Skip to content

Skip to content

On March 6th 2022, both Visa and Mastercard announced that they would suspend their Russian operations. As a result, cards issued by Russian banks which use Visa and Mastercard networks will no longer work outside of Russia. Conversely, cards issued outside Russia will not work within Russia.

Visa and Mastercard represent a significant duopoly in the digital payments system, but one would be hard pressed to describe their business succinctly and accurately. Yet, their role is critical in facilitating global digital payments. Are they credit card issuers? Debit cards processors? Payment companies? Not quite – these descriptions do not capture the essence of the core value these two companies deliver.

Despite the innovation in digital payments (Apple/Google Pay or Buy Now Pay Later), these are still largely built on top of Visa and Mastercard.

To understand Visa and Mastercard, let’s discuss their origins first.

The history of Visa and Mastercard

In September 1958, the first credit cards were first introduced by Bank of America in Fresno, CA. These cards were delivered to unsuspecting consumers (back then, it was common for banks to send customers credit cards unprompted – the practice was only banned 12 years later). The first iteration of the credit card was not a smashing success, however. At over 20%, card delinquencies were much higher than expected. Fraudsters quickly figured out how to forge the cards, and merchants hated the 6% transaction fees that they had to bear.

Luckily, the credit card did not die. Over the years, Bank of America licensed its card system and provided accounting software and marketing support so that other banks could issue their own cards. But the system was still flawed and was at the verge of collapse. In order to understand what happened, we must first understand how credit card payments used to work.

When you swipe your credit card to buy an item, the transaction is recorded by your bank and the bank of the merchant. It was then the merchant’s bank responsibility to get the payment from your bank and settle the transaction. But as volumes grew, the system became difficult to manage. Unprocessed transactions, billing errors, and unreconciled ledgers made the system unreliable, and losses mounted.

Out of this chaos, Visa was born. The company came out of an effort to create a new organization to manage the ledger of transactions and ensure transactions cleared between banks. In other words, Visa’s “job to do†was to manage the exchange of value. From these humble beginnings, the company now processes more than $10 trillion in transactions annually.

Mastercard was born to perform similar functions, out of a different set of coalition of banks. Here’s what the flow of value and information looks like in a modern credit card system (Figure 1). The Visa and Mastercard systems act as the intermediary between the buyer and the seller. Although we are showing credit cards here, both companies play the same role for debit cards.

Nowadays, both systems are ubiquitous. Anywhere you go, Visa and Mastercards are accepted. However, in order to achieve this level of market penetration, both companies employ significant network effects:

- They incentivize consumers to use credit/debit cards (by giving them rewards – this is especially true for credit cards).

- Since a lot of consumers use Visa/Mastercard cards, merchants are incentivized to accept them. Usage of cards promotes frictionless payment. For this, merchants have to pay fees (called interchange fees, ranging from ~1% – 3% of transaction value). The merchants would happily pay this as not only do additional fees mean more frequent purchases, they can also outsource the credit underwriting, reconciliation, and other back office functions to Visa/Mastercard. Merchants also typically pass the cost to consumers.

- For banks, they are motivated to issue cards to earn more revenue (from a portion of the interchange fees or from interest rates).

So you end up with not just any network effect, but a powerful three-sided network effect. In his book, Zero to One, Peter Thiel outlined that any new entrant needs to be 10x better than the incumbent. This means that for any new entrant to successfully replace the Visa/Mastercard network, the new entrant has to be better for consumers, merchants, and banks. In other words, it has to be 10^3 or 1,000x better. That is no easy feat. As a result, Visa and Mastercard have very defensible businesses.

How Visa and Mastercard make money

Both companies have reached ubiquitous status in the digital payments space, especially in developed markets, and their total addressable market continues to expand as the transition from cash to digital payments continues. Excluding China, digital payments represent about 43% of consumer purchases, up from 28% in 2010. Currently, Visa has about 60% of the global payment share, while Mastercard has 30%, and American Express has 8.5%.

