Skip to content

Skip to content

Imagine you have some extra money, and a friend needs funds to start a project. You both agree to formalize the arrangement through an agreement. As the lender, you expect to receive a return on your investment, which you can structure in two ways.

The first option is equity funding. In this case, you invest money for a stake in the project. Your returns are tied to the project’s success—if it performs well, your share value increases, and you might receive dividends. Equity funding offers the potential for significant returns over the long term, especially if the project grows and gains value.

The second option is debt funding, which involves lending money with the understanding that it will be repaid with interest. This is set up through a bond, a legal contract that specifies the loan amount, interest rate, and repayment period. Bonds offer fixed returns and a defined term, providing you with clarity on how much you’ll earn and when you’ll receive it. This structure makes bonds an attractive option if you prefer to know your expected returns and timeline upfront.

This is a basic concept that every investor should be aware of—understanding the difference between equity and debt funding is crucial for making informed financial decisions.

As an investor, it’s essential to grasp three key aspects of the bond market: how bonds work, its structure and the different types of bonds available. Understanding the bond market’s structure reveals how it operates while knowing the various bond types helps you evaluate their risk and return profiles. In this blog, we’ll guide you through the types of bonds you need to know, enabling you to make investment decisions that align with your financial goals.

Different Types of Bonds in India

Investors must know the different types of bonds. It helps them assess each bond’s risk and return. These distinctions help investors make better decisions. They can now align their choices with their financial goals and risk tolerance.

Bonds in India fall into different categories based on several key factors. Each of these categories further breaks down into specific types that offer different benefits and risks. Let’s understand these categories:

- Issuer classification

- Collateral backing

- Seniority-based classification

- Credit quality

- Interest rate structure

- Maturity spectrum

- Market listing status

- Convertibility feature

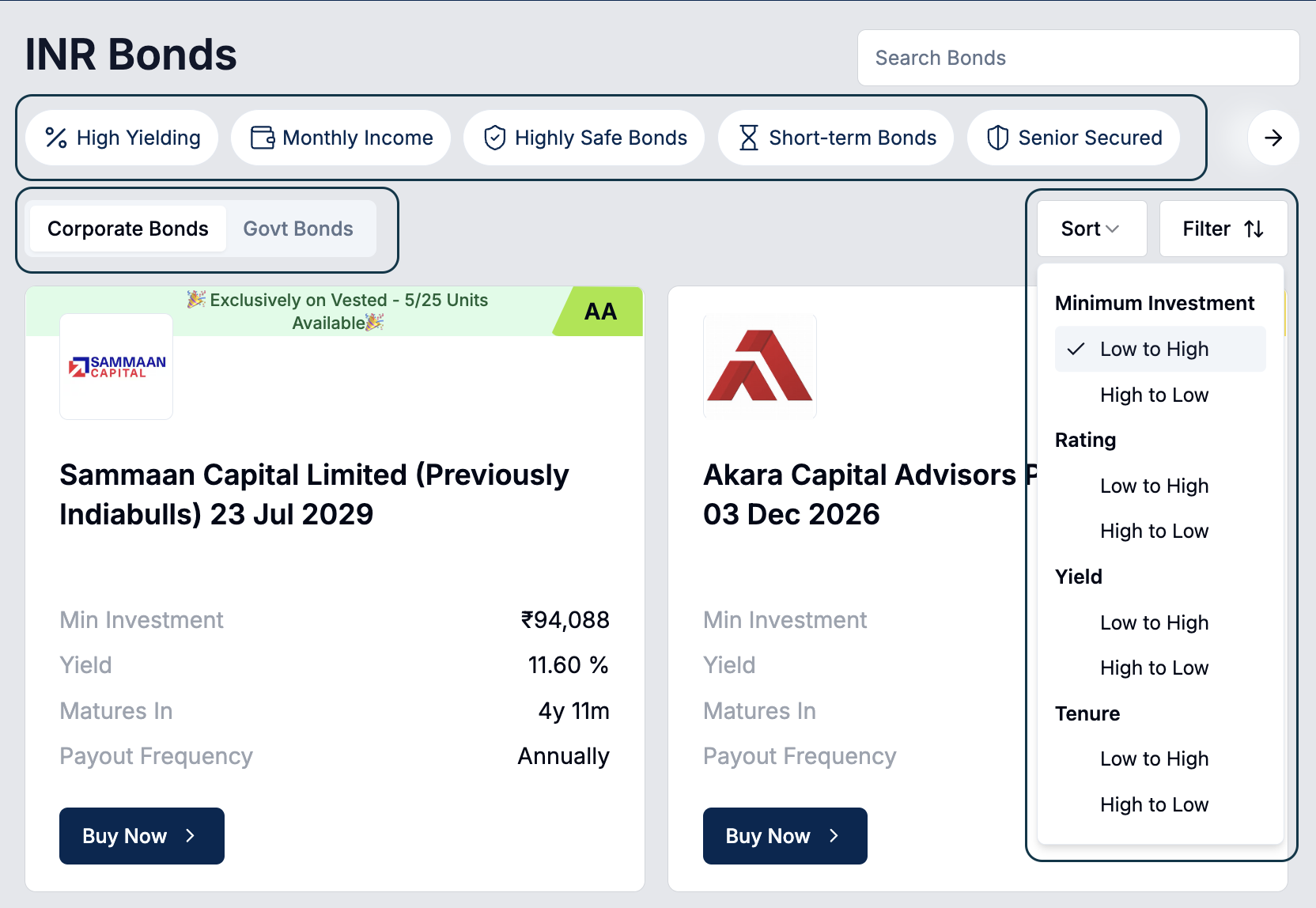

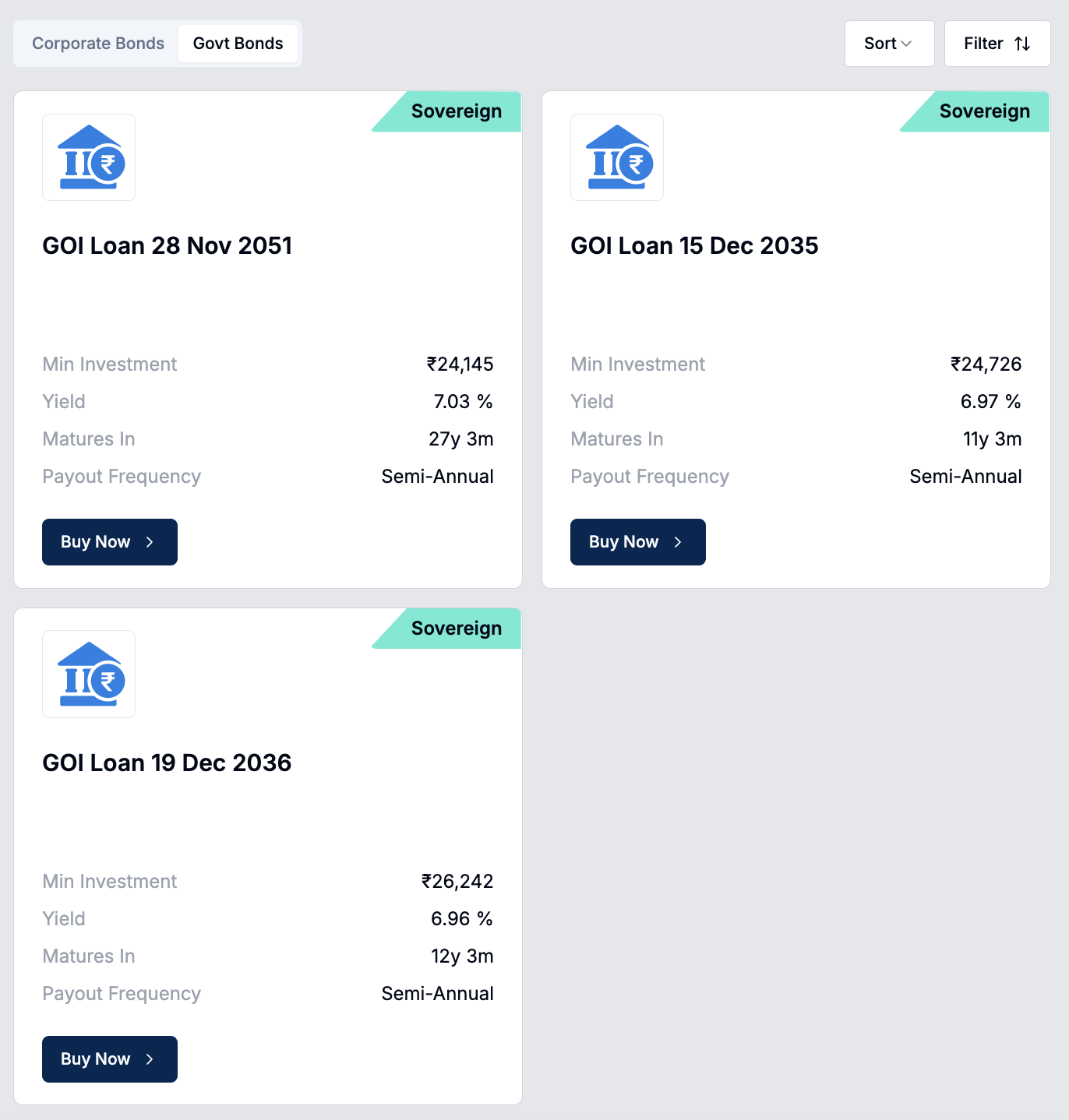

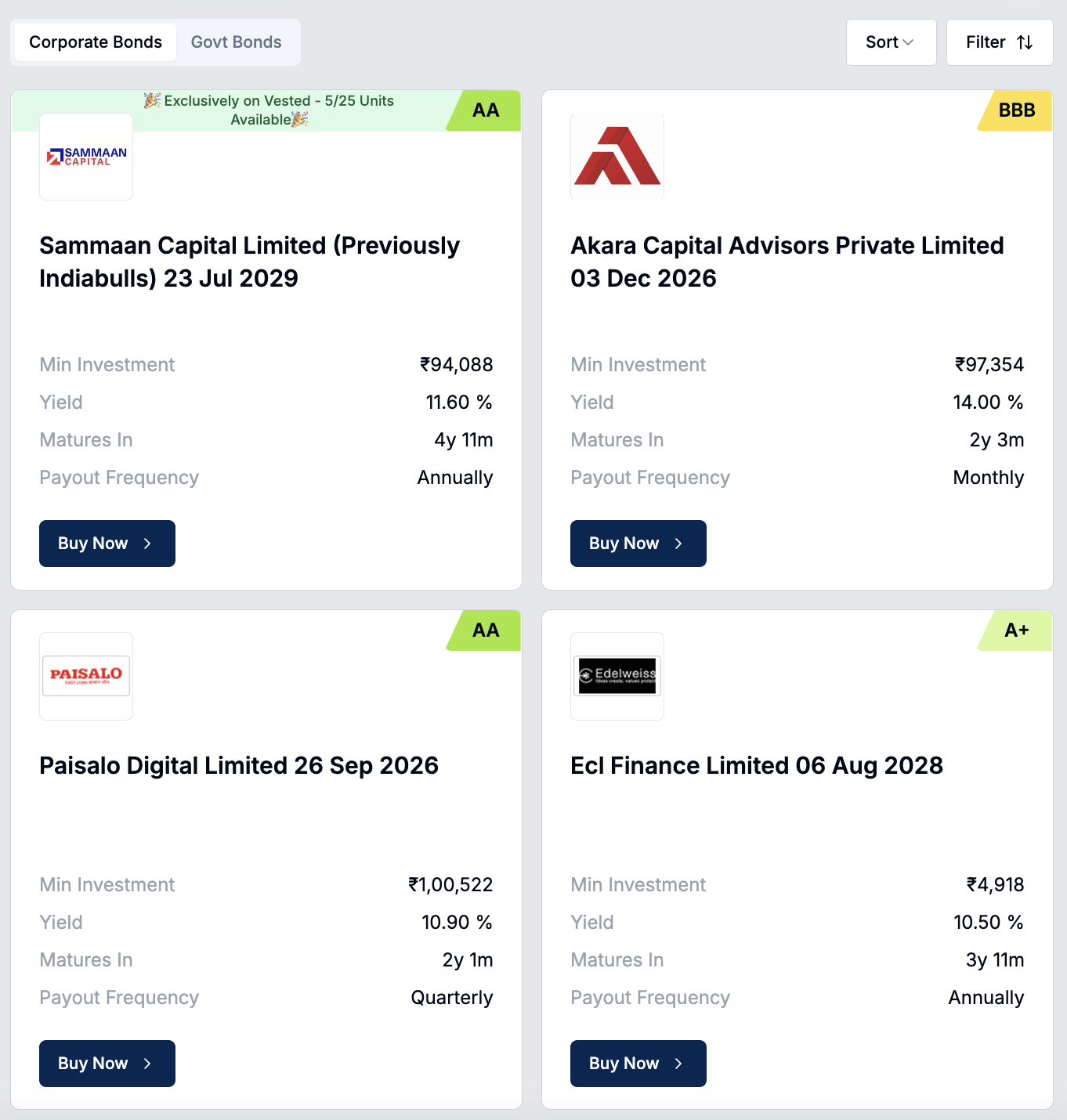

As an investor, these categories are often used to filter bonds when selecting investments. Even when you log in to invest through INR Bonds, you will find these criteria (see Figure 1) to help you pick and choose. Thus, understanding what each category includes is essential for making informed investment decisions.

Figure 1: Categorization of Bonds

1. Issuer Classification

The issuer of a bond is crucial because it directly impacts the bond’s risk and return. Timely interest payments and return of the principal at maturity depend on the issuer’s financial health.

Types of Issuers:

Government Bonds:

- Central Government Bonds: Issued by the Government of India, such as Government Securities (G-Secs) and Treasury Bills (T-Bills). These have a reputation for being extremely safe with low risk.

