Let’s take a well-known example so this becomes easy to understand.

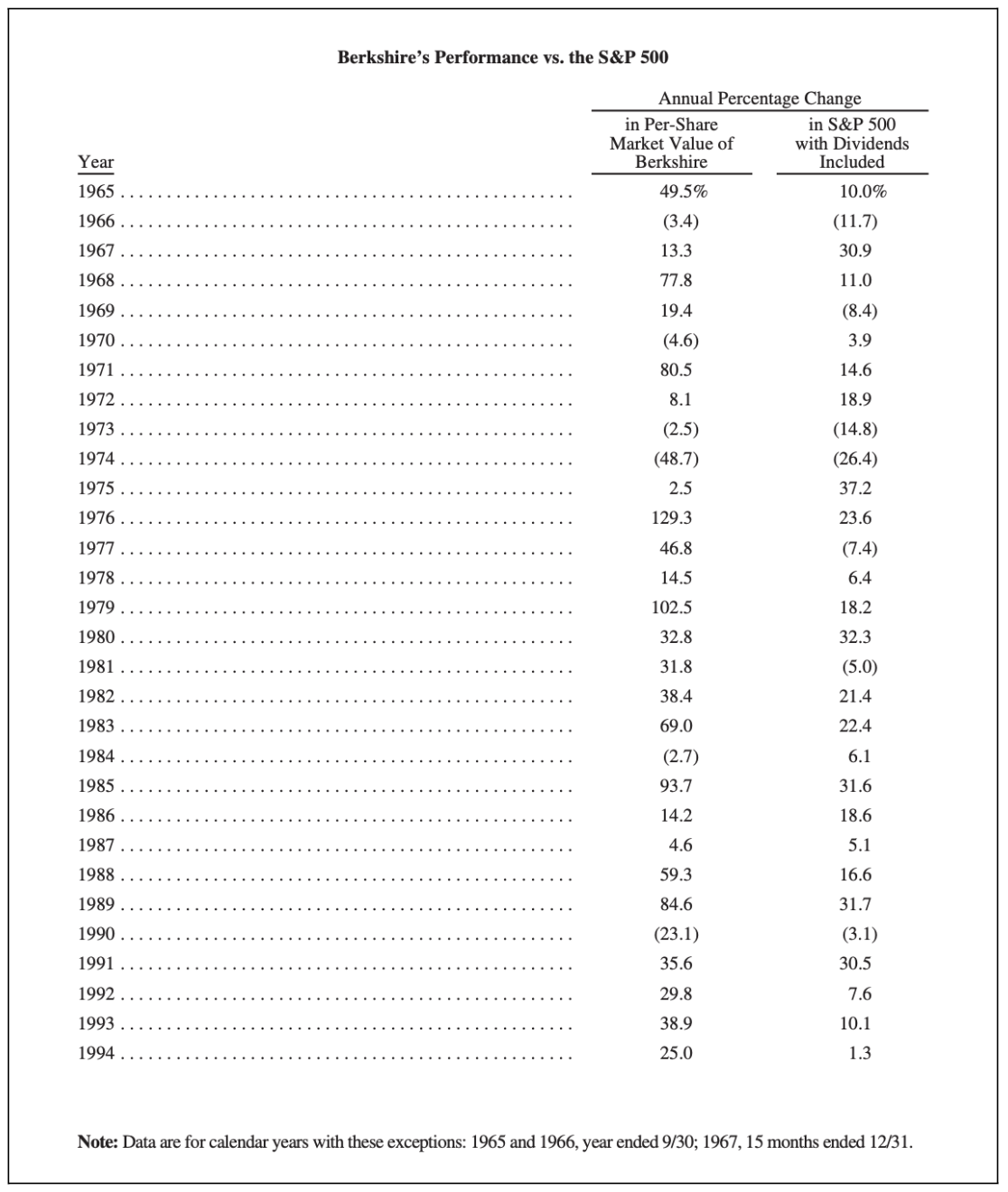

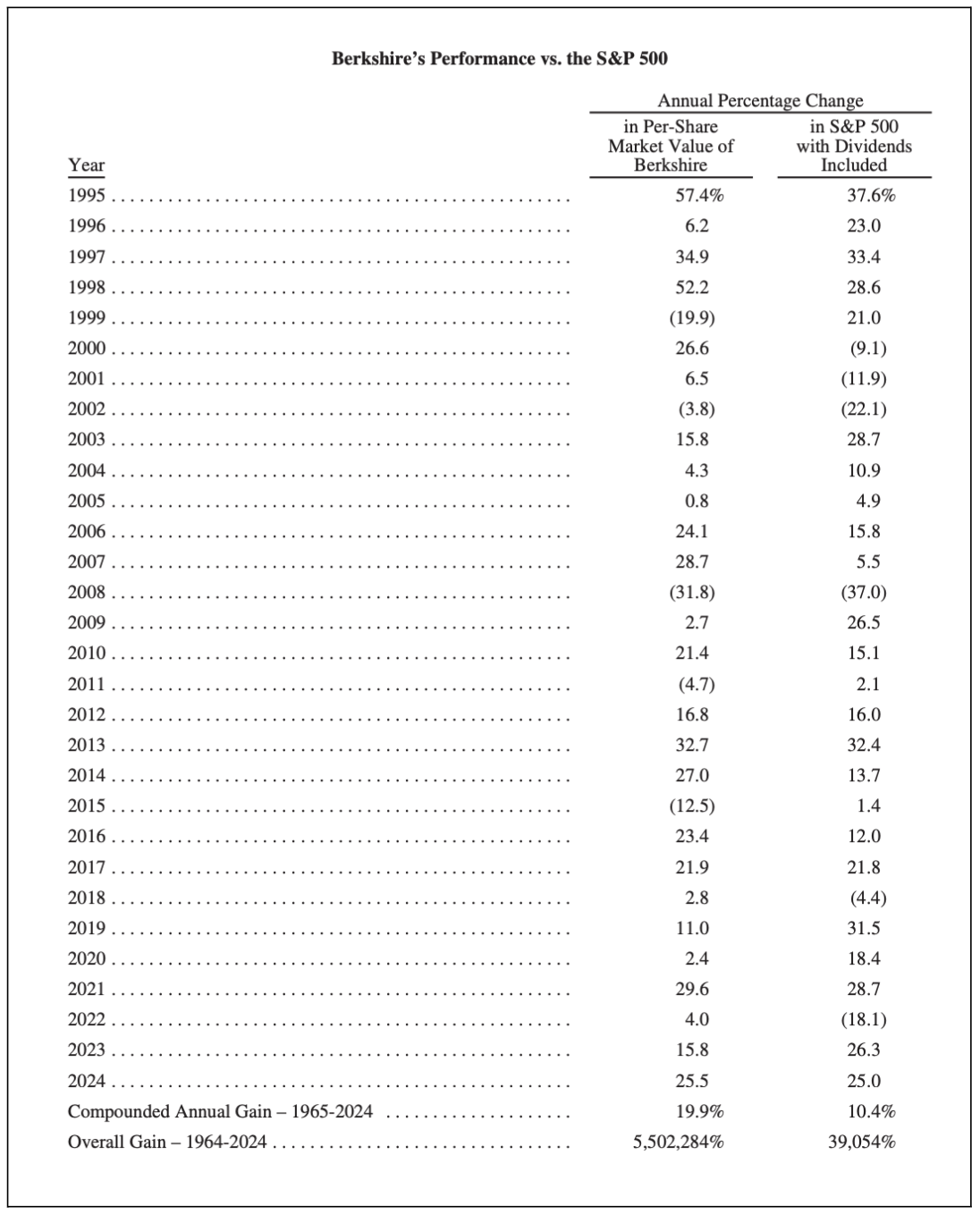

Warren Buffett has compounded capital at roughly 19.9% per year since 1965. That number is always quoted in US dollars (very few actually mention this on social media). It shows how Berkshire Hathaway performed in the US market.

Now look at the exchange rate movement.

In the mid-1960s, one US dollar was roughly ₹5. Today, it is around ₹90. Over those decades, the rupee has weakened significantly against the dollar.

So if an Indian investor had invested alongside Buffett from 1965, their returns would not have been limited to 19.9% annually in rupees. The business may have compounded at around 20% in dollars, but when you convert those dollars back into rupees after decades of currency depreciation, the effective return becomes 26%.

Put differently, ₹100 invested in 1965 and allowed to grow at roughly 26% a year when you include both business performance and currency movement, would today be worth somewhere around ₹10 crore. 🙂

When you look at it like that, the impact of currency is really significant.

Over long stretches of time, exchange rates change outcomes in ways we rarely account for when we talk about returns

Comments

Login or register to join the conversation.