Every few months, Wall Street has one of those weeks where everything feels like it is riding on a handful of earnings calls. This is one of those weeks. Except this time, the stakes are genuinely different.

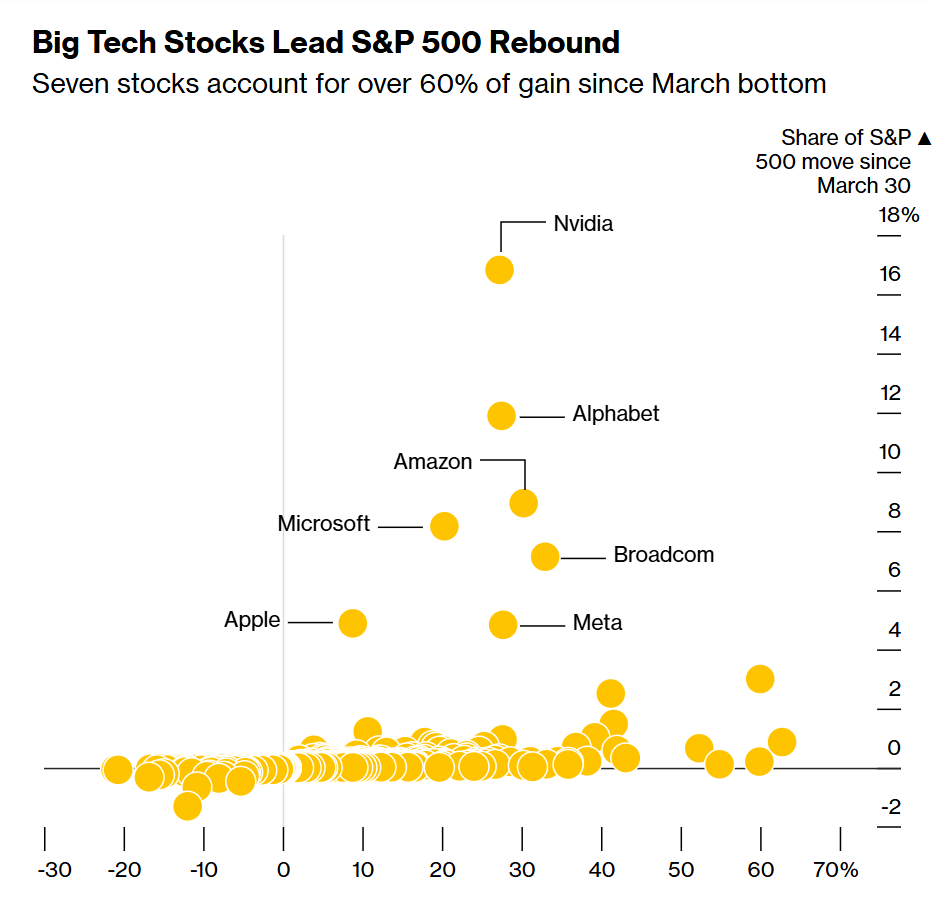

Microsoft, Alphabet, Amazon, Meta and Apple are all reporting earnings within 48 hours of each other. Five of the Magnificent Seven. Back to back. And together, these five companies make up nearly a quarter of the entire S&P 500. Which means this is not just an event for tech investors. This is an event for anyone who has ever put money into an index fund and gone to sleep thinking it would be fine.

But before we get into what could go wrong, let us understand what is actually being tested here.

The Bet That Everyone Made

Over the past two years, the biggest companies in the world made a collective decision. They decided that artificial intelligence was not just a feature. It was the future. And they started spending accordingly.

Meta committed somewhere between $115 and $135 billion on AI infrastructure for 2026 alone. Alphabet doubled its AI spending compared to last year, guiding between $175 and $185 billion. Amazon is projected to cross $200 billion in capital expenditure. And Microsoft spent nearly $30 billion in a single quarter on AI, up 89% year over year.

To put that in perspective, these four companies reporting this week are collectively expected to spend between $600 and $645 billion on AI in 2026. That is not a typo. Six hundred billion dollars, in a single year, from four companies.

The market did not panic when these numbers came out. In fact, it celebrated. Because the assumption was simple: spend big today, earn bigger tomorrow. Investors gave these companies the benefit of the doubt and priced their stocks accordingly.

That benefit of the doubt expires this week.

What Everyone Is Actually Watching

Here is the thing about big tech earnings. Most people focus on revenue beats and EPS surprises. But this week, the number that every analyst, every fund manager and every serious investor is obsessing over is capex. Capital expenditure.

Not because spending is bad. But because at some point, spending has to become earning. And right now, the market is not entirely sure that is happening fast enough.

The concern crystallised this Monday when the Wall Street Journal reported that OpenAI, the company that Microsoft has staked its entire AI future on, is quietly missing its own internal growth targets. That one report was enough to spook the sector. Stocks sold off. The mood turned defensive almost overnight.

