Skip to content

Skip to content

The Story

When Mark Zuckerberg talks about “superintelligence being in sight,” you know something big is happening. This week, both Meta and Microsoft dropped their quarterly earnings, and the results were nothing short of spectacular. But buried beneath the headline-grabbing revenue beats and stock price surges lies a more intriguing story about the future of technology itself.

Both companies are essentially rewriting the rules of corporate spending, pouring unprecedented amounts of money into artificial intelligence infrastructure. The question isn’t whether AI will transform business — it’s whether these massive bets will actually pay off.

The Numbers Don’t Lie

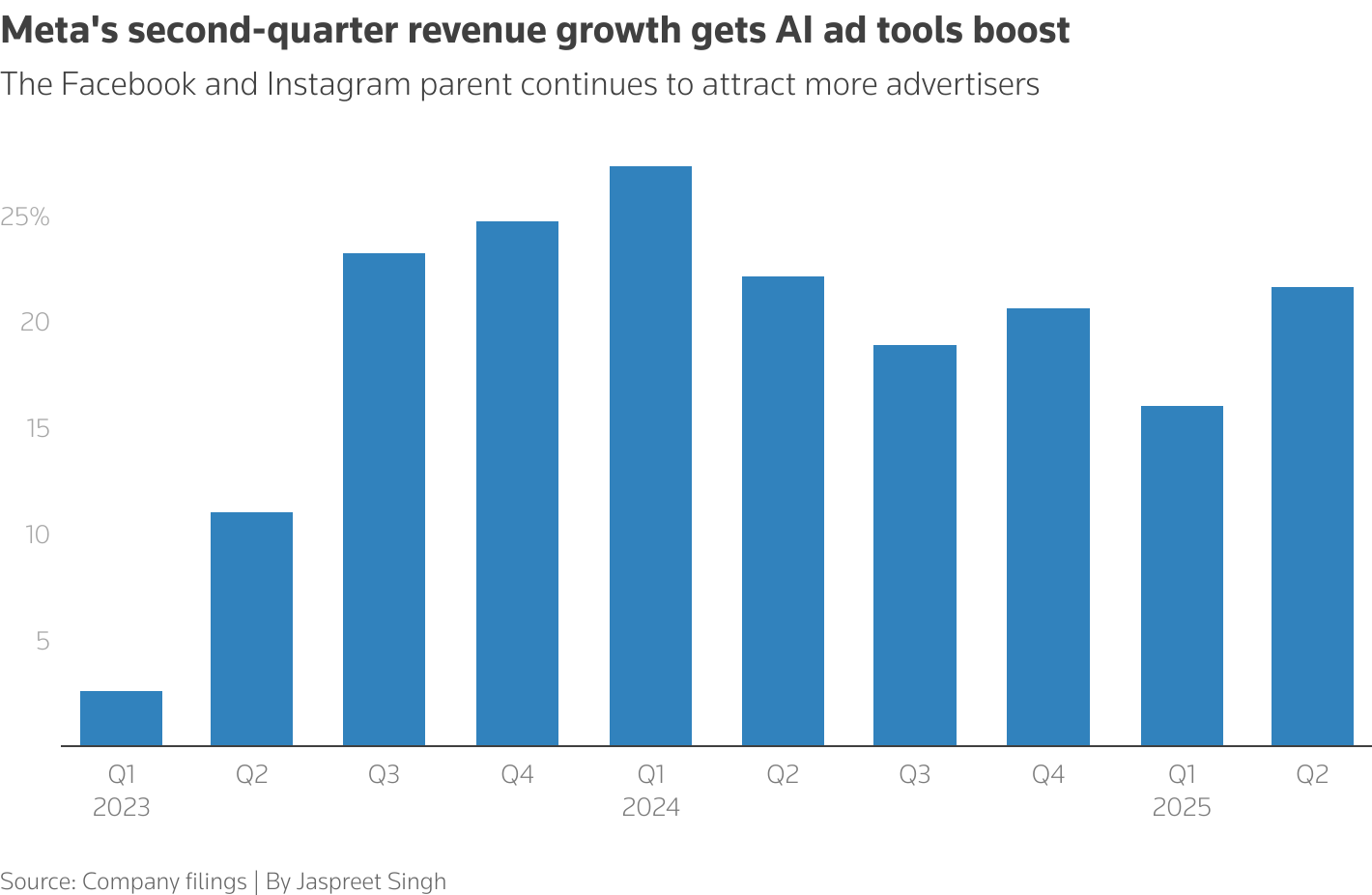

Let’s start with Meta, the company that owns Facebook, Instagram, and WhatsApp. When they announced their second-quarter results, investors nearly fell off their chairs:

Meta’s Blockbuster Quarter:

- Revenue: $47.52 billion (vs. $44.80 billion expected)

- Earnings per share: $7.14 (vs. $5.92 expected)

- Revenue growth: 22% year-over-year

- Stock reaction: Jumped over 10% after hours

But here’s where it gets interesting. Meta didn’t just beat expectations — they obliterated them. Their advertising revenue alone hit $46.56 billion, crushing Wall Street’s projection of $43.97 billion. That’s like expecting someone to score 20 points in a basketball game and watching them drop 25 instead.

Microsoft wasn’t far behind with their own impressive show:

Microsoft’s Cloud Story:

- Revenue: $76.4 billion (vs. $73.89 billion expected)

- Adjusted EPS: $3.65 (vs. $3.37 expected)

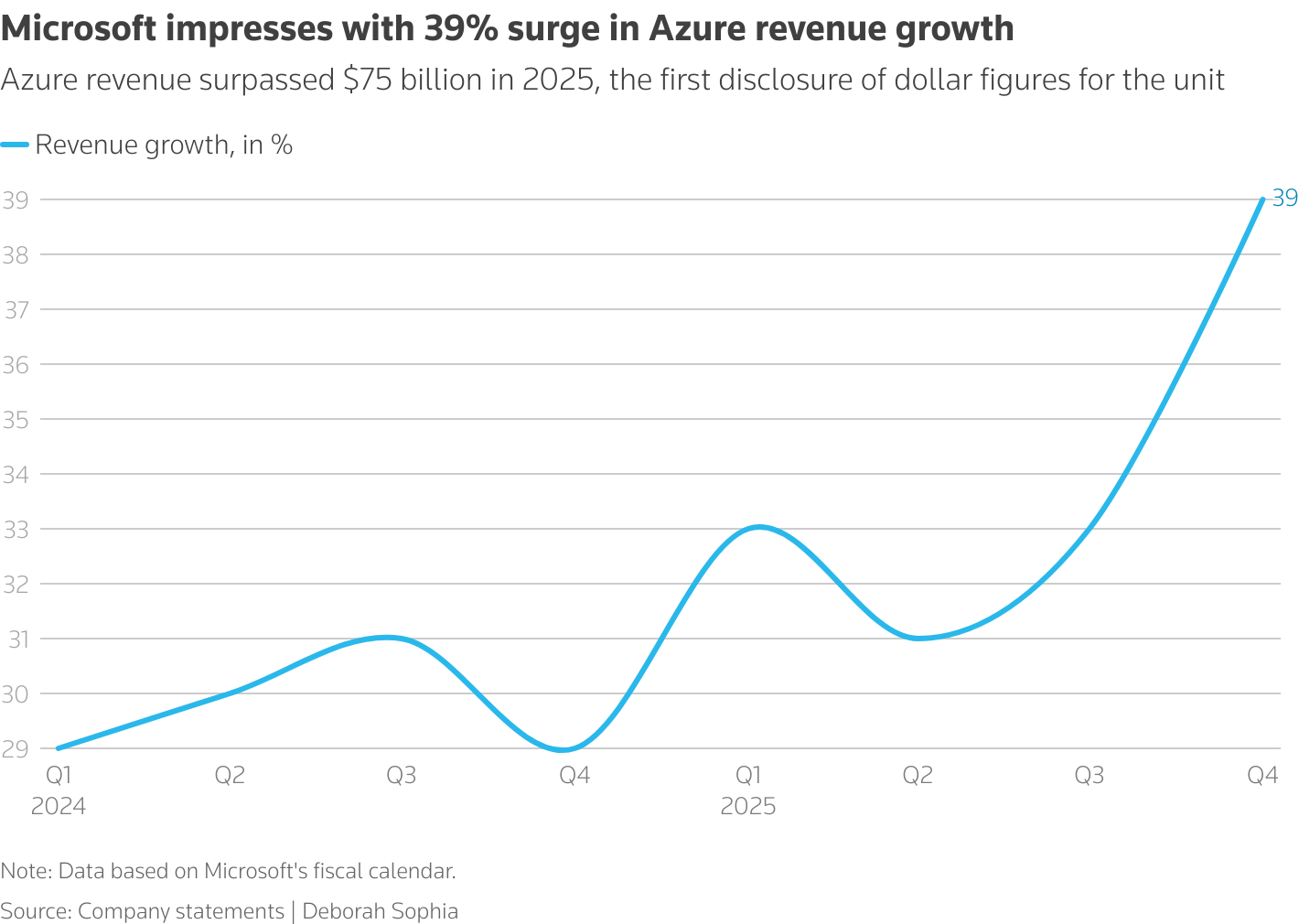

- Azure revenue: Surpassed $75 billion annually for the first time

- Azure growth: 39% (beating the 34.75% estimate)

The market’s response? Microsoft’s stock climbed over 6%, and combined with Meta’s gains, the two companies added a whopping $500 billion in market value in a single day.

The AI Investment Frenzy

Now, here’s where the story gets really juicy. Both companies are spending money on AI like there’s no tomorrow, but their approaches are fascinatingly different.

Meta’s AI Shopping Spree:

Mark Zuckerberg has turned into something of an AI talent scout. The company recently invested $14.3 billion in Scale AI and poached its 28-year-old billionaire CEO, Alexandr Wang. They’re also building massive data centers — one called “Hyperion” will eventually support 5 gigawatts of capacity. To put that in perspective, that’s enough power to run about 3.8 million homes.

Meta’s capital expenditure forecast for the year? Between $66-72 billion, with the company raising the lower end by $2 billion. CFO Susan Li warned investors that 2026 expense growth would exceed 2025 levels, primarily due to infrastructure costs and employee compensation.

Microsoft’s Record-Breaking Spend:

Microsoft announced plans for a record $30 billion in capital spending for just the current fiscal quarter. That’s more than many countries’ entire annual budgets. At this pace, Microsoft could spend roughly $120 billion on AI this fiscal year alone.

