Skip to content

Skip to content

The fourth quarter of 2024 has been a strong one for major US banks like JPMorgan, Goldman Sachs, and Citigroup, with their profits surpassing expectations. But what is driving this impressive performance, and what does it mean for the financial landscape in the coming months?

The Fuel Behind the Surge

For starters, let’s talk about what’s fueling this growth. Banks have been benefiting from several factors that have aligned at just the right time. First off, interest rates have remained relatively high, giving banks a much-needed boost in their lending businesses. Higher interest rates mean that banks can charge more for loans, which translates into higher profits. But that’s not the only thing at play.

Banks have also capitalized on strong trading activity, particularly in the bond and equity markets. Despite volatility, institutional investors have continued to pour money into financial markets, and banks like Goldman Sachs have profited from their trading desks.

The Market’s Reaction

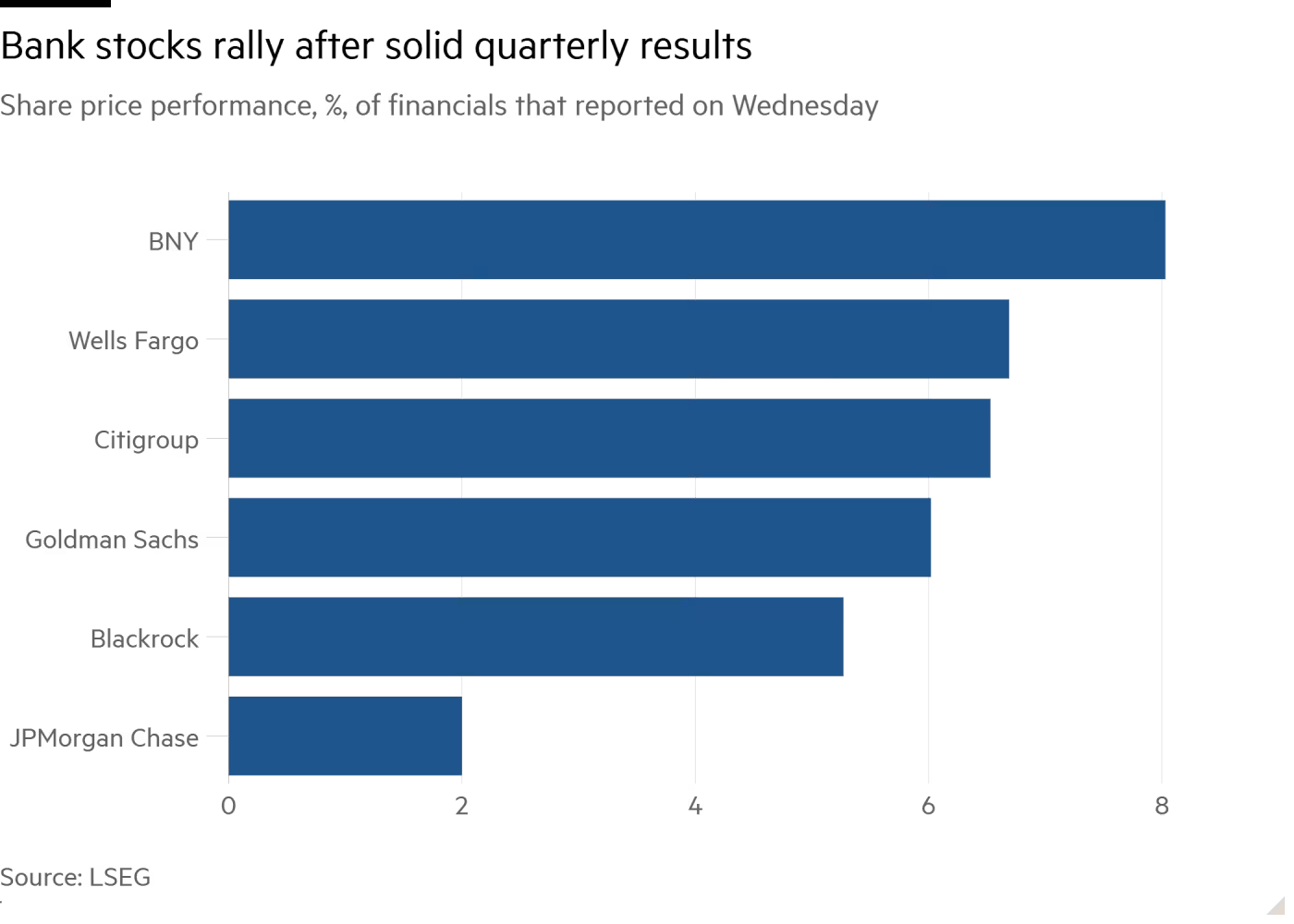

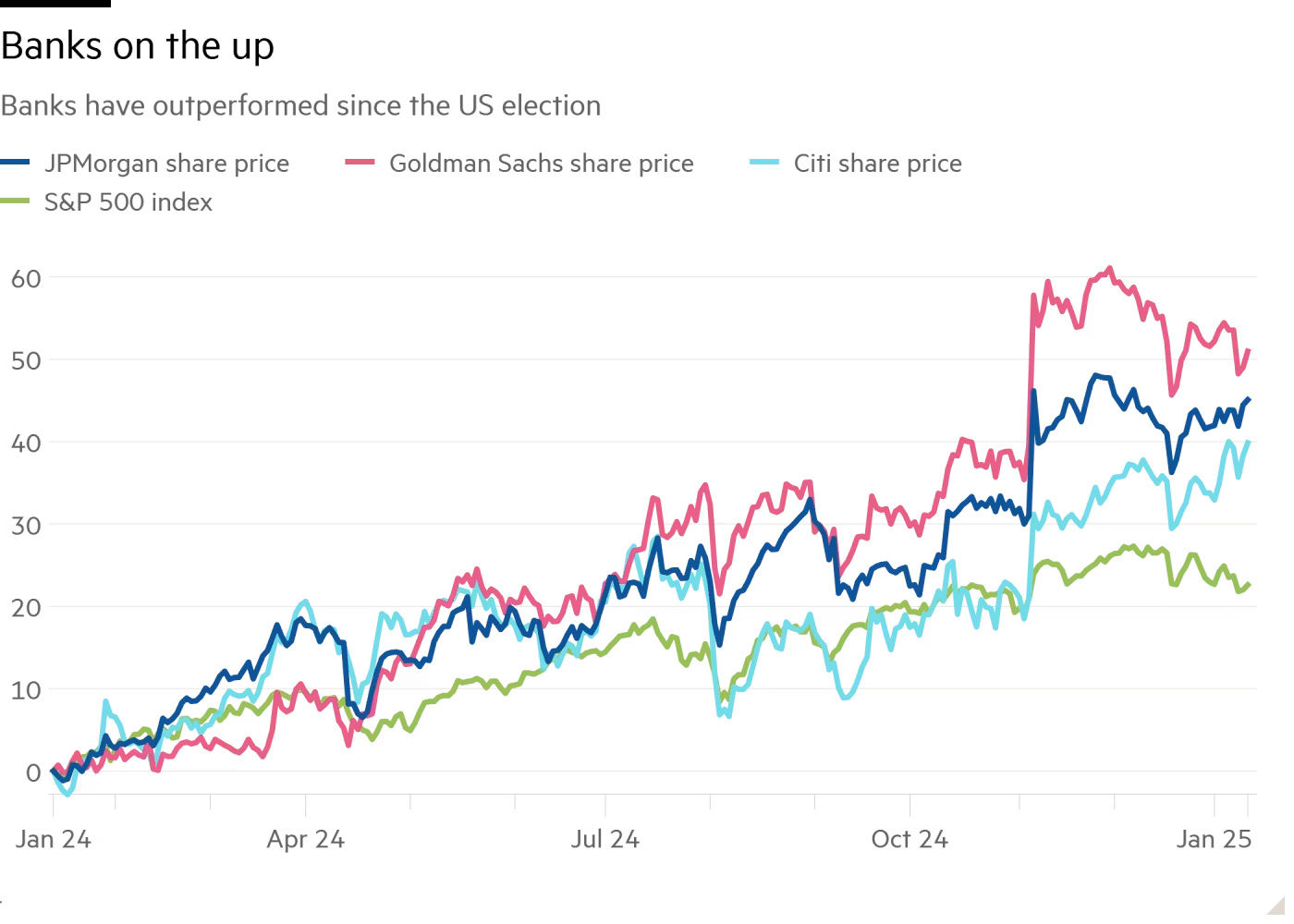

The performance of big U.S. banks also had a noticeable impact on their stock prices. Bank stocks jumped again in pre-market trading on Wednesday, continuing their strong momentum from 2024, when they recorded their biggest outperformance over the broader market in nearly a decade.

Source: Financial Times

The banking sector was a standout performer in 2024. The KBW Bank Index soared by 33%, its best year since 2013. It outpaced the S&P 500 by 9.4%, marking its biggest lead over the broader market since 2016. Despite concerns over high interest rates, investors remained confident in the sector’s strength.

