Skip to content

Skip to content

The Story

This week, two of America’s most-watched tech companies released their quarterly results, and they painted completely different pictures of where technology is headed. One company – Alphabet – delivered strong performance but announced significant increases in capital spending for AI infrastructure.

The other company – Tesla – reported challenging numbers but emphasized future opportunities in autonomous driving technology.

That’s essentially what happened when Alphabet and Tesla released their quarterly earnings this week. And the contrast tells us everything about where Big Tech is headed right now.

Alphabet: The Overachiever with Expensive Tastes

Alphabet’s quarterly performance was strong by most financial metrics. Revenue reached $96.43 billion, exceeding analyst expectations of $94 billion.

Earnings per share came in at $2.31 compared to the expected $2.18. Net income increased nearly 20% to $28.20 billion. These results typically indicate solid business performance.

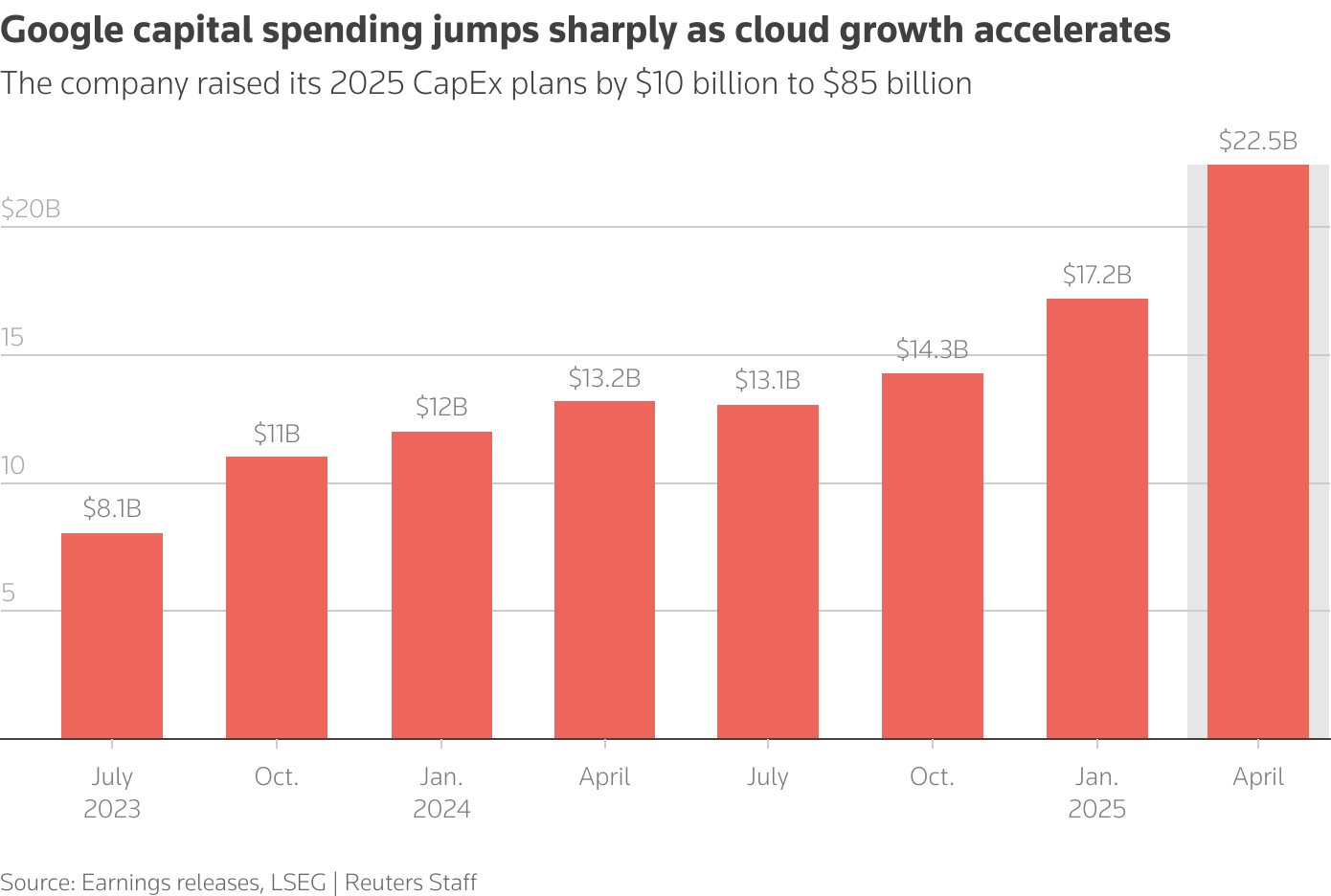

Alphabet announced an increase in their capital expenditure plans for 2025 from $75 billion to $85 billion. This $10 billion increase is primarily allocated for AI infrastructure including data centers and specialized computing hardware.

Now, imagine you’re an investor. You’re thrilled that your company is making money hand over fist, but then they tell you they want to spend an extra $10 billion. Your first thought is probably “Wait, what?” And that’s exactly what happened to Alphabet’s stock price after hours – it initially dropped before recovering.

Here’s the thing though – there’s method to this apparent madness. Google’s cloud business brought in $13.62 billion this quarter, which is a 32% jump from last year. Analysts were expecting a 26.5% increase, so Google basically said “hold my coffee” and surpassed those expectations.

But wait, it gets better. CFO Anat Ashkenazi revealed something fascinating – they literally can’t keep up with demand. Companies want Google’s cloud services faster than Google can build the infrastructure to provide them. It’s like having a restaurant so popular that you need to keep expanding the kitchen just to handle all the orders.

