Skip to content

Skip to content

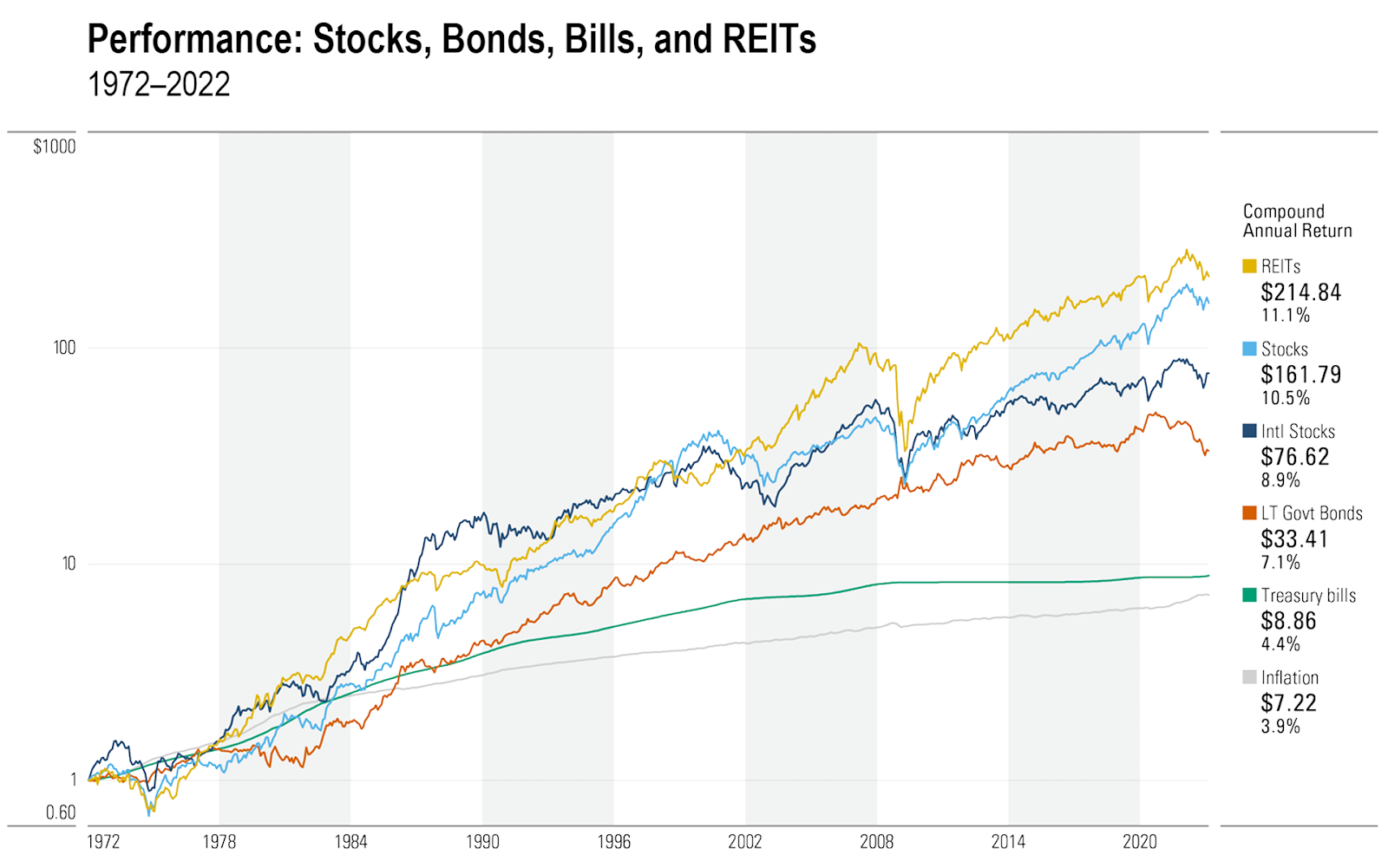

Investing in real estate has long been recognized as an effective hedge against inflation, outperforming other asset classes in 6 out of 7 inflationary periods (see Figure 1). During periods of high inflation and economic growth, real estate valuations have adjusted due to increased demand and supply shortages. Landlords can capitalize on these conditions by adjusting rental contracts through annual price hikes and generating growth through acquisitions and developments. However, the current situation is different for a number of reasons (COVID-19, interest rate hikes, war in Ukraine). In this article, we will delve into the current state of commercial real estate in the US.