Source: Financial Times

JPMorgan: Resilient Growth Amidst Market Shifts

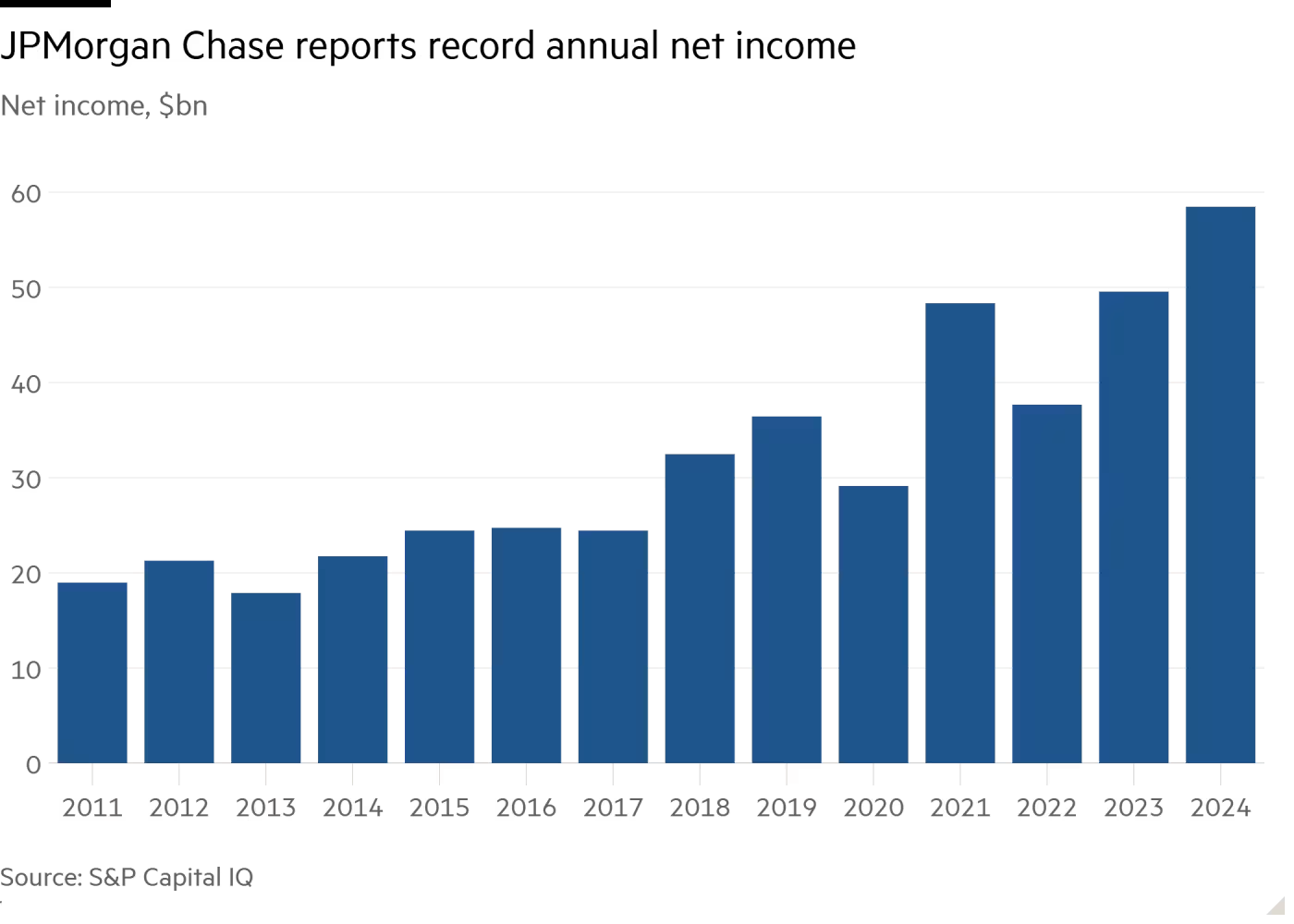

JPMorgan Chase has just wrapped up the most successful year in its history. The bank reported record earnings and revenue for Q4 2024, solidifying its position as the most profitable U.S. bank ever.

Source: Financial Times

The Numbers: A Record-Breaking Quarter

JPMorgan posted earnings of $4.81 per share, easily surpassing the expected $4.11. Revenue shot up by 10% to reach $43.74 billion, beating analysts’ forecasts of $41.73 billion. It’s clear that the bank’s diversified business model is paying off, but what’s really standing out is the performance of its Wall Street operations.

