Skip to content

Skip to content

In this blog, we discuss the latest inflation updates and how Europe averted an energy crisis this winter.

Inflation expectations

The latest US inflation data came out last week. There are two areas of interest for investors: overall CPI and core CPI. Core CPI is a measure of inflation that excludes volatile energy and food prices (which are heavily impacted by the war in Ukraine). It’s a more closely watched metric by investors and is the Fed’s go-to metric.

Here are the numbers (see Figure 1 below):

It’s evident that while inflation is still rising, the rate of increase has peaked. However, at 5.7%, core inflation is still too high for the Fed (its target is 2%). After the release of the inflation data, the Fed commented that everything is going according to plan and that it will likely reduce the size of the interest rate hike to 0.25% in February (compared to 0.50% per hike in the past few quarters).

This means that it is increasingly likely that the Fed will be able to achieve a soft-landing (slowdown in inflation without causing a deep recession). When reality matches investors’ expectations, equity prices respond accordingly. In the past 3 months, the S&P 500 went up 10% while the Nasdaq rose 5.4% (I guess we are not in a bear market anymore).

That said, there is still a mismatch in expectations between the Fed and the market on how long the elevated interest rate regime will last. The Fed has warned the market that it is resolved to keep interest rates higher for a longer period (up to the end of 2023). Meanwhile, the market is already pricing a 60% probability that the Fed will cut rates in the second half of 2023 (see Figure 3 below).

There’s a contradiction embedded in these mismatched expectations. Both parties (the Fed and investors) want a soft landing (no recession), but one of them (investors) seems to be pricing a recession later this year:

- If the economy enters a recession, the Fed will have to lower interest rates much sooner, which is the prevailing market’s view. If this happens, the stock market (and other risky assets) may appreciate.

- If the economy continues to be strong (in particular wage growth and the unemployment rate, which is at a 50-year low in the US), the Fed will stay the course and hold rates above 5% for the year. This will translate to a decline in stocks.

Time will tell which party will be proven right.

Speaking of mismatched expectations…

The gas situation in Europe and the floating thermos

At the beginning of the Russian/Ukraine war, Russia used its status as one of the primary gas suppliers to Europe as leverage. As the war raged on, Russia started to restrict the natural gas supply to Europe. As a result, prices of natural gas went up more than 5x between January (before the war began) and September 2022 (see Figure 4 below).

At the time, the expectation was that supply would continue to be extremely constrained as winter enveloped much of Europe. Thus, the race to fill up reserve tanks was well underway toward the second half of 2022. So far, this year’s winter has been milder than in recent years (about 1.1 degrees Celsius warmer than average). As such, gas consumption is not as high, leaving European nations with about 88% of gas storage capacity filled, much higher than the typical year. As a result, prices have returned to pre-war levels.

This is another example where even the most apparent expectations did not manifest. An investor betting that European gas prices would continue to rise in the winter would’ve been badly burned.

The European energy crisis had other secondary effects. Before the war, Germany imported more than 55% of its natural gas needs from Russia. Currently, that level is zero due to the sabotage of the Nord Stream pipelines.

