Skip to content

Skip to content

If we were to ask you what the most important factor is when deciding on an investment, what would you say?

Usually, we hear answers like price, returns, and a way to measure risk. And you know what? That’s completely fair—it makes perfect sense.

After all, it’s crucial to know what price you’re paying, how much return you can expect, and how to quantify the risks. Numbers matter, right? They help you compare risks across various investments.

But things start getting a little confusing when technical terms come into play—especially with fixed-income instruments like bonds. That’s exactly where most investors get stuck, and that’s precisely what we’re going to clear up.

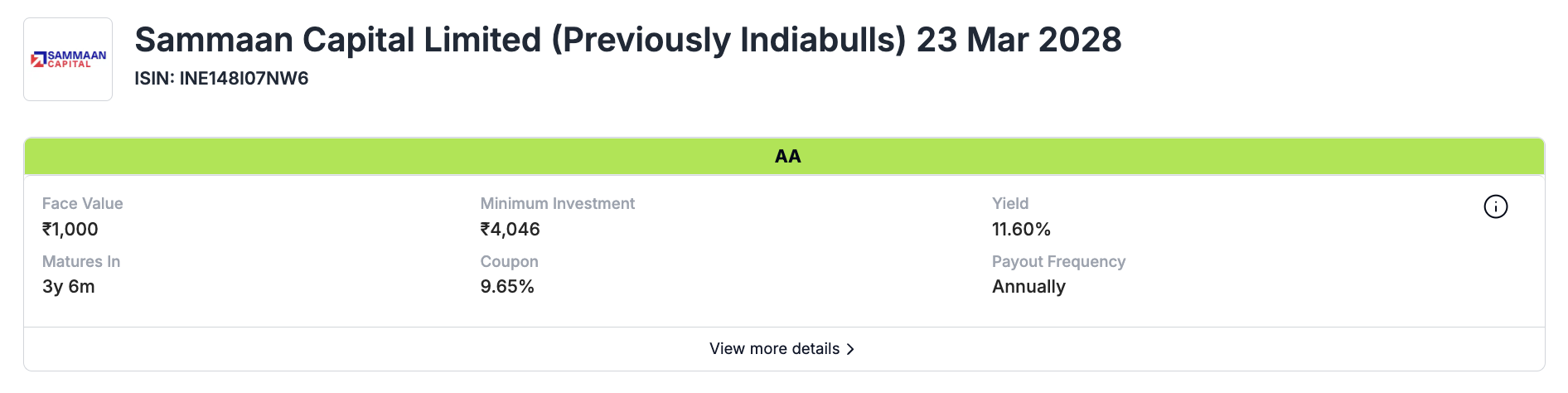

Figure 1: Sammaan Capital Limited Bond Details

Take a look at the bond in the image (see Figure 1). You see terms like investment amount, coupon, yield, and maturity date. These are all important, but they’re very different from the terms you’d typically see with stock investments.

Terms like price, yield, and duration might seem intimidating at first, but once you understand what they represent, you’ll see how they fit into the larger picture of bond investing. Whether you’re looking at how much you need to invest, what kind of return to expect, or how to measure the risks involved, this guide will provide the clarity you need to make informed decisions.

Understanding Bond Price

Alright, let’s start with two of the most important terms you’ll see when it comes to bonds: Face Value and Bond Price. Understanding these terms will help you get a clearer picture of what you’re really paying for and what you’ll get back from a bond investment.

Let’s dive in!

Face Value

The face value of a bond (also known as par value) is the amount you, as the bondholder, will receive when the bond reaches its maturity date. Think of it as the bond’s original worth. When bonds are initially issued, they are sold at their face value—so, if the face value is ₹1,000, that’s exactly what you pay for it when it is first offered to the market.

Here’s how it works: If you buy a bond directly from the issuer when it’s first issued, you’ll pay ₹1,000 (or whatever the face value is). At the end of the bond’s term, when the bond matures, you get this ₹1,000 back as the principal repayment, along with any interest payments you earned during the bond’s life.

In the example of the Sammaan Capital Limited bond above, the face value is ₹1,000.

So, when this bond matures on 23rd March 2028, the issuer will pay you ₹1,000 for each bond you hold. However, if you’re buying this bond in the secondary market (after the bond was first issued), the price you pay might be higher or lower than the face value depending on current interest rates and other factors.

Bond Price

Now, the bond price is the amount you’ll pay today to buy the bond—this can be higher, lower, or equal to the face value. The bond price fluctuates after it’s issued due to changes in interest rates and the bond’s coupon rate.

For instance, in the example above, the bond’s minimum investment price is ₹810.6. That’s lower than the face value of ₹1,000.

Why the difference?