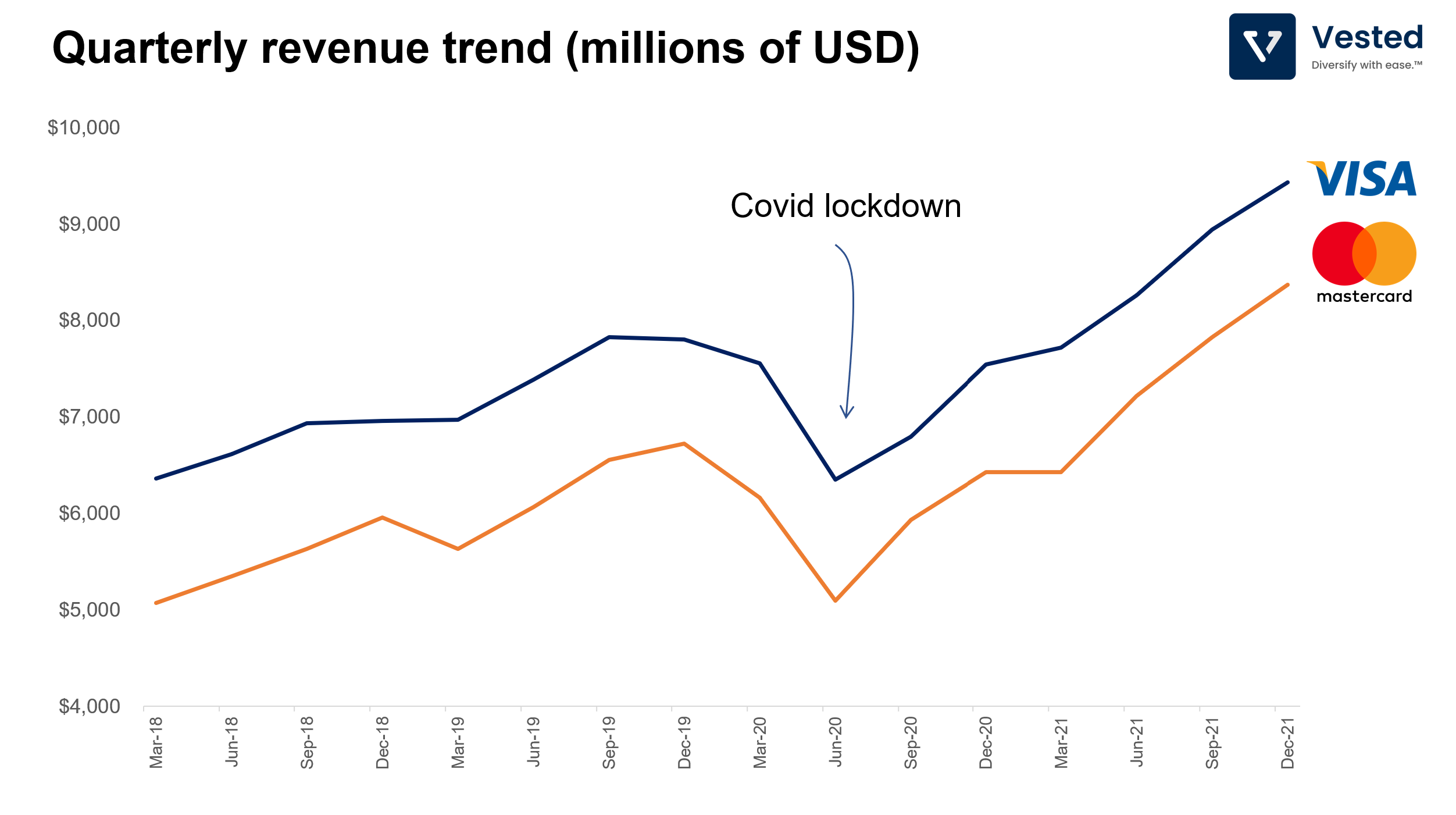

Because of this, revenues of both Visa and Mastercard are largely driven by macroeconomic sensitivity (revenue is a function of amount and volume of consumer spending). Figure 2 shows the quarterly revenue trends of the two companies from the past 4 years. As you can see, revenues of both companies dipped in Q2 of 2020, upon the global lockdown, but quickly rebounded as physical commerce was replaced by online transactions. By 2021, despite the lack of cross-border transactions/international travel which generates higher revenues, sales have returned to growth.

In Figure 2 above, you can clearly see that Visa is larger. But the revenue gap is narrowing (see the gap between the blue line vs. the orange line). Mastercard is growing its top line revenue faster than Visa. Four years ago, Visa generated 1.25x that of Mastercard’s revenue. At the end of the previous quarter, that ratio had shrunk to 1.13x.

