Skip to content

Skip to content

It’s not every day that a software company captures Wall Street’s full attention. But that’s exactly what Figma’s IPO is doing.

By the time you’re reading this, Figma’s $18.8 billion public listing may have already closed its books — 40 times oversubscribed, according to Bloomberg.

Yes, 40 times.

That kind of frenzy is rare.

That’s not normal. Even hot IPOs like Circle’s in June (which was 20x oversubscribed) don’t see this kind of frenzy. Some reports even say the company may price the IPO above the top of its new range — a rare move, showing just how much demand is building.

And it begs the question: what makes Figma this special?

When Dylan Field and Evan Wallace founded Figma in 2012, the design world was fragmented. Designers worked in isolation on desktop apps like Sketch, then handed off static files to developers who had to guess at implementation details. Collaboration happened through email attachments and Slack screenshots.

Figma’s insight was deceptively simple: design should happen in the browser, in real-time, with everyone involved in product creation. No downloads, no version control nightmares, no “final_final_v3.sketch” files cluttering hard drives.

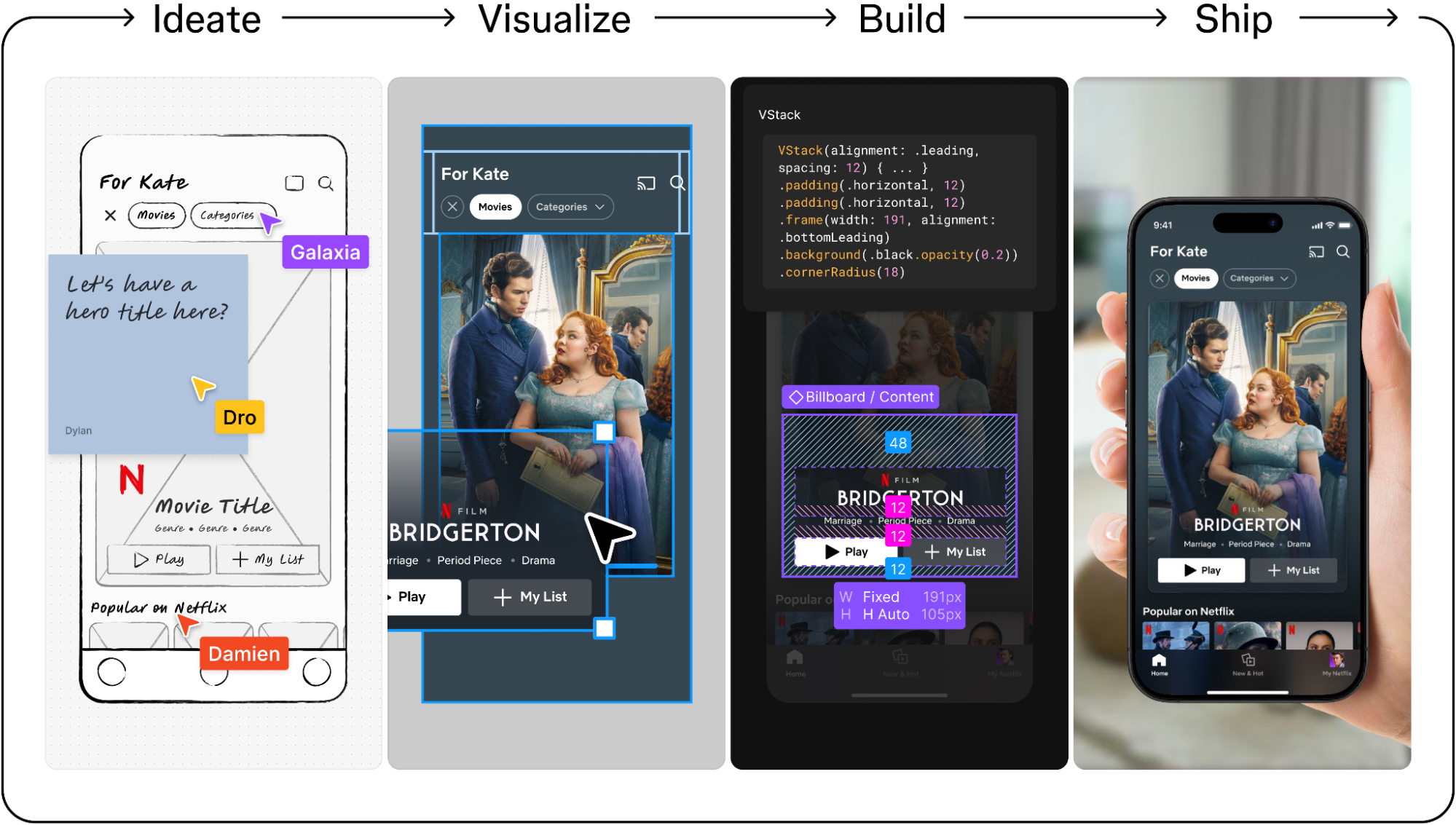

But what started as a design tool has metamorphosed into something much larger. Today’s Figma includes:

- Figma Design: The core collaborative interface design tool

- FigJam: Digital whiteboarding for brainstorming and user journey mapping

- Dev Mode: A workspace where engineers inspect designs and extract production-ready code

