One of the most unusual ways to access global stocks through GIFT City is through instruments called UDRs, or Unsponsored Depository Receipts.

The name sounds technical, but the concept is not that difficult to understand.

What a UDR Actually Is

A depository receipt is not the actual share itself. It is a financial instrument that represents ownership of that share.

Think of it like a cloakroom token.

You hand over your jacket and receive a token in return. You do not carry the jacket around. The jacket stays safely inside the cloakroom. The token simply proves that the jacket belongs to you.

A UDR works on the same logic.

The actual Apple or Microsoft shares remain in custody in the United States, while what you buy and trade on the Indian exchange is a receipt that represents your claim on those shares.

If the price of the underlying share moves, the value of the receipt moves proportionally.

The second part of the name is unsponsored.

This simply means the company whose shares are being represented did not create the structure. Apple, Microsoft, or Google are not involved in issuing these instruments.

Instead, a financial intermediary builds the structure around shares that are already trading in the US market.

So if you hold an Apple UDR, Apple itself may not even know you exist as an investor. The company sees the custodian bank as the shareholder of record.

How the UDR Structure Works

The structure works through a chain of custody.

First, the actual shares are held in the United States.

These shares sit with Deutsche Bank’s New York branch, located at 60 Wall Street (in this case). The shares are held within the DTCC, which is the central clearing and settlement system for US securities markets. Almost every stock trade in the US ultimately settles through DTCC.

Deutsche Bank acts as the sub-custodian, physically holding the shares.

Second, inside India, HDFC Bank’s GIFT City branch, known as the IFSC Banking Unit (IBU), acts as the primary custodian. HDFC Bank holds the legal title to the shares on behalf of investors.

Third, investors themselves hold UDRs in a demat account maintained by CDSL IFSC Limited.

So the structure looks like this:

Your demat account → HDFC Bank IBU (custodian) → Deutsche Bank (US sub-custodian) → underlying shares

You hold the receipt. The custodian bank holds legal title. And the actual shares remain in the US market infrastructure.

Holding global stocks in your Indian demat account

One practical difference with UDRs compared to owning direct US stocks, say through Vested, is where your investments appear.

When you invest through an international brokerage platform, your global stocks sit in a separate account outside India. Your Apple or Microsoft shares are held with a US broker, while your Indian shares remain in your domestic demat account.

With UDRs, the structure is different.

The receipts you buy are credited directly to your demat account maintained with CDSL IFSC. This means the same demat account that holds your Indian stocks can also hold global companies.

So when you look at your holdings, you might see something like this:

- Reliance Industries

- Infosys

- TCS

- Apple UDR

- Microsoft UDR

Everything appears in one place.

For some investors, this consolidation is convenient. Instead of tracking investments across multiple platforms and jurisdictions, your entire equity portfolio sits inside the same demat infrastructure.

This can also simplify certain practical aspects of investing, such as:

- estate planning, where all securities are visible in a single account

- pledging securities for loans

- tracking overall portfolio value without logging into multiple platforms

The underlying shares still remain in custody in the United States, but the receipt representing your ownership sits inside your Indian demat account.

For investors who prefer a single, consolidated view of their holdings, this structure can be a useful feature of UDRs.

Fractional ownership through UDRs and trading hours

One another feature of UDRs is that they allow investors to buy a fraction of a US stock, rather than the entire share.

Many global companies trade at relatively high prices. A single share of companies like Amazon, Tesla, or Microsoft can easily cost a few hundred dollars. For investors who want exposure to several companies at once, buying full shares of each stock can quickly require a large amount of capital.

UDRs solve this by representing a fixed fraction of the underlying share (focus on the word fixed).

