Skip to content

Skip to content

Vested Solar is a first-of-its-kind product that allows you to create your own power plant. It allows you to own electricity generating assets i.e. a solar panel and to sell electricity generated by that asset to generate monthly income.

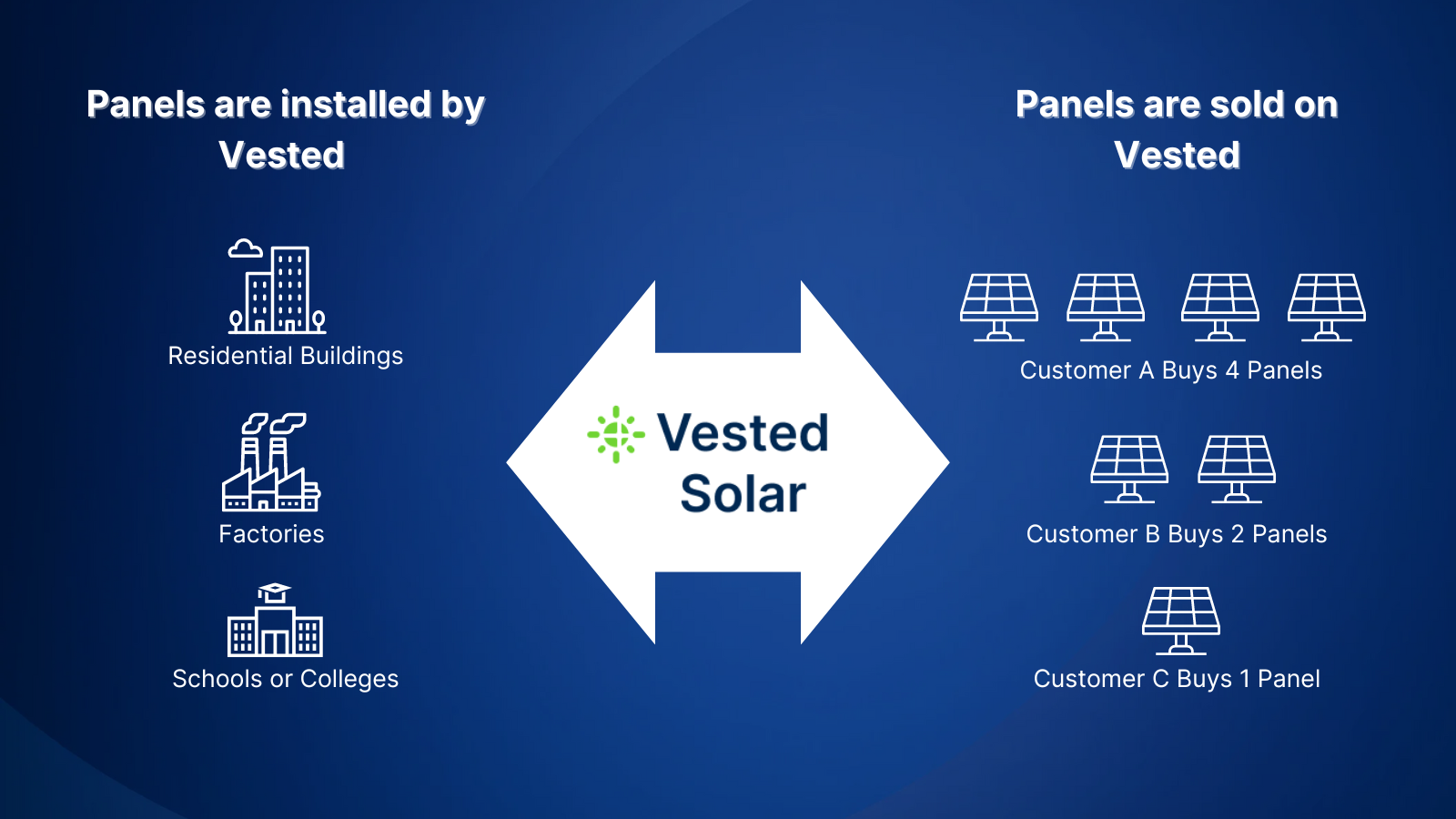

Before we get into the financial aspects, a quick look at how the Vested Solar model works. The product is essentially a marketplace that connects electricity consumers with panel owners like you.

On one end, Vested sources electricity consumers like schools, residential buildings, factories, etc. that want to move to renewable energy and reduce their electricity bill. On the other end, we have panel owners who purchase a panel on Vested, lease it to Vested to install on the consumer’s rooftop and earn an income from the electricity generated.

Next let’s understand a couple of key aspects related to the income your solar panels generate.

Income generation from solar panels

1. What influences your income

First and foremost, income is directly linked to the electricity generated by the solar panel. The amount of electricity generated varies depending on:

- Location of the panels

- Month of the year

- Cleanliness of the panel surface

- Age of the panel

It is important to ensure that there is no shadow falling on the panels at any point during the day.

