When you confirm a fund transfer in the Vested app, the experience on your end is fairly simple.

You enter the amount, confirm the transaction, and wait for the funds to arrive.

What happens next involves a chain of institutions, each performing a specific role. Understanding this chain helps explain why international transfers take time and why delays occasionally occur.

Here is what actually happens, step by step.

Step 1: You initiate the transfer

If you are transferring funds from partner banks such as HDFC Bank, Axis Bank, ICICI Bank, or IDFC First Bank the process can be completed directly inside the Vested app.

Your beneficiary details are already pre-filled. You enter the transfer amount, verify the transaction through OTP authentication, and confirm the payment.

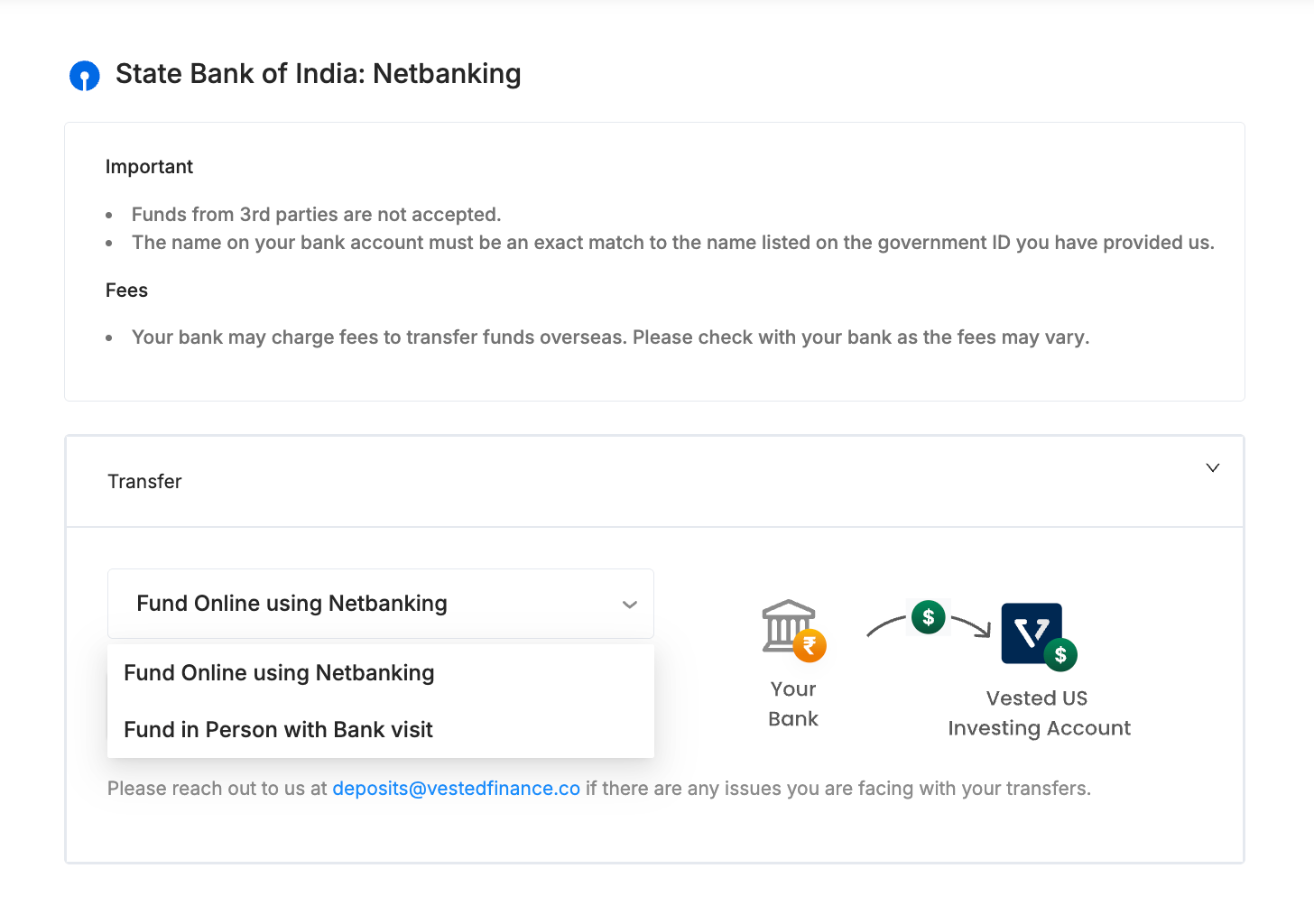

If you are transferring funds from other banks, the process works slightly differently. You download the transfer instructions from the Vested app and initiate an outward remittance through your bank’s net banking portal.

The instructions contain all the required details, including:

- your unique Vested account number

- the SWIFT code of the correspondent bank

- beneficiary bank details

- payment reference information

At this stage, your bank also records your PAN and the LRS purpose code associated with the transfer. These regulatory elements are explained in the next section.

Step 2: Your bank reviews the request, converts the currency, and sends the wire

Once you initiate the transfer, the bank does not immediately send the money abroad. The request first goes through a short internal approval process.

This stage ensures that the transfer complies with both banking rules and RBI regulations under the Liberalised Remittance Scheme (LRS).

The process typically involves several checks.

- The transfer request is received by the bank

Your bank receives the outward remittance request along with the beneficiary details, transfer amount, and LRS purpose code.

If the transfer is initiated through the Vested app with a partner bank, much of this information is already pre-filled.

- The bank performs internal account checks

The bank first verifies basic conditions within your account.

This includes confirming that:

- sufficient balance is available in the account

- the funds are not coming from overdraft limits or loan proceeds

- the account is compliant with KYC requirements

Under RBI guidelines, outward remittances for investments must be made using own funds, not borrowed money.

- LRS eligibility and limit checks

