At this point, a natural question usually comes up.

If LRS allows individuals to send money abroad for so many different purposes, how does the regulator actually know why the money is leaving the country? How does the RBI track whether it is being used for investment, travel, education, or something else?

This is where an important operational detail comes in.

Before we get to that, it helps to understand the boundaries of the framework itself.

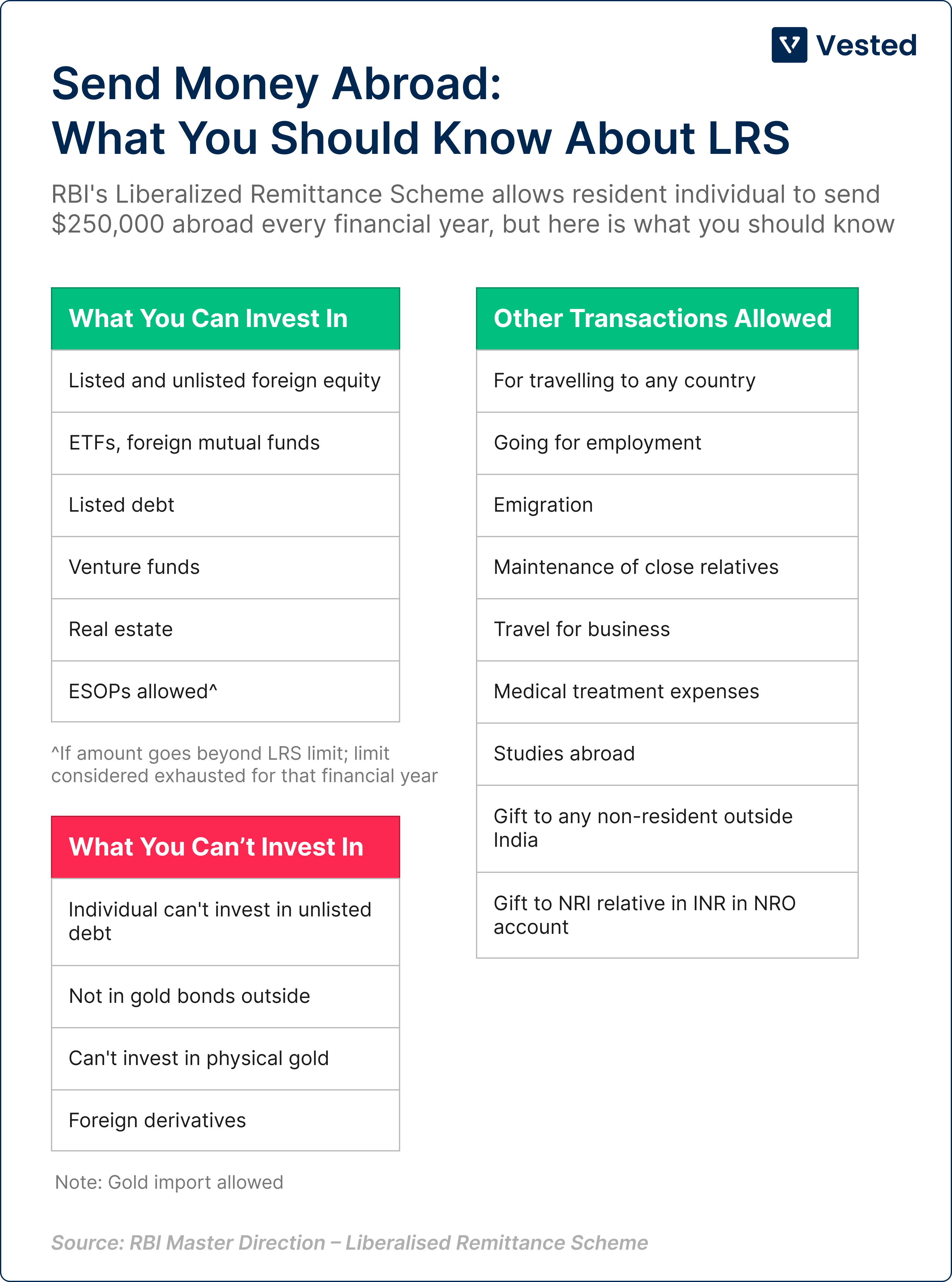

LRS is quite broad in what it permits.

As a resident individual, I can use it to invest in foreign stocks, ETFs, global funds, bonds, or even real estate abroad. I can send money for education, medical treatment, or travel. I can gift funds to relatives, maintain dependents living overseas, make donations to foreign charities, or even set up a foreign business as an individual.

So the framework does not restrict legitimate global financial activity. In many ways, it enables it.

At the same time, certain transactions are clearly not allowed.

For instance, LRS cannot be used for lottery tickets, sweepstakes, margin trading, leveraged derivatives (including any form of Futures and Options in global markets), or speculative forex trading abroad. Remittances to countries flagged by Financial Action Task Force, or popularly known as FATF as high-risk or to entities linked to terrorism are also prohibited.

There is also one rule that surprises many people.

LRS is meant only for resident individuals. Businesses, partnership firms, HUFs, and trusts cannot use this route.

Now, coming back to the earlier question.

If the system allows so many different uses, how does the RBI know the purpose of each remittance?

The answer lies in something called purpose codes.

Whenever I make a remittance under LRS, the bank requires me to tag the transaction with a specific RBI-defined code. These codes standardise the reason for the transfer and allow regulators to track the flow of funds across categories.

So when I fill out a remittance form, I do not just write “investment”. I select the exact category that describes the transaction.

In a way, it works just like the airport example we discussed earlier. The question is not just whether something is leaving the country. The system also records what it is and why it is being carried out.

Some commonly used purpose codes include:

- S0001 – Investment in foreign equity (stocks and ETFs)

- S0002 – Investment in foreign debt instruments (bonds)

- S0301 – Personal travel

- S1301 – Maintenance of close relatives abroad

- S1302 – Gifts to individuals overseas

The RBI publishes the complete list – you can refer to the appropriate code before making a remittance.

Choosing the wrong code can affect the tax treatment of the transaction and sometimes lead to delays or rejection by the bank.

In practice, this usually becomes visible at the moment you transfer money.

If you are making a manual outward remittance through your bank, you will typically be asked to fill out a remittance form. Along with details like the beneficiary and amount, you also need to select the correct RBI purpose code that describes why the money is being sent abroad.

So if the transfer is for investing in foreign stocks, the form must reflect the appropriate investment code (S0001). If it is for education, travel, or gifting, the code will be different.

However, the experience can look quite different when the platform you are using is integrated directly with banks.

For example, in the case of Vested, several partner banks (including HDFC Bank, ICICI Bank, Axis Bank and IDFC First Bank) are integrated end-to-end with the fund transfer process. Because the infrastructure is already built around overseas investing, the correct purpose code for investment remittances is pre-configured in the backend.

So as an investor, you do not have to manually figure out which code to select each time.

This is one of the advantages of using a localized infrastructure built specifically for global investing. Many of the regulatory and operational details are already mapped within the system, which makes the experience simpler for the investor while still remaining compliant with the RBI framework.

Comments

Login or register to join the conversation.