Skip to content

Skip to content

As the U.S. presidential election approaches on November 5, market watchers are bracing for the usual bout of political uncertainty. Historically, these events bring short-term market jitters, but they rarely disrupt the long-term trajectory of stocks. In fact, election cycles tend to generate less upheaval than expected, with markets generally regaining stability post-results.

In this article, we’ll examine three main areas where shifts in U.S. administration policies could affect the market: trade tariffs, tax policies, and sector-specific outlooks. We’ll also look into the market’s historical behavior around elections, dismantle a few election-year myths, and consider how other factors—like Federal Reserve policy—often play a more decisive role in market movements than election results alone.

The Election-Year Market: Resilient Despite the Rhetoric

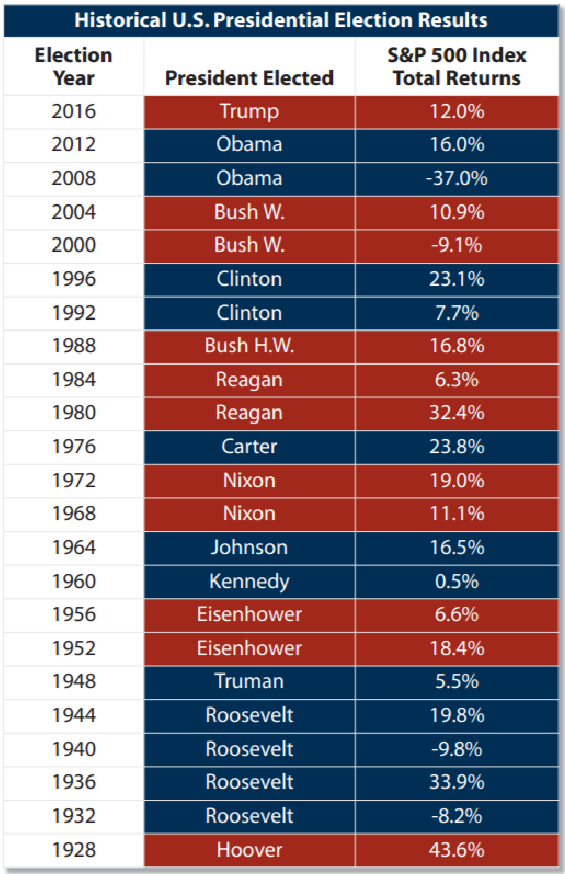

Despite the heightened focus on elections, the U.S. stock market has historically demonstrated resilience. As per a research by JP Morgan, the election years are generally favorable for U.S. stocks. Since 1932, the S&P 500 has posted gains in 74% of election years, with an average annual return of 6.2%—only slightly lower than the 8.7% average return across all years since 1932. But these numbers don’t capture every election year’s unique context. For instance, in 2000 and 2008, markets faltered due to the dotcom bubble burst and the global financial crisis, not election-related issues.

Market volatility does tend to increase somewhat in election years, with average volatility at 16.5% compared to 15.3% in non-election years. However, removing outliers like 2000 and 2008 reveals a much smaller difference. This suggests that, while volatility may heighten as election results approach, markets typically stabilize after the outcome is clear. For instance, election years since 1936 show median returns rising from 1.9% in the first three quarters to 3.1% in the fourth quarter, reflecting a pattern of regained stability.