Wall Street Powers the Growth

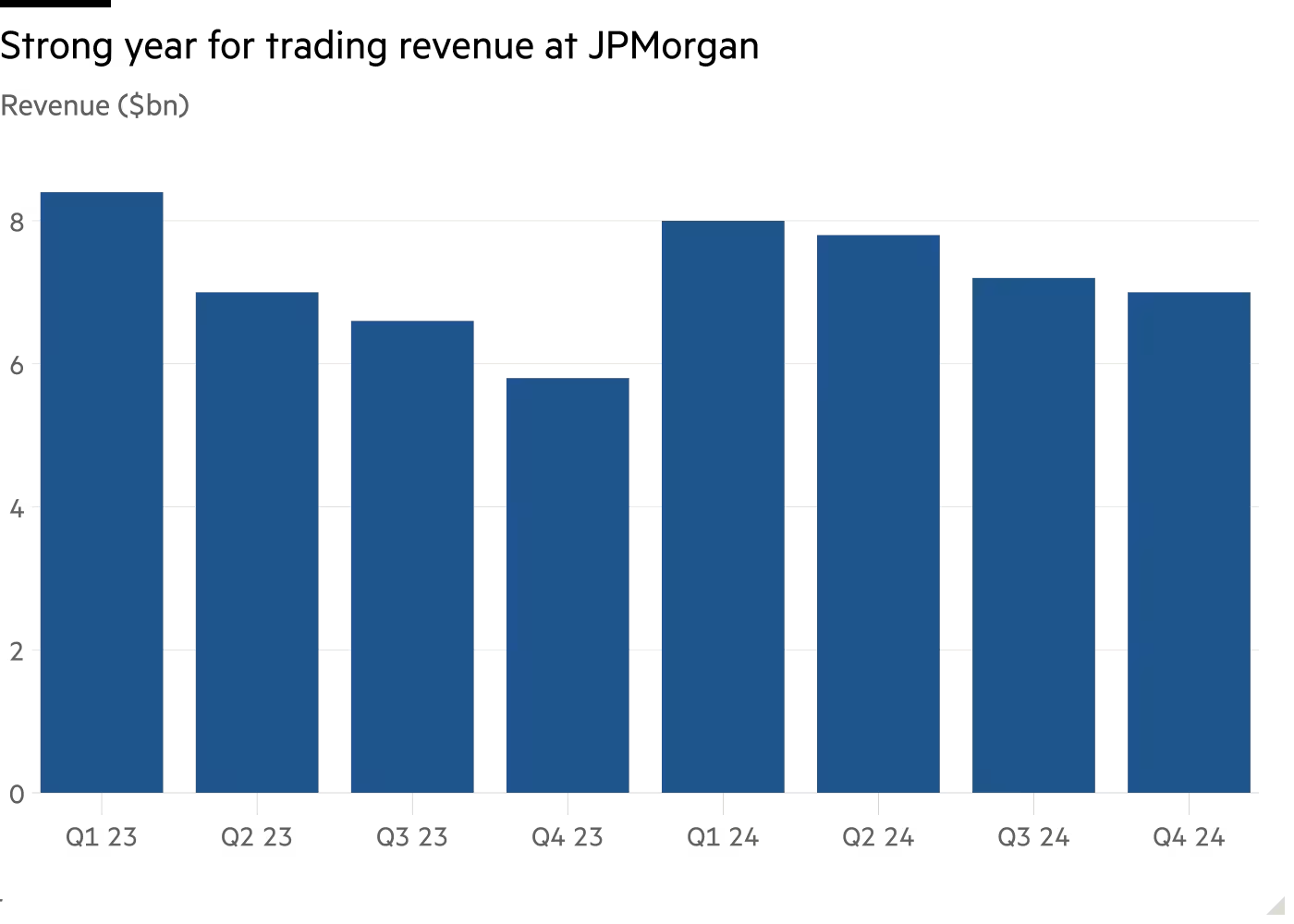

JPMorgan’s fixed-income trading business had a stellar performance, with revenue climbing 20% to $5 billion, driven by strong credit and currency trading. Equities trading, too, saw a 22% increase, although it slightly missed expectations. But the real showstopper was investment banking fees, which surged 49% to $2.48 billion, easily beating estimates of $2.39 billion.

Source: Financial Times

It’s clear that JPMorgan is benefiting from