Skip to content

Skip to content

Be it a millennial or a 50 year old nearing retirement, these days everyone seeks stable and predictable income. Dividend-paying equities can be a tempting option; however, they inherently carry market risks, and dividend payouts may be relatively modest.

For a more stable income stream, investors may consider fixed-income investments like bonds. Bonds generally carry lower risk since they offer reliable returns through periodic coupon payments, while equities are volatile since their performance is linked to the market sentiment. This fixed income component reduces exposure to market volatility.

While bonds typically provide higher returns than traditional savings accounts or fixed deposits (FDs) which do not even beat inflation, it’s important to note that bond prices can fluctuate due to factors like interest rate changes.

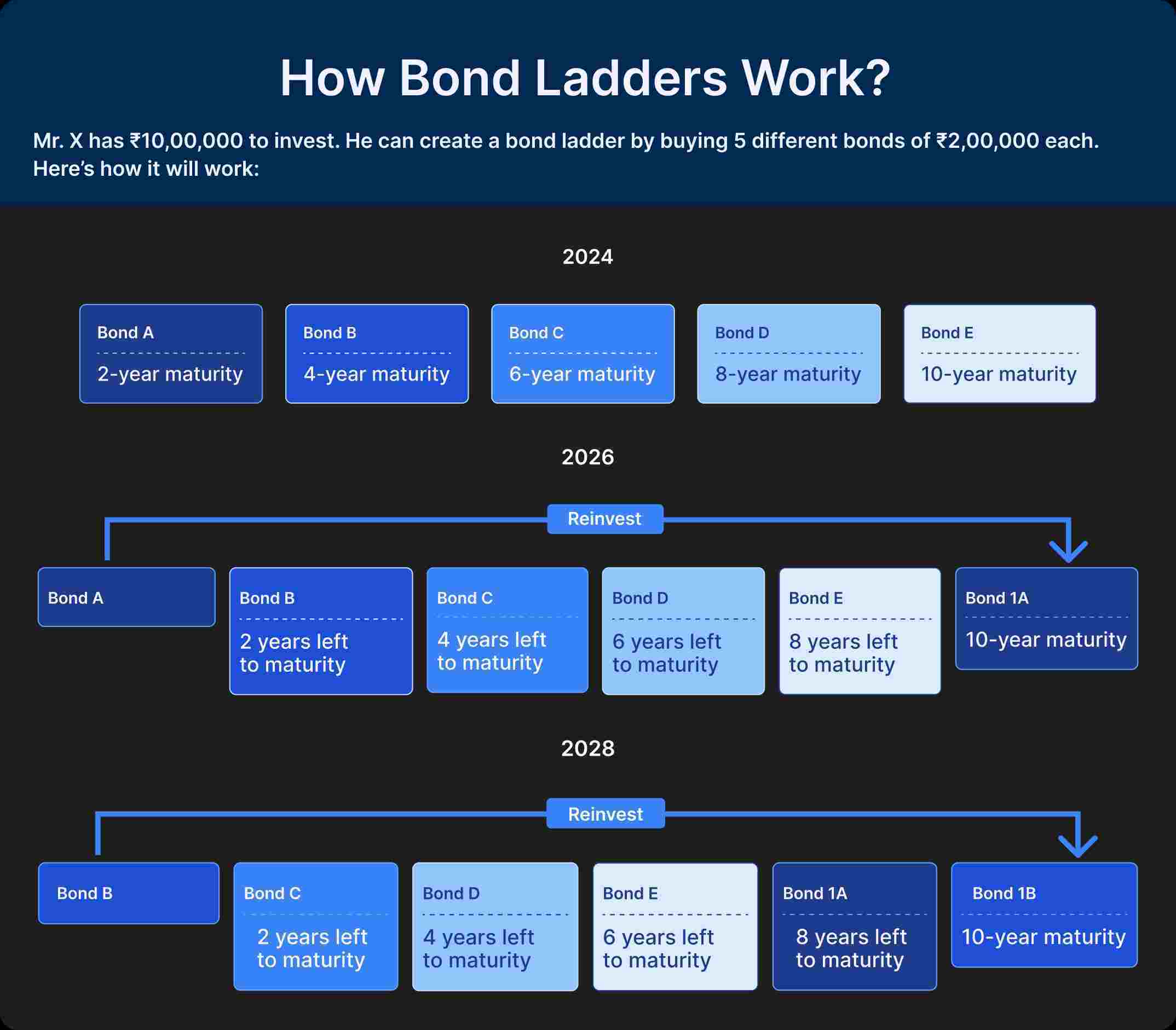

Now with bonds you can build a stable income stream and lock-in interest rates through bond laddering. This strategy involves purchasing bonds with staggered maturity dates, allowing for reinvestment at potentially higher rates when earlier bonds mature. Bond laddering can help manage interest rate risk and provide a steady income stream over time.

