After the Japan episode, one question naturally follows.

What made the US so dominant? And is it the same kind of dominance Japan had, or is it built on something more real?

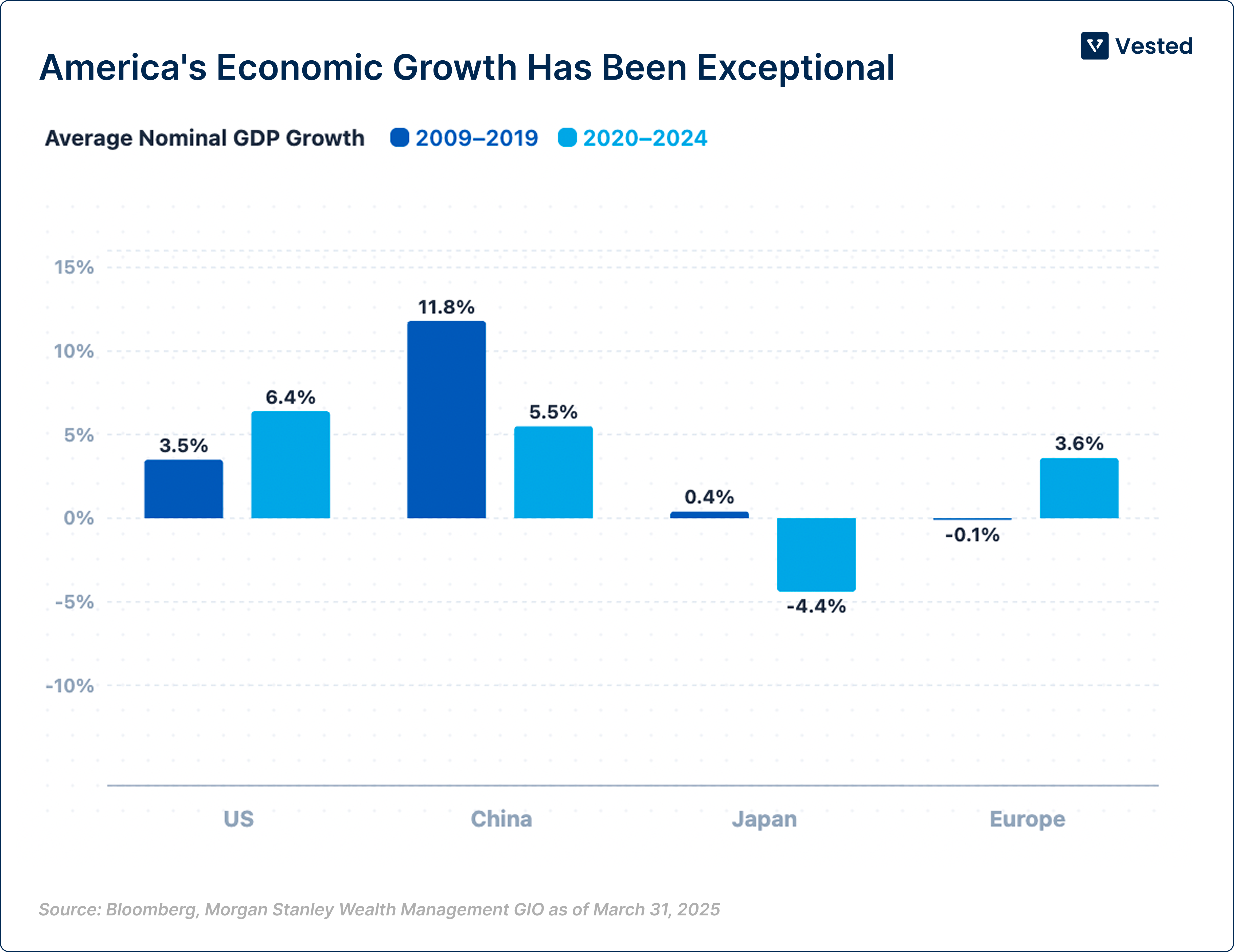

There are four structural reasons why the US pulled far ahead of the rest of the world, particularly in the 15 years after the 2008 global financial crisis.

What makes these reasons worth studying carefully is that they are measurable. This is not a story built on national pride or market momentum. The data is unusually clear.

