At this point, the question is: if international ETFs are already available in India, why would someone go through the process of transferring money and buying the same ETF in the US through a broker such as Vested?

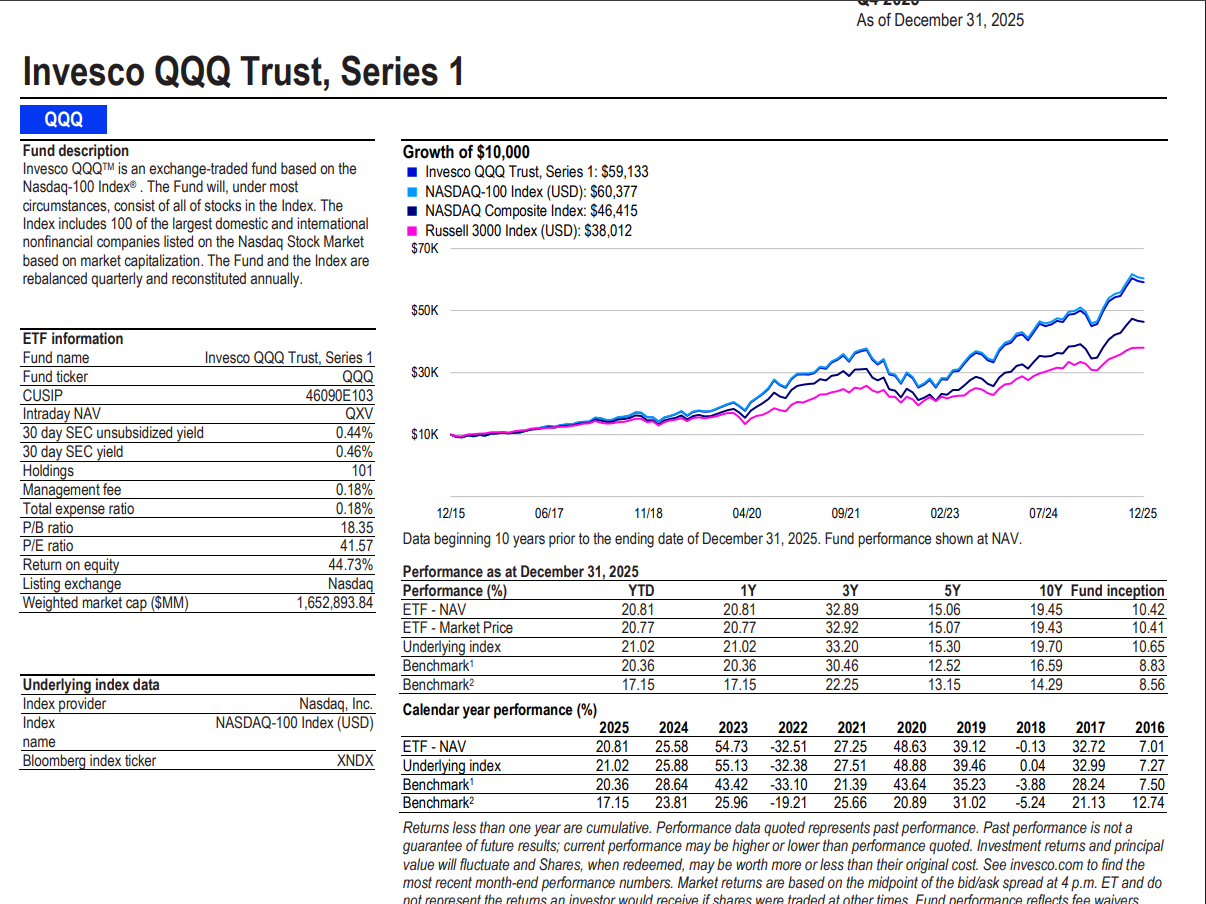

After all, both options appear to give exposure to the same underlying market. Whether you buy a NASDAQ ETF in India or buy QQQ (Invesco QQQ Trust, Series 1) directly in the US (more on US ETFs in the next chapters), the underlying companies are largely the same: Apple, Microsoft, Nvidia, Amazon, and others that make up the NASDAQ-100 index.

So what is the practical difference?

The difference lies in how you access the investment, and that affects cost, flexibility, and operational complexity.

When you buy an India-listed international ETF, the entire transaction happens within the Indian financial system. You invest in rupees, buy the ETF through your Indian bank and broking account, and trade during Indian market hours.

There is no need to remit money abroad, which means the investment does not use your LRS limit (we discussed this at length in Chapter 1). You also avoid foreign brokerage accounts and the annual foreign asset disclosure requirements that come with them.

The expense ratios for India-listed international ETFs generally fall around 0.5 to 0.6% per year.

Buying the ETF directly in the US works differently.

To do that, you first send money abroad under the Liberalised Remittance Scheme (LRS). The money is converted into US dollars and credited to your brokerage account, say Vested. From there, you can buy ETFs listed on US exchanges.

This route gives investors access to a much larger universe of ETFs and strategies. Many of the largest global ETFs also have lower expense ratios, often around 0.15 to 0.20% per year.