After the internal checks, the bank verifies whether the remittance falls within the annual LRS limit for that individual.

The bank checks this using your PAN, which is used to track the total amount remitted abroad during the financial year.

This verification is typically performed through the banking system that records outward remittances across institutions.

If the requested transfer does not exceed the remaining limit under the $250,000 annual LRS cap, the process moves forward.

- TCS applicability check

The bank also determines whether Tax Collected at Source (TCS) applies to the transfer.

Under current rules, TCS may apply once outward remittances cross certain thresholds during the financial year. If the cumulative transfers remain within the specified limit, TCS may not apply at that stage.

The bank automatically performs this check and applies the appropriate tax collection if required.

- Currency conversion and wire initiation

Once these checks are completed and the transfer is approved, the bank converts the rupees into US dollars using the TT Selling Rate applicable on that day.

After the conversion, the bank initiates the international SWIFT wire transfer. The flat wire fee charged by the bank is deducted at this stage before the funds leave India.

Step 3: The SWIFT network carries the payment instruction

Once your bank has completed its checks and initiated the transfer, the next step involves the SWIFT network.

SWIFT stands for Society for Worldwide Interbank Financial Telecommunication. It is the global communication network used by banks to send secure financial messages to each other.

More than 11,000 financial institutions across over 200 countries are connected through this network. Each participating bank has its own SWIFT code, which acts like a unique identifier. When your bank sends an international transfer, it uses this code to ensure that the payment instruction reaches the correct institution.

One important point often causes confusion.

SWIFT itself does not move the money. It functions as a secure messaging system, not a payment rail in the way domestic systems such as UPI or NEFT work.

When your bank sends money abroad, it sends a SWIFT message to the receiving bank or intermediary bank. This message contains the payment instructions. It includes details such as:

- the sending bank

- the receiving bank

- the beneficiary account number

- the transfer amount

- reference information needed to identify the recipient

Once this instruction is received, the actual movement of funds happens through correspondent banking relationships between banks.