- State Government Bonds: Known as State Development Loans (SDLs), issued by state governments. While still relatively safe, they may carry slightly more risk than central government bonds.

Corporate Bonds:

- Public Sector Undertaking (PSU) Bonds: Issued by government-owned companies. They are safer than private corporate bonds but offer slightly lower returns.

- Private Sector Bonds: Issued by private companies, these bonds typically offer higher returns to compensate for the higher risk associated with private issuers.

Municipal Bonds:

- Urban Local Bodies Bonds: Issued by municipal corporations, these bonds are used to finance infrastructure projects. They may offer tax benefits and are generally safe, though not as secure as government bonds.

On the INR Bonds, you have the option to select between Government Bonds (see Figure 2) and Corporate Bonds (see Figure 3), allowing you to choose the type of issuer that best aligns with your investment strategy and risk tolerance.

Figure 2: Government Bonds on Vested

Figure 3: Corporate Bonds on Vested

2. Collateral Backing

Collateral backing determines whether a bond is secured by assets, which affects its safety. Secured bonds are less risky because they are backed by specific assets that can be claimed if the issuer defaults.

Types of Collateral Backing:

Secured Bonds:

- Asset-Backed Bonds: These bonds are secured by specific assets, such as real estate or equipment. In case of default, bondholders have a claim on these assets.

- Mortgage-Backed Bonds: Secured by mortgages, these bonds are common in the real estate sector. They offer lower yields but are safer due to the underlying collateral.

Unsecured Bonds (Debentures):

- General Obligation Bonds: These bonds aren’t backed by specific assets. They rely solely on the issuer’s creditworthiness. They tend to offer higher interest rates due to the increased risk.

- Subordinated Debentures: They are riskier than other bonds. They have lower priority for repayment. But, they offer higher returns.