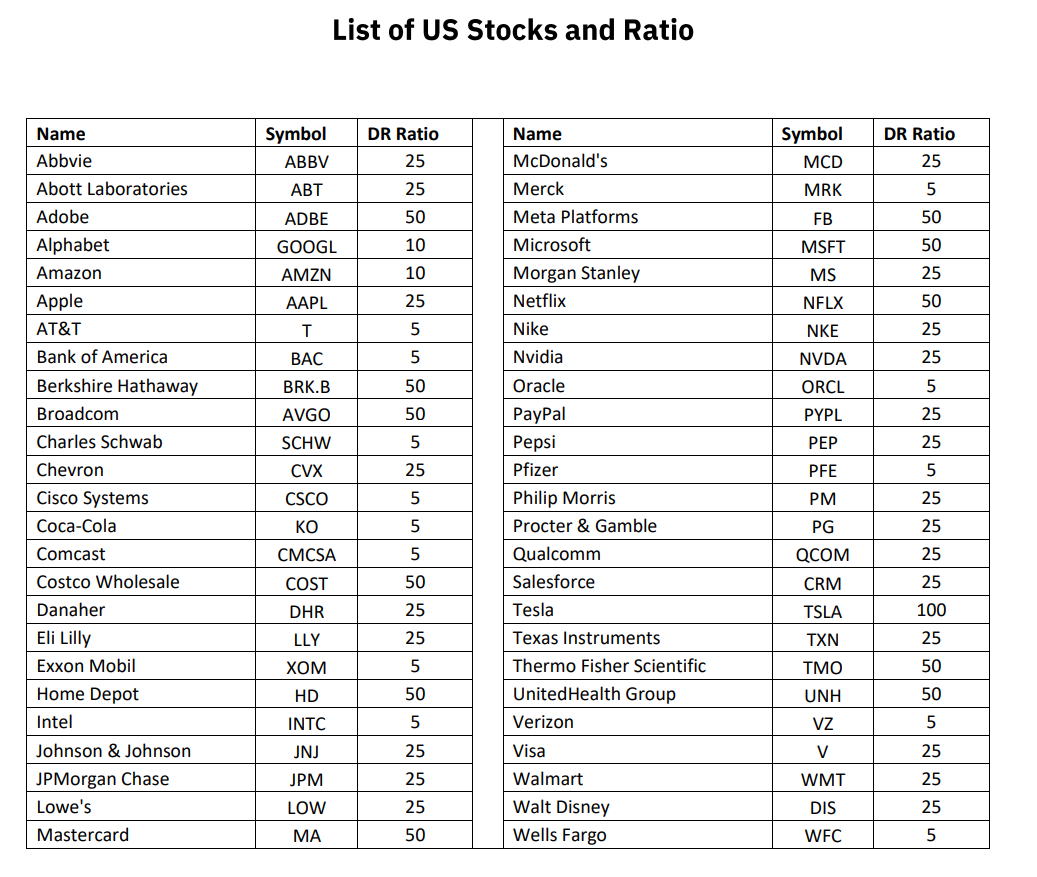

Each company has a specific conversion ratio.

For example, a ratio of 1:50 means that one UDR represents one fiftieth of a share. If Microsoft is trading at $400 in the US market, a single Microsoft UDR would be priced at roughly $8.

