Most Indian investors have heard of the US stock market. Far fewer have heard about what Japan’s market was doing in the late 1980s.

Throughout the 1970s and 1980s, Japan’s economy grew at an extraordinary speed. Sony, Toyota, and Honda were conquering global markets. Japanese banks were sitting on enormous amounts of capital. Property prices in Tokyo became almost fictional. At the peak of the bubble, the land beneath the Imperial Palace grounds was estimated to be worth more than all the real estate in California.

By December 1989, Japan’s stock market had grown to represent about 42% of global market capitalisation.

Let that sink in for a moment.

Japan, a country of roughly 120 million people, held almost half of the entire world’s listed company value. The Nikkei 225 index had risen nearly fivefold during the 1980s, climbing from around 7,000 in 1980 to almost 39,000 by December 1989.

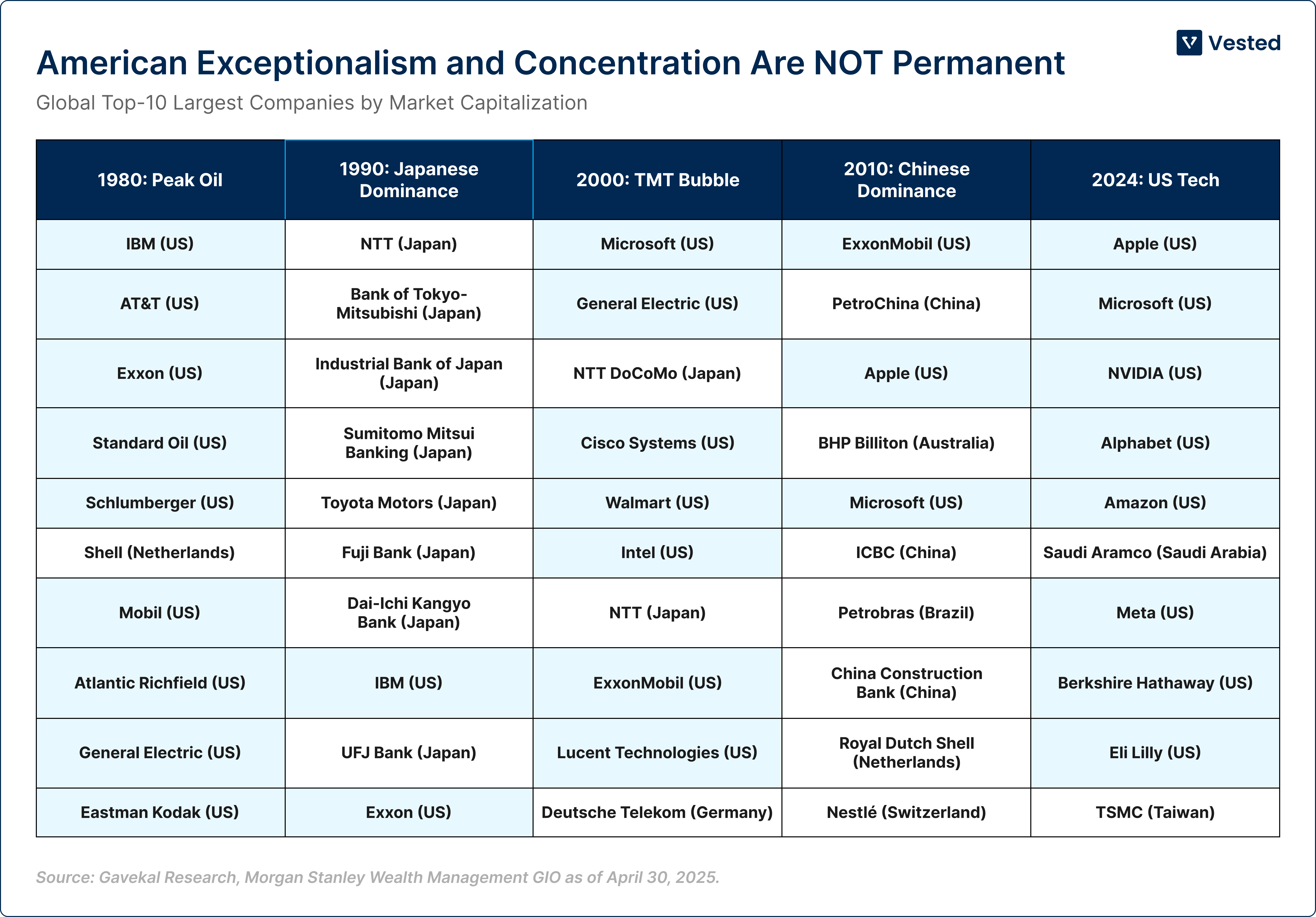

At the peak of the boom, 13 of the world’s 20 most valuable companies were Japanese. The Tokyo Stock Exchange was larger than the New York Stock Exchange in total market value. Analysts at major brokerages were confidently predicting that the Nikkei would reach 80,000 by 1995.

But the rise had been built on a powerful asset bubble.

During the second half of the 1980s, commercial land prices in Tokyo had increased nearly five times. At one point, it was widely said that the land underneath the Imperial Palace in Tokyo was worth more than all the land in California.

Rising property prices allowed companies and investors to borrow heavily. Those loans were often used to buy more stocks and more real estate. Asset prices began reinforcing each other.

At the same time, valuations were becoming extremely stretched.

