In the last section, we walked through what happens when you actually send money abroad: the form, the declaration, the purpose code, the bank acting as the gatekeeper.

Now let me take that one step forward.

Imagine this.

You have been investing globally for a few months. You transferred and invested ₹3 lakh. Then ₹4 lakh. Everything went exactly as planned. The amount you entered is the amount that got debited.

And then one day, you initiate another transfer, and the debit is slightly higher than you expected.

That’s usually when people discover TCS.

So what just happened?

When your total outward remittances under LRS cross a certain level in a financial year, banks are required to collect Tax Collected at Source (TCS) at the time of transfer.

It was introduced under the Finance Act, 2020.

But pause here, because this is important: TCS is not an extra cost of global investing. It is not a penalty, either. It is simply an advanced tax collected upfront.

Your bank collects it and deposits it with the Income Tax Department. When you file your tax return, that amount is adjusted against your final tax liability.

If excess tax were collected, you would get it back. So, effectively, the money is not lost. It is just that the tax is paid earlier.

Why does the system work this way?

If you think back to everything we have discussed so far – limits, declarations, purpose codes – you will see that everything is part of the system designed.

Effectively, the system is designed for visibility.

Large outward remittances represent meaningful capital movement. TCS is simply another layer of tracking and early tax capture within that framework.

When does TCS actually apply?

Here’s where the story becomes practical.

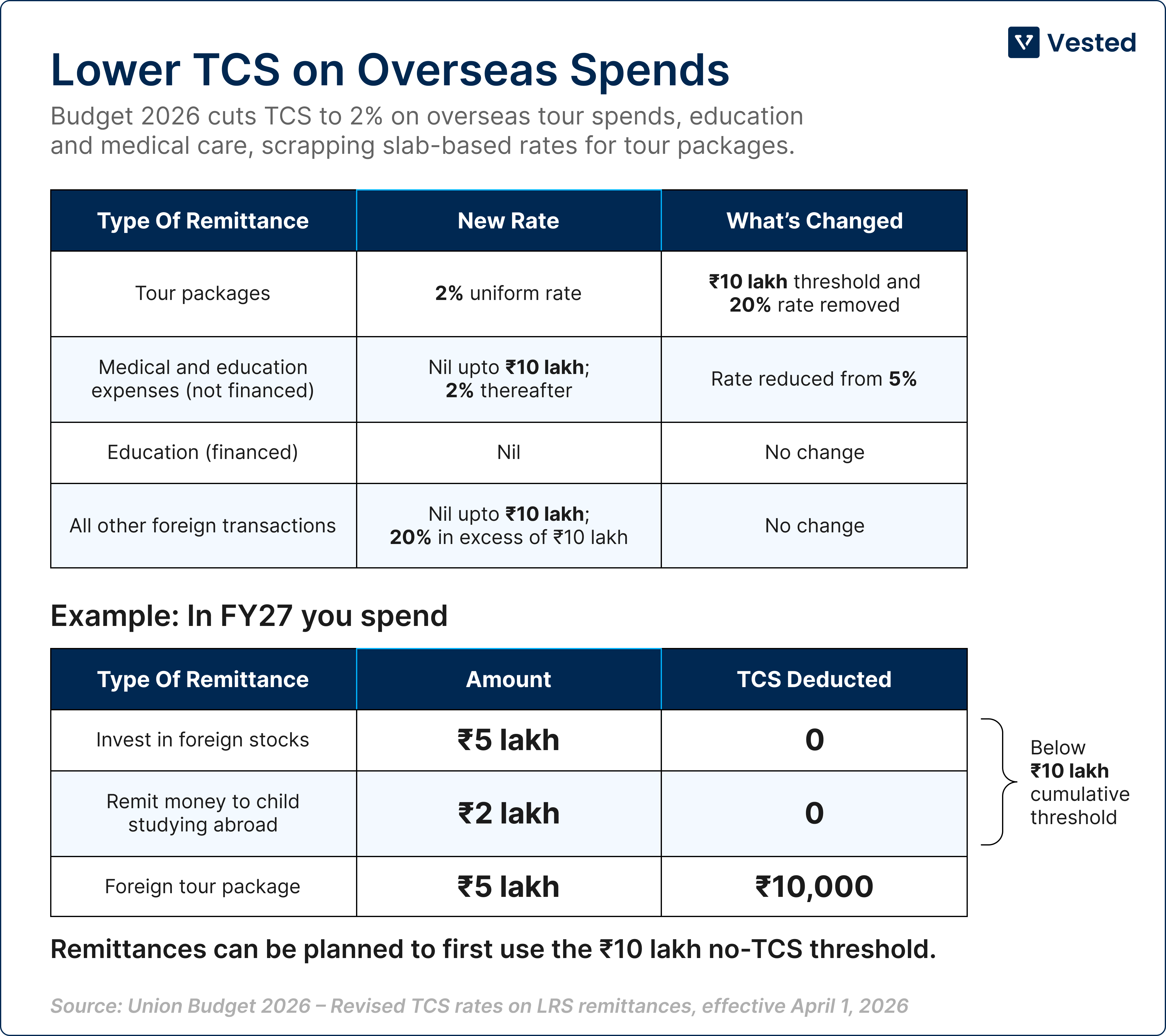

There is one number to remember: ₹10 lakh in a financial year.

As long as your total outward remittances under LRS stay below ₹10 lakh, no TCS applies (except for overseas tour packages, which have their own rule).

The moment your total remittances cross ₹10 lakh, TCS applies but only on the amount exceeding ₹10 lakh.

And the rate depends on what the money is for.

If you are investing in foreign stocks, ETFs or global funds: 20% TCS applies on the portion exceeding ₹10 lakh.

If the remittance is for education or medical treatment abroad: 2% TCS applies on the portion exceeding ₹10 lakh. (And if the education is funded through an approved loan, no TCS applies.)

For overseas tour packages: 2% TCS applies from the first rupee.

Now, what happens to that deducted amount?

TCS is collected in rupees before currency conversion.

So when you send money, you need slightly more funds in your bank account to cover the tax component. The full intended investment amount still reaches your brokerage account. The TCS portion goes separately to the government.

Later, when you file your tax return:

- If you owe tax, this reduces your payable amount.

- If you don’t, you receive a refund.

The only friction is time. Refunds can take a few months. Until then, that portion of capital feels temporarily locked.

But here’s the part most investors don’t realise

If you are salaried, there are ways to manage this better.

Instead of waiting passively for a refund, TCS can often be adjusted against your regular salary TDS during the year. With some planning and sometimes coordination with your employer or CA – the cash-flow impact can be significantly reduced.

We have written a detailed guide explaining exactly how this works:

- How TCS reflects in Form 26AS

- How to offset it against salary TDS

- When advance tax adjustments help

- What steps to take during the financial year

If you expect your remittances to cross ₹10 lakh, I strongly recommend reading the following: How TCS on Foreign Investments Can Be Adjusted Against Salary TDS — A Complete Guide

Comments

Login or register to join the conversation.