Source: JPMorgan

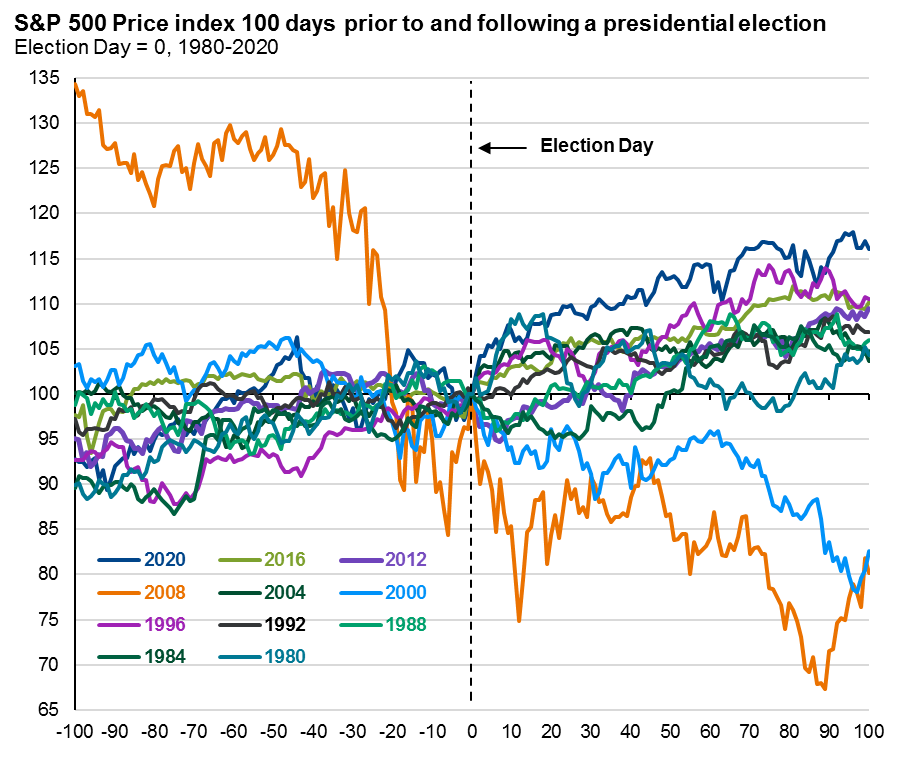

In the case of delayed results, such as with potential recounts or increased mail-in ballots, short-term market volatility may spike. However, history shows that once the outcome is resolved, markets generally revert to a stable course. The 2016 and 2020 elections, for instance, saw a pre-election rally followed by gains once results were finalized, underscoring the resilience that investors often overlook amid the election fervor.

Source: Morgan Stanley

Policy Areas to Watch: Trade, Taxes, and Sector Effects

While elections rarely shift the market’s long-term direction, certain policy areas can trigger short-term impacts, especially if an administration enacts significant changes. Here’s where the current race could have an influence.

Trade Tariffs: Potential Shifts in Import Costs

Trade policies directly influence market dynamics, especially during presidential transitions. Trump’s re-election campaign has proposed aggressive trade measures, including a sweeping 10% tariff on all U.S. imports and potential tariffs of up to 60% on Chinese goods. These proposals could drive up consumer prices and squeeze profit margins for companies that rely heavily on imports.

Currency markets react swiftly to trade policy shifts. The U.S. dollar strengthened notably after Trump’s 2016 victory as investors anticipated stricter trade measures. Yet global markets typically adapt to new trade policies over time, moderating these initial currency movements.

The current Biden administration has maintained and even expanded many Trump-era tariffs, marking a significant shift from traditional free trade approaches. This continuity in trade policy highlights how both parties now favor more protective trade measures, particularly regarding China.

Looking forward, both candidates’ economic plans emphasize fiscal stimulus, though through different mechanisms. Trump focuses on expanding tax incentives, while Biden prioritizes targeted government spending. The treatment of Chinese imports remains a key point of divergence, with each candidate proposing distinct approaches to U.S.-China trade relations. These policy differences could create significant market movements as investors adjust their positions based on election outcomes and subsequent policy implementations.

Tax Policies: Contrasting Approaches

Tax policy remains a core focus in the current race.A central focus here is the future of the Tax Cuts and Jobs Act (TCJA) from 2017, a signature domestic policy of the Trump administration. The TCJA introduced a broad array of tax cuts, set to expire at the end of 2025, sparking discussions on whether to extend, modify, or allow these provisions to lapse.

