Magnificent 7 also reveal this pattern. In Q4 2024, just three companies – NVIDIA, Amazon, and Meta – accounted for roughly 73% of the group’s total earnings growth, contributing 29% to the overall S&P 500’s growth. NVIDIA has been the standout leader in earnings growth contribution for six consecutive quarters, a trend expected to continue, but even NVIDIA faces the inevitable slowdown as comparisons get tougher.

The Quarterly Earnings Tightrope

Here’s something that might surprise you: investors have been punishing these companies for being merely “great” instead of “astounding.” Take Microsoft, for example. Last year, the stock only rallied when quarterly earnings beat Wall Street estimates by 8% or more. Anything less than that spectacular performance actually caused the stock to fall.

This creates a peculiar situation where some of the world’s most profitable companies are walking a tightrope every quarter. With forward price-to-earnings ratios of 28.3x for the Magnificent 7 (compared to 21.8x for the broader S&P 500), investors are essentially pricing in perfection.

The Profit Margin Story

One bright spot for the Magnificent 7 is their incredible profitability. Their net profit margin hit an all-time high of 25.8% in Q4 2024 – nearly double the S&P 500’s 13.4%. The 2025 profit margin forecast of 25.3% actually surpasses the 2024 margin of 24.0%, showing these companies aren’t just growing; they’re growing efficiently and maintaining their competitive moats.

However, valuation concerns are mounting. The forward price-to-earnings ratio for the group stands at 28.3x compared to 21.8x for the S&P 500 (or 19.7x excluding the Magnificent 7). While this is below the recent peak of 33.5x in Q1 2024, it’s still a significant premium. The forward price-to-sales ratio tells a similar story at 7.2x versus the S&P 500’s 2.7x.

But even here, there are subtle warning signs. Revenue surprise rates for the group dropped to just 0.5% in Q4 2024 – the lowest since Q4 2022 and well below their prior four-quarter average of 1.3%. Earnings surprises were also muted at 7.3%, below their four-quarter average of 7.7%. This suggests that analysts have largely caught up with predicting these companies’ performance, making it harder to surprise on the upside.

The Great Rotation That’s Already Starting

Perhaps the most telling sign of changing times is what’s happening in the investment world. Fund flows data shows a dramatic shift toward equal-weighted ETFs starting in Q4 2024. While 84.4% of the £64.4 billion in U.S. ETF inflows in 2024 still went to market-cap-weighted funds (which are heavily tilted toward the Magnificent 7), equal-weighted funds captured a significant 15.6%.

The monthly breakdown is even more revealing. November 2024 saw massive inflows of £13.4 billion post-election, with £3.49 billion (26% of total flows) going to equal-weighted ETFs. December maintained strong momentum with £12.9 billion in total flows.

But 2025 has brought a reality check. February marked the first monthly net outflows (£68 million) in at least 23 months, coinciding with concerns about tariff implementation in March and April. The Magnificent 7 as a group has fallen 7.7% year-to-date compared to just a 0.7% decline for the broader S&P 500.

This shift represents something profound: investors are starting to bet on the broader market rather than just the biggest names. It’s like diversifying your stock portfolio after realizing you’ve put too many eggs in the tech basket.

Looking Ahead: The 18-Month Window

According to Bank of America’s analysis, the Magnificent 7 is expected to maintain its earnings growth advantage over the rest of the S&P 500 for about 18 more months. After that, the broader market is projected to catch up significantly.

This timeline creates an interesting dynamic. The next six quarters will likely determine whether the Magnificent 7 can engineer another growth acceleration (perhaps through new AI applications or market expansions) or whether we’re witnessing the beginning of a more balanced market structure.

What This Means for Investors

The Magnificent 7’s growth slowdown isn’t necessarily bad news – it might actually be healthy for the overall market. A more balanced market where growth is distributed across sectors and company sizes typically leads to more stable, sustainable returns.

For individual investors, this trend suggests a few key considerations:

Diversification becomes more important: Relying heavily on tech giants for returns might not be the winning strategy it once was.

Sector rotation opportunities: As the broader market catches up, previously overlooked sectors might offer better value propositions.

Valuation sensitivity: With the Magnificent 7 trading at premium valuations, any growth disappointments could lead to more significant stock price corrections.

The Bottom Line

The Magnificent 7 aren’t going anywhere – they’re still incredible companies with strong competitive positions and healthy profit margins. But their era of unchallenged market dominance appears to be evolving into something more nuanced.

We’re potentially entering a phase where market leadership becomes more distributed, where the S&P 493 start pulling their weight, and where investors need to look beyond the obvious winners of the past decade.

The tech giants taught us that growth and innovation could redefine entire markets. Now, ironically, they might be teaching us the equally valuable lesson that even the mightiest growth stories eventually mature – and that’s not necessarily a bad thing for the broader investment landscape.

The marathon continues, but the race is getting more interesting as more runners join the leading pack.