- Figma Slides: Presentation software that keeps product teams aligned

- Figma Sites: Turn designs into live websites without developer handoff

- Figma Buzz, Draw, Make: AI-powered tools for asset creation and prototyping

The numbers tell the expansion story: 76% of customers now use two or more Figma products, up from 64% a year earlier. This isn’t just feature creep—it’s strategic platform building.

The Viral Loop That Prints Money

Here’s where Figma gets interesting from a business perspective. Most SaaS companies struggle with customer acquisition costs and complex enterprise sales cycles. Figma flipped the script with what might be the most elegant viral loop in B2B software.

It works like this:

- A designer signs up for Figma (often on the free plan)

- They share a design file URL with colleagues

- Product managers jump in to leave feedback

- Engineers need Dev Mode to inspect designs

- Marketing wants to use the design system for campaigns

- Soon the entire product org is collaborating in Figma

The results are staggering: 70% of Organization and Enterprise customers started with at least one user on a Professional plan. That’s not a sales funnel—that’s a viral engine that converts individual users into enterprise accounts.

Figma has around 450,000 customers, including 1,031 that were spending $100,000 or more in annual revenue. But perhaps most remarkably, 13 million monthly active users includes roughly two-thirds who aren’t designers. For every designer they acquire, Figma pulls in two other people from the organization.

The Numbers That Make VCs Salivate

Let’s talk about the metrics that matter:

