Skip to content

Skip to content

In this Blog, we discuss (i) a new gold rush in AI applications and (ii) Netflix’s shifting strategy.

A new gold rush in AI applications

There’s a Cambrian explosion in consumer-facing AI applications. Thanks to a relatively new class of AI model, the transformer model, we are seeing new applications in generative AI. The transformer model is a machine learning architecture first developed by the folks at Google, published in 2017, that is more parallelizable, requiring significantly less time to train.

It allows for the training of massive datasets (scraped from the internet), generating models that can be used to generate text, images, and even videos:

- Text-to-Image: This is an AI capability whereby the user can enter a text prompt to create an image. Stable Diffusion, Midjourney, and DALL-E2 are some of the more well-known examples. Adobe recently announced that it is integrating similar technologies to help create and edit images faster.

- Text-to-video: This is an AI capability whereby the user enters a text prompt to create a short video. A few weeks ago, Meta (Facebook) announced Make-A-Video. Soon after, Google announced its own version, called Imagen Video.

- Text-to-text: This is an AI capability whereby the user enters text, and the AI generates more text. It can help with writing marketing copy (examples here and here), blog posts (an example here is Lex, an online document writer powered with GPT-3 that helps you write faster. Check out a video of it in action here. It looks incredible.), and even software code (Microsoft has Copilot, which helps programmers write functions faster. Another example is from Replit).

- Text-to-music: It’s still in its early days, but here are two examples.

There’s a paradigm shift into the mainstream. These AI applications are now consumer-facing (as opposed to helping in the background: making search better or reducing data center energy usage). As a result, despite the difficult macroeconomic conditions, some of these companies are raising venture funding at sky-high valuations. For example, Stability AI, a for-profit company that developed the open-source Stable Diffusion mentioned above, just raised a $101 million seed round, valuing the company at $1 billion, at a pre-revenue and pre-product stage.

It’s still an open question whether these AI application companies will be able to capture a meaningful share of the value. These companies use AI hardware made by NVIDIA (which has the lion’s share of AI hardware market share), hosted in one of the cloud platform providers (and there are only three providers: AWS, Microsoft, and Google Cloud), and provide their services via API. Typically, API companies, due to the nature of consumption-based variable costs, have less gross margins than the pure play software-as-a-service model.

Nevertheless, one thing that is unexpected is the pace of the release of these consumer-facing applications. Everyone thought that AI and automation will replace blue-collar workers first (the prime example often cited in the media is the fear of self-driving cars replacing commercial drivers), but as it turns out, AI will impact white-collar jobs first. But for now, these AI applications are not replacing, but rather augmenting the workers.

Note: this post is still written by a human.

The shift in Netflix’s monetization strategy

Netflix recently announced its Q3 2022 earnings. The company reported paying subscriber growth that is above expectations. It added 2.4 million new paying subscribers (vs. 1 million forecasts). As is always the case, the share price jumped after the subscriber growth beat expectations.

The most interesting part of the earnings release, however, is that Netflix decided to stop providing forward guidance on expected paying subscribers starting with the next quarter.

Predictability of growth is becoming worse

Since Q1 2020, Netflix lost the ability to accurately predict paying subscriber growth. Since this period, Netflix missed more than 1/3 of its paying subscriber forecast. This is partly due to the global lockdown at the beginning of Covid, which pulled forward the demand for Netflix subscriptions. When growth slowed down in 2021, management attributed that due to the pulling forward effect. But the misses are still occurring in 2022. It seems that the pull-forward effect alone does not explain the forecast misses. What might be true is that:

- In addition to the pulling forward effect, Netflix is running into market saturation in North America. A lot of new paying subscribers added in the US are not as sticky. They “service hop” different streaming services. This makes the business hit-driven (more so than before). This past quarter, Netflix had a handful of hit releases that may have contributed to stronger-than-expected paying subscriber growth.

- Netflix is also experiencing lagging growth in other regions as users are becoming more price sensitive.