By creating a ladder-like structure of bonds, investors aim to balance risk, return, and liquidity. This strategy has been employed by both individual investors and institutional portfolios to optimize fixed-income allocations. In this blog, we will discuss what is bond laddering, how it works and pros and cons of bond laddering.

What is Bond Laddering?

At the core of bond laddering is the concept of diversification. Rather than concentrating investments in bonds with similar maturity dates, investors spread their funds across a range of maturities. This reduces the portfolio‘s sensitivity to interest rate fluctuations. When interest rates rise, bond prices typically fall, especially for longer-term bonds. However, with a bond ladder, only a portion of the portfolio is affected, mitigating the overall impact.

Bond laddering also offers the potential for a consistent income stream. As bonds mature, the principal is reinvested into new bonds with longer maturities, creating a perpetual cash flow cycle. This is particularly attractive for retirees or individuals seeking regular income.

Liquidity is another benefit. Because bonds mature at different intervals, investors have access to their funds periodically without needing to sell bonds at potentially unfavorable prices. This flexibility can be crucial for unexpected expenses or investment opportunities.

How Does a Bond Ladder Work?

A bond ladder consists of a portfolio of bonds that mature at different future dates. Here’s an example of a bond ladder. Mr X wants to invest Rs.10,00,000 in bonds. He invests Rs.2,00,000 in five different bonds with different maturities and creates a ladder. The ladder consists of five high-quality corporate bonds, each maturing two years apart:

| Bond Name | Bond Maturity | Investment value | Yield | Annual Income |

| Bond A | 2 years | ₹2,00,000 | 10% | ₹20,000 |

| Bond B | 4 years | ₹2,00,000 | 10.5% | ₹21,000 |

| Bond C | 6 years | ₹2,00,000 | 11% | ₹22,000 |

| Bond D | 8 years | ₹2,00,000 | 11% | ₹22,000 |

| Bond E | 10 years | ₹2,00,000 | 11.5% | ₹23,000 |

The total annual income from this ladder is ₹1,08,000, or 10.8% XIRR on an investment of ₹10,00,000, assuming all bonds were purchased at par value.

As Bond 1 matures in two years, you can replace it with a new bond maturing in 10 years to maintain the ladder:

| Bond | Bond Maturity | Investment Value | Yield | Annual Income |

| Bond B | 2 years | ₹2,00,000 | 10.5% | ₹21,000 |

| Bond C | 4 years | ₹2,00,000 | 11% | ₹22,000 |

| Bond D | 6 years | ₹2,00,000 | 11% | ₹22,000 |

| Bond E | 8 years | ₹2,00,000 | 11.5% | ₹23,000 |

| Bond 1A | 10 years | ₹2,00,000 | 12% | ₹24,000 |

The new ladder’s annual income increases to ₹1,12,000, yielding 11.2%.

Benefits of Bond Ladders

1. Managing Interest Rate Risk

Interest rate risk refers to the potential impact of changes in interest rates on bond prices. When interest rates rise, bond prices typically fall, and vice versa. Bond ladders mitigate this risk by diversifying maturity dates across the portfolio.

Bond ladders can provide a measure of protection against declining interest rates. When rates fall, newly issued bonds typically offer lower interest payments. However, a bond ladder allows you to maintain income from older bonds purchased at higher interest rates.

For instance, imagine you have a bond ladder with bonds maturing every two years. If interest rates decline significantly after the first two years, the proceeds from the maturing bonds would be reinvested at lower rates. But the remaining bonds in your ladder would continue to generate income at the higher rates locked in when you initially purchased them. This helps to preserve your overall income level. Think of it like this, if you had invested your entire corpus in the first bond which matured in the first two years. You would have to reinvent your proceeds in bonds with lower interest rates.

Essentially, a bond ladder helps you “lock in” higher yields for a portion of your portfolio, providing a buffer against the effects of falling interest rates.

2. Ensuring Liquidity

Liquidity is crucial for investors needing access to funds without incurring significant penalties or market risks. Bond ladders provide liquidity by ensuring that bonds mature at regular intervals, providing cash flow for reinvestment or other financial needs.

Unlike bond funds or ETFs, where liquidity is subject to market conditions and fund policies, bond ladders offer predictable liquidity. As bonds mature, investors have the flexibility to reinvest the proceeds or allocate them as needed, without disrupting the overall structure of the ladder.

This liquidity feature is particularly advantageous for retirees or investors seeking regular income streams to cover living expenses or unforeseen financial obligations.