Figure 1: Hypothetical investment of $1. Note that the Y-axis is in log-scale. Source

Early signals from private markets

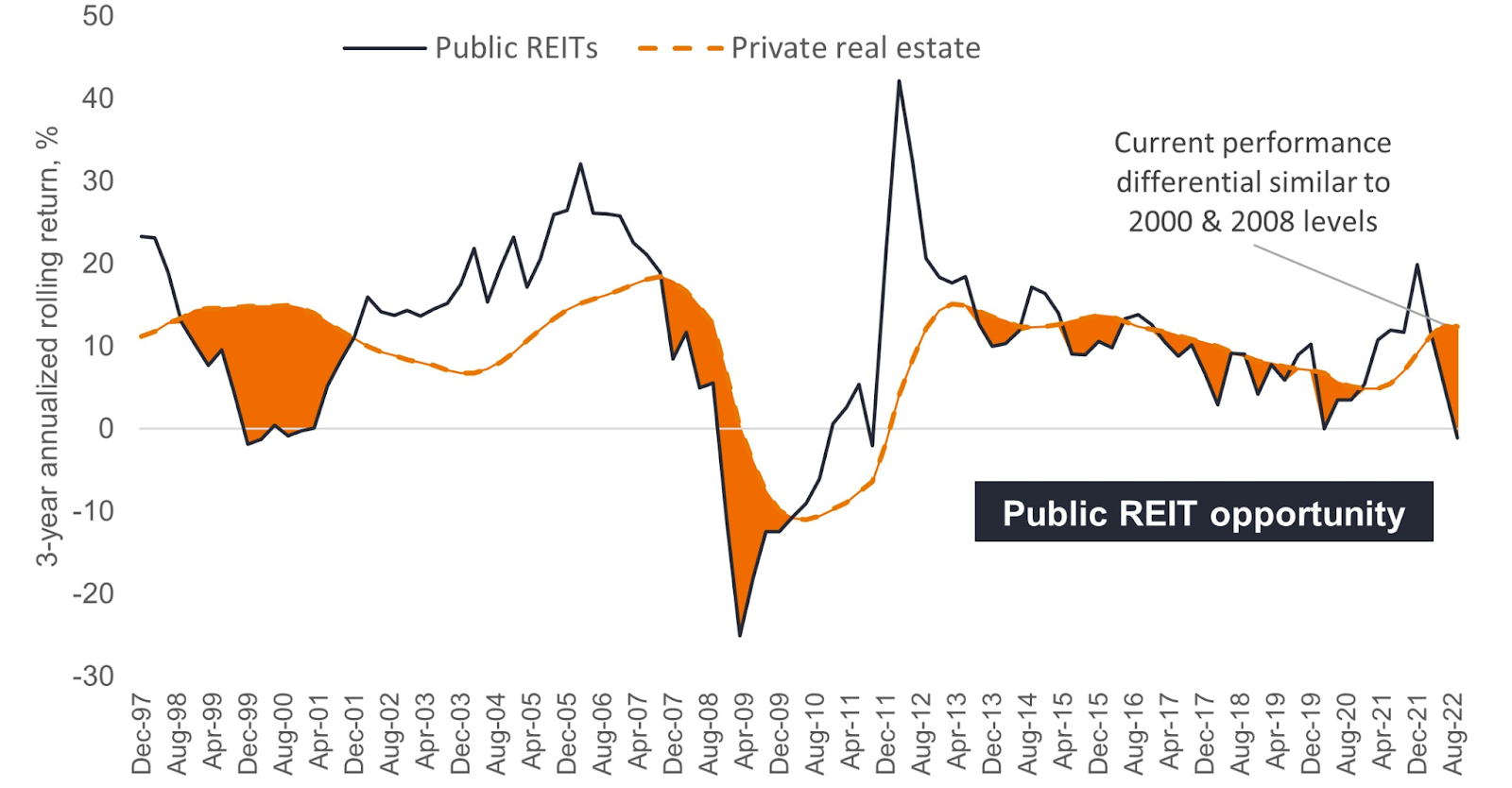

You can invest in commercial real estate either through public means or private. Investing in publicly listed Real Estate Investment Trusts (REITs) is done through the stock market and is, therefore, the most liquid form of real estate investment. On the other hand, private REITs are only available to accredited investors with a $1 million net worth. Therefore, private real estate, in general, is much less volatile compared to its public counterparts. This discrepancy can be explained by one of two reasons.

- Efficient Market Hypothesis: According to this theory, the stock market incorporates all relevant information through fast price discovery. Consequently, private markets are unable to price in all relevant factors in real-time and therefore lag behind their public counterparts.

- Noisy Market Hypothesis: This theory argues that stock markets are heavily influenced by speculation and irrational biases and, therefore, do not represent the actual underlying value of a company. According to this theory, stock prices result from the public’s ignorance, whereas experts with industry knowledge control private market prices.

Figure 2: Returns from private real estate are outperforming public ones. Source

Regardless of which theory you believe to be true, this divergence of prices is not permanent. Fundamentally both markets hold the same type of assets, and their prices tend to converge over time. Therefore, the present gap is expected to be reduced through corrections in both the private and public markets, as it has done before in 2000 and 2008 (see Figure 2). Despite the short-term fluctuations, long-term returns from public real estate have outperformed private ones by 1.7%. This presents an opportunity for real estate investors if the current market has undervalued public real estate assets.