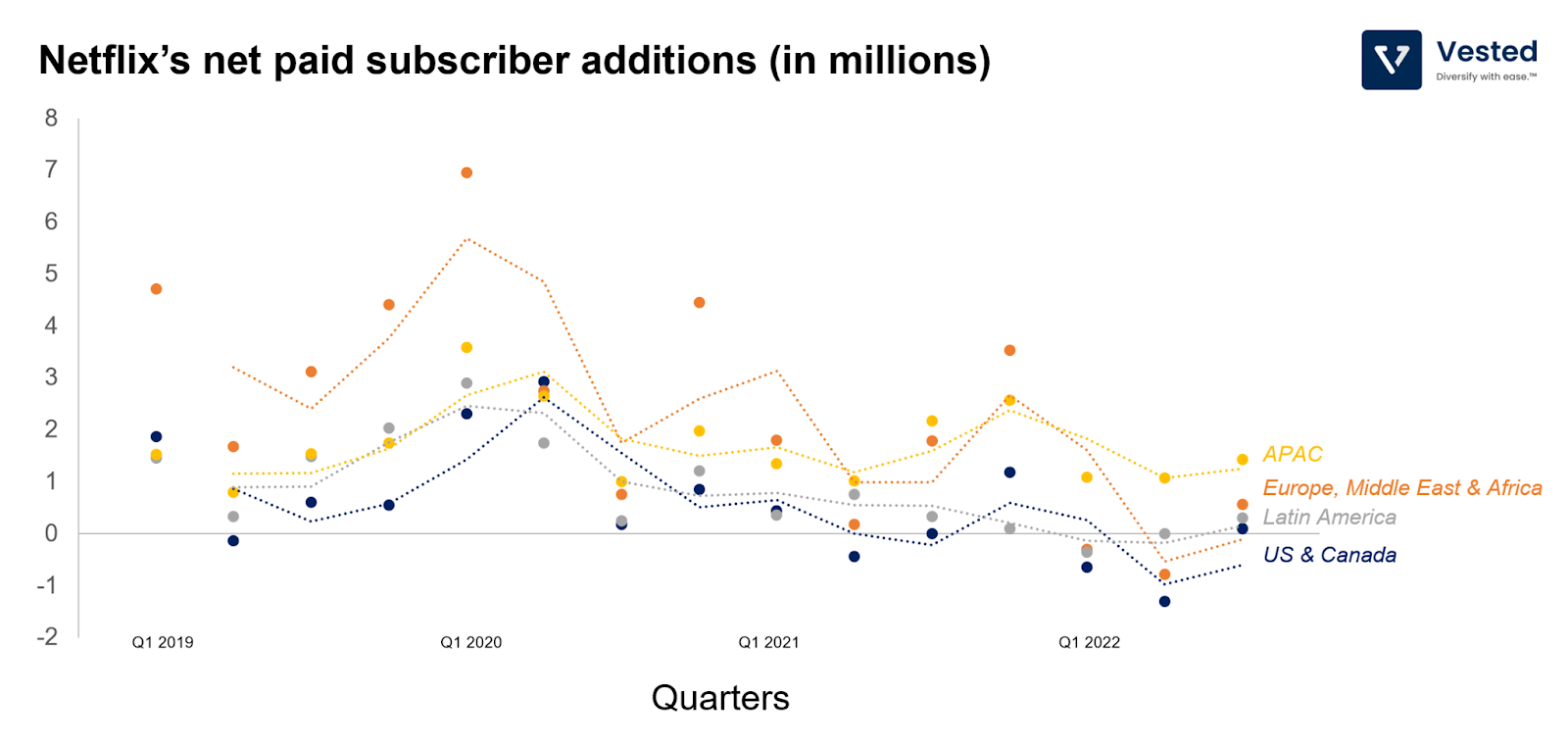

As a result of these two factors, the overall growth rate is stagnating (with US & Canada contracting). Figure 1 below shows the trend of the net paid subscribers from the past 15 quarters.

More ways to make money

So rather than pursuing a singular strategy of revenue growth via paid subscription growth, Netflix is shifting its strategy. In the near future, there are two additional ways Netflix can monetize its users:

- Through a new ad-supported plan, the company will be charging $7 per month. This new plan will first be available in the North American market, and then in France, Germany, Japan, Korea, Australia, and the UK (starting with developed countries).

- Through paid sharing, where any paying subscribers can pay for other users in another household. Account sharing is a very common practice. Netflix estimates that the service is being shared by an additional 100 million households (or about 45% of current total paying subscriber base), including 30 million in Canada and the US, the market with the higher average revenue). This feature won’t be released until 2023.

In a way, this is similar to a move Apple made in 2018, where, after more than a decade of growth, Apple stopped sharing iPhone sales figures on a quarterly basis. The company wanted to shift its focus to increasing the monetization rate of iPhone owners (through services and peripherals).