3. Seniority-Based Classification

Seniority determines the order in which bondholders are repaid in the event of the issuer’s bankruptcy. This classification affects the bond’s risk level and its place in the capital structure.

Types of Seniority:

Senior Bonds:

- Senior Secured Bonds (First-Lien Bonds): These bonds are first in line to be repaid and are secured by specific assets. They are the safest type of bond within a company’s capital structure.

- Senior Unsecured Bonds: These bonds are not backed by assets but still take precedence over subordinated bonds in case of default.

Subordinated (Junior) Bonds:

- Subordinated Debt: These bonds are repaid only after senior debts have been settled. They offer higher interest rates due to the increased risk.

- Perpetual Bonds: Often subordinated, these bonds do not have a maturity date and offer ongoing interest payments, but with higher risk due to their lower repayment priority.

4. Credit Quality

Credit quality reflects the issuer’s ability to repay the bond, which is crucial for assessing the risk of default. Higher credit quality means lower risk but often lower returns, and vice versa.

Types of Credit Quality:

Investment-Grade Bonds:

- AAA to BBB-Rated Bonds: These bonds are considered safe with a low risk of default. They are issued by financially stable entities and are ideal for conservative investors seeking steady returns.

- Bank Bonds: Often rated high, these bonds are issued by banks and are generally considered safe due to regulatory oversight and financial stability.

High-Yield (Junk) Bonds:

- BB+ and Lower-Rated Bonds: These bonds offer higher returns but come with a higher risk of default. They are often issued by companies with lower credit ratings or in more volatile industries.

- Distressed Bonds: These bonds are rated even lower and are at a high risk of default. They offer the highest yields but are suitable only for aggressive investors.

5. Interest Rate Structure

The structure of interest payments affects the bond’s predictability and attractiveness, depending on the interest rate environment.

Types of Interest Rate Structures:

Fixed-Rate Bonds:

- Consistent Interest Payments: These bonds pay a fixed interest rate throughout their tenure, offering predictable and stable returns, making them ideal for income-focused investors.

- Government Bonds: Most Indian government bonds fall into this category, providing stability and security.

Floating-Rate Bonds:

- Variable Interest Payments: The interest rate on these bonds changes periodically, based on a benchmark rate like the RBI’s repo rate. They offer protection against rising interest rates.

- Corporate Floating-Rate Bonds: Common in corporate finance, these bonds adjust their interest payments according to market conditions.

Zero-Coupon Bonds:

- No Regular Interest: These bonds are issued at a discount and redeemed at face value upon maturity, providing all returns in one lump sum. They are suitable for investors seeking a long-term investment without the need for regular income.

- Long-Term Savings Bonds: Often used for long-term financial goals, such as retirement savings.

6. Maturity Spectrum

Maturity affects a bond’s sensitivity to interest rate changes and its suitability for different investment horizons.

Types of Maturity:

Short-Term Bonds:

- Maturities of Less Than 3 Years: These bonds are less sensitive to interest rate changes and offer quick liquidity, making them ideal for conservative investors or those with short-term financial goals.

- Treasury Bills: Commonly used by the government for short-term financing, they offer low returns but high safety.

Medium-Term Bonds:

- Maturities of 3 to 7 Years: These bonds offer a balance between risk and return, suitable for investors looking for stable income over a medium timeframe.

- Corporate Medium-Term Bonds: Issued by corporations, these bonds are popular among income-focused investors seeking a balance between safety and returns.

Long-Term Bonds:

- Maturities of More Than 7 Years: These bonds are more sensitive to interest rate fluctuations but offer higher yields. They are suitable for long-term investors willing to take on more risk for greater returns.

- Government Securities (G-Secs): Often used for long-term funding, these bonds offer safety and steady income.

Perpetual Bonds:

- No Maturity Date: These bonds pay interest indefinitely and are often issued by banks to meet regulatory capital requirements. They carry higher risks due to their perpetual nature.

- Bank Perpetual Bonds: These bonds are common in the banking sector and offer higher yields to compensate for the lack of maturity.