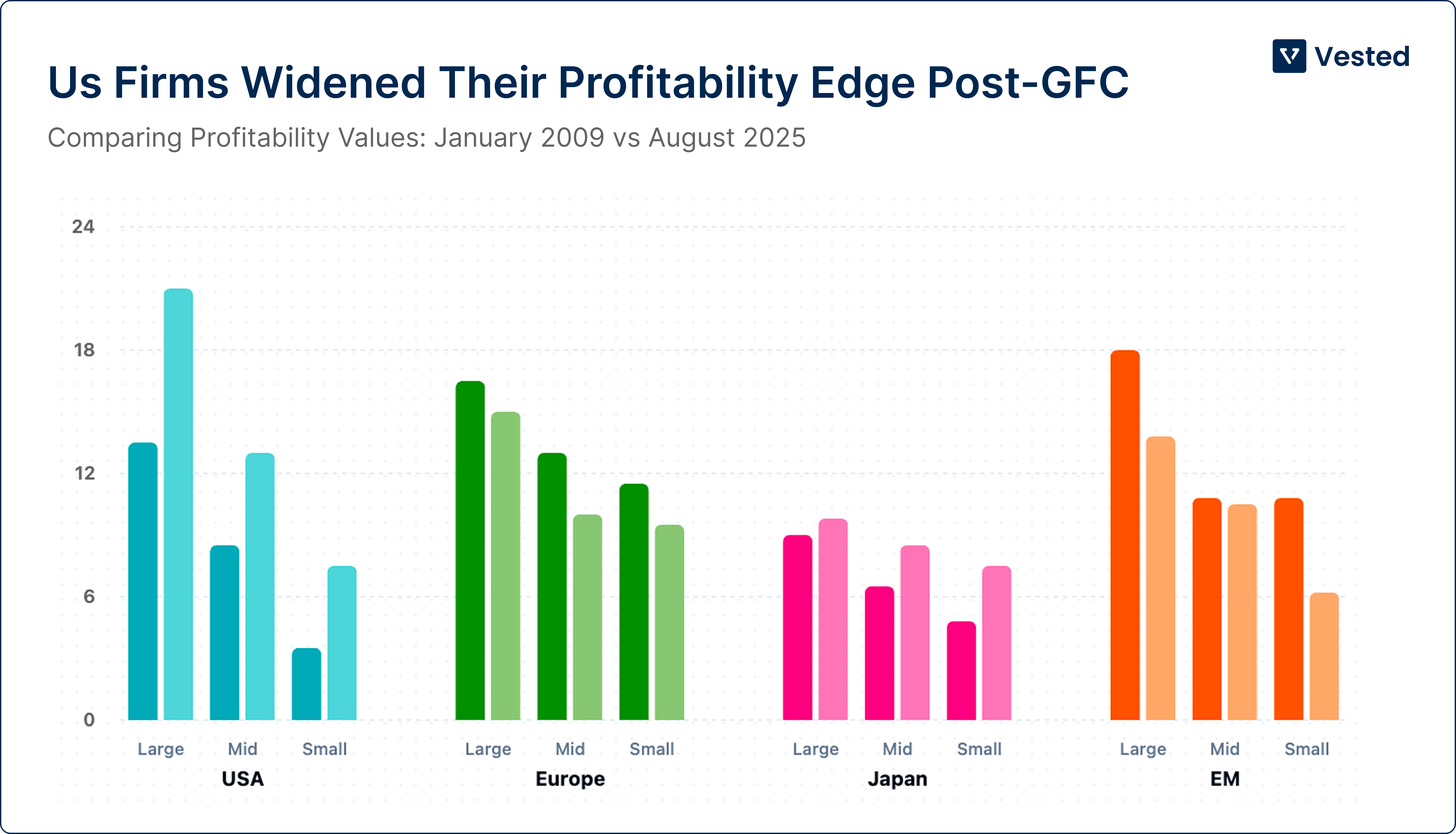

The first is profitability, and how much of it there is.

US large-cap return on equity rose by over 500 basis points between 2009 and 2025, while non-US markets broadly struggled to regain pre-crisis levels.

Sales per employee roughly doubled among the largest US firms over the same period. European and Japanese companies, facing more rigid labour markets, heavier regulation, and a greater dependence on traditional industries, could not match this.

The second is the nature of the businesses behind these returns.

Technology, software, semiconductors, and digital media now represent 40% of US market capitalisation, compared to just 16% outside the US.

These are not ordinary businesses. They operate at minimal marginal cost. The 10th million user of a platform costs almost nothing to serve compared to the first.

They generate enormous free cash flows, fund their own R&D from profits, and can expand globally without building factories in every country. That one sector alone accounted for 63% of total S&P 500 gains between 2009 and 2024.

The US today spends about $975 billion per year on research and development, roughly 38% of all global R&D spending, while representing only 25% of global GDP.

The third is how long that growth has lasted.

This is perhaps the most important and least discussed part of the story. Research published by MSCI in 2025 tracked how long companies in different markets stayed in the top quintile of revenue growth, what researchers call the extraordinary growth phase.

From 1997 to 2009, survivorship in this category was broadly similar across the US, Europe, Japan, and emerging markets. Since 2009, something changed. The half-life of high growth lengthened materially in large and mid-sized US firms, while remaining relatively stable elsewhere.

Investors in US stocks are not just paying for faster earnings growth. They are paying for growth that keeps going longer than almost anywhere else in the world. And the data shows that premium has been justified.

The fourth is immigration and workforce dynamism.

Since 2020, virtually all US labour force growth has come from immigration.

More than 45% of today’s Fortune 500 companies were founded by immigrants or first-generation Americans.

Four of the seven CEOs of the companies we know as the Magnificent Seven are immigrants. Countries like Japan and Germany face the opposite problem: shrinking, aging workforces.

The US workforce stayed younger, larger, and more dynamic precisely because it kept absorbing talent from everywhere else.

Underneath all four of these is one more factor that amplifies everything else: the US dollar. It accounts for about 57% of global foreign exchange reserves.

Central banks, pension funds, and sovereign wealth funds around the world hold dollar-denominated assets not purely by choice but as a matter of institutional necessity. That creates a persistent, structural demand for US equities that no other market enjoys. Money flows into US markets partly because global institutions have no choice but to hold dollars.

Comments

Login or register to join the conversation.