This is the part that surprises most people when they first encounter it.

When you redeem your GIFT City fund units, you pay zero capital gains tax. Not 12.5%. Not slab rate. Zero.

That sounds too good to be true. So let us understand exactly where the tax goes.

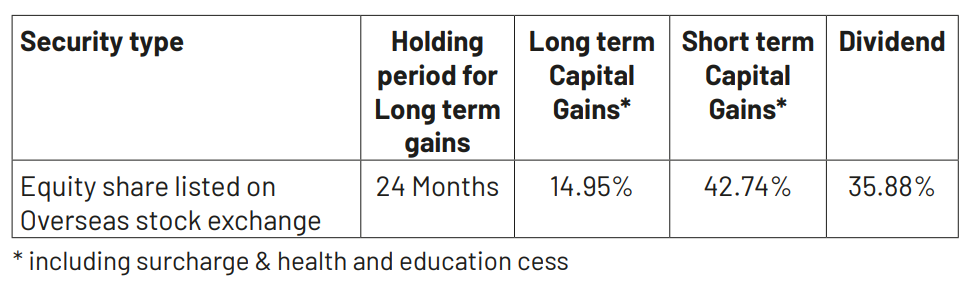

The tax is paid at the fund level, not the investor level. When the fund manager sells a stock inside the fund, say the fund bought Apple at $150 and is now selling it at $200, that is a capital gain for the fund. The fund itself pays tax on that gain. The rate depends on how long the fund held the stock. For holdings sold within two years, the tax rate is approximately 43%. For holdings sold after two years, the rate drops to approximately 15%.

Source: DSP Mutual Fund

These taxes reduce the fund’s NAV. So you do bear the tax impact, just indirectly through a lower NAV rather than a direct deduction when you sell your units.

This structure exists because it mirrors how funds operate in other international financial centres. In Ireland, Luxembourg, and Singapore, the fund is typically the taxpaying entity rather than the individual investor.

Now here is the part that matters most practically.

If a fund makes a 20% return on a trade but holds the stock for less than two years, after paying 43% tax at the fund level, the net return reflected in the NAV is only about 11.4%. Nearly half the gain has gone to tax. But if the fund held that stock for more than two years and paid only 15% tax, the same 20% gain becomes a 17% gain after tax.

The difference is huge, actually.

Two GIFT City Funds investing in identical stocks can deliver meaningfully different returns simply because one trades more actively than the other. This dimension of fund selection does not exist with regular mutual funds or global funds, and it is worth paying attention to before you invest.

When evaluating a GIFT City fund, it is worth asking about the fund’s typical holding period, whether the manager follows a buy-and-hold philosophy or trades actively, and what the portfolio turnover ratio looks like. Lower turnover and longer holding periods mean less tax drag at the fund level, which means more of the returns flow through to your NAV.

This is also why the passive Parag Parikh funds have a structural advantage (for now and only time will tell) from a tax perspective.

Index funds, by design, hold stocks for long periods and trade infrequently. Their turnover is low. That means the fund-level tax they pay skews heavily toward the 15% long-term rate rather than the 43% short-term rate.

Comments

Login or register to join the conversation.