And now every one of these companies has to walk on stage and answer the same question. All this money we have spent on AI, is it actually working?

The War Makes Everything Harder

Here is the context that makes this earnings week unlike any other in recent memory. This is the first major earnings cycle since the Iran war began disrupting the global economy earlier this year. Oil prices spiked. Shipping costs climbed. Advertising budgets at smaller companies tightened. Consumer confidence wobbled.

For a company like Amazon, higher oil prices directly translate into higher shipping costs, which directly eat into retail margins. For Meta and Alphabet, whose revenues depend almost entirely on advertising, a slowdown in ad spending from smaller businesses could show up very visibly in the numbers.

The war has not crashed the market. But it has made investors far less forgiving. In a normal quarter, a slight miss on guidance might be brushed off. This week, in this environment, it could trigger something much uglier.

What Each Company Actually Needs to Prove

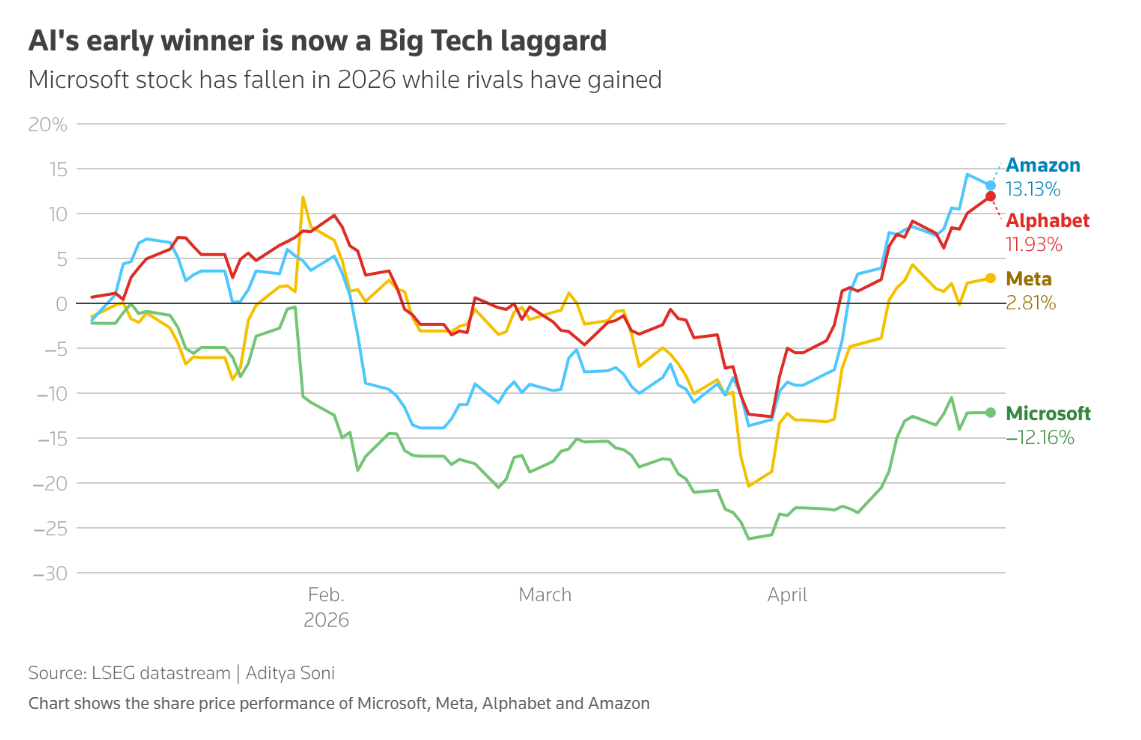

Microsoft has the hardest job this week. Its entire AI story rests on Azure growing fast enough to justify the spending. Investors want to see Azure growing at 37% or above. Anything below 35% and the questions about whether AI investments are paying off become very loud very fast. The Copilot numbers matter too. Microsoft now has 15 million paid Copilot seats, and daily active users have grown tenfold since launch. But monetisation still feels early, and investors want a clearer path to margin expansion.

