Skip to content

Skip to content

Picture this: You’re the world’s most valuable company, worth a staggering $4.5 trillion, and you’ve just announced you’re going to invest $100 billion in a startup. But here’s the twist – that startup is going to turn around and spend all that money buying your products. Sounds like the ultimate “you scratch my back, I’ll scratch yours” deal, right?

Welcome to Silicon Valley’s latest blockbuster announcement that has everyone talking. On September 22nd, Nvidia dropped a bombshell that sent shockwaves through the tech world and added $180 billion to its market cap in a single day. The chip giant announced it would invest up to $100 billion in OpenAI, the makers of ChatGPT, while simultaneously becoming their primary supplier of AI chips for the next few years.

The Circular Money Machine

Let’s unpack this gripping deal. OpenAI plans to build data centers with a combined capacity of 10 gigawatts – that’s roughly equivalent to ten nuclear power plants worth of computing power. To make this happen, they’ll need between 4 to 5 million of Nvidia’s cutting-edge AI chips, specifically the next-generation “Vera Rubin” platform that hasn’t even launched yet.

Here’s where it gets deliciously complex. Nvidia will invest $10 billion in OpenAI for every gigawatt of computing capacity built, starting with the first deployment in late 2026. According to analysts, OpenAI will pay roughly 71% in cash and receive 29% in equity funding from Nvidia. So as OpenAI builds these digital fortresses, Nvidia essentially funds the construction by buying equity in the company, which OpenAI then uses to purchase Nvidia’s chips. Bank of America estimates this circular arrangement could generate $300-500 billion in revenue for Nvidia over time.

The timing is particularly eyebrow-raising. This announcement comes on the heels of OpenAI’s other astronomical commitment – a $300 billion deal with Oracle to build even more data centers over five years. The math is starting to look surreal, with OpenAI promising to spend hundreds of billions while generating only about $13 billion in annual revenue. It’s classic Silicon Valley economics: spend tomorrow’s hypothetical money today, but on an unprecedented scale.

The Achilles Heel Revealed

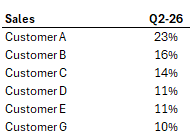

But here’s what makes this deal seem truly fascinating from a strategic perspective. Despite its perceived dominance, Nvidia has a fundamental vulnerability probaby that keeps CEO Jensen Huang awake at night. According to the company’s latest filings, six customers account for a staggering 85% of its sales, with the largest single customer representing 23% of total revenue. These aren’t just any customers – they’re tech titans like Google, Amazon, Meta, and Microsoft, all desperately working to reduce their dependence on Nvidia.

The real Achilles heel isn’t customer concentration, though. It’s that Nvidia’s business model, at its core, is still about selling hardware. Unlike software companies that can scale infinitely, hardware businesses tend to face inevitable upgrade cycles and market saturation.

That’s why Jensen expressed long ago to operate on aggressive product release cycles – originally two years, now compressed to just one year in the AI era. The company needs customers to constantly upgrade to sustain the growth rates that justify its astronomical valuation.

Already, the warning signs are appearing. The “second derivative” of Nvidia’s growth is slowing, with the most recent quarter marking the lowest growth rate since 2023. While growth is expected to reaccelerate, consensus projections show a steep decline from 58% growth in 2025 to just 17% by 2027. More concerning, investor scrutiny on AI capital spending is intensifying, with expectations that 2026 will mark a significant slowdown in customer investments.

The Frenemies Problem Gets Worse

Enter the most intriguing subplot: OpenAI isn’t just another customer – it’s actively competing with Nvidia’s biggest clients. Sam Altman, OpenAI’s charismatic but combative CEO, has seemingly been throwing digital punches at everyone. He claims he “can’t remember the last time he used Google,” wants to build a social network to compete directly with Meta, has partnered with Shopify to challenge Amazon’s e-commerce dominance, and acquired Johnny Ive’s design company to build hardware that could rival Apple. Oh, and he famously has a rocky relationship with Microsoft despite their $13 billion investment in his company.

Meanwhile, Nvidia’s traditional customers aren’t sitting idle. Google’s TPUs are already powering most of their internal AI workloads, Amazon’s Trainium chips are becoming the backbone of Anthropic’s massive computing clusters, and many companies are working with AMD and other competitors to find alternatives to Nvidia’s dominance. The company has been quietly investing in “neoclouds” like CoreWeave and increasing GPU allocations to customers like Oracle – essentially betting against its traditional clients while trying to create new power centers.