7. Market Listing Status

Whether a bond is listed or unlisted affects its liquidity and the ease with which it can be traded.

Types of Market Listing:

Listed Bonds:

- Traded on Stock Exchanges: These bonds are listed on exchanges like the NSE or BSE, providing transparency and liquidity. Investors can buy or sell these bonds easily in the secondary market.

- Government and Corporate Bonds: Many government bonds and large corporate bonds in India are listed, offering safety and ease of trade.

Unlisted Bonds:

- Privately Traded: These bonds are not traded on public exchanges and may be sold through private placements. They offer higher yields but come with less liquidity and transparency.

- Private Corporate Bonds: Often issued by smaller companies, these bonds are riskier due to their lack of liquidity and public trading.

8. Convertibility Feature

Convertibility into equity can provide additional upside potential, allowing bondholders to participate in the company’s growth.

Types of Convertibility:

Convertible Bonds:

- Option to Convert into Equity: These bonds can be converted into a predetermined number of shares of the issuing company, offering potential capital appreciation in addition to interest income.

- Equity-Linked Bonds: Often issued by companies looking to raise capital without immediately diluting their equity, these bonds appeal to investors looking for growth opportunities.

Non-Convertible Bonds:

- Cannot Be Converted: These bonds must be held until maturity or sold as bonds. They typically offer higher interest rates due to the lack of equity upside.

- Fixed-Return Bonds: Popular among conservative investors who prefer stable, predictable income without the variability of equity markets.

What Are the Main Features of Bonds

When you invest in bonds, you’re essentially lending money to the bond issuer in exchange for regular interest payments and the return of the principal amount when the bond matures. To make informed decisions, investors need to understand several key features of bonds. These features are typically published to provide transparency, help assess risk, and assist investors in aligning bond investments with their financial goals.

1. Face Value (Principal)

The face value, also known as the principal or par value, is the amount of money that the bond issuer agrees to repay the bondholder at the bond’s maturity. This is the nominal value of the bond, and it is also the reference amount used to calculate the interest payments (coupon payments).

Investor Consideration: Investors should look at the face value to understand the initial capital they are committing and the amount they will receive at maturity. Comparing the face value with the current market price can also help in identifying whether the bond is trading at a discount or a premium.

2. Maturity Period

The maturity period of a bond refers to the length of time from the date of issuance until the issuer is obligated to repay the bond’s face value to the bondholder. Bonds can have short-term (up to 3 years), medium-term (3 to 10 years), or long-term (more than 10 years) maturities.

Investor Consideration: Investors should consider the maturity period in relation to their investment horizon. If they need liquidity soon, short-term bonds may be preferable. For those looking for higher yields and who are comfortable with longer investment horizons, long-term bonds may be a better choice.

3. Minimum Investment

The minimum investment is the smallest amount of money that an investor must put into purchasing a bond. This is often set by the issuer and can vary significantly depending on the type of bond and the issuer.

Investor Consideration: Investors should ensure that the minimum investment amount fits within their budget and overall portfolio strategy. High minimum investment requirements might restrict an investor’s ability to diversify across multiple bonds.

4. Coupon Rate (Interest Rate)

The coupon rate is the annual interest rate that the bond issuer pays to the bondholder, expressed as a percentage of the bond’s face value. This interest is typically paid at regular intervals, such as annually or semi-annually.

Investor Consideration: Investors should compare the bond’s coupon rate to current interest rates in the market. If the coupon rate is higher than the prevailing market rates, the bond could be an attractive investment. However, they should also consider the risk associated with higher coupon rates, as these often accompany higher-risk bonds.

5. Yield

Yield represents the return an investor can expect on a bond, considering both the interest payments and any capital gains or losses if the bond is purchased at a price different from its face value. It’s a dynamic measure that changes with market conditions and the bond’s price.

Investor Consideration: Investors should look at the yield to assess whether the bond meets their return expectations, especially if the bond is being bought in the secondary market. A higher yield might be attractive but often comes with higher risk, so it’s important to balance yield with the bond’s credit quality and other risk factors.