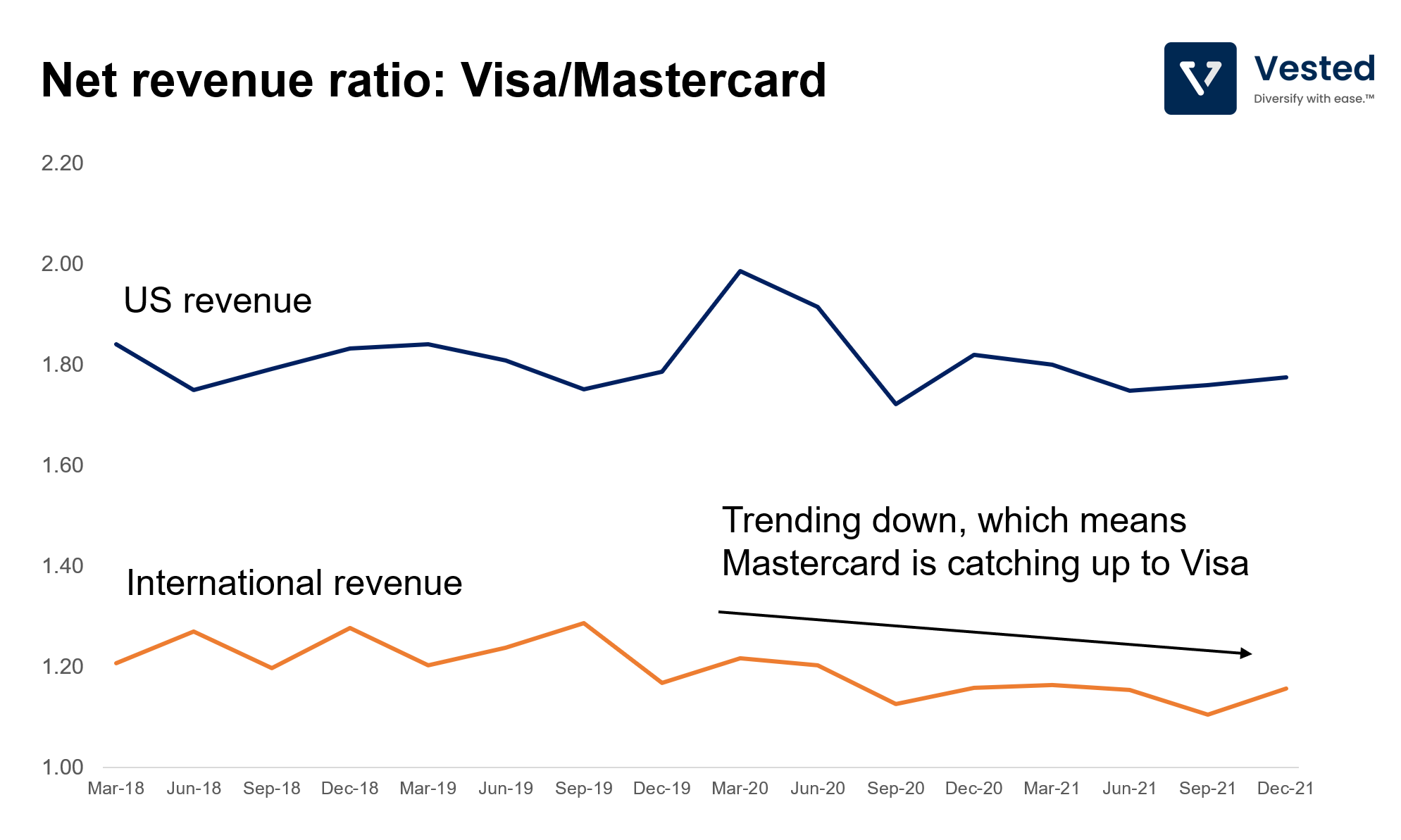

To understand which segment is the source of Mastercard’s growth, let’s plot the quarterly net revenue of Visa divided by that of Mastercard’s. See Figure 3 below.

It seems that the source of the growth for Mastercard is in the international markets (orange line in Figure 3). For the quarter ending in December 2021, Visa generated $3.9 billion, while Mastercard generated $3.4 billion. In contrast, Visa is much more dominant in the US, where it made $3.2 billion, much higher than the $1.8 billion Mastercard generated.

