Skip to content

Skip to content

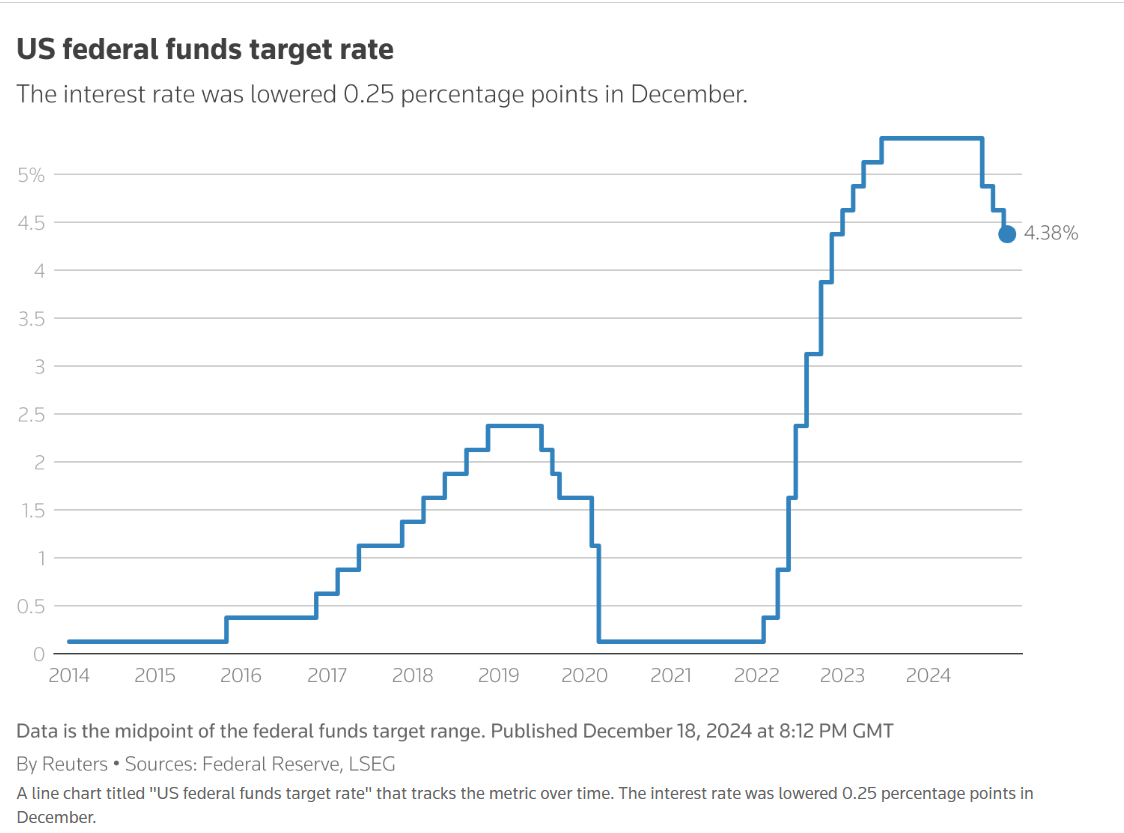

The Federal Reserve’s decision to cut interest rates by 0.25% was a mixed message. On one hand, they eased borrowing costs for the third consecutive time. On the other, they signaled a more cautious approach for 2025, hinting at fewer rate cuts than expected. This news sent shockwaves through the markets, causing the dollar to surge to a two-year high and triggering a global sell-off in stocks.

The Federal Open Market Committee (FOMC) voted on Wednesday to reduce the benchmark rate to a range of 4.25% to 4.50%. This marks the third rate cut in a row, which some may interpret as a sign of the Fed’s commitment to easing monetary policy. However, there was a clear shift in tone.

Cleveland Fed president Beth Hammack dissented, voting to keep rates unchanged, signaling that not all members are convinced about the need for further cuts. While the Fed still expects some easing, the number of cuts has been scaled back, pointing to the fact that inflation remains stubbornly high.