If the provisions are extended, as proposed by Trump, tax rates would remain lower, benefiting both individuals and corporations but potentially escalating federal deficit concerns due to decreased tax revenue

Should the TCJA provisions not be extended, tax rates could rise for nearly 60% of filers, alongside reductions in the standard deduction, child tax credits, and higher estate and gift tax thresholds. Corporations, in particular, would face a sharp increase, with the top corporate tax rate reverting from 21% to 35%. President Biden has expressed support for extending tax breaks for those earning $400,000 or less, while letting provisions for higher-income earners expire. His approach also includes raising corporate tax rates and implementing a global minimum tax. Currently, Vice President Harris has yet to specify if she supports this approach, though she and Trump have both backed eliminating taxes on tips for service and hospitality workers. Additionally, Trump has proposed reducing the corporate tax rate further to 20%.The tax policies would have an effect on the future earnings of the companies.

Sector Performance: Temporary Swings with Policy Priorities

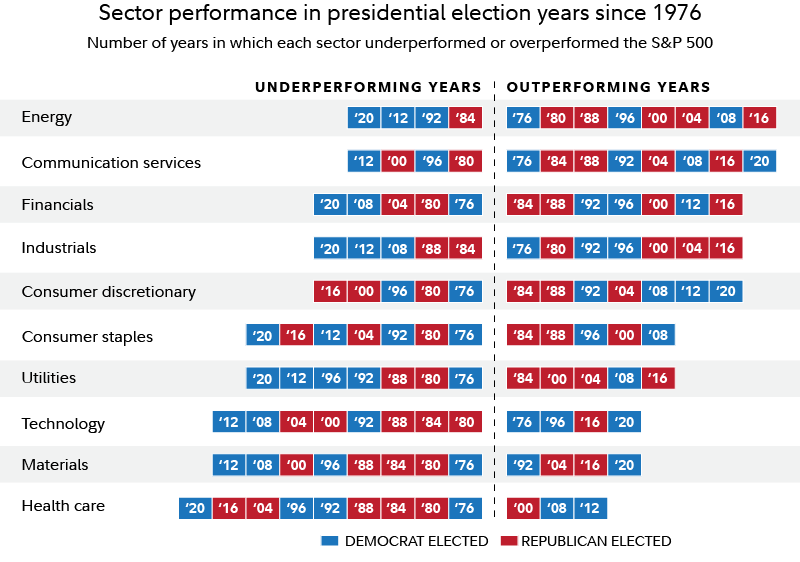

Election outcomes can lead to short-term fluctuations in specific sectors, influenced by the priorities of the newly elected administration. Typically, Republican administrations tend to favor sectors such as aerospace, defense, and financial services, whereas Democratic administrations are more inclined to support healthcare and renewable energy initiatives. However, the effectiveness of these policies often hinges on Congressional support, particularly in a divided government. For instance, while the Biden administration advocates for advancements in clean energy, the realization of those goals requires legislative backing to turn policy proposals into action.

Predicting which sectors will benefit from election results can be a challenging task. While it’s possible to anticipate potential policy impacts at a broad level, accurately forecasting which sectors, industries, or stocks may gain from the next administration’s policies is fraught with uncertainty. As noted by industry experts, “There are very few consistent patterns of relative sector returns in election years.”

This unpredictability is supported by historical data on sector performance. Past performance does not guarantee future results. Each box in this analysis represents one calendar year of performance during a year that included a U.S. presidential election. “Underperforming” indicates that a sector’s price performance lagged behind that of the S&P 500, while “outperforming” signifies that it exceeded the index’s performance. The color of each box denotes whether a Democrat or Republican candidate was elected president in that year.Each sector’s performance is represented by companies within the S&P 500 that belong to that sector.

Source: Fidelity

Federal Reserve Policy and Elections

It’s a common misconception that election results dictate market movements. However, market movements depend more on interest rate and economic scenario.