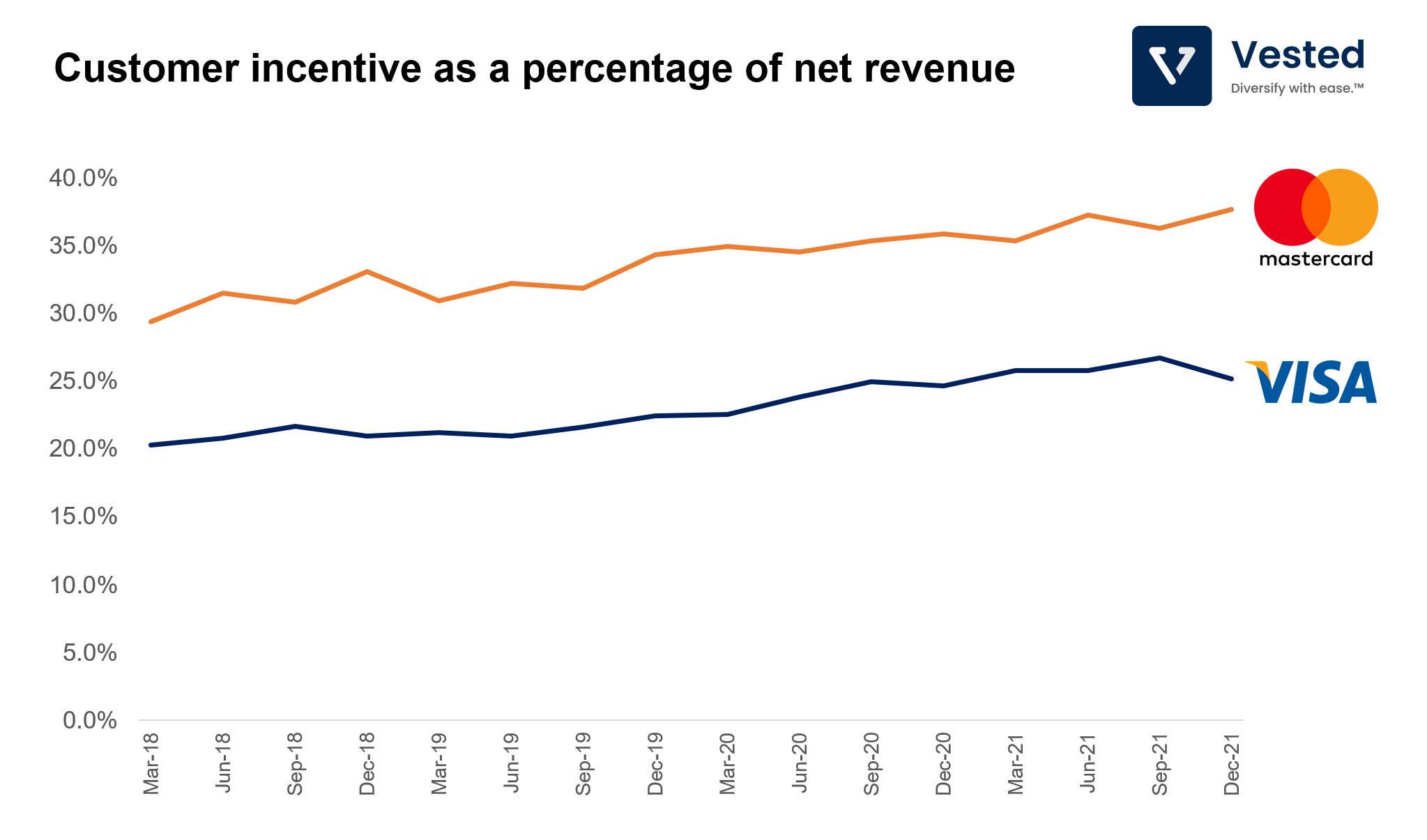

These gains do not come cheap, however. To promote growth, Mastercard spends more on user incentives (the amount of money it gives back to its customers, which you can think of as customer acquisition cost). Both companies employ this incentive strategy. But Mastercard spends more than Visa and has been increasing that spend more rapidly than Visa (see Figure 4 for the customer incentive spending as percentage of net revenue).

As a result, Visa is the more profitable company. Visa has an operating margin of 66%, while Mastercard has an operating margin of 54%. As of this writing, however, Wall Street seems to prefer the company that is less profitable, smaller, but growing the international business at a faster rate (Mastercard) – Mastercard is valued more highly than that of Visa. The price-to-earnings (P/E) ratio for the next twelve months are 29.6x (Visa) and 33.7x (Mastercard).

How it may all end

Ubiquity of network does not guarantee that either company will continue to thrive in the long term, however:

- In the emerging markets, as countries leapfrog their developed counterparts in developing their own payment systems, Visa and Mastercard are increasingly eliminated from the value chain. For example, India established its homegrown real time payment system, the UPI. While in South East Asia, as is the case in China, homegrown wallet solutions developed by the local super apps tend to dominate the digital payments landscape (the big four are: GrabPay, GoPay, AliPay and AirPay).

- Meanwhile in the US domestic market, payment companies such as Square (Block) are developing a payment system that disintermediates Visa and Mastercard completely, something that we discussed in depth.

As for the Russia shut down, for both networks, Russian transactions accounted for ~4% of net revenue, so this decision will result in a slight revenue headwind.