Inflation Worries and a Strong Dollar

The key takeaway from the Fed’s latest move is its recognition that inflation is far from being under control. Despite the rate cut, the central bank’s projections show that inflation is likely to remain above its 2% target for the foreseeable future. In fact, the Fed raised its inflation forecast for 2025, now predicting a rise to 2.5% from the earlier estimate of 2.1%. This adjustment indicates that the Fed no longer believes it has fully tamed inflation, and it’s adjusting its expectations accordingly.

The core Personal Consumption Expenditures (PCE) price index, the Fed’s preferred inflation gauge, showed a 2.8% annual increase in October. That’s a stark reminder that inflation is proving stickier than expected, even with aggressive rate hikes earlier this year. And while the rate cut might seem like a step towards easing, it could also be a recognition from the Fed that it has more work to do.

This was a key reason why the Fed cut back its expectations for future rate cuts. Instead of the three cuts that some economists had predicted for 2025, the Fed now forecasts just two.

In fact, the central bank’s forecast for core inflation has been raised, with projections now indicating it will be 2.5% in 2025 and 2.2% in 2026. While this is still below current levels, it’s far from the 2% target the Fed is aiming for.

Despite efforts to curb inflation, the central bank has acknowledged that it underestimated inflation’s staying power. The Fed’s new policy stance reflects this, with officials now less inclined to make aggressive cuts to rates moving forward. The idea of a “soft landing,” where inflation comes down without derailing the economy, is becoming increasingly uncertain.

The impact on the markets was swift and severe. US stocks dropped sharply following the Fed’s announcement. The S&P 500 fell nearly 3%, while the tech-heavy Nasdaq Composite dropped 3.6%. The sell-off wasn’t limited to the US. Asian markets, including South Korea and Taiwan, saw sharp declines as well. Stocks of companies sensitive to economic fluctuations—like small-cap stocks—suffered significantly, with the Russell 2000 index dropping 4.4%.

The Dollar Reigns Supreme

Perhaps one of the most striking results of the Fed’s decision was the surge in the US dollar. The dollar gained 1.2% against a basket of six major currencies, reaching its highest level since November 2022. This rally was partly driven by expectations of higher tariffs under President-elect Donald Trump, which could spur inflation. As Mike Pugliese, senior economist at Wells Fargo, put it, the Fed’s decision “puts more fuel on the fire.”

The strength of the dollar has had a ripple effect on other currencies. The South Korean won plummeted to a 15-year low, while the Japanese yen weakened by 0.5% to ¥154.5.

Fed’s Forward-Looking Projections: A New Phase

In his statement, Fed Chair Jerome Powell mentioned that the central bank’s policy settings were now “significantly less restrictive” and that officials could be “more cautious” in future easing. Powell also suggested that the December decision had been a “closer call” than previous meetings, acknowledging the challenges in balancing inflation control and economic growth.

The Fed’s goal remains clear: to apply enough pressure on consumer demand and business activity to bring inflation back to its 2% target, without derailing the job market or broader economic recovery. Powell also emphasized that the economy’s resilience in the face of higher borrowing costs had changed the central bank’s approach. Officials are now aiming for a “neutral” rate that neither stifles growth nor overheats the economy.

Looking ahead, inflation could remain a major concern. The Fed raised its forecast for core inflation to 2.5% in 2025 and 2.2% in 2026. Furthermore, the unemployment rate is expected to stay steady at 4.3% over the next three years. This indicates that while the economy is holding up, inflation risks are far from gone.

The Bigger Picture: A Complex Economic Outlook

The Fed’s recent actions are part of a broader effort to recalibrate its policies after successfully reducing inflation from a peak of 7% in 2022. The central bank’s new “neutral rate” estimate, now pegged at 3%, suggests that they believe the economy is nearing a more balanced state. However, the uncertainty surrounding inflation and fiscal policies—especially with Trump’s return to office—means the Fed’s job is far from over.

As we look towards 2025, the Fed’s projections suggest that inflation will be a persistent issue. The combination of lower-than-expected rate cuts and a stronger dollar could have ripple effects across global markets. Investors, particularly those in emerging markets, will likely face headwinds as the US policy shift reverberates through the global economy.