However, the process involves a few additional steps. You pay foreign exchange conversion costs and brokerage charges when bringing money back to India. You also have to declare foreign assets every year in Schedule FA when filing your tax return.

So the trade-off is fairly straightforward.

The India-listed ETF route wins on simplicity and convenience. The direct US ETF route wins on cost efficiency and wider investment choice, especially for larger investment amounts.

An actual example helps illustrate this.

The Invesco QQQ Trust, which tracks the NASDAQ-100 index, delivered a 3-year USD CAGR of 32.89%. After adjusting for roughly 3% annual depreciation of the rupee, that translates to approximately 35.89% in INR terms.

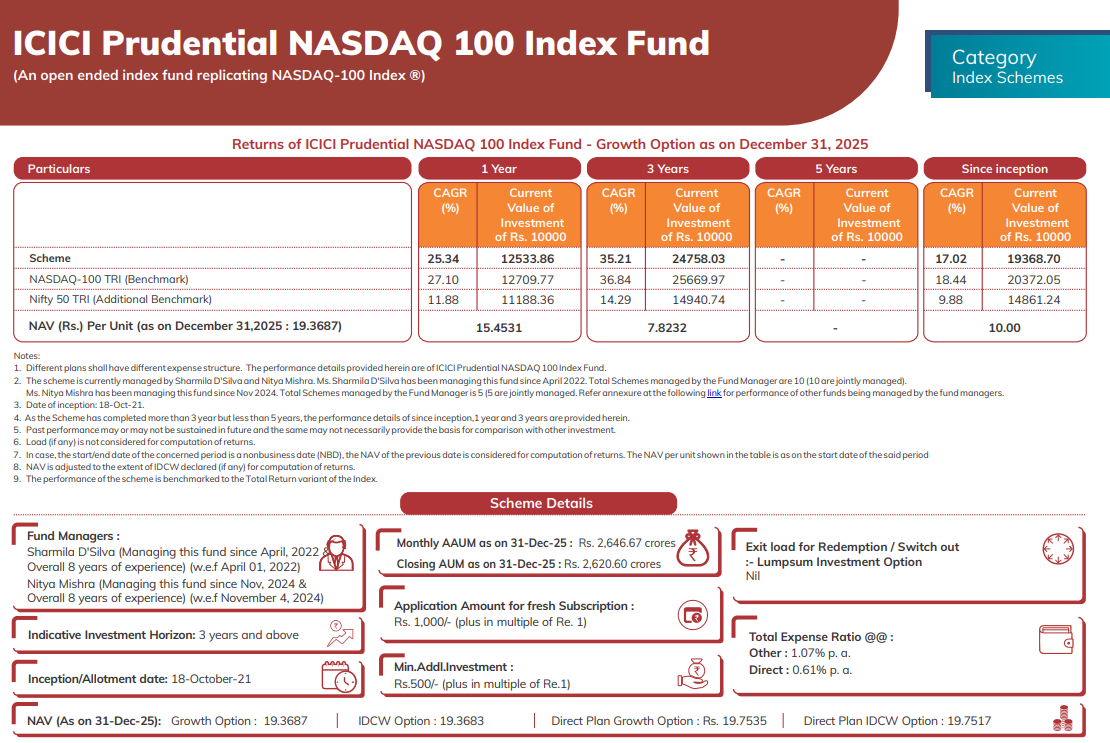

Over the same period, the ICICI Prudential NASDAQ 100 Index Fund delivered 35.21% in INR terms.

Before transaction costs, the direct US ETF route therefore shows a slight return advantage.

However, buying QQQ requires sending money abroad, paying brokerage, absorbing the FX spread during currency conversion, and paying withdrawal fees when bringing money back.

On an investment of ₹10 lakh over three years, these friction costs can add up to roughly ₹12,900.

Even after accounting for those costs, the direct QQQ investment still ends up ahead by about ₹27,000 on a ₹10 lakh investment over three years, which works out to roughly 1.1% higher total return.

The picture changes when the investment amount is smaller.

On a ₹1 lakh investment, the difference over three years shrinks considerably. In this case, QQQ ends up ahead by only about ₹2,350. At that level, the additional operational steps and transaction costs largely offset the advantage.

The pattern becomes clearer when viewed this way.

The direct US ETF route benefits from lower ongoing costs, which compound over time. But the route also involves fixed transaction and operational costs that matter more when the investment amount is small.

For smaller investments, the simplicity of India-listed ETFs may outweigh the marginal cost advantage. As the investment size increases, the lower expense ratios of US ETFs start to make a more noticeable difference.

From a tax perspective, the treatment is broadly similar.

India-listed international ETFs are taxed under Section 50AA, the same rules that apply to feeder funds. Gains within 24 months are taxed at your slab rate, and gains after 24 months are taxed at 12.5% without indexation.

Directly held US ETFs follow similar capital gains treatment under Indian tax rules for foreign securities, along with the requirement to disclose them in your annual tax filings.

Comments

Login or register to join the conversation.