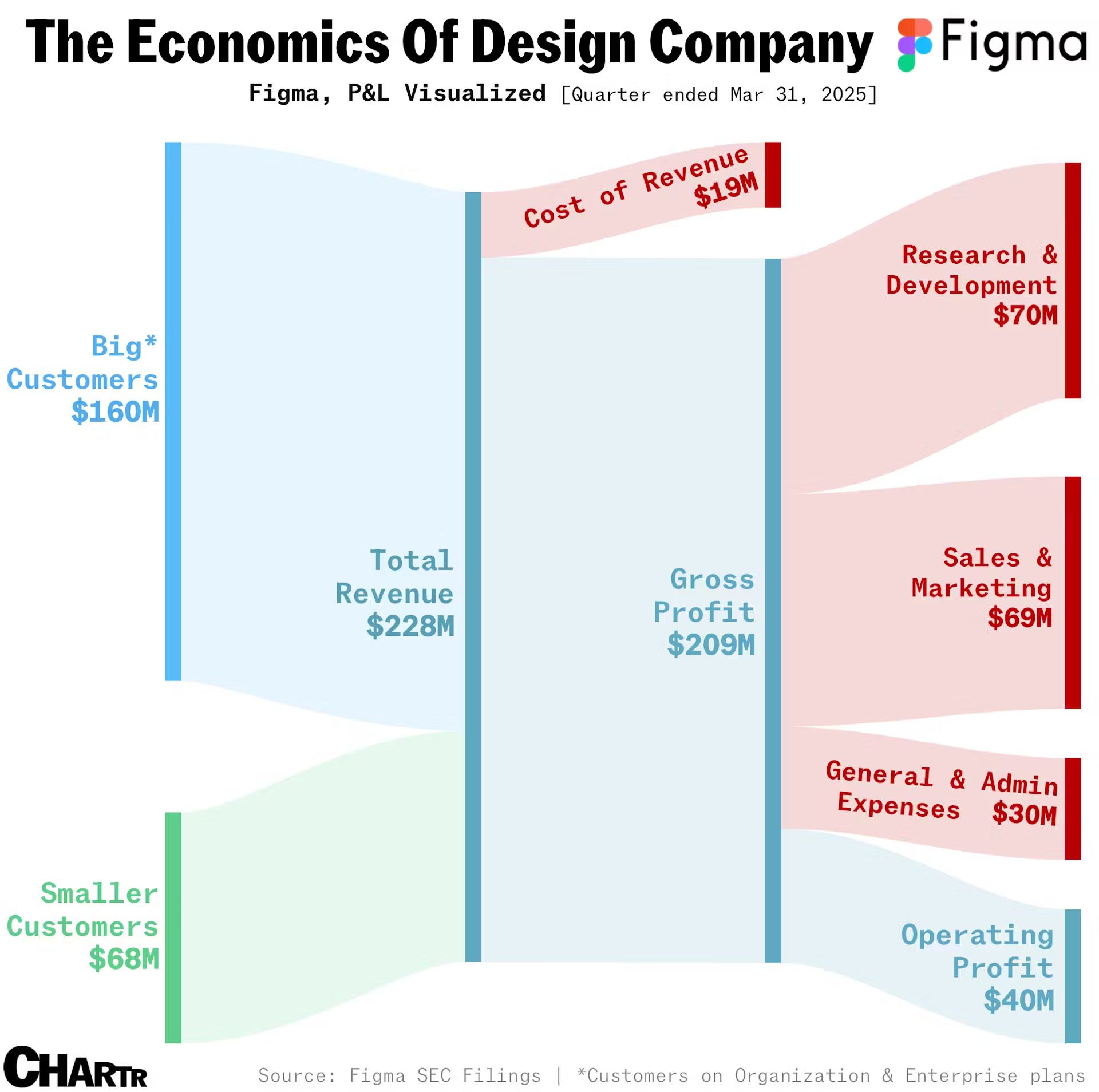

Revenue Growth: Figma saw revenue in its first quarter of $228.2 million, up 46% year-over-year, putting them at $913M ARR. In the current SaaS landscape, maintaining 46% growth at nearly $1 billion in revenue is almost unheard of.

Profitability: recorded net income of $44.9 million, up from $13.5 million a year earlier. This isn’t just revenue growth—Figma is generating real, sustainable profits while scaling.