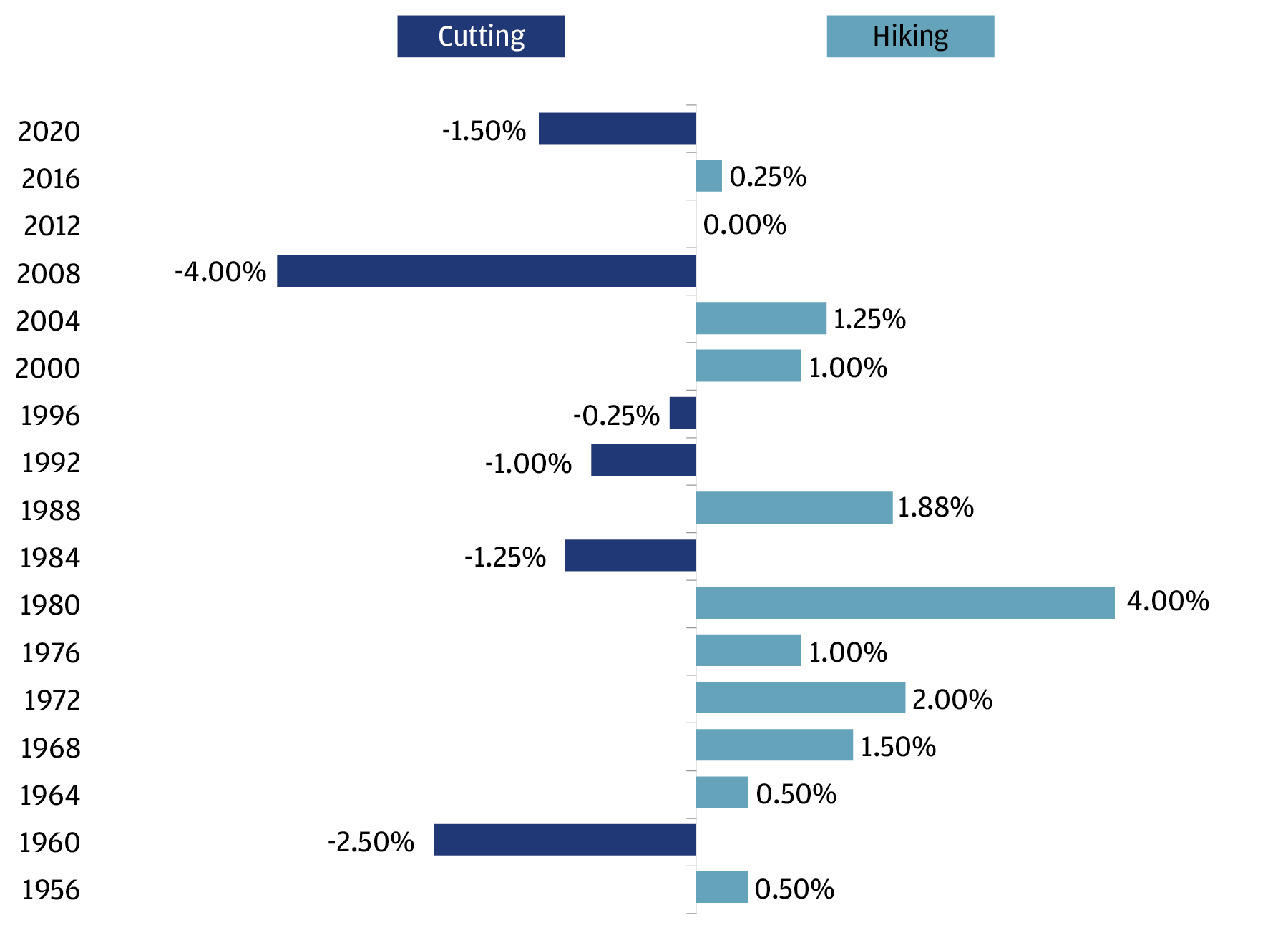

The upcoming Fed meeting would be a key event for the US economy. Historically, the Fed does not shy away from making significant policy changes during election years. While there has been some reluctance to adjust interest rates in the two months leading up to a November presidential election, policymakers generally pursue their agendas throughout the rest of the year. Since 1956, the Fed has raised or lowered interest rates in every election year except one—2012.

Source: JP Morgan

Currently, the Fed’s focus is on achieving a soft landing for the economy—managing growth without triggering a recession. This delicate balancing act becomes even more critical as they contemplate rate cuts. The challenge lies in ensuring that inflation continues to moderate while fostering economic growth. In 2024, for instance, the Fed must navigate these complexities, and its decisions regarding interest rates will likely have a more profound effect on the markets than the outcomes of the elections themselves.