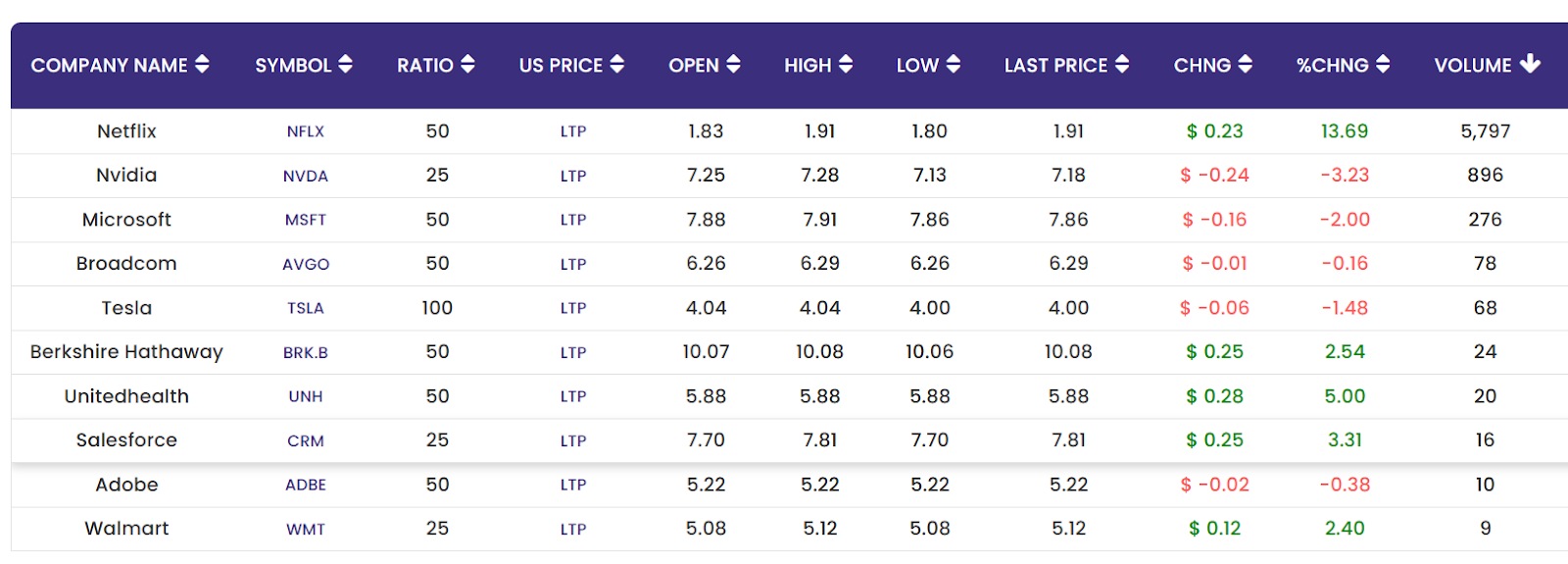

Here are a few examples from the current list.

If the underlying share rises by 10%, the value of the UDR also rises by about 10%. The economics remain the same. The only difference is that you are holding a smaller slice of the share.

This fractional structure makes global stocks more accessible for investors who prefer to build positions gradually rather than committing large amounts to a single company.

The trading hours for UDRs are designed to align with the US market.

UDRs trade on the NSE IFSC exchange from 7:00 PM to 1:30 AM Indian Standard Time, with slight adjustments when the United States shifts between standard time and daylight saving time.

This window overlaps with live trading on the New York Stock Exchange and Nasdaq. As a result, the price of a UDR reflects the real-time movement of the underlying stock.

If Netflix rises sharply at 9 PM Indian time while the US market is open, the Netflix UDR will move accordingly on the exchange. Investors are therefore trading based on the current market price of the underlying stock, not on the previous day’s closing price.

Now, it is also useful to compare this structure with owning the stock directly through a US brokerage account.

When you buy shares through a platform like Vested, you also have access to fractional ownership (more on its working in the later chapter). The broker allows you to purchase a portion of a share based on the dollar amount you invest – one can invest with as just $1 (this is a plus vs fixed proportion as in the case of UDRs).

For example, you might invest $50 in Apple even if a full share costs $250. The broker records the fractional ownership inside your brokerage account.

With UDRs, the fractional structure is built into the instrument itself through the fixed conversion ratio between the receipt and the underlying share.

Cost

It is important to understand the cost structure of UDRs because there are a few layers involved, and some of them are not immediately obvious.

