Invest in 10,000+ US Stocks and ETFs

* Offering through VF Securities, Inc. (member FINRA/SIPC)

Skip to content

Skip to content

Disclosure: Companies shown are meant to a representative sample of stocks available and not a recommendation to purchase.

Read about experiences of those who have taken their portfolio global with Vested

Founder and Managing Partner, Abanwill Consultants LLP

Before Vested, investing internationally was quite a hassle. Their interface is very user-friendly and transfer of funds from India has been made easy. Most importantly, reports to file income taxes are also available at a click. The Management team is open to feedback and works on improving the platform continuously. I would recommend them to everyone who wants to make an international portfolio

Growth at Smallcase

I am thrilled to share my experience with Vested, the US investing platform. Since I started using Vested, my investment journey has been nothing short of exceptional. The platform’s user-friendly interface and powerful features have made investing in US markets accessible and efficient. Thanks to Vested, I have been able to seize opportunities and witness my investments grow.

Head of M&A and Strategic Advisory

Simple stuff – easy to explore – not much complications – never faced any glitch – easy to track the portfolio – REALLY USEFUL FILTERS in Watchlist and Portfolio – easy transfer of USD – great content from time time. Perfect.

Co-founder at Ascent Health

Vested has been one the earliest and definitely one of the most user-friendly service helping investors like me to diversify their portfolio. I have never faced a single issue with either fund transfer, buying or selling stocks or even withdrawals back to my Indian account. I am a big fan of vested direct and also their tax harvesting feature which they introduced recently. ?Kudos to the team! Keep it up!!

Delivery manager

I am delighted with Vested Finance’s exceptional services. Their user-friendly platform offers advanced tools and analytics, empowering informed investment choices. The team’s transparency, expert guidance, and educational resources are commendable. Their outstanding customer service makes them a true industry leader. Thank you for helping me achieve my financial goals!

SVP - Tata Digital

My journey with Vested started in 2020 while I was looking for a platform for seamless investing in US markets. In the universe of options, Vested stood out now and still stands out today. It has made the all the key processes like fund transfer, asset assortment/selection, portfolio allocation, etc. as seamless as possible and continues to evolve with great customer centricity. My best wishes to the team to keep out-innovating the competition and to build one of the finest investment platforms out of India for the world!

Founder-Director at Happy Software International

Great app to invest Globally. I like to invest in U.S.A stocks with both. Vested website and App. When I am in a hurry to check purchased stocks or have to invest quickly then i always use vested app. Vested team is also very much communicative. Thanks Dinesh Kumar Founder: Happy Software International

Software Consultant

I’ve been with Vested since 2019, one of the early ones. I was so grateful to have a commission free broker who enabled me to buy and sell US stocks while residing in India. I continue to enjoy the ease with which I can conduct serious business from my cellphone. Since I have a long term commitment to stay invested in my stocks, I am depending on Vested being my facilitator for the long term as well.

Disclosure: These customers were not paid for their testimonials and may not be representative of the experience of other customers. These testimonials are no guarantee of future performance or success.

Learn about the world of alternative assets with our in-depth educational modules on US Stocks, P2P Lending, INR Bonds and more

Start Learning

Get answers to frequently asked questions by our investors or get help on any topic

Get in touch

Stay up to date on the latest investing trends in the markets and other announcements from Vested