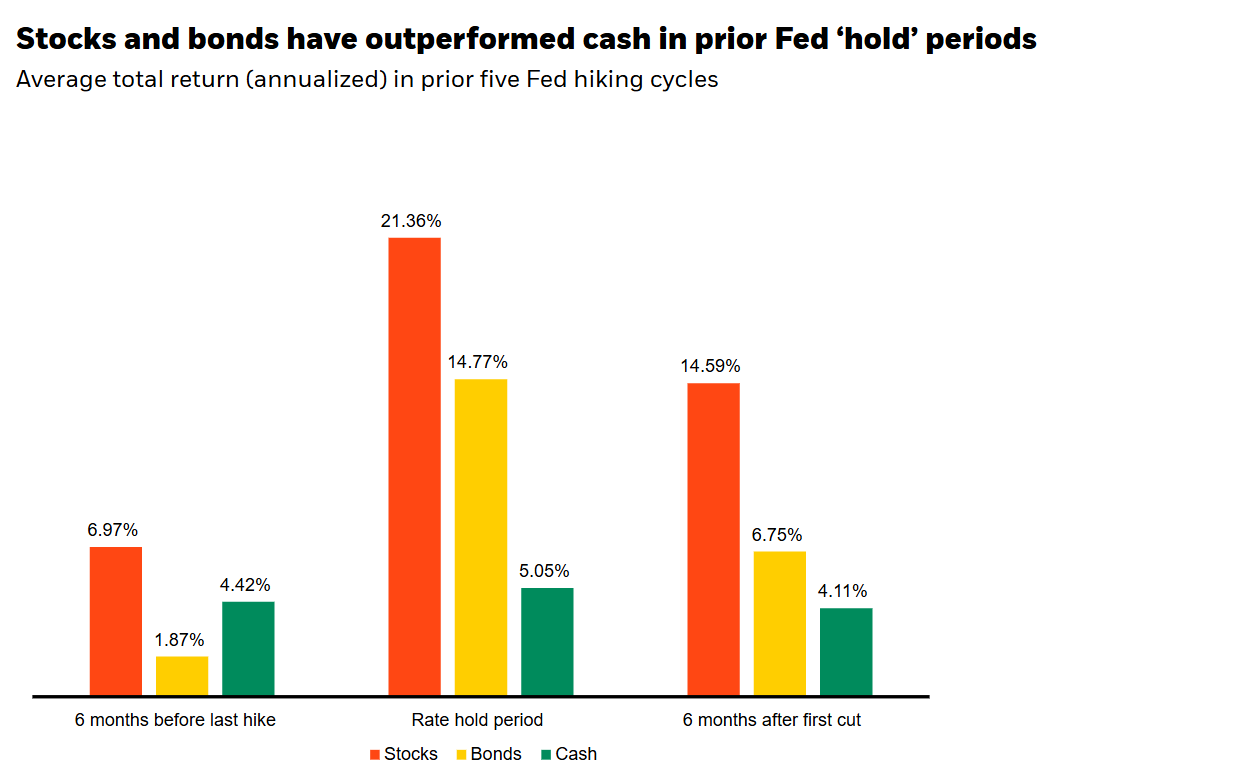

Historical Performance Trends

Historical trends reveal that both bonds and stocks tend to perform well during periods when the Fed pauses rate hikes prior to initiating cuts. This underscores the importance of understanding Fed policy cycles as a crucial element of a strategic, long-term investment approach, often more so than election cycles.