Commercial Real Estate is in a slump

The US commercial real estate (CRE) sector is currently facing a crisis. According to MSCI, commercial real estate prices declined in the first quarter of 2023 for the first time in 11 years (see Figure 3 below). About $1.5 trillion in CRE mortgages will mature in the next three years, and based on current interest rates, property income, and values, 35% of them are expected to default. This may force landlords to sell their properties, exacerbating the decline in their value. Moreover, regional banks with high exposure to the sector may have to devalue their commercial loans and allocate additional funds for potential losses.

Figure 3: Prices of all real estate property types are decreasing. Source

Several sector-wide factors contribute to the decline in prices:

Slow rent growth

While historically, rents tend to grow faster during inflation; it does not grow fast enough to keep on par with inflation, and real rent growth declines. During past inflationary periods, rent increased at an annualized rate of 3% while inflation was at 5%. Currently, the median asking rent has reached its lowest level in 13 months. However, certain property sectors are able to grow rent faster than others.

- Rents from office and retail real estate grow slower due to their longer lease terms. In large metropolitan areas like San Francisco and Manhattan, rent growth has slowed by 30.8% and 13.6%, respectively.

- In contrast, apartments and industrial buildings have seen rent growth in the first quarter of 2023 due to persistent demand. Multifamily apartment rent is expected to grow at a moderate level of 2.5%, while industrial rent growth was 6.9% year-over-year in February.