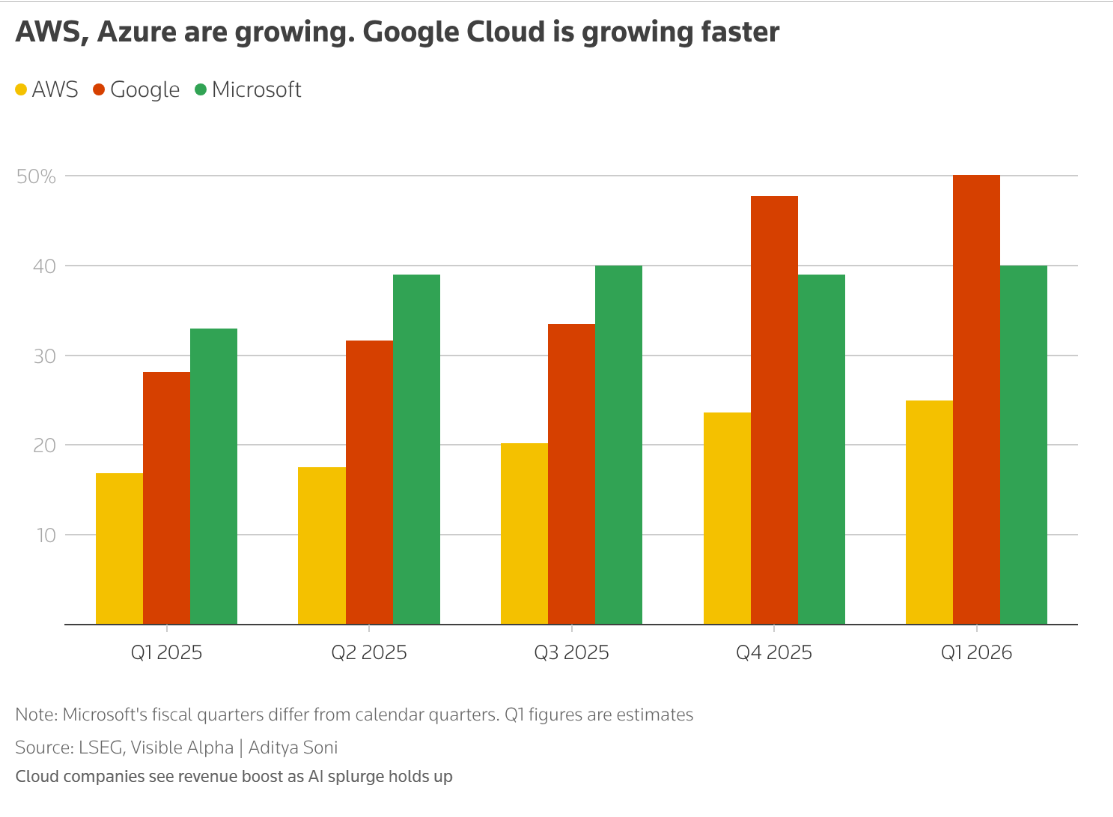

Alphabet needs to show two things simultaneously. One, that Google Search is not being eaten alive by AI tools pulling users away. And two, that Google Cloud is growing fast enough to matter. Cloud grew 48% in Q4 2025. Analysts expect that momentum to continue. If it does, Alphabet looks like a company winning on both sides of the AI equation. If it slows, the narrative gets complicated quickly.

Meta has the most interesting setup. It has already announced 8,000 layoffs this year while simultaneously committing to spend more than any other company on AI. The market will want to know how both of those things are true at the same time. If ad revenue accelerates because of AI-driven targeting improvements, Meta can justify every dollar it is spending. If ad growth slows while capex creeps higher, the story falls apart.

Amazon is the one where AWS re-acceleration is essentially the only thing that matters. Analysts expect AWS growth to accelerate to around 28% or higher. If that happens, every concern about Amazon’s spending gets answered. If it does not, the bull case weakens considerably.

Apple is the outlier in this group. It is not a hyperscaler. It is not burning billions on data centres. Its story this week is about whether the AI iPhone cycle is real, whether services revenue keeps accelerating, and whether China is stabilising. A quieter story, but not a smaller one.

The Framework That Actually Matters

There is a simple way to think about what separates a good week from a bad week for these stocks.

Beat and raise means the company delivered strong results and guided even higher. In this market, that is the only outcome that gets rewarded unconditionally.

Beat and hold means strong results but cautious guidance. In a normal market that would be fine. In a market priced for perfection, that often reads as a warning sign and stocks sell off even on good quarters.

Beat and lower is the nightmare scenario. Strong quarter, weaker outlook. That combination in the current environment could trigger the kind of sector-wide correction that wipes out months of gains in a matter of days.

The technology sector is expected to grow earnings by roughly 41% this year, nearly four times faster than the broader S&P 500. That premium comes with an expectation of flawless execution. And flawless execution, quarter after quarter, in the middle of a global conflict and an AI arms race that nobody fully understands yet, is genuinely very hard to pull off.

So What Actually Happens?

The honest answer is that nobody knows. That is what makes this week so interesting and so dangerous at the same time.

The long term AI story remains intact. The infrastructure being built today will almost certainly generate enormous returns over the next decade. The companies doing the building have wide moats, extraordinary cash flows and management teams that have navigated difficult moments before.

But short term? The market is priced for a version of events where everything goes right. Azure accelerates. Cloud grows. Ad revenues hold. Capex gets justified. Margins improve. If even one of those pieces does not land the way investors expect, the repricing can be swift and severe.

Six hundred and forty five billion dollars in AI spending is either the smartest collective bet in corporate history, or the most expensive lesson the market has ever learned. This week, we start finding out which one it is.