6. Payout Frequency

Payout frequency refers to how often the bond issuer makes interest payments to the bondholder. Common frequencies include annually, semi-annually, quarterly, or monthly.

Investor Consideration: Investors should choose a bond with a payout frequency that aligns with their cash flow needs. For instance, retirees or those needing regular income might prefer bonds with monthly or quarterly payouts, while others may be content with annual payments.

7. Security

Security in the context of bonds refers to whether the bond is backed by specific assets of the issuer, making it a secured bond. Unsecured bonds, also known as debentures, are not backed by collateral and are thus riskier.

Investor Consideration: Investors who are risk-averse should consider secured bonds, especially in volatile economic conditions. They should also evaluate the type and value of the collateral backing the bond to ensure it provides adequate protection.

8. Seniority

Seniority determines the order in which bondholders are repaid in the event of the issuer’s bankruptcy. Senior bonds are repaid first, followed by subordinated or junior bonds.

Investor Consideration: Investors should evaluate the seniority of a bond to understand its risk profile. Those seeking lower risk might prefer senior bonds, even if they offer lower yields. Subordinated bonds might offer higher returns but come with greater risk, appealing to those with a higher risk tolerance.

9. Credit Rating

A bond’s credit rating reflects the creditworthiness of the issuer, indicating the likelihood that the issuer will be able to meet its financial obligations. Ratings are assigned by agencies such as CRISIL, ICRA, and CARE, and range from AAA (highest) to D (default).

Investor Consideration: Investors should choose bonds with a credit rating that matches their risk tolerance. Those seeking stability might prefer investment-grade bonds (rated BBB or higher), while those willing to take on more risk for potentially higher returns might consider lower-rated bonds.

Key Takeaways

Bonds are essential for a well-diversified portfolio, providing stability, regular income, and capital preservation. In India, issuers categorize bonds based on interest rate, maturity, security, and convertibility, each carrying its own risks and benefits. Aligning your bond investments with your financial goals and risk tolerance is key. Consider factors like credit ratings, interest rates, issuer health, and bond maturity to optimize returns and manage risks. Bonds hedge against market volatility, which is crucial for long-term financial stability. If you’re considering bonds, INR Bonds by Vested offers secure and potentially profitable options in Government and Corporate Bonds. You just have to sign up on Vested, complete your KYC and you are all set to invest in Bonds.

Frequently Asked Questions (FAQs)

What are the Popular Bond Types in India?

Popular bond types in India include Government Bonds (like G-Secs), Corporate Bonds, Tax-Free Bonds, and Infrastructure Bonds. These bonds vary in terms of risk, return, and tax benefits.

What is the Primary & Secondary Market in Bonds?

The primary market is where new bonds are issued and sold directly to investors, often through auctions. The secondary market is where existing bonds are traded among investors, typically on exchanges or over-the-counter.

What are the Types of Bonds Based on Credit Rating?

Bonds are classified based on credit ratings into investment-grade bonds (e.g., AAA, AA) and non-investment-grade or “junk” bonds (e.g., BB, B). Investment-grade bonds are considered safer but offer lower yields, while junk bonds carry higher risk and higher returns.

What is the Credit Rating of Government Bonds?

Government bonds typically have high credit ratings, often AAA or equivalent, due to the low risk of default by the government. This makes them one of the safest investment options.

What are the Types of Bonds Based on Maturity Terms?

Bonds are categorized into short-term (up to 3 years), medium-term (3 to 7 years), long-term (over 7 years), and perpetual bonds (no maturity date). Each type has different risk and return profiles based on the duration.

What Bond Type is the Safest One?

Government Bonds are generally considered the safest, especially those with high credit ratings, as they are backed by the government’s ability to meet its financial obligations.

Which Bond Type Has the Highest Yield?

High-yield (junk) bonds, typically issued by corporations with lower credit ratings, offer the highest yields to compensate for the higher risk of default.