Amy Hood, Microsoft’s CFO, tried to reassure investors by saying, “I feel very good that the spend that we’re making is correlated to basically contracted, on-the-books business that we need to deliver.” Translation: We’re not just throwing money at the wall and hoping something sticks.

The Early Returns: A Deep Dive Into ROI

But here’s the million-dollar question (or should we say billion-dollar question): Are these massive investments actually paying off?

The answer appears to be a cautious yes, but the devil is in the details.

Meta’s AI Success Stories – The Math Behind the Magic:

Let’s break down what those AI-driven conversion improvements actually mean. A 5% increase in Instagram conversions and 3% on Facebook might sound modest, but when you’re dealing with Meta’s scale, these numbers are massive.

Meta’s advertising revenue hit $46.56 billion this quarter. If we assume AI improvements contributed even a fraction of the revenue beat (they exceeded expectations by $2.59 billion), we’re looking at AI potentially driving billions in additional revenue per quarter. That’s a return on investment that would make any CFO smile.

But here’s the more telling metric: Meta’s cost per result (the amount advertisers pay for each conversion) has been declining while conversion rates improve. This is the holy grail of advertising technology — better results for less money. It’s why Meta can confidently project Q3 revenue between $47.5-50.5 billion, well above Wall Street’s $46.14 billion estimate.

Microsoft’s AI Momentum – The Cloud Economics:

Microsoft’s story is even more fascinating from an economics standpoint. Azure’s 39% growth, while impressive, needs context. Cloud infrastructure typically has economies of scale — the more you build, the cheaper each additional unit becomes. But AI workloads flip this equation.

AI computing requires specialized chips (GPUs) that cost significantly more than traditional server hardware. Microsoft’s $30 billion quarterly capex forecast suggests they’re buying these expensive chips at unprecedented scale. Yet Azure growth is accelerating, not decelerating. This indicates that AI demand is so strong that customers are willing to pay premium prices.

