When you want to convert rupees into dollars, the first instinct for most people is to check the exchange rate on Google.

If you open Google and search USD to INR, it will show you a live number.

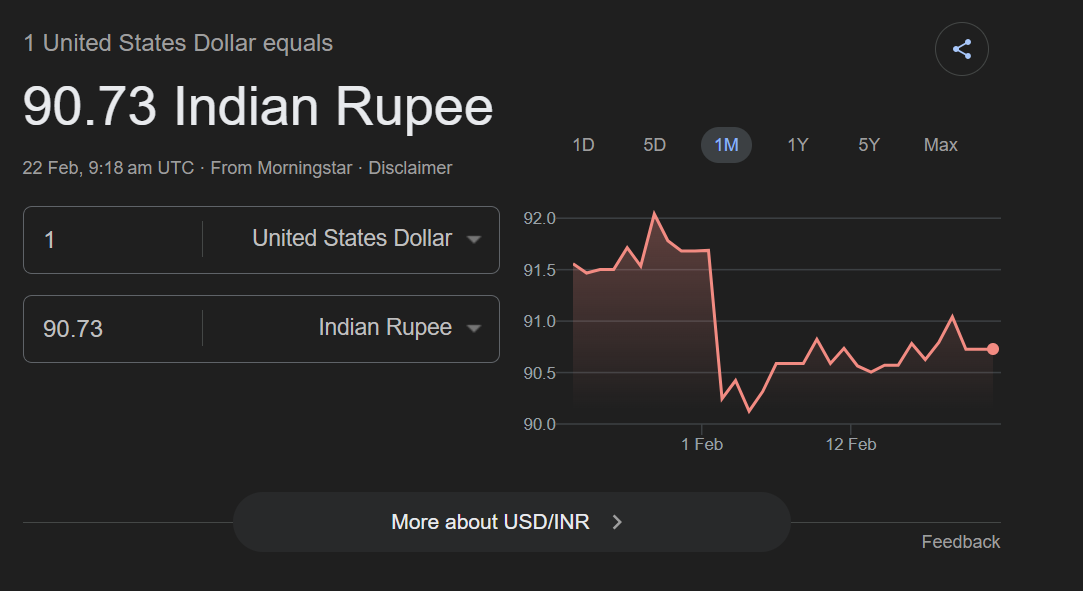

For example, on 20 February 2026, the rate shows roughly ₹90.73 for one US dollar.

This number is known as the interbank rate, sometimes also called the mid-market rate.

It represents the rate at which large banks and financial institutions trade currencies with each other in the global foreign exchange market. These transactions typically happen in very large volumes between institutions, and the interbank rate reflects the real-time price of one currency relative to another.

Because it is easily accessible, many investors treat this number as the “true” exchange rate. However, when you actually convert money through a bank, the rate applied is usually different.

