In the earlier discussion, we spoke about diversification and how it affects long-term returns.

The natural extension of that conversation is asset allocation. Most investors diversify by spreading money across equity, debt, and gold. The logic is quite simple. If one asset class struggles, another may provide stability.

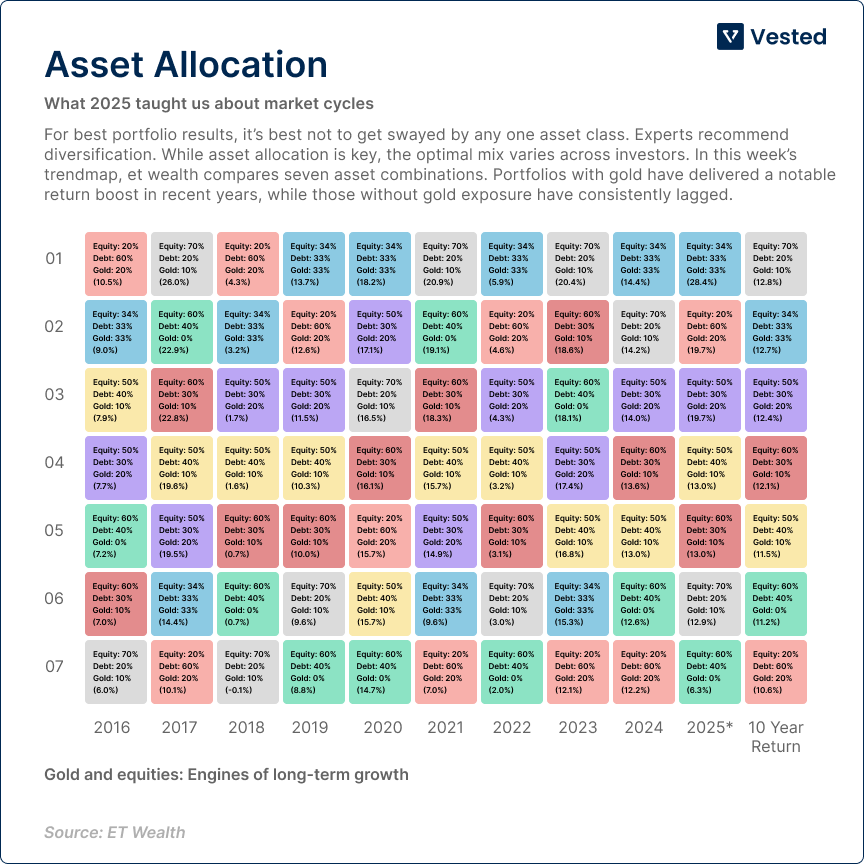

The ET Wealth data you see below compares different asset combinations across multiple years.

What stands out is that portfolios which included both equities and gold consistently ranked higher over long rolling periods. Portfolios that excluded growth assets, or were too conservative tended to lag.

The broader takeaway is not that one specific mix is perfect. The takeaway is that combining growth assets with stabilisers improves long-term outcomes.

However, there is a second layer to this idea.

Even if you get asset allocation right at the top level, the structure of your equity allocation still matters. If the equity portion of your portfolio is concentrated within one country and one economic system, then a large part of your long-term growth remains dependent on that single system.

Let us think about this practically.

Suppose you build a portfolio with 60% equity, 30% debt, and 10% gold. Now, that looks diversified. The ET Wealth data suggests such balanced combinations have historically delivered competitive long-term returns.

But now ask a deeper question. What does that 60% equity consist of?

If it is entirely domestic equities, then even though you are diversified across asset classes, your growth engine still depends on one economy. All the sectors inside that equity allocation operate under the same currency, the same interest rate cycle, and the same domestic policy environment.

In stable times, that may not feel restrictive. Sector rotation can smoothen returns. But during broader economic stress, correlations rise. Banking, IT, consumption, and manufacturing may all react to the same macro pressures.

This is where combining local asset allocation with global exposure becomes meaningful.