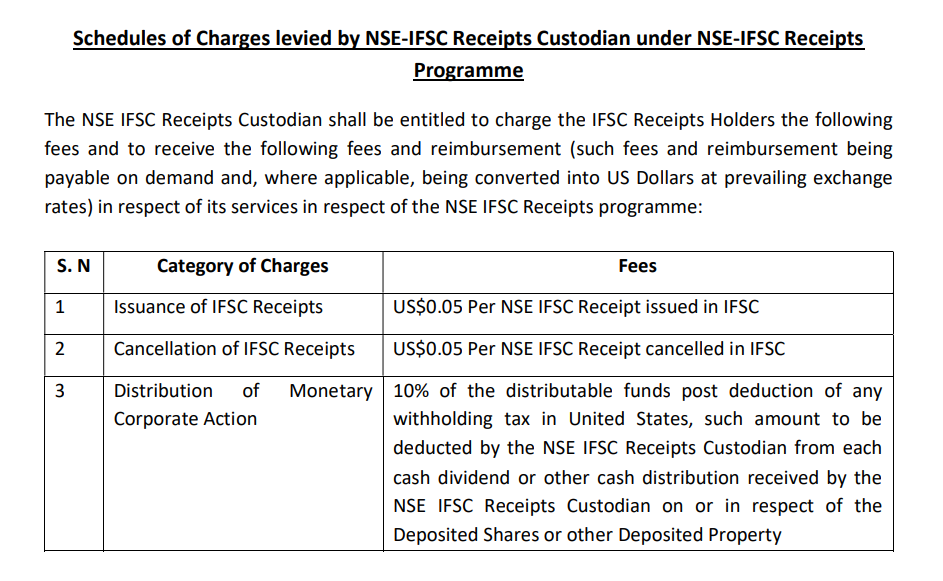

The first cost comes from the issuance of the UDR itself.

When you buy a UDR, the custodian has to create that receipt against the underlying shares held in custody. For this process, HDFC Bank’s IFSC Banking Unit charges an issuance fee of $0.05 per UDR.

This fee applies per receipt, not per transaction.

Take an example. Suppose you want to invest in Microsoft.

If Microsoft is trading at $400 per share in the US market, and the UDR ratio is 1:50, then you need 50 Microsoft UDRs to represent one full Microsoft share.

Now, let us look at the issuance cost.

50 UDRs × $0.05 issuance fee = $2.50

So the moment you buy UDRs equivalent to one Microsoft share, $2.50 goes towards issuance fees.

If you later decide to convert those UDRs into the actual underlying shares and transfer them to a US brokerage account, the same $0.05 per UDR cancellation fee applies again.

That means another $2.50 in cancellation charges for those 50 UDRs.

On top of these custodian fees, investors also incur the usual trading-related costs such as:

- brokerage charged by the NSE IFSC broker

- exchange transaction charges

- annual demat account maintenance charges

These costs vary depending on the broker through which the trade is executed.

Now it helps to compare this with direct investing through a global brokerage platform like Vested.

On Vested, there is no per-share issuance charge because you are buying the stock directly. Instead, the platform charges a percentage-based brokerage fee on the trade value.

The fee structure typically looks like this:

- 0.25% on the Basic plan

- 0.15% on the Premium plan

Let us use the same Microsoft example.

If you buy $400 worth of Microsoft shares directly through Vested, the brokerage cost would be:

- Basic plan: $400 × 0.25% = $1

- Premium plan: $400 × 0.15% = $0.60

So for the equivalent of one Microsoft share:

- UDR issuance cost: about $2.50

- Vested brokerage cost: between $0.60 and $1

For investors making frequent investments, the percentage-based brokerage model can therefore work out cheaper.

There is another cost associated with UDRs: dividends.

When a US company declares a cash dividend, the money flows through the custody chain before it reaches you.

The company pays it to Deutsche Bank in New York. Deutsche Bank passes it to HDFC Bank IBU in GIFT City.

Before HDFC Bank sends anything to your account, two deductions happen, one after the other.

The first is the US withholding tax of 25%. This applies to all Indian investors in US stocks — whether you are on Vested or UDRs.

There is no way around it. On a $1 dividend, $0.25 goes to the US government and $0.75 remains.

The second is HDFC Bank IBU’s own distribution fee of 10% of whatever is left after withholding tax. On the $0.75 that remains, HDFC Bank takes $0.075 as its fee. You receive $0.675.

So from a $1 dividend, you get $0.675. That is a combined drag of 32.5%.

On Vested, the same $1 dividend would go through the 25% US withholding tax, leaving $0.75. Vested does not charge an additional distribution fee. You receive $0.75.

The 10% custodian distribution fee is a real cost, and it adds up if you are holding dividend-paying stocks. Companies like Johnson & Johnson, Procter & Gamble, Coca-Cola, or Walmart, which are all available as UDRs, pay meaningful dividends.