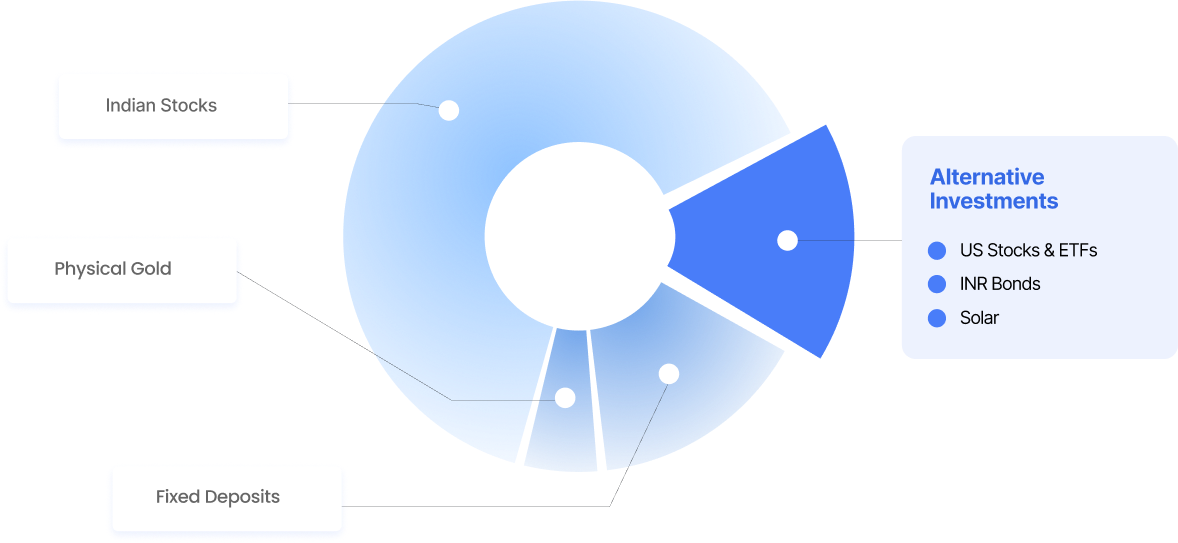

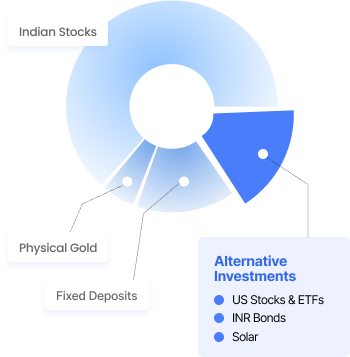

Browse ArticlesAlternative investments are non-traditional financial assets that exist outside of conventional options, such as Indian stocks, fixed deposits, physical gold, and cash. They offer diversification opportunities into new-age asset classes and help investors build a more balanced portfolio.

Vested is a comprehensive platform for investing in alternative assets, facilitating diverse and global investment opportunities.

At Vested, the alternative investment options include:

The alternative investments offered on Vested are legal and follow the guidelines set by the regulators (the RBI and SEBI). Before you venture into the world of alternatives, it is vital to consider the following points:

Understanding the investment: Before investing, you should have a clear understanding of the asset class, its structure, and potential risks and returns. This includes understanding the market dynamics, historical performance, and factors influencing the asset’s value. It’s essential to ensure that they align with your overall investment strategy and risk tolerance

Liquidity: Alternative investments often have lower liquidity compared to traditional investments. You must consider your liquidity needs and whether you can afford to have your money tied up for the investment period.

Vested is accessible to Indian residents, allowing them to invest in US stocks and ETFs, as well as alternative investment options like P2P lending and INR bonds. It’s suitable for both beginners and experienced investors who are looking for opportunities to invest in global markets and non-traditional assets.

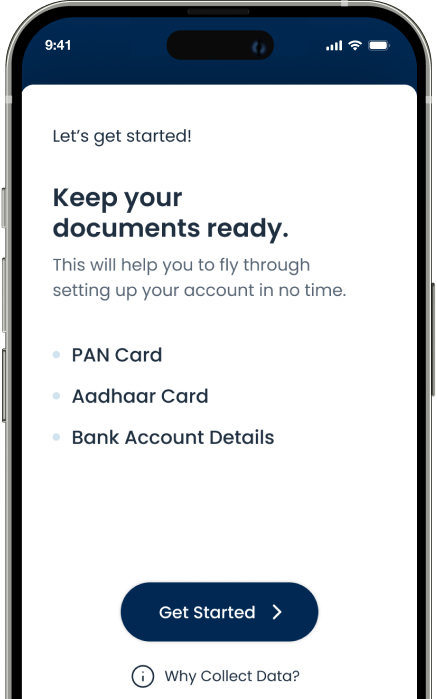

Non-resident Indians (NRIs) can also invest in US Stocks with Vested. To open an account with Vested, NRIs need to provide their PAN card or passport, proof of address like a passport, and their tax ID from the country where they are currently a tax resident.

To open an account on Vested as an investor, follow these steps:

Your assets are held at a 3rd party custodian, and we do not ever touch or hold your money.

For US Stocks, If Vested shuts down, you would still have access to all your cash and securities, as we will ensure that direct DriveWealth access is established for you to continue to buy or sell securities. In the highly unlikely event that Vested and DriveWealth shut down, your SIPC insurance kicks in. Each brokerage account opened with Vested is insured by SIPC (Securities Investor Protection Corporation) up to $500,000. This includes $250,000 in cash. For more details, please read here

For other asset classes – Vested Edge and INR Bonds, you will still have access to your cash and securities through our NBFC-P2P partners (for Vested Edge), and your INR Bonds holdings will persist in your demat account with NSDL/CDSL.

Vested offers two plans, Basic and Premium, with different fee structures:

Basic Plan

Premium Plan