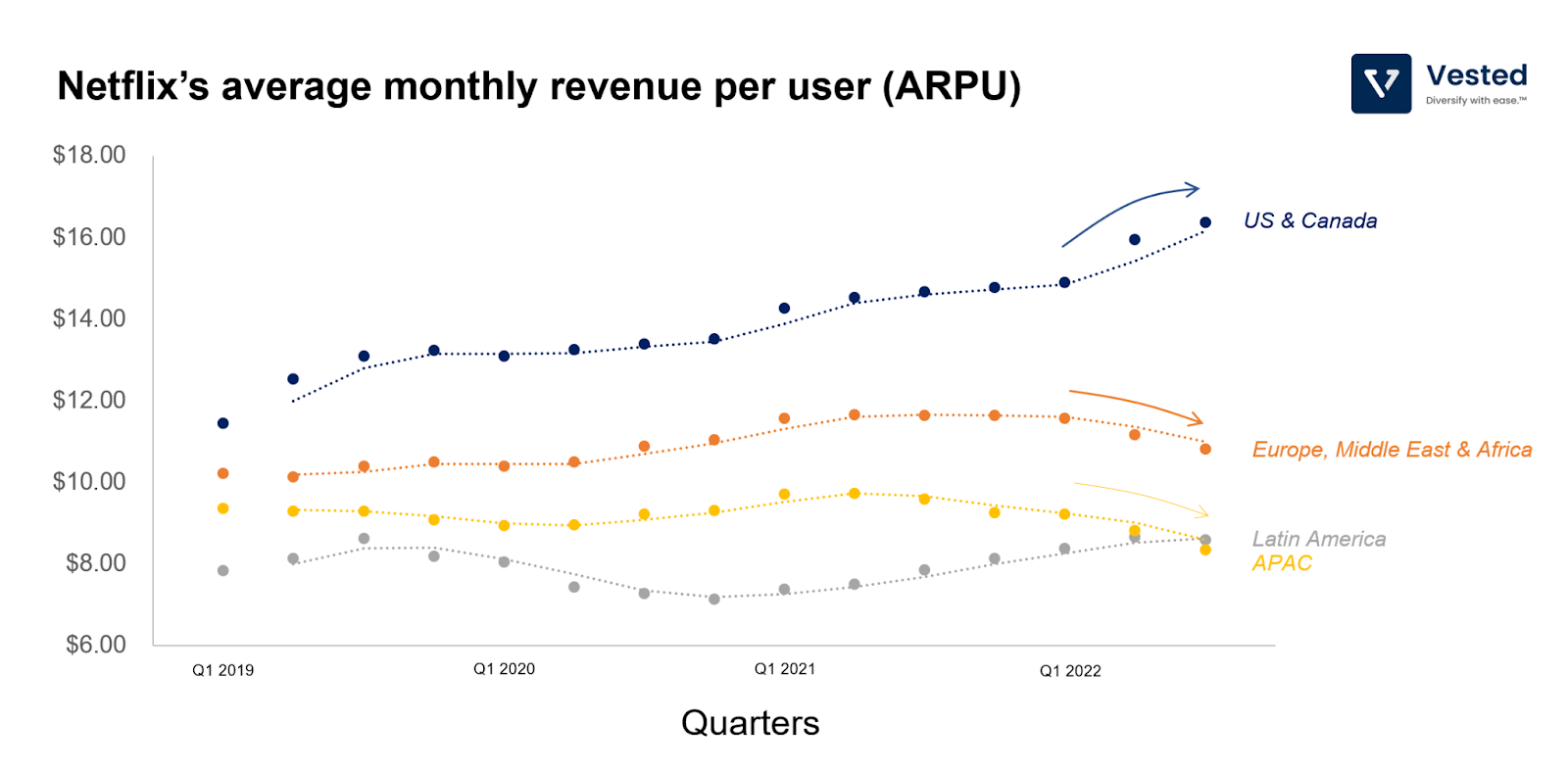

Now that Netflix has additional methods of generating revenue on a per-user basis, it will focus its reporting on revenue, operating margins, net income, and total members. It makes sense that we shift our analysis from paying subscribers to average revenue per user (ARPU). See Figure 2 below for Netflix’s ARPU trend from the past 15 months.

Key takeaways from Figure 2:

- The dispersion of ARPU between the different regions has been increasing these past 3 years. In Q1 2019, the US & Canada region’s ARPU was $11.45 per user, and the Latin America region was $7.84 per user. In Q3 2022, the ARPU for US & Canada has gone up to $16.37 per user (a 43% increase!), while ARPU for Latin America has only increased ~9% per user.

- To be fair, the decline in ARPU in the past 3 quarters for all the other non-US regions, is due to FX headwinds. The US dollar has strengthened against most other currencies in the past year. This poses a revenue challenge for most US multinationals.

- For US & Canada, the ARPU increase in the first 3 quarters of 2022 is due to higher prices. Netflix has been flexing its pricing power in these two countries in the past few years, and with the recent price hike and heightened competition, it might be hitting a limit on users’ tolerance for price. Hence, the additional ad-tier plan.

- The APAC region is supposed to be the region with the highest growth potential, but Netflix is hitting a price sensitivity wall there too. Overall, even if you exclude the impact of a stronger dollar, the ARPU of APAC declined by -3% in the past year. This is due to lower ARPU in India (Netflix lowered its prices in India in December 2021).

It is difficult to predict the impact of these two new revenue drivers for Netflix as we do not know the price sensitivity curve of Netflix’s customers in different regions. The company tends to increase and decrease prices in different countries simultaneously, and only reports the subscriber count on the region level (as opposed to the country level). For example, when Netflix lowered prices in India, the APAC region saw a 23% increase in subscriber growth. But the APAC region also comprises Australia, South Korea (two countries that experienced price hikes 2021), Japan, and other countries in Southeast Asia.

Nevertheless, the ad-supported plan likely will positively impact revenue in all markets, but specifically in the APAC region where the users are most price sensitive. One estimate predicts that Netflix can add $8 billion in incremental revenue by 2025 (which is roughly 26% of this year’s annual revenue).