The numbers back this up. Deals worth over $250 million doubled this quarter. Google signed as many billion-dollar deals in the first half of 2025 as they did in all of 2024. That’s the kind of growth that makes spending $10 billion on infrastructure seem less crazy and more like “we need bigger kitchens, stat.”

And here’s a plot twist worthy of a soap opera – OpenAI, the company behind ChatGPT and arguably Google’s biggest AI rival, recently became a Google Cloud customer. Yes, Google’s main competitor is now paying them for services. It’s like McDonald’s deciding to buy their beef from Burger King. CEO Sundar Pichai said they’re “very excited to be partnering with them,” which is corporate speak for “we’ll gladly take their money.”

The AI adoption numbers are genuinely mind-boggling. Google’s AI Overviews feature – you know, those AI-generated summaries that appear at the top of search results – now has over 2 billion monthly users.

That’s up from 1.5 billion just three months ago. Their Gemini AI app has 450 million monthly users. And something called AI Mode reached 100 million users in just two months.

Think about that for a second. Google launched a new AI feature and got 100 million people using it in eight weeks. That’s faster adoption than most social media apps dream of.

Meanwhile, Google’s core search business continues to print money like it’s going out of style. Search ad revenue grew 12% when analysts expected 9%. Total advertising revenue hit $71.34 billion, up 10.4% from last year. YouTube advertising revenue came in at $9.8 billion, beating expectations.

Tesla: The Former Star Student Having a Rough Semester

Now let’s talk about Tesla, where the story is quite different. Revenue fell 12% to $22.5 billion from $25.5 billion last year. This is the second straight quarter of declining revenue, which is never a good look.

Global deliveries dropped 13.5%, and something called automotive regulatory credits – basically money other car companies pay Tesla to meet environmental rules – plunged 51%.

If you’re keeping score at home, Tesla is selling fewer cars and making less money from regulatory credits. That’s not exactly a winning combination.

But here’s where Tesla’s story gets interesting. Despite all the doom and gloom, their automotive gross margin came in at 14.96%, which was actually better than Wall Street expected. This means Tesla is getting more efficient at making cars, even though they’re selling fewer of them. It’s like a restaurant that’s serving fewer customers but making more profit per meal.

When asked about the challenging numbers, Elon Musk did what Elon Musk does best – he acknowledged the problems but then pivoted to talking about the future. “We probably could have a few rough quarters,” he admitted, specifically mentioning Q4, Q1, and maybe Q2. But then he said something that basically summarizes Tesla’s entire strategy: “Once you get to autonomy at scale in the second half of next year, certainly by the end of next year, I think I’d be surprised if Tesla’s economics are not very compelling.”

This statement reflects Tesla’s strategic focus on autonomous driving technology as a key growth driver.

Tesla’s entire future hinges on autonomous driving technology. They’ve started a small robotaxi trial in Austin with about a dozen Model Y vehicles. Musk outlined plans to roll out robotaxi services to roughly half the U.S. population by the end of this year. They’re seeking regulatory approval in California, Nevada, Arizona, Florida, and other states.

The company expects to start mass-producing something called the Cybercab (their purpose-built robotaxi) and Semi trucks in 2026. Musk called autonomy “the story” for Tesla, which is either visionary leadership or a very expensive gamble, depending on your perspective.

Tesla is also working on that long-promised cheaper car. They produced some initial units by the end of June, but CFO Vaibhav Taneja said production would ramp up slower than expected. When asked what the car would look like, Musk joked, “It’s just a Model Y. I let the cat out of the bag there.” So much for keeping secrets.

The Tale of Two Strategies

What’s fascinating about these earnings is how they reveal completely different approaches to the AI revolution. Alphabet is essentially playing the infrastructure game – they’re building the digital equivalent of highways and power plants that will enable the AI economy. It’s expensive, but there’s clear demand and they’re already making money from it.

Tesla is playing the moonshot game – betting everything on breakthrough technology that could either make them the king of transportation or leave them scrambling to catch up with traditional car companies who are rapidly improving their electric vehicles.

The market seems to be getting pickier about which approach it prefers. This year, some tech giants like Meta, Microsoft, and Nvidia are up an average of 22%, while others like Alphabet and Amazon have been flat, and Apple and Tesla are down around 12%. The “Magnificent Seven” tech stocks aren’t moving together like they used to.

Both companies face their own unique challenges beyond just quarterly numbers. Alphabet has to prove that spending $85 billion on AI infrastructure will actually generate proportional profits. Their operating expenses jumped 20% to $26.1 billion, partly due to a $1.4 billion settlement with Texas over data privacy issues.

Tesla faces different problems. Chinese electric vehicle manufacturers are offering cheaper alternatives. There’s ongoing criticism of Musk’s political activities – reports suggest he formed a new political party this month despite promising to focus on his companies. Several high-profile executives, including longtime Musk allies, have left the company recently.

What This All Means

From an investment perspective, Alphabet trades at a forward price-to-earnings ratio below 20x, making it relatively cheap among big tech companies. The company generates massive cash flows from search and advertising, providing a solid foundation for their AI investments.

Tesla’s valuation still assumes it will become much more than just a car company. If autonomous driving works out, Tesla could become incredibly valuable. If it doesn’t, well, they’re a car company facing increasing competition and declining sales.

The earnings reports show that while both companies are navigating the AI revolution, they’re playing fundamentally different games. One is building the infrastructure for incremental but profitable growth. The other is betting everything on revolutionary technology that may or may not work.

It’s like watching two different approaches to getting rich. One person is steadily building a profitable business while investing in expansion. The other is buying lottery tickets with their rent money, convinced they’ve found the winning numbers.

Time will tell which strategy pays off, but these earnings give us a pretty clear picture of where each company stands right now.