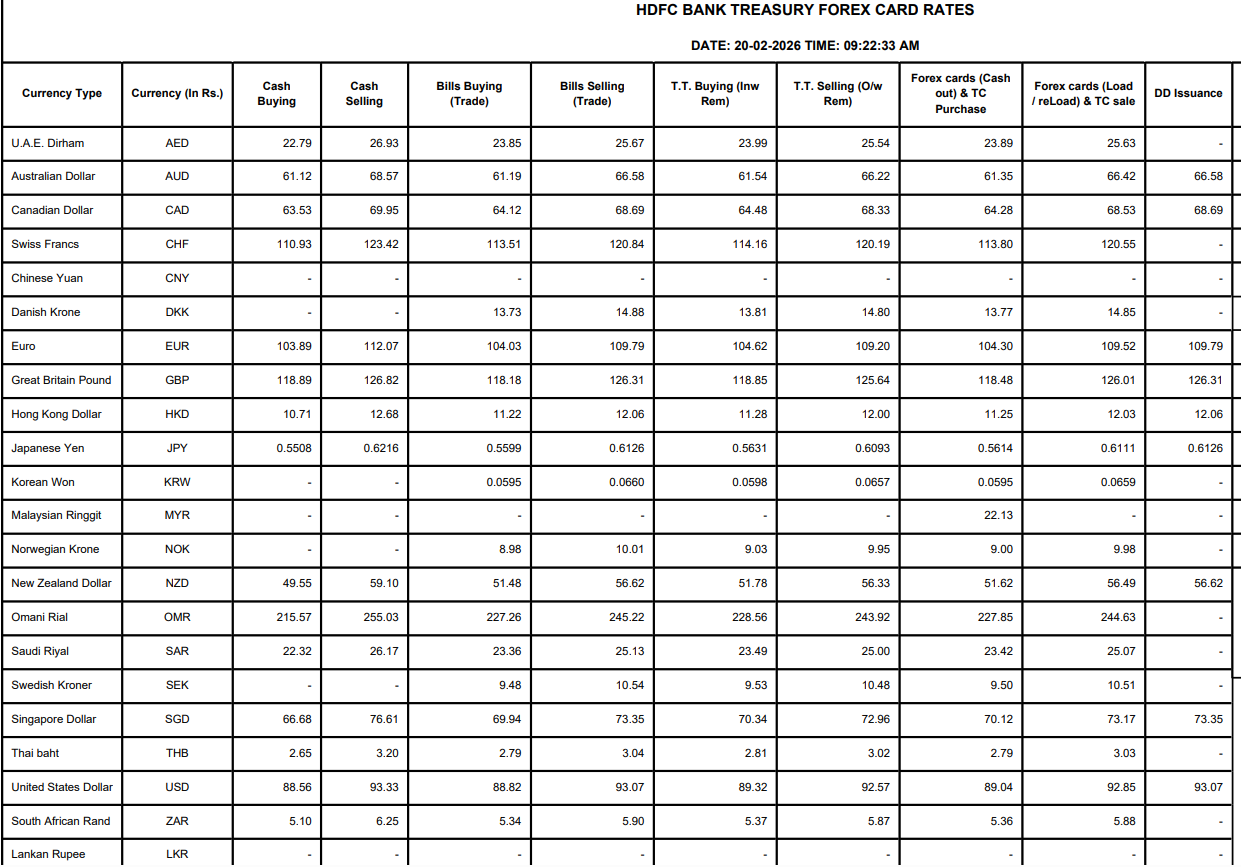

To see this, open the forex rates page of any major bank.

For example, on 20 February 2026, the TT Selling Rate for USD quoted by HDFC Bank was approximately ₹92.54.