Consider this: Microsoft’s Copilot tools reached 100 million monthly active users. If even a fraction of these convert to paid enterprise plans (which typically cost $30-60 per user per month), we’re looking at potential recurring revenue in the billions. That’s high-margin, sticky revenue that justifies massive upfront infrastructure investments.

The Strategic Chess Game: Why These Investments Make Sense

What makes this story even more intriguing is how these companies are positioning themselves differently in the AI race — and why their strategies reflect deeper understanding of market dynamics.

Meta’s Vertical Integration Play:

Meta’s $14.3 billion investment in Scale AI isn’t just about access to data annotation services. It’s about controlling the entire AI pipeline. Scale AI specializes in training data preparation — the often overlooked but crucial step in AI development. By bringing this in-house, Meta reduces dependency on external vendors and gains competitive advantages in data quality and speed.

The hiring of Alexandr Wang as co-head of Meta’s Superintelligence Labs is particularly strategic. Wang, at 28, has built Scale AI into one of the most valuable AI infrastructure companies. His expertise in data curation and model training gives Meta an edge in developing proprietary AI systems that can’t be easily replicated by competitors.

Meta’s approach to “personal superintelligence” also reveals shrewd market positioning. While competitors focus on enterprise AI (which has limited total addressable market), Meta is targeting the consumer market — all 3.48 billion daily active users across their platforms. The revenue potential is exponentially larger.

Microsoft’s Partnership Paradox:

Microsoft’s relationship with OpenAI is both their greatest asset and biggest risk. The partnership gave Microsoft early access to cutting-edge AI technology, but it also created dangerous dependency. The current renegotiation of their deal highlights a crucial strategic inflection point.

Microsoft’s diversification strategy — partnering with xAI, Meta, and Mistral — isn’t just risk management. It’s market intelligence. By hosting multiple AI models on Azure, Microsoft gains insights into which approaches work best for different use cases. This positions them to make informed decisions about internal AI development.

The $30 billion quarterly capex isn’t just about meeting current demand — it’s about creating switching costs. Once enterprise customers build their AI workflows on Azure infrastructure, migrating to competitors becomes prohibitively expensive and complex.

The Hidden Risks: What the Earnings Reports Don’t Tell You

Despite the impressive numbers, both companies face significant headwinds that deserve deeper analysis.

Meta’s Efficiency Paradox:

Reality Labs posted a $4.53 billion operating loss on just $370 million in revenue. That’s a staggering 1,124% loss rate. While this was “better than expected,” it raises fundamental questions about Meta’s ability to monetize next-generation computing platforms.

The concerning trend isn’t the absolute loss — it’s the trajectory. Reality Labs has burned through approximately $50 billion since 2020 with minimal revenue growth. If AI investments follow a similar pattern, Meta could face investor revolt.

More troubling is the regulatory overhang. Antitrust lawsuits seeking to break up Meta could force divestiture of Instagram or WhatsApp — platforms that generate the advertising revenue funding AI investments. This creates a circular vulnerability: AI investments depend on advertising revenue that depends on maintaining current market structure.

Microsoft’s Infrastructure Trap:

Microsoft’s record capex spending creates what economists call “sunk cost escalation.” Once you’ve invested $30 billion in AI infrastructure for a quarter, you must continue investing to maintain competitive positioning. This creates a capital allocation trap where Microsoft may be forced to overspend relative to actual returns.

The OpenAI relationship adds another layer of risk. If OpenAI successfully transitions to a public benefit corporation without Microsoft’s preferred terms, Microsoft could lose preferential access to the most advanced AI models. Given that Azure’s growth is significantly driven by AI workloads, this could devastate their competitive positioning.

There’s also a capacity utilization risk. Microsoft admits demand outstrips supply, but what happens when supply catches up? AI workloads are typically bursty and seasonal. Building infrastructure for peak demand could lead to significant underutilization during low-demand periods.

The Market Structure Analysis: Winner-Take-All Dynamics

The AI infrastructure buildout isn’t just about technology — it’s about creating insurmountable competitive moats.