By 1989, the Nikkei was trading at a price-to-earnings ratio of roughly 60 times earnings. Historically, equity markets around the world have averaged closer to 15 times earnings. In other words, Japanese stocks were trading at about four times their long-term valuation norms.

The market had been priced for perfection.

And perfection did not arrive.

In 1989, the Bank of Japan began raising interest rates to slow the overheating economy and asset bubble. The policy rate increased from 2.5% to around 6% by 1990.

Higher borrowing costs quickly exposed how much leverage had built up in the system.

Investors who had borrowed heavily to buy stocks faced margin calls. Companies that had used rising property values as collateral suddenly looked overleveraged. Banks became cautious about lending.

Prices began to fall.

By August 1992, the Nikkei had lost about 60% of its value from its December 1989 peak. What had looked like unstoppable growth only a few years earlier turned into one of the most dramatic market collapses in modern financial history.

And the recovery was painfully slow.

The Nikkei did not cross its 1989 high of 38,915 again until February 2024 — 34 years later.

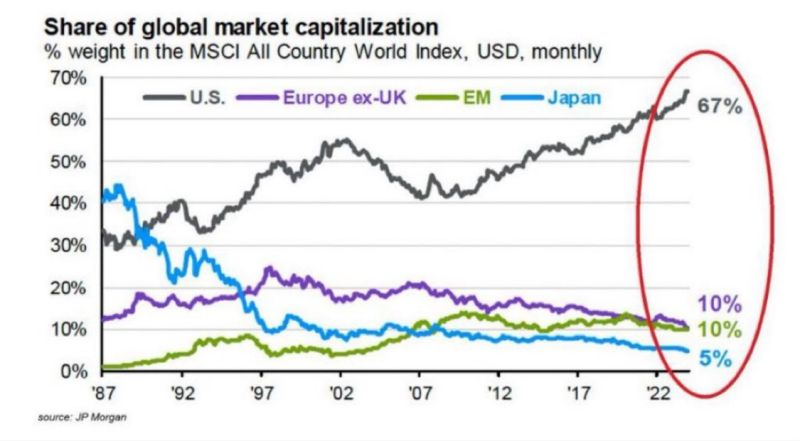

Over those decades, Japan’s position in the global market shrank dramatically. Its share of world equity markets fell from 42% at the peak to roughly 6% today.

Not one Japanese company now ranks among the twenty most valuable companies in the world.

This is one of the most important lessons in all of market history. The largest market in the world is not necessarily the best investment. Size and momentum are not the same thing as value.

| Country | Share in 1989 | Share in 2025 |

| United States | 30% | 49% |

| Japan | 42% | 6% |

| United Kingdom | 10% | 4% |

| Germany | 8% | 2% |

| China | Less than 1% | 3% |

Comments

Login or register to join the conversation.