We work with engineering partners who help design the solar plant in the best optimal manner and also provide estimates of the monthly generation. Based on the estimates, we determine the price of each installed panel such that panel owners can make at least 11-12% IRR on their purchase across the entire lifespan of the project. In the initial years, since the panel is new IRR is in fact higher.

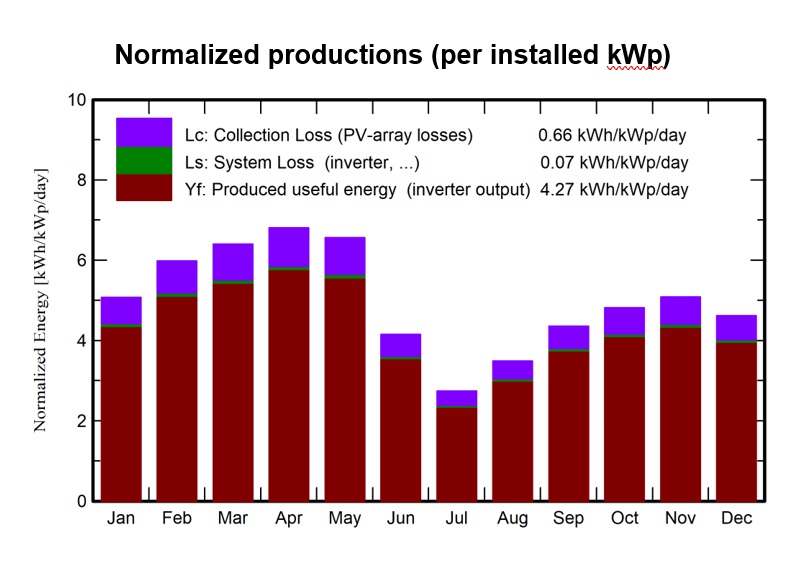

Example monthly generation based on Vested’s Radhey Heritage project

2. Recovering your upfront purchase cost

One of the key aspects you may want to understand before purchasing panels is how your upfront purchase cost is returned and the income you make beyond the upfront cost.

There are two ways you can look at the return of your cost:

- Loan structure

- You can think of your purchase cost as a loan to the power purchaser at an interest rate of 12%

- Every month, the power purchaser returns some of your original amount + your interest

- Eventually as is in the case of loan EMIs, more and more of your principal keeps getting returned with each payment

- Click here to see in an excel how principal + return payouts would work for a 15 year project

- Principal first then return

- The other way to think about your upfront cost is that all the initial income goes towards recovery of your principal

- Once the principal is recovered, which is typically 5-7 years in a solar project, then the rest is purely profit

The most important aspect of both of these models is that you get regular monthly cash-in-hand which can be used or re-deployed (more on this in the next section). This makes owning a solar panel different from any fixed maturity investment options like fixed deposits.

Ok, now onto how you can make the most of your solar-generated income.

Making the most of your solar-linked income

The beauty of owning your solar panel is that it gives you monthly cash flows that you can utilize in two different ways:

1. For monthly expenses

One way to utilize the funds is to meet any regular expenses you may have.

Panels worth 10L at an IRR of 12% for a 15 year project, would earn an income of ~INR 1.45L per year. As we saw above, this includes both your principal + your returns.

In the case of solar, this income will be higher in the earlier years because the electricity generation is higher in the beginning and reduces as the panel becomes older.

2. To boost the returns of other investments

Another way you can utilize your monthly solar income is by reinvesting solar income into other asset classes. For those that are familiar with the concept of an STP or Systematic Transfer Plan, this works exactly like that.

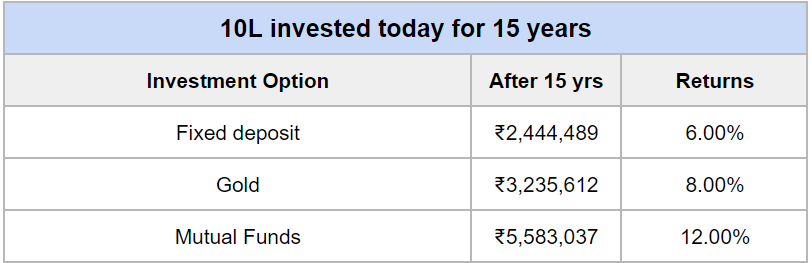

If you keep systematically transferring your solar income into an FD or Gold or Mutual Funds, you can effectively boost the returns from these underlying assets. Apart from the return boost, it helps convert a lump sum investment into a consistent monthly investment so you avoid timing risk in assets like Gold or Mutual Funds.

Here is a simple snapshot of how your returns in each of the underlying assets (FD, Gold or Mutual Fund) would be improved:

In conclusion, via Vested Solar, you not only have the option to contribute to a greener Earth, but you can also benefit financially from the monthly income by either paying your expenses or reinvesting it into other return-generating assets and boosting your returns.