This happens because of the bond’s coupon rate (the interest rate it pays). If the coupon rate is higher than current market interest rates, the bond becomes more valuable, and investors are willing to pay a premium to get those higher interest payments.

How Is Bond Price Calculated?

The bond price is calculated by taking the present value of all future cash flows (coupon payments and the face value at maturity) and discounting them back to their value today.

Here’s the formula:

Let’s break that down with an example:

- Face value: ₹1,000

- Coupon rate: Let’s say 10% (which means you’ll receive ₹100 per year as interest)

- Years to maturity: 3 years

- Market yield: 8%

To calculate the bond price:

- You’ll receive ₹100 each year as interest (the coupon payment).

- At the end of 3 years, you’ll get back the ₹1,000 face value.

Using the market yield (8%) to discount these future payments back to today’s terms, the bond price works out like this:

When you crunch the numbers, the bond price comes out to be around ₹1,051. In this case, the price is higher than the face value because the coupon rate (10%) is more attractive than the current market yield (8%).

How Coupons, Price, and Yield Are Related?

Now that we’ve covered face value and bond price, it’s time to dive into how the coupon, price, and yield are connected. These three terms are essential to understanding bond investments, and once you grasp their relationship, you’ll be able to make more confident investment decisions.

Let’s keep things simple by using the Sammaan Capital Limited bond from the image as an example.

What Is a Coupon?

The coupon is the fixed interest payment that a bondholder receives, usually annually or semi-annually. It’s the income you earn from the bond.

In our example, the coupon rate is 9.65%, which means you’ll receive ₹96.50 each year for every ₹1,000 of face value (or principal) that you hold.

How Does Coupon Relate to Price?

The relationship between the coupon rate and the price of a bond is crucial to understanding how bonds behave in the market. While the coupon rate is fixed, the bond’s price fluctuates based on changes in interest rates. Let’s break it down to make sense of this dynamic using the Sammaan Capital Limited bond example.

When Bonds Are First Issued

When a bond is first issued, it is typically sold at its face value (also called par value). In our example, that’s ₹1,000.

The coupon rate—which determines the interest you earn—is set based on prevailing market interest rates. For instance, if market interest rates are around 9.65%, the bond issuer might set the coupon rate at 9.65% as well, meaning you’d earn ₹96.50 annually on each ₹1,000 of face value.

How Changes in Interest Rates Affect Bond Prices?

Over time, interest rates in the market fluctuate due to economic conditions. However, the coupon rate on the bond remains fixed. This causes the bond’s price to adjust in response to market interest rates.

Here’s how it works:

When Interest Rates Rise: If market interest rates rise above the bond’s coupon rate, new bonds will be issued at these higher rates. Let’s say new bonds in the market are now offering 12% interest. Investors would prefer these new bonds because they provide a higher return compared to your bond, which is still paying a fixed coupon of 9.65%.

To make your older bond more attractive, its price will drop below face value (in this case, to ₹810.6) to compensate for its lower coupon rate. This drop in price gives investors a better yield, making it competitive with new, higher-interest bonds.

When Interest Rates Fall: Conversely, if market interest rates fall below your bond’s coupon rate, let’s say to 7%, your bond with a fixed 9.65% coupon becomes more valuable. Why? Because it pays more interest than new bonds being issued in the market.

In this case, investors would be willing to pay more than the face value for your bond because it offers a better return than newly issued bonds. So, your bond’s price would rise above ₹1,000, reflecting the higher demand for its better coupon rate.

So, What Is Yield?

Yield is the actual return you earn on a bond based on the price you pay for it. While the coupon rate is fixed and represents the interest paid annually, the yield changes depending on the bond’s current price in the market. The most important measure of yield is Yield to Maturity (YTM), which calculates your total return if you hold the bond until it matures. YTM accounts for both the coupon payments and any price difference between what you pay and the bond’s face value.

Let’s break it down using the Sammaan Capital Limited bond:

- Face value: ₹1,000

- Coupon rate: 9.65% (you get ₹96.50 annually)

- Current bond price: ₹810.6

- YTM: 11.90% (96.5 divided by 810.6)

Since you’re buying the bond at ₹810.6, which is below face value, the yield is higher than the coupon rate. Even though the coupon payment is ₹96.50, you’re paying less upfront, so your total return is greater. The YTM of 11.90% reflects the overall return you’ll earn, including the annual coupon payments and the ₹1,000 you’ll receive at maturity.

But if you look at the image, the YTM is listed as 11.60%, not 11.90%. Why is that?

This slight difference is because the bond pays interest annually and was issued on 23rd March 2023. Now, as we’re writing this in September 2024, we’re halfway through the interest period, meaning interest has accrued from March to September 2024. If you sell the bond now, the buyer would owe you that accrued interest. This adjustment causes the yield to dip slightly to 11.60%.