3. Generating Predictable Income

Steady income generation is a primary objective for many fixed-income investors. Bond ladders generate predictable income through regular interest payments from bonds maturing at different intervals.

Each bond within the ladder pays interest at predefined intervals, typically semiannually or annually, depending on the bond’s terms. This staggered payment structure ensures a consistent cash flow stream, which can be essential for budgeting and financial planning purposes.

For example, retirees may structure a bond ladder to coincide with anticipated expenses, such as healthcare costs or home repairs, ensuring that funds are available when needed without relying on volatile market conditions.

4. Enhancing Portfolio Diversification

Diversification is a fundamental strategy in investment management, aimed at spreading risk across different asset classes and securities. Bond ladders enhance portfolio diversification by incorporating bonds with varying credit qualities, issuers, and maturities.

A well-diversified bond ladder may include bonds issued by governments, PSUs, corporations etc. By diversifying across sectors and institutions, investors reduce the risk of significant losses from any single bond issuer or sector-specific downturn.

Moreover, diversification within a bond ladder helps mitigate credit risk—the risk of default—by spreading investments across bonds with different credit ratings and financial profiles. This diversification strategy enhances portfolio stability and resilience against adverse market conditions.

How to construct a Bond Ladder

Building a bond ladder involves several key decisions:

- Investment Horizon: Determine the desired holding period for the ladder, which will influence the range of maturity dates selected. A longer horizon allows for a broader ladder with more potential for income generation.

- Risk Tolerance: Assess your comfort level with interest rate fluctuations and credit risk. Risk-averse investors may prefer shorter-term bonds, while those seeking higher returns might consider a mix of maturities.

- Income Needs: Evaluate your required income level and the potential yield of different bond types. Higher income needs may necessitate a ladder with a focus on higher-yielding bonds.

- Hold to Maturity: To maximize the benefits of regular income and risk management, commit to holding bonds until maturity. Selling bonds before maturity can lead to income loss and potential transaction fees.

- Credit Quality: Focus on high-quality bonds with strong credit ratings (e.g., “A” or better) to ensure predictable income and minimize default risk.

- Diversification: Spread investments across multiple issuers, industries, and bond types to reduce concentration risk. The number of issuers may vary based on credit quality (see table below):

- Yields: Avoid bonds with unusually high yields, as they often indicate higher risk. Focus on bonds with yields that reflect their credit quality.

If you want to build a laddered bond portfolio, Vested offers a range of high-quality bonds with yields up to 14%. By utilizing Vested’s platform, you can potentially enhance your income generation strategy through a diversified bond ladder.

Things to Keep in mind while constructing a Bond Ladder

- Time Horizon and Frequency: Determine the desired length of the ladder and the frequency of bond maturities. A longer ladder with more frequent maturities offers greater flexibility.

- Rebalancing: Regularly review and rebalance the ladder to maintain the desired maturity profile and adjust for changing market conditions or personal circumstances.

- Bond Ratings: Understand the role of credit rating agencies like Moody’s and Standard & Poor’s in assessing bond issuer creditworthiness and always consider their ratings before selecting a bond.

- Investment Costs: Consider transaction fees and other costs associated with buying and selling bonds.

- Tax Implications: Be aware of the tax consequences of different bond types (e.g., municipal bonds, corporate bonds).

By carefully considering these factors, investors can build a bond ladder that aligns with their financial goals and risk tolerance while maximizing the benefits of this investment strategy.

Ladder Structures and Customization

While the classic evenly spaced ladder is popular, variations can cater to specific investor needs:

- Bulletproof Ladder: A more conservative approach where bonds are concentrated in shorter maturities, providing higher liquidity and reduced interest rate risk. This is suitable for investors seeking capital preservation and income generation with minimal volatility.

- Barbell Ladder: Focuses on both short-term and long-term bonds, aiming to balance liquidity and potential for higher returns. This strategy can be beneficial for investors with a moderate risk tolerance who seek a mix of income and capital appreciation.

- Custom Ladders: Tailored to specific investor goals, such as income generation, capital preservation, or a blend of both. These ladders can be designed based on individual risk tolerance, time horizon, and investment objectives.

In essence, while bond ladders promise stability, they often come with hidden costs and limitations. Bond mutual funds, particularly index funds, generally offer better income potential, diversification, liquidity, and cost-efficiency.

Conclusion

Bond laddering offers a structured approach to fixed-income investing, providing potential benefits like income generation, interest rate risk management, and portfolio diversification. However, it requires careful planning, ongoing management, and an understanding of its limitations. By carefully considering factors such as investment goals, risk tolerance, and market conditions, investors can determine if a bond ladder aligns with their financial objectives.