Banks maintain accounts with each other in different currencies. When a SWIFT instruction is received, the funds are settled through these accounts. This is how the money moves from one country to another.

Because multiple banks may be involved in this process, the transfer can pass through one or more intermediary institutions before reaching the final destination. This is one of the reasons international transfers typically take one to three business days to complete.

Step 4: The money moves through the correspondent bank

Most Indian banks do not maintain a direct banking relationship with every financial institution in the United States. Because of this, international transfers usually pass through an intermediary known as a correspondent bank.

A correspondent bank acts as a bridge between two banks that do not have a direct settlement relationship.

In Vested’s setup, that correspondent bank is JPMorgan Chase. Its SWIFT code is CHASUS33, and it operates as the gateway through which the funds enter the US banking system.

When your Indian bank sends the USD wire, the funds are first routed to JPMorgan Chase. JPMorgan then forwards the payment to DriveWealth LLC, Vested’s US brokerage partner located in Jersey City, New Jersey.

This is why, when you download the transfer instructions from the Vested app, the SWIFT code listed is CHASUS33 rather than DriveWealth’s own details. DriveWealth is the final destination of the funds, but JPMorgan serves as the intermediary that routes the transfer into the US system.

At this stage, the correspondent bank may deduct a small processing or transit fee. The way this fee is handled depends on the charge type selected when the transfer was initiated.

Banks typically offer three charge options for international wires: SHA, OUR, and BEN. For most outward remittances from India, the commonly used options are SHA and OUR.

SHA (Shared Charges)

Under SHA, the transfer costs are shared between the sender and the recipient.

The sending bank charges its wire fee upfront when the transfer is initiated. Any intermediary bank fees along the way are deducted from the transferred amount. In this case, the correspondent bank such as JPMorgan may deduct a transit fee of around $15 to $25 before forwarding the funds to the final institution.

As a result, the amount credited to your brokerage account may be slightly lower than the original USD amount sent.

OUR (Sender Pays All Charges)

Under OUR, the sender agrees to bear all transfer-related charges.

In this case, your Indian bank collects the expected intermediary bank fees in advance when you initiate the transfer. Because the intermediary charges are already paid, the full converted USD amount moves through the system without deductions.

For investors funding brokerage accounts, the difference between SHA and OUR usually determines whether the intermediary bank fee is deducted later or paid upfront during the transfer.

Step 5: Funds arrive in your Vested account

Once the wire reaches the US side, the final step is not just “money received”. It is “money received and matched to the correct brokerage account”.

That matching is what determines how quickly the funds show up in your Vested buying power.

What happens when the wire reaches DriveWealth

When DriveWealth receives the incoming wire, they see a payment instruction that includes:

- the amount received in USD

- the sending bank details

- the correspondent bank route it came through

- and most importantly, the beneficiary reference that identifies the exact account

DriveWealth then uses this information to confirm which specific investor account should be credited.

Once the credit is confirmed, the funds reflect in your Vested account as buying power, and you can place trades.

This final matching step is also why wires can sometimes show as “delivered” at the bank level but still take a few hours to reflect in the app. The funds may have arrived at the brokerage bank, but the brokerage still needs to allocate them to the correct account.

Here is the typical timeline across all stages:

| Stage | Who Is Involved | Typical Time |

| Transfer initiated and approved | You and your Indian bank | Same day if before cut-off |

| Currency converted, wire sent | Your bank | Within hours of approval |

| SWIFT message processed | Correspondent bank JPMorgan | Same to next business day |

| Funds arrive at DriveWealth | JPMorgan to DriveWealth | 1 to 2 business days |

| Funds reflect in Vested | DriveWealth confirmation | Within hours of receipt |

| Total end-to-end | 1 to 2 business days |

This is why two people can initiate transfers on the same day and still see different arrival times, depending on:

- bank cut-off timings

- whether the transfer was initiated on a weekend or holiday

- whether intermediary banks process it the same day or the next business day

- whether additional compliance checks are triggered

Comments

Login or register to join the conversation.