Source: HDFC Bank Forex Card Rate

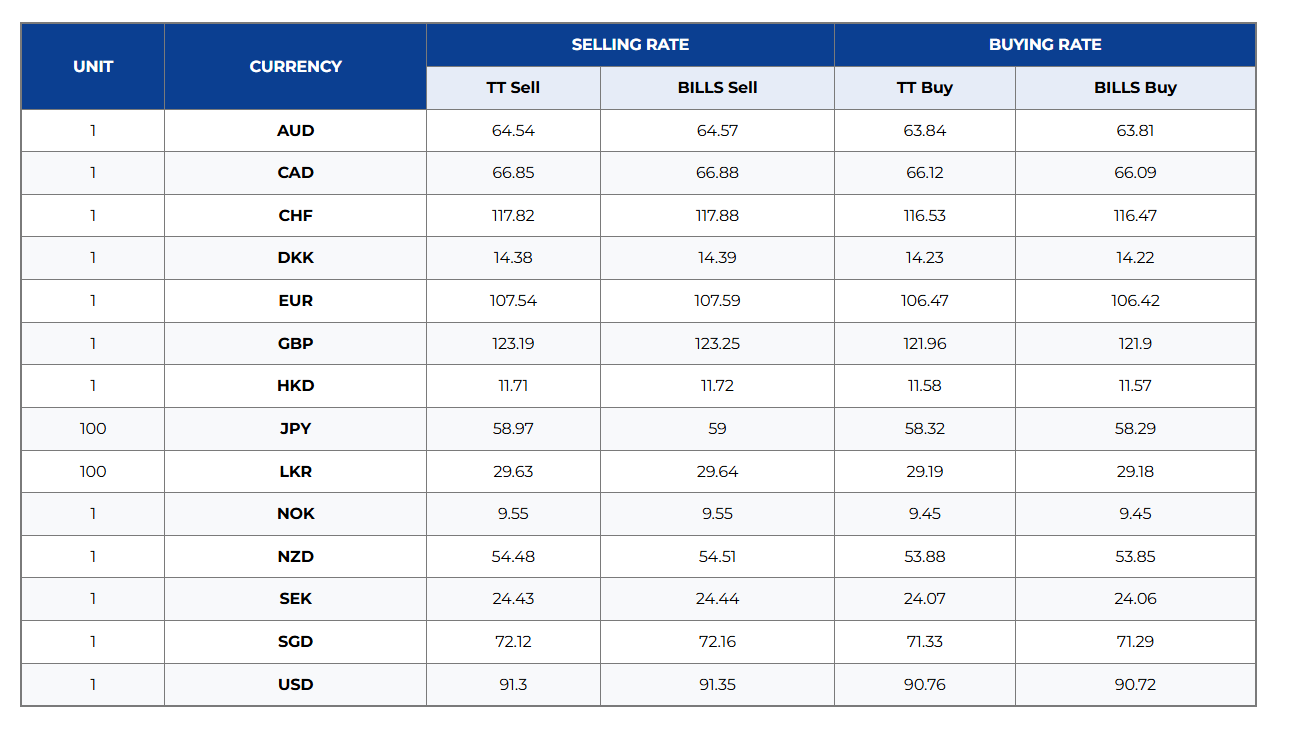

On the same day, Indian Overseas Bank quoted a TT Selling Rate of roughly ₹91.30 for outward remittances.

Source: IOB Forex Card Rate

Source: IOB Forex Card Rate

Both numbers are higher than the ₹90.73 interbank rate shown on Google.

The difference between these numbers represents the foreign exchange margin charged by the bank. Instead of appearing as a separate line item fee, the margin is built directly into the exchange rate offered to the customer.

Why do banks charge a markup?

Banks apply this margin for a few practical reasons.

First, banks themselves do not always access the currency market at the exact interbank rate that appears on Google. They buy and sell currencies through dealing desks and liquidity providers, and there is usually a small spread involved even at the institutional level.

Second, banks take on currency price risk between the time you initiate a transfer and the time the currency conversion is actually executed. Exchange rates move constantly throughout the day, so the margin provides a buffer for that volatility.

Third, processing international transfers involves operational infrastructure. Banks maintain foreign exchange trading desks, international payment networks, compliance teams, and settlement systems that allow cross-border transactions to happen safely.

The markup on the exchange rate effectively becomes the way banks recover these costs and ofcourse to make money.

Instead of charging a large visible fee, the cost is embedded directly into the conversion rate offered to the customer.

This is why the margin often goes unnoticed. Unless someone compares the interbank rate and the bank’s TT Selling Rate side by side, it simply appears as the “exchange rate for the day”.

And by the way, this practice is not unique to one bank.

HDFC Bank, ICICI Bank, Kotak Bank, SBI, IOB and all other banks follow the same process. Every institution that processes international transfers applies a markup over the interbank rate. The exact spread varies across banks and also changes from day to day depending on market conditions.

The specific rate used for international wire transfers is called the TT Selling Rate.

TT stands for Telegraphic Transfer, which is the traditional term used for international bank transfers. This rate applies when funds are being sent abroad through a bank transfer.

It is different from the exchange rates used for travel cards, airport forex counters, or currency exchange shops. Each of those services uses its own pricing structure.

For global investors, the TT Selling Rate is the one that matters, because it determines how many dollars are credited when you transfer money to fund your international investment account.

At first, the difference between ₹90.73 and ₹92.54 may not appear that big. But the impact becomes clearer when applied to an actual transfer amount.

Suppose you want to send ₹10 lakh to invest in US stocks.

If the conversion happened at the interbank rate of ₹90.73, your ₹10 lakh would convert to approximately $11,019.

But if the bank applies a TT Selling Rate of ₹92.54, the same ₹10 lakh converts to around $10,806.

The difference is $213, which is roughly ₹19,000.

This amount disappears purely due to the exchange rate markup, before any transfer fee or GST is added, and before the money even leaves India.

Understanding this difference is important because the exchange rate used during conversion is often the largest cost component in an international transfer.

Comments

Login or register to join the conversation.