If dividend income is part of your plan, you should factor this in.

Shareholder rights, conversion, and the current availability of companies

Before investing through UDRs, it is also important to understand what you do and do not receive as a holder of these instruments.

When you buy a UDR, you receive the economic benefits of the underlying share. If the stock price rises, the value of your UDR rises in the same proportion. If the company declares a dividend, that dividend flows through the custody chain and is credited to you after the applicable taxes and fees.

However, you are not the registered shareholder of the company.

The legal shareholder on record is the custodian bank that holds the shares in custody, which in this structure is HDFC Bank’s IFSC Banking Unit. Because of this, certain shareholder rights do not pass directly to UDR holders.

For example, you cannot vote at shareholder meetings. Decisions such as board elections, executive compensation approvals, or other shareholder votes are handled at the custodian level.

This, for some investors, is a dealbreaker.

Similarly, discretionary corporate actions do not pass through in the same way they would for a direct shareholder.

If a company offers a rights issue, where shareholders are given the option to buy additional shares, you cannot participate directly. The same applies to certain types of tender offers or buybacks where shareholders must individually decide whether to participate.

In such situations, the custodian manages the process. In many cases, the rights may simply lapse, or the custodian may sell them and distribute the proceeds.

For most investors who are primarily buying these stocks for market exposure and capital appreciation, this limitation does not significantly affect the investment outcome. You still receive the price movement and dividend income linked to the underlying share.

Another feature of UDRs is that they can be converted into actual shares if an investor wishes to move them to a US brokerage account.

This process involves submitting a cancellation request. Once the request is processed, the UDRs are cancelled and the corresponding underlying shares are transferred through the US settlement system to the investor’s brokerage account.

There is one condition.

The UDRs must add up to a whole underlying share.

For example, if one Apple share corresponds to 25 Apple UDRs, then you need to hold 25 UDRs in order to convert them into one full Apple share. Fractional UDR holdings cannot be converted.

The $0.05 cancellation fee per UDR applies during this process as well.

Finally, it is worth noting the current availability of these instruments.

At present, around 50 US companies are available as UDRs on the NSE IFSC exchange. These companies are largely drawn from the S&P 500, covering sectors such as technology, consumer goods, and healthcare.

The exchange has indicated plans to expand this list to around 100 companies over time, and there are also discussions around introducing US-listed ETFs in the future.

If ETFs are eventually added, investors could potentially gain exposure to indices such as the S&P 500 or Nasdaq-100 directly through their Indian demat account, without opening a separate international brokerage account.

UDRs vs Direct ownership through global platforms such as Vested

Too much information, I agree 🙂

The table below summarises the key differences between holding US stocks through UDRs in your demat account and owning the shares directly through a global investing platform such as Vested.

| Feature | UDRs (GIFT City – NSE IFSC) | Direct Shares through Vested |

| What you hold | A depository receipt representing the share | The actual share held through a US broker |

| Where it appears | In your Indian demat account (CDSL IFSC) | In your US brokerage account |

| Legal shareholder | Custodian bank (HDFC Bank IBU) | You are the beneficial owner through the broker |

| Voting rights | Not available | Available |

| Corporate actions | Managed by custodian | Investors can participate |

| Fractional investing | Built into UDR ratio | Broker provides fractional shares |

| Dividend flow | 25% US withholding tax + 10% custodian fee | 25% US withholding tax |

| Trading hours | 7:00 PM – 1:30 AM IST | Same US market hours |

| Fees | $0.05 per UDR issuance + broker charges | 0.25% (Basic) or 0.15% (Premium) trade fee |

| Conversion | Can convert to actual shares if UDRs equal a full share | Already held as actual shares |

Essentially, UDRs offer the convenience of seeing global stocks inside the same demat account as Indian equities but with limited investing options.

Direct international investing, on the other hand, provides full shareholder rights and typically lower transaction costs for smaller purchases and many more options to invest in.

Comments

Login or register to join the conversation.