High vacancy rates

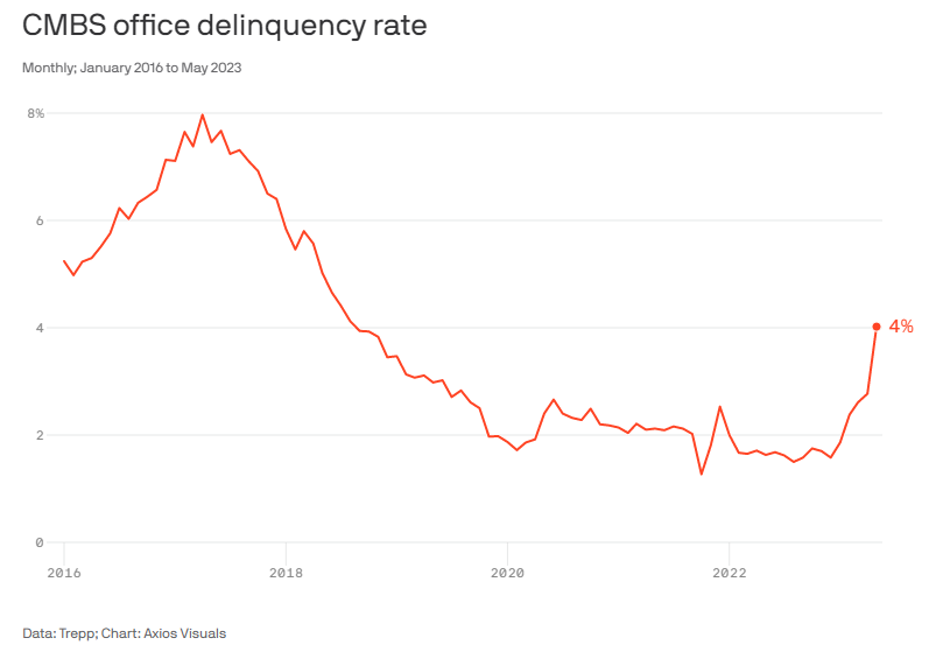

Remote work and changing consumer behavior have resulted in a record-low occupancy rate of 12.9% for office spaces nationwide. This has left many office spaces empty and led to struggles for retail businesses, significantly impacting the income and value of these properties. Consequently, a number of office real estate owners defaulted on their property loans. In May, the delinquency rate for office loans shot up by 125 basis points (see Figure 4 below).

Figure 4: More offices are defaulting on their loans. Source

Higher cost of debt

The consecutive interest rate hikes by the central bank made real estate debts more expensive. High mortgage rates have become an obstacle for first-time buyers and middle-income families looking to relocate. In 2022, the 30-year mortgage rate reached a 20-year peak, dissuading property owners from selling their properties with low mortgage rates or borrowing at high-interest rates to acquire new ones. However, the demand for additional space has increased as more young adults move back with their families and work from home. This is forcing would-be buyers back into the rental market and has increased the asking rent for apartments by $17 (just below 1%).

The resilience of REITs

Despite the challenging market conditions, REITs have demonstrated resilience by divesting in low-return sectors and investing in more profitable ones. The most affected sectors in the current macroeconomic environment are offices and retail properties, particularly malls. These two sectors have historically dominated REIT allocations, with significant investments over the past decade. In December 2013, malls and offices comprised more than a quarter of the market capitalization-weighted FTSE NAREIT All REITs Index. However, there have been significant shifts in the composition of REITs in recent years.

Figure 5: REITs have changed their composition. Source

Recently the composition of REITs has changed with the emergence of specialized industrial property types such as cell towers, data centers, and gaming. These properties are essential for the modern economy, enabling wireless communication, cloud computing, data storage, and e-commerce. While these sectors accounted for only 14% of the FTSE NAREIT All REITs Index in 2013, their weightings have significantly increased since then. In Figure 5, we can see the index’s weighting to towers has grown by almost 10% from March 2013 to March 2023, while the weightings to industrial and data centers have both increased by more than 6%. In contrast, the weighting to malls has dropped by more than 10%, and office has fallen by almost 9%.

In conclusion, although the CRE market currently faces challenges, there are opportunities for investors and stakeholders to navigate this period. The convergence of private and public real estate markets, the potential undervaluation of public real estate assets, and the adaptability of REITs to changing market dynamics all present avenues for potential growth. Historical data indicates that REITs often underperform just before recessions but rebound shortly after. Following the 2008 financial crisis, REITs nearly tripled in value within two years. According to the Bank of America, REITs specializing in the data center, lodging, and healthcare sectors are poised to outperform private markets this year.