Skip to content

Skip to content

In this week’s article, we will continue our deep dive into Amazon. You can read part 1.

Welcome back to our deep dive into Amazon’s strategy. In part 1, we talked about Amazon’s efforts to expand into other consumer spending categories, namely healthcare, music/video and groceries. In this follow up article, we will be discussing Amazon’s other businesses: fintech, advertising and cloud computing.

Amazon fintech efforts

Since you’re already buying almost everything from Amazon, shouldn’t you be paying for these purchases with Amazon payments as well?

Amazon surely thinks that you should.

Amazon’s payments efforts can be categorized into two categories:

- B2C

- B2B

B2C – direct to consumer

One of the key challenges of new payment adoption is distribution, afterall, the provider of the payment solution cannot generate revenue from the payment channel if the solution is not used.

Here are Amazon’s initiatives on payments:

- Amazon Prime credit card, a credit card for Prime members that gives 5% cash back for purchases on Amazon.com. There’s no doubt that Amazon can negotiate lower fees on these transactions because of the company’s large volume.

- Amazon Cash, a cash wallet solution to enable consumers to spend on Amazon without the need for a debit or credit card, an important initiative especially internationally where cash-based transactions still dominates daily spending.

- Amazon One, which we will discuss in greater detail below.

Both the Prime credit card and Amazon Cash are for transactions where Amazon is the merchant. But in reality, the majority of consumer spend is still done outside Amazon. Furthermore, as we mentioned above, one of the key challenges in payment solutions adoption is distribution.

Both Apple and Google are leveraging their dominant positions as smartphone OS makers to distribute their payment solutions. Amazon does not have a distribution advantage. Initially, it experimented with the Amazon Go app, where you download an app and use a QR-based payment solution. Compared to Google’s or Apple’s solutions however, this approach has more friction.

Using Biometric Identification

To reduce friction and still ensure massive distribution, Amazon has multiple projects to leverage biometric identification as a form of payment.

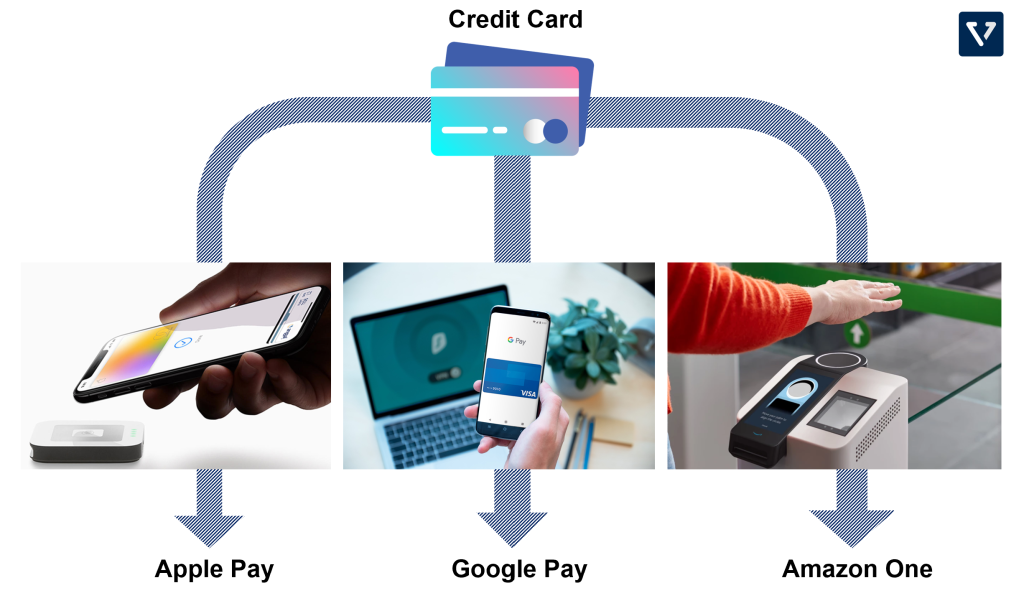

Amazon One

Amazon One removes the need for the phone altogether, and relies on the hand print as the unique identifier tied to the consumer’s credit card (Figure 1).

Some quick facts about Amazon One:

- How it works: Amazon One works by taking an image of your palm (both surface images and vein patterns) and sending this image (in an encrypted format) to the cloud to identify you. This means that Amazon will have a copy of your palm signature – the downside of this is privacy concerns: you can change your phone, but you cannot change your palm.

- What is it for: the application can identify you, your credit card, and your identity. Amazon has ambitions to expand One to be more than just a payment solution. The company plans to push this solution to other merchants as a point-of-sale solution. That said, Amazon emphasizes that they will not be tracking users’ purchase information. Amazon even wants to make this application a full identity management platform (for example, in the future you will be able to enter an office building with a wave of your palm instead of waving your badge).

Voice purchase

Amazon has also made inroads in voice-based payment efforts. Through the Alexa app or Alexa enabled infotainment equipped cars, consumers can now pay for gas by just uttering “Alexa, pay for gas†at Exxon and Mobil stations.