The Capital Requirements Barrier:

Microsoft’s $30 billion quarterly spending and Meta’s $66-72 billion annual capex create entry barriers that few companies can match. Only Apple, Google, and Amazon have similar financial resources. This effectively locks smaller competitors out of the AI infrastructure race.

But there’s a catch: these investments only pay off if AI demand continues growing exponentially. If growth plateaus or alternative technologies emerge, these companies could face stranded asset problems on an unprecedented scale.

The Talent War Economics:

Meta’s strategy of poaching researchers with “$100+ million pay packages” isn’t just about acquiring talent — it’s about denying talent to competitors. In a market where AI expertise is the primary constraint, hiring becomes a zero-sum game.

This creates wage inflation that benefits individual researchers but increases industry costs. Meta and Microsoft can afford this; smaller AI companies cannot. The result is further market consolidation around well-capitalized players.

The Data Network Effects:

Meta’s 3.48 billion daily active users generate training data that cannot be replicated by competitors. This data advantage becomes more valuable as AI models require larger, more diverse datasets. Microsoft’s enterprise customer base provides similar advantages in business data.

These data network effects suggest that early AI leaders will become increasingly dominant over time. The companies making massive investments today are essentially buying future market positions that may be unassailable.

The Bigger Picture

What we’re witnessing is essentially a new kind of arms race. Just as countries once competed to build the most nuclear weapons, tech companies are now competing to build the most powerful AI systems.

Google parent Alphabet recently raised its capital spending plans to about $85 billion for the year. Amazon is expected to announce similar massive investments. The combined capital expenditure from Big Tech companies could reach $330 billion this year alone.

This level of spending would make even the most ambitious infrastructure projects look modest by comparison. The U.S. Interstate Highway System, adjusted for inflation, cost about $500 billion. These companies are approaching that level of investment in just a couple of years.

What This Means for Investors

For investors, these earnings reports present both opportunity and risk. On one hand, both Meta and Microsoft are showing that AI investments can drive real revenue growth. Meta’s advertising business is clearly benefiting from AI-powered recommendations, while Microsoft’s cloud business is thriving on AI demand.

On the other hand, the scale of investment required is staggering, and there’s no guarantee that current growth rates can be sustained. As Emarketer senior analyst Minda Smiley noted, “Meta’s exorbitant spending on its AI visions will continue to draw questions and scrutiny from investors who are eager to see returns.”

The Bottom Line

Meta and Microsoft’s latest earnings reports tell us that the AI revolution isn’t coming — it’s already here. Both companies are making massive bets that AI will fundamentally transform how we work, communicate, and live.

The early returns are promising, but we’re still in the early innings of this game. The companies that can successfully navigate the transition from massive investment to sustainable profits will likely dominate the next decade of technology.

For now, Wall Street seems willing to bet alongside Zuckerberg and Microsoft CEO Satya Nadella. But as any good investor knows, past performance doesn’t guarantee future results. The AI gold rush is real, but only time will tell who strikes it rich and who goes bust trying.

What’s certain is that we’re witnessing one of the most significant technological and financial shifts in modern history. And if these earnings reports are any indication, the ride is just getting started.

Disclaimer – This article draws from sources such as the Financial Times, Bloomberg, and other reputed media houses. Please note, this blog post is intended for general educational purposes only and does not serve as an offer, recommendation, or solicitation to buy or sell any securities. It may contain forward-looking statements, and actual outcomes can vary due to numerous factors. Past performance of any security does not guarantee future results. This blog is for informational purposes only. Neither the information contained herein, nor any opinion expressed, should be construed or deemed to be construed as solicitation or as offering advice for the purposes of the purchase or sale of any security, investment, or derivatives. The information and opinions contained in the report were considered by VF Securities, Inc.to be valid when published. Any person placing reliance on the blog does so entirely at his or her own risk, and does not accept any liability as a result. Securities markets may be subject to rapid and unexpected price movements, and past performance is not necessarily an indication of future performance. Investors must undertake independent analysis with their own legal, tax, and financial advisors and reach their own conclusions regarding investment in securities markets. Past performance is not a guarantee of future results