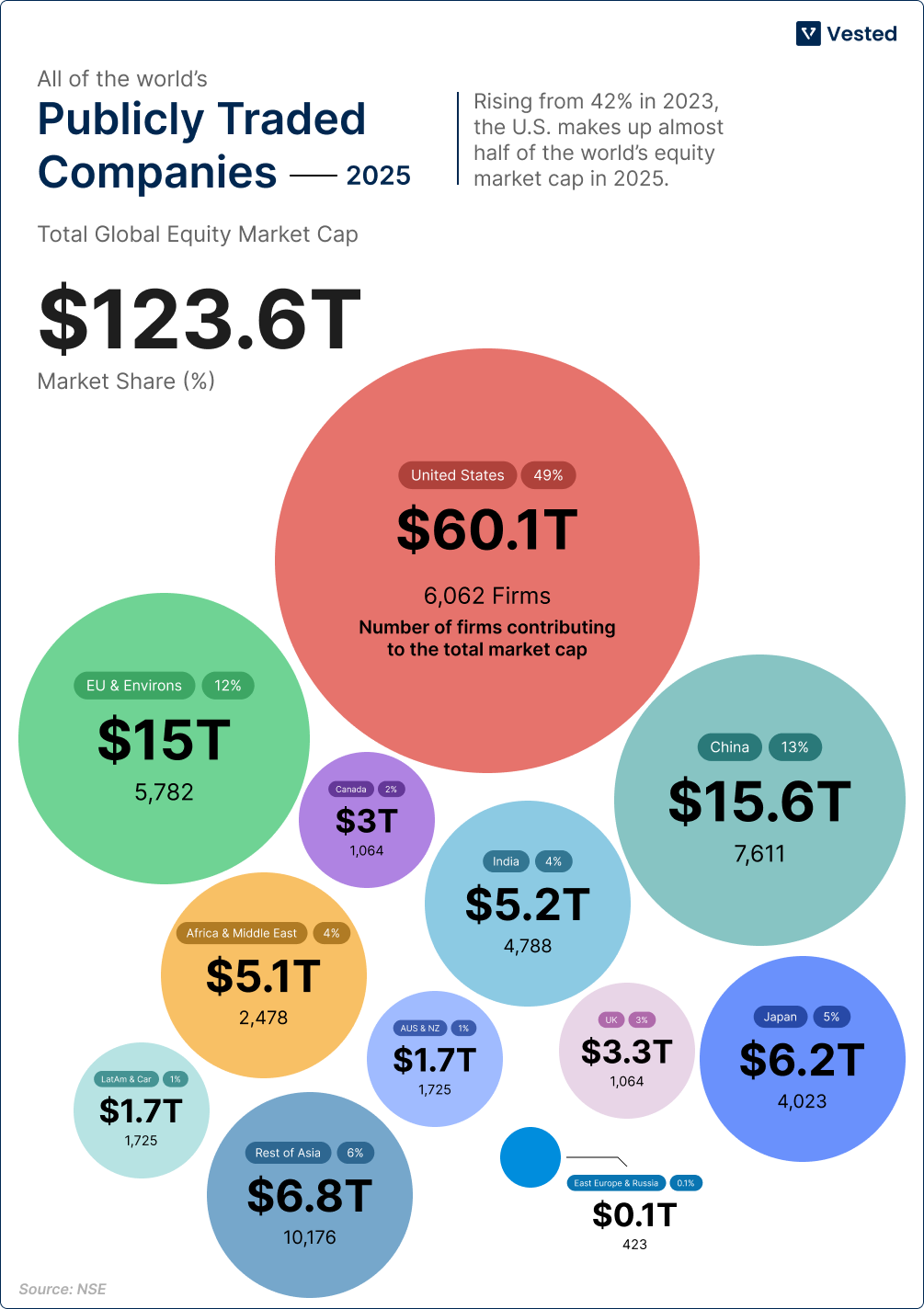

India represents roughly 4% of global equity market capitalisation. That means the overwhelming majority of listed companies and sector leaders sit outside domestic markets.

The United States alone accounts for more than half of global market value. It houses many of the dominant players in semiconductors, biotechnology, enterprise software, aerospace, and global consumer brands.

When global equities are added alongside domestic equities, the equity allocation itself becomes more diversified. The return drivers expand beyond a single economy. You introduce exposure to different currencies and industries that are not fully in sync or affected by Indian growth.

Asset allocation across equity, debt, and gold gives balance.

Adding global exposure strengthens the equity component within that allocation.

This does not remove volatility, and it does not prevent market corrections. But it reduces the likelihood that your entire growth portfolio is reacting to the same domestic shock at the same time.

That is the practical portfolio impact of limited sector exposure.

And that is why diversification is not only about how much equity you own, but also about what kind of equity you own and where it operates.

But when you step outside India, you are also stepping into another currency. That layer can also change long-term outcomes, sometimes positively, sometimes negatively. Understanding how currency fits into diversification is important, and that is where we turn next.

jjjjl

jk

jjj