Two interesting observations here:

- Two key challenges of voice based shopping are discovery and selection, or lack thereof. Imagine if every time you buy something with your voice (say: “Ok Google, order Chinese food to be delivered by 6PMâ€), the smart speaker must revert back by giving you all the relevant options (“Which Chinese food?â€, “The new restaurant that you visited yesterday?†“Or the closest one to your home?â€). For voice shopping to work, the buyer must have already decided on what to purchase. This is problematic for Google, because Google’s main business is predicated on advertising, which means serving options to customers.

- Amazon solves this problem by first going after purchases that are tied to specific locations, eliminating the need for discovery and selection; if you’re giving voice instruction to pay from a specific gas station, that means you have already made your purchasing selection and are just trying to complete the purchasing process.

B2B – payments for other businesses

Amazon Pay

Amazon has payment and address information on hundreds of millions of consumers. The company is leveraging this data into a payment solution called Amazon Pay. With this service, other ecommerce websites or retailers can offer a more streamlined checkout process (consumers no longer need to create an account and fill out payment and shipping information), increasing conversion and reducing checkout time. On this front, Amazon competes with PayPal, credit cards and buy now, pay later companies (Klarna, Affirm and Afterpay).

How does Amazon make money from payments? Similar to other payment processing companies, Amazon makes money from a mix of both fixed (Authorization fee) and variable (Processing fee). Some of these revenues are then shared with the issuer;s bank and Visa (see Figure 3).

Notice however that the processing fee for Alexa (voice based) transactions is higher – this is why Amazon is pushing hard to widen Alexa adoption (through smart speakers, glasses, earbuds, and car infotainment).

Figure 3: Amazon’s fees for payment processing

Merchant services

Now that Amazon has become a very large platform for other ecommerce businesses, it has created multiple financial products to help small businesses on its platform:

SMB Lending (Amazon Lending): created in conjunction with Goldman Sachs, to provide working capital to merchants selling products on Amazon. Since Amazon has data on the health of the businesses on its platform, it can help banks underwrite loans. The effort seems to be faltering however. The total amount of loans made only grew less than 3% from US $692 million in 2017 to US $710 million in 2018.

Amazon Business American Express card (Amazon Amex): Business owners spend more on credit cards than the average consumer, and therefore can generate a higher revenue for the card issuers. In the US, although business credit cards make up only 4% of the total number of cards, it represents 17% of the total spend.

Amazon Web Services (AWS)

This is arguably the most important segment of the company’s business. As a standalone entity, it has the potential to muster a US $1 trillion valuation and is the most profitable segment of Amazon.

In the early 2000s, Amazon was struggling with scalability issues. As the number of consumers it served grew, so did the selection of items and the number of external merchants on the platform. To make matters worse, these complexities were coupled with the inefficiencies of different teams within Amazon that were reinventing the wheel for the different projects they were working on.

Borne of its own need, the company started building a shared common infrastructure resource that can be freely accessed by internal team members. It took several years after the deployment of this internal infrastructure before Amazon launched AWS (in 2006).

Starting with a cloud storage solution (S3), which launched in 2006, AWS now offers hundreds of different databases, compute and artificial intelligence solutions. It powers Apple’s iCloud products, Netflix’s streaming empire, the Department of Defense, and the CIA.

As of Q3 2020, AWS contributes 12.7% of Amazon’s total quarterly net sales (or US $11.6 billion), but 57% of its operating cash flow. For Amazon, this is a very profitable segment of its business. Note that as the size of the business grows, its growth rate has slowed (to 30% year over year).

Not just an e-commerce business anymore

For most observers, Amazon is just an e-commerce company. But as you can now see, e-commerce is just the beginning. Amazon has turned itself into a diverse platform that powers many other things. In Q3 2020, while its core 1st party e-commerce business contributes only about half of its net sales, the rest of Amazon has grown into substantial revenue generators.

After analyzing Amazon’s different segments, one can’t help but see the different flywheels that businesses have; growth in one area promotes growth in the other. It is truly formidable – as most businesses are lucky to have just one flywheel.

Back to our original premise. As of this writing, Amazon’s market capitalization is at US $1.6 trillion. Is this an under-valuation? Or an over-valuation?

Over the course of this two-part deep dives (part 1), we’ve listed numerous companies that Amazon competes with. But how do their valuations stack up?

Figure 6 shows the back of the envelope comparison (it does not take into account growth rate, profitability or market share) market capitalization of Amazon vs. other companies it competes with. In streaming, it competes with Netflix and Roku. In e-commerce, it competes with Walmart and Shopify, etc. We estimate that AWS as a standalone company is valued at about 40% of Amazon’s market cap.

As you can see, adding the market cap of these companies together gives you a value that exceeds Amazon’s current market cap. It is often the case that investors value a business more highly when it is spun off into an independent entity.

So, it is likely that even as part of FAANG, Amazon is undervalued.