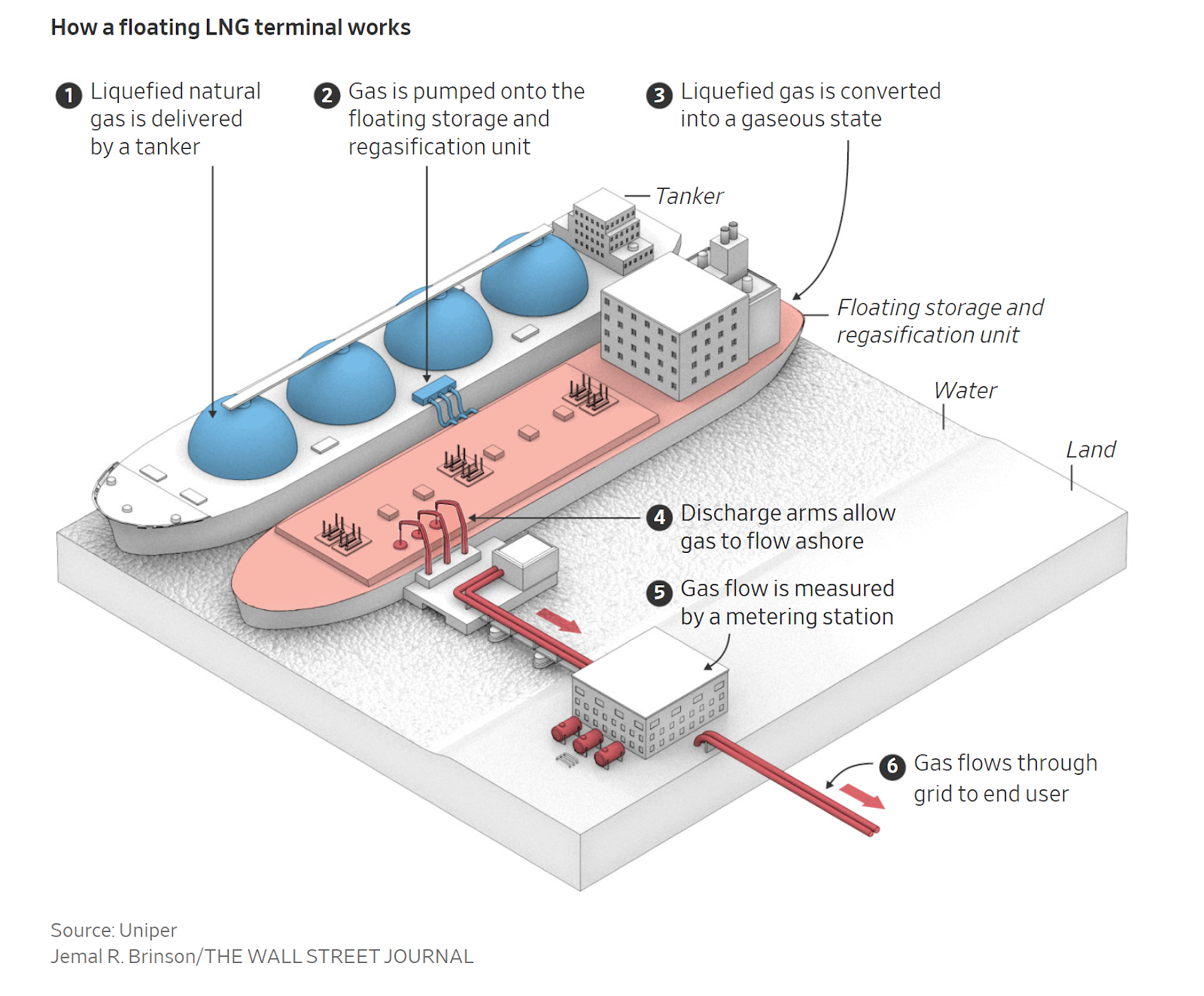

Despite facing this setback, Germany took drastic actions. To keep its economy afloat during the energy crisis, it needed to procure natural gas elsewhere. However, unlike coal or oil, transporting natural gas via the ocean is difficult and expensive. Natural gas must be chilled and liquefied during transport. This requires special shipping ports, transport ships, and receiving facilities.

At the time, Germany did not have enough capacity to receive liquefied natural gas (LNG). So it rushed to build more. It fast-tracked regulatory reviews and mobilized energy companies to accomplish the impossible, which was to build a new liquefied natural gas imports terminal, a task that typically requires 5 years to complete, in 9 months.

This strategy worked.

In December 2022, one of the first facilities was completed and received a shipment from the US. Currently, dozens of other LNG facilities are slated for construction across the EU. The region’s bid to end reliance on Russian fossil fuels will add at least $320 billion in infrastructure costs through 2030.

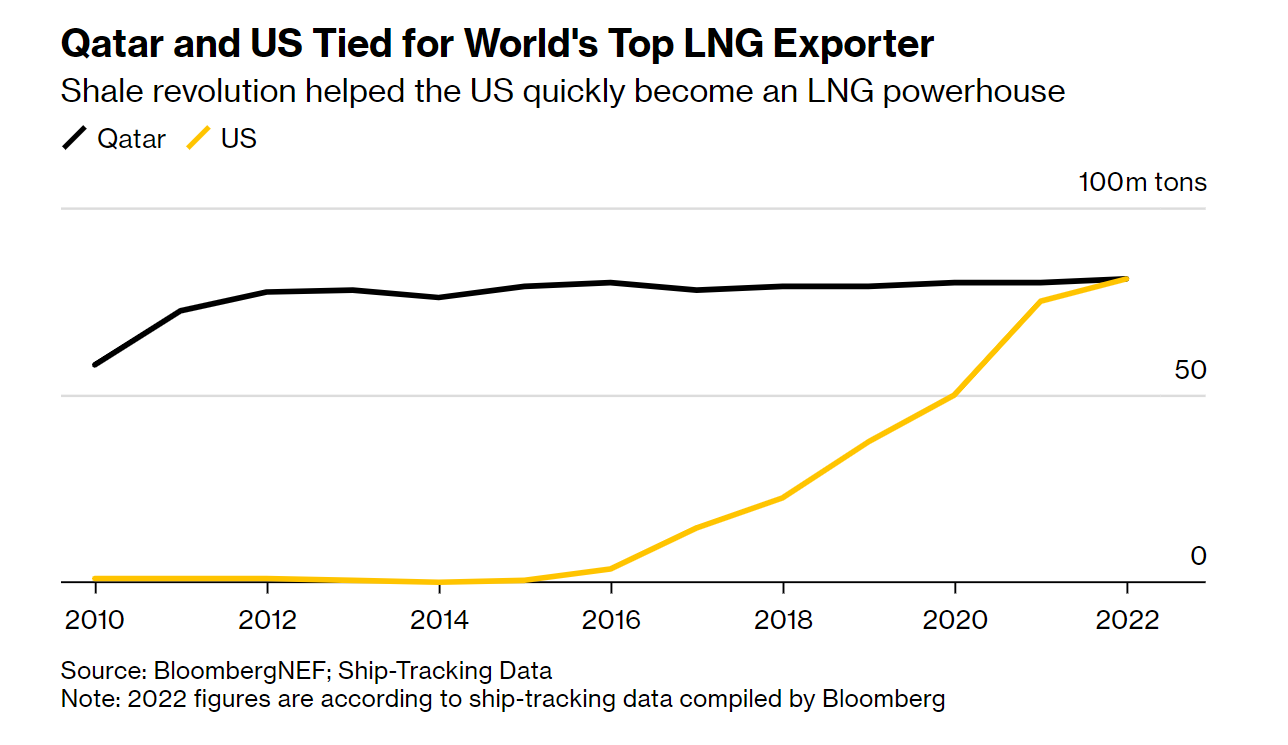

The energy trade divorce of Europe and Russia also benefited the US. Europe’s newfound hunger for LNG supply has helped the US grow into the number one LNG exporter in the world.