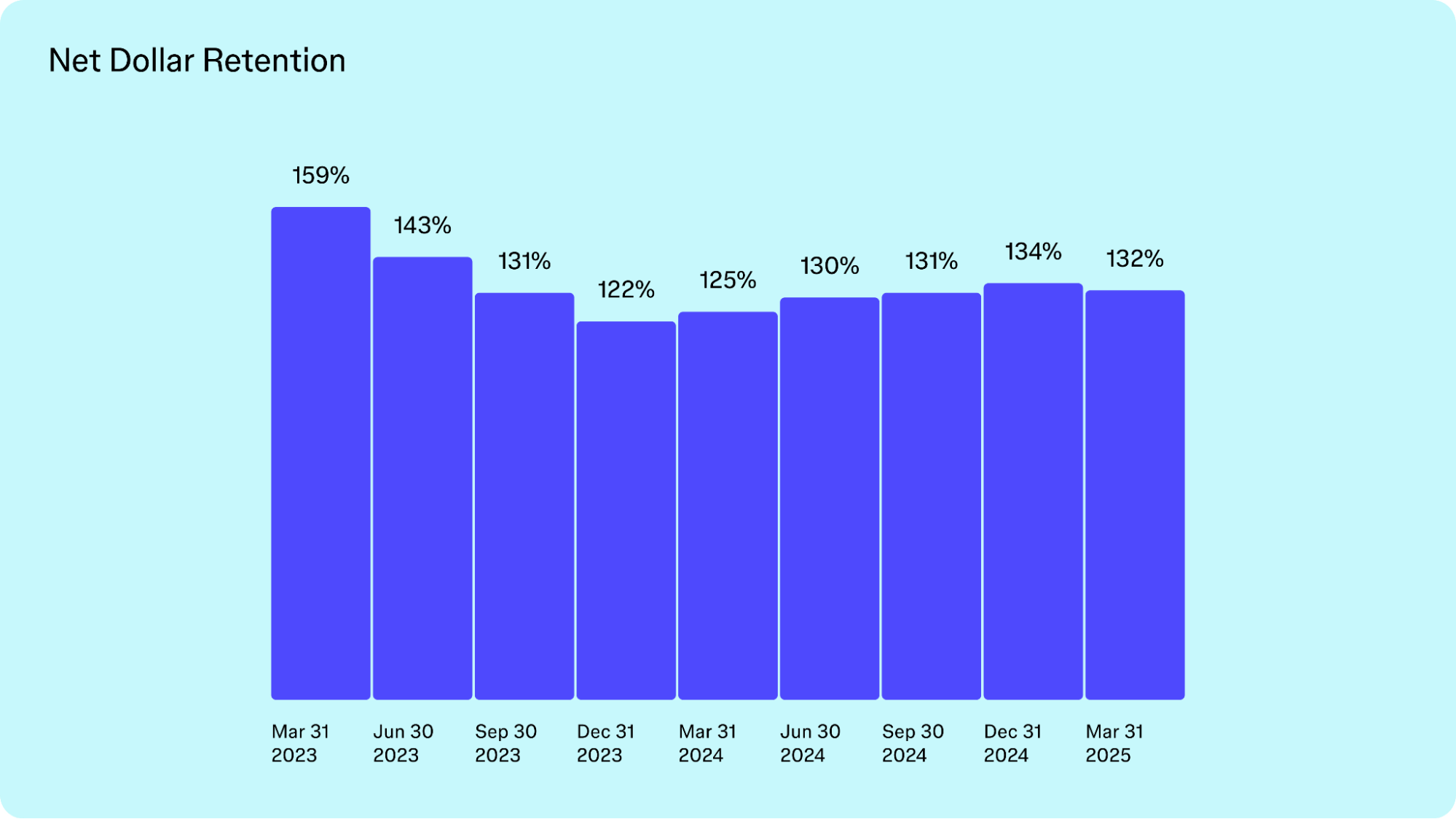

Retention: Net Dollar Retention of 132% means existing customers are spending 32% more each year. Gross Dollar Retention of 96% means almost nobody churns once they’re hooked.

Margins: 91% gross margins reflect the beauty of browser-based, product-led software. There’s no physical infrastructure to scale, no complex implementation services—just pure software leverage.

These aren’t just good metrics. These are generational software company metrics.

From Adobe Heartbreak to IPO Triumph

The Adobe acquisition saga deserves its own Netflix documentary. In September 2022, Adobe agreed to acquire Figma for $20 billion—a staggering 50x revenue multiple that made headlines for all the wrong reasons. Critics called it desperation, regulatory bodies called it anti-competitive, and in December 2023, the deal died under regulatory pressure.

Adobe paid Figma a $1 billion breakup fee.

That “failure” might be the best thing that ever happened to Figma. The breakup fee provided cash runway, the media attention boosted brand awareness, and most importantly, it gave Figma time to prove it could become something much bigger than a design tool acquisition target.

Since the Adobe deal collapsed, Figma has:

- Launched five new product categories

- Nearly doubled its revenue

- Achieved consistent profitability

- Expanded from 11 million to 13 million monthly active users

- Built out enterprise features that positioned it for long-term platform dominance

The Platform Play: Expanding the Moat

What makes Figma compelling isn’t just its current metrics—it’s the platform opportunity ahead.

Consider the total addressable market expansion:

- Design tools: Figma’s original market, largely conquered

- Collaboration software: Competing with Miro, Notion, Microsoft

- Web development: Challenging Webflow, WordPress

- Presentation software: Taking on PowerPoint, Google Slides

- Content creation: Battling Canva, Adobe Creative Suite

- No-code development: Emerging category with massive potential

Each new product category doesn’t just add revenue streams—it increases switching costs. Once a company has built its design system in Figma, integrated its development workflow through Dev Mode, created presentations in Figma Slides, and launched websites through Figma Sites, migration becomes nearly impossible.

This creates what venture capitalists call “expansion revenue”: existing customers naturally grow their spending as they adopt new products. It’s why Figma’s Net Dollar Retention stays consistently above 130%.

The AI Wild Card

Figma’s newest products—Buzz, Make, and Draw—represent a bet on AI-powered creativity. These tools promise to automate asset creation, generate prototypes from prompts, and accelerate the design process through machine learning.

But AI creates a paradox for seat-based SaaS companies: Does automation expand the total addressable market by making design accessible to non-designers, or does it cannibalize existing seats by making designers more productive?