It’s like owning the only burger joint in town where six regular customers provide 85% of your business, but you overhear them planning to open competing restaurants. Your solution? Give massive discounts and free meals to a new customer who happens to be planning to compete directly with your regulars. The strategy might work short-term, but it’s virtually guaranteed to accelerate your existing customers’ efforts to find alternatives.

The Infrastructure Reality Check

The deal also highlights some uncomfortable practical realities. OpenAI’s planned 10GW of additional power capacity represents almost half of all utility-scale electricity generation added in America during the first half of this year. Even with relaxed infrastructure permitting, bringing this online could take years. Sam Altman himself acknowledged three major challenges: pushing AI research frontiers, building compelling user products, and overcoming “unprecedented infrastructure challenges” around chips and power supply.

The response to OpenAI’s latest model, GPT-5, has been notably underwhelming despite ChatGPT’s 700 million weekly active users. This raises questions about whether the massive infrastructure investments will generate proportional returns, or if the industry is building digital cathedrals for a congregation that may not materialize as expected.

Financial Theater or Strategic Masterstroke?

Some analysts are calling this arrangement “financial theater” – and they might be right. The deal bears uncomfortable similarities to the vendor financing schemes that became infamous during the early 2000s telecom bubble, where companies like Nortel and Lucent essentially funded their own sales by lending money to customers. The key difference is that Nvidia is offering equity instead of debt, eliminating repayment obligations but creating new risks around circular dependencies.

Critics argue this reveals weakness rather than strength. If Nvidia truly had unassailable technological superiority and unlimited customer demand, why would it need to fund its own sales? The company has already had to publicly clarify that it won’t give OpenAI preferential treatment amid rising antitrust concerns, suggesting regulatory scrutiny may be inevitable.

At current valuations of 41 times forward earnings, Nvidia is trading at levels not seen since the early days of the AI boom. With consensus expecting growth to decelerate significantly over the next few years, the timing of this deal appears designed to extend the current investment cycle and justify valuations that may already reflect several years of future growth.

The Verdict: Brilliant Desperation

Nvidia’s $100 billion OpenAI investment represents the ultimate Silicon Valley paradox – a move that could be simultaneously brilliant and desperate. It’s brilliant because it creates artificial demand for Nvidia’s products while positioning the company as kingmaker in the AI ecosystem. It’s desperate because it reveals the fundamental fragility of depending on a small number of customers who are actively working to replace you.

The deal essentially turns Nvidia into a venture capitalist using its own products as currency, betting that the AI revolution will continue indefinitely and that infrastructure spending will justify today’s valuations. It’s like a high-stakes game of musical chairs where everyone knows the music will eventually stop, but nobody wants to be the first to sit down.

Whether this proves to be strategic genius or expensive folly will depend on whether artificial general intelligence arrives as promised and whether the astronomical investments in AI infrastructure generate proportional economic value. What’s certain is that Silicon Valley has never seen anything quite like this circular financing arrangement, where the world’s most valuable company essentially funds its own growth by investing in its customers’ dreams of digital dominance.

Disclaimer – This article draws from sources such as the Financial Times, Bloomberg,and other reputed media houses. Please note, this blog post is intended for general educational purposes only and does not serve as an offer, recommendation, or solicitation to buy or sell any securities. It may contain forward-looking statements, and actual outcomes can vary due to numerous factors. Past performance of any security does not guarantee future results.This blog is for informational purposes only. Neither the information contained herein, nor any opinion expressed, should be construed or deemed to be construed as solicitation or as offering advice for the purposes of the purchase or sale of any security, investment, or derivatives.The information and opinions contained in the report were considered by VF Securities, Inc.to be valid when published. Any person placing reliance on the blog does so entirely at his or her own risk, and does not accept any liability as a result.Securities markets may be subject to rapid and unexpected price movements, and past performance is not necessarily an indication of future performance. Investors must undertake independent analysis with their own legal, tax, and financial advisors and reach their own conclusions regarding investment in securities markets.Past performance is not a guarantee of future results