Source: Bloomberg

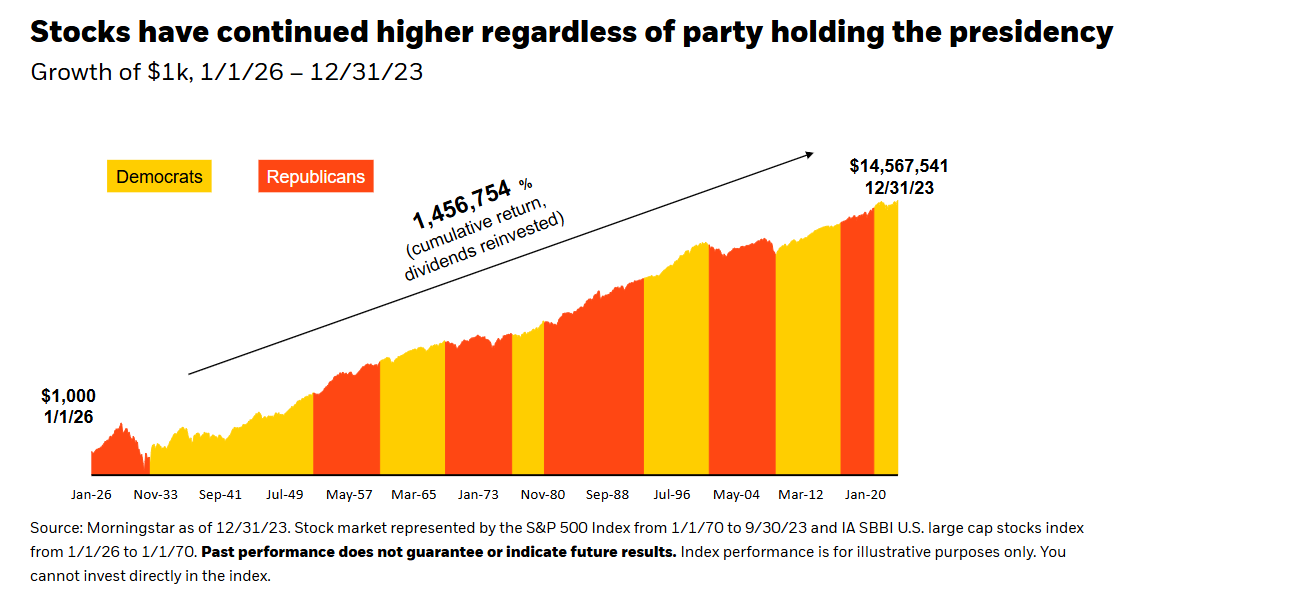

As per Bloomberg, Since 1926, despite the shifting political landscape, the S&P 500 has delivered staggering cumulative returns of 1,456,754%. This performance showcases that stocks have consistently risen regardless of which party occupies the presidency.

Source: Bloomberg

The Importance of Staying Invested

The market’s indifference to political parties is also apparent over shorter timeframes. Investors who maintained their investments outperformed those who only invested when their preferred party was in power. This reinforces the idea that aligning investment strategies with political beliefs often leads to underperformance compared to a long-term focus on market fundamentals.

The Bottom Line: Focus on Long-Term Fundamentals

As November approaches, while elections may create some short-term market volatility, the broader focus will inevitably shift back to inflation, interest rates, and global economic trends. These factors play a much more substantial role in shaping market dynamics than any political transition.

In conclusion, while the upcoming election may introduce fluctuations, anchoring your investment strategy in long-term fundamentals is crucial. The markets have successfully weathered numerous election cycles, and investors who concentrate on economic indicators rather than short-term political changes are often in a better position to navigate the complexities of the market.

Disclaimer: This article draws from sources such as Financial Times, Bloomberg,and other reputed media houses. Please note, this blog post is intended for general educational purposes only and does not serve as an offer, recommendation, or solicitation to buy or sell any securities. It may contain forward-looking statements, and actual outcomes can vary due to numerous factors. Past performance of any security does not guarantee future results.This blog is for informational purposes only. Neither the information contained herein, nor any opinion expressed, should be construed or deemed to be construed as solicitation or as offering advice for the purposes of the purchase or sale of any security, investment, or derivatives.The information and opinions contained in the report were considered by VF Securities, Inc.to be valid when published. Any person placing reliance on the blog does so entirely at his or her own risk, and does not accept any liability as a result.Securities markets may be subject to rapid and unexpected price movements, and past performance is not necessarily an indication of future performance. Investors must undertake independent analysis with their own legal, tax, and financial advisors and reach their own conclusions regarding investment in securities markets.