Figma seems to be betting on expansion. Their AI tools aim to democratize design creation, potentially turning every marketing manager, product manager, and entrepreneur into a design creator. If successful, this could multiply their addressable market.

The risk? If AI makes individual designers 10x more productive, companies might need fewer Figma seats, not more.

Valuation: What’s Fair for Digital Product Infrastructure?

Figma disclosed preliminary results for the second quarter showing revenue growth between 39% and 41% year over year, suggesting continued momentum despite the slight deceleration from Q1’s 46% growth.

At the current IPO pricing, Figma would debut around $19 billion valuation—roughly 21x forward revenue.Figma’s combination of 40%+ growth, 90%+ gross margins, and actual profitability justifies a premium multiple. The question is how much premium.

The Risks Nobody Talks About

Every growth story has blind spots. Figma’s include:

Market Saturation: 95% of Fortune 500 companies already use Figma, but only 1,031 customers pay $100K+ annually. The land-and-expand model works until you run out of land.

Competitive Pressure: Microsoft is bundling design tools into Office 365. Adobe isn’t giving up. Notion, Canva, and others are expanding into adjacent territories. Real-time collaboration is becoming table stakes, not a differentiator.

AI Disruption: Figma is betting AI expands their market, but what if AI-powered tools from OpenAI, Anthropic, or others make dedicated design software obsolete? What if ChatGPT can generate entire user interfaces from text prompts?

Governance Concentration: Dylan Field holds 15:1 super-voting shares plus proxy control over his co-founder’s stake. Public market investors might be uncomfortable with such concentrated control.

International Gap: Despite global usage, only ~20% of revenue comes from outside the US. Can Figma build the sales infrastructure to monetize international users at US rates?

The Platform Thesis

Strip away the metrics and multiple expansion theories, and Figma’s IPO comes down to one question: Is this a design tool company or a platform company?

Design tool companies have natural growth limits. Once every designer uses your product, growth slows to the rate of designer hiring plus pricing increases.

Platform companies can expand across roles, departments, and use cases. They become digital infrastructure that’s increasingly difficult to replace.

Figma’s early expansion beyond designers suggests platform potential. 13 million monthly active users with only one-third being designers indicates something bigger than a design tool. The question is execution: Can Figma successfully expand into new categories without losing the simplicity that made it great?

The Verdict: Generational Software or Overhyped Design Tool?

Figma represents the strongest IPO opportunity in years, but that doesn’t make it a guaranteed winner.

The bull case writes itself: best-in-class metrics, viral growth engine, platform expansion potential, AI positioning, and recession-resistant creative software category. If Figma successfully evolves from design tool to digital product operating system, the current valuation could look conservative in five years.

The bear case is equally compelling: growth deceleration, market saturation, competitive pressure, AI disruption risk, and rich valuation expectations. If Figma remains primarily a design tool, even a very successful one, the current premium multiple might prove unsustainable.

For public market investors, Figma offers something rare: a chance to own a piece of genuinely innovative software infrastructure at the moment it transitions from startup to platform. The company has proven it can execute, scale, and generate profits while maintaining remarkable growth rates.

But this isn’t a value play. This is a bet on Figma becoming the foundational layer for how digital products get built—the Salesforce of creative workflows, the Slack of product development, the operating system for the design-to-deployment pipeline.

At nearly $20 billion, that bet better be right.

Disclaimer – This article draws from sources such as the Financial Times, Bloomberg,and other reputed media houses. Please note, this blog post is intended for general educational purposes only and does not serve as an offer, recommendation, or solicitation to buy or sell any securities. It may contain forward-looking statements, and actual outcomes can vary due to numerous factors. Past performance of any security does not guarantee future results.This blog is for informational purposes only. Neither the information contained herein, nor any opinion expressed, should be construed or deemed to be construed as solicitation or as offering advice for the purposes of the purchase or sale of any security, investment, or derivatives.The information and opinions contained in the report were considered by VF Securities, Inc.to be valid when published. Any person placing reliance on the blog does so entirely at his or her own risk, and does not accept any liability as a result.Securities markets may be subject to rapid and unexpected price movements, and past performance is not necessarily an indication of future performance. Investors must undertake independent analysis with their own legal, tax, and financial advisors and reach their own conclusions regarding investment in securities markets.Past performance is not a guarantee of future results