However, as an investor, you don’t need to focus too much on these minor technicalities—they don’t significantly affect your overall yield or returns.

Understanding Duration: Connecting It to Price and Yield

Now that we’ve unpacked yield and its connection to bond prices, it’s time to explore how duration fits into the picture.

Duration is a powerful tool that tells you how sensitive a bond’s price is to changes in interest rates, and it ties directly into both yield and price movements. While yield explains the return you’ll get, duration helps you understand how much that return could fluctuate based on market conditions.

How Duration Connects Price and Yield?

- Yield and price have an inverse relationship—when yields rise, bond prices fall, and vice versa.

- Duration measures the degree of this price change when yields move. Essentially, it tells you how much the price will drop or rise for a 1% change in interest rates.

If a bond has a higher duration, its price is more sensitive to changes in yields. A small rise in yields could lead to a significant drop in the bond’s price. Conversely, a lower-duration bond will have a smaller price movement in response to the same yield change, making it less volatile.

Let’s apply this to the Sammaan Capital Limited bond:

- Current bond price: ₹810.6

- YTM: 11.60%

While we haven’t calculated the exact duration for this bond, let’s imagine it has a high duration. This means if market yields increase, the price of this bond could drop significantly from ₹810.6 because it’s sensitive to interest rate changes. On the flip side, if yields drop, the bond’s price would rise more sharply compared to a bond with a lower duration, offering you greater potential price appreciation.

Duration as a Risk Indicator

Think of duration as the sensitivity gauge for your bond’s price. A higher duration means greater price swings as interest rates change. For instance, if interest rates go up by 1%, a bond with a duration of 5 years could lose around 5% of its price. The opposite is true as well: if rates drop, the bond’s price could increase by that same percentage.

- Higher Duration: Greater price sensitivity to interest rate changes (both risks and rewards).

- Lower Duration: Less price sensitivity, meaning the bond is more stable and less affected by rate fluctuations.

Making Prudent Investment Decisions with Bond Information

Navigating the bond market can be challenging, but with the right resources, it becomes a powerful avenue for diversifying your investment portfolio. Understanding key concepts like bond pricing, yield, and duration is crucial to making informed decisions.

When you choose to invest through platforms like Vested, each bond listed comes with comprehensive information tailored to help you evaluate its potential. Vested ensures that investors like you have access to detailed data on price, yield, maturity, and other relevant factors, empowering you to compare and analyze different bonds effectively.

By utilizing these insights provided by Vested, you can confidently assess the risks and returns associated with various bond investments, ensuring that your investment decisions align with your financial goals and risk tolerance. This approach not only simplifies the investment process but also enhances your ability to make prudent and informed decisions in the bond market.

Frequently Asked Questions (FAQs)

Q1. What’s the difference between coupon rate and yield?

- Coupon rate is the fixed interest payment a bondholder receives annually, based on the bond’s face value. For example, a bond with a 9.65% coupon rate pays ₹96.50 annually for each ₹1,000 face value.

- Yield, on the other hand, represents the actual return you earn based on the price you pay for the bond. If you buy the bond at a discount (less than face value), your yield will be higher than the coupon rate because you’re receiving the same interest payment but paid less upfront.

Q2. How does duration impact my bond investment?

Duration measures a bond’s price sensitivity to interest rate changes. Bonds with higher durations experience larger price fluctuations when interest rates move. If interest rates rise, higher-duration bonds will see a larger drop in price, while lower-duration bonds will be less impacted. Duration helps you manage the risk of interest rate changes in your bond portfolio.

Q3. Why does bond price drop when interest rates rise?

When interest rates rise, newly issued bonds offer higher yields, making older bonds with lower coupon rates less attractive. To compensate, the price of existing bonds drops so that their yield aligns with current market rates. This inverse relationship between bond price and interest rates is a key concept for bond investors.

Q4. What is Yield to Maturity (YTM) and why is it important?

Yield to Maturity (YTM) is the total return you can expect if you hold a bond until maturity. It considers both the coupon payments and any price difference between what you paid for the bond and its face value. YTM is important because it gives you a complete picture of the bond’s return, helping you compare bonds with different prices and coupons.

Q5. How does accrued interest affect bond transactions?

Accrued interest is the interest that accumulates between coupon payment dates. If you buy or sell a bond between interest payment periods, the buyer compensates the seller for the interest earned up to that point. While it slightly impacts the transaction price, it doesn’t significantly affect the overall yield or return.

Q6. Should I invest in long-duration or short-duration bonds if I expect interest rates to rise?

If you expect interest rates to rise, it’s generally safer to invest in short-duration bonds. These bonds are less sensitive to rate changes, meaning their prices will drop less compared to long-duration bonds. Conversely, if you expect rates to fall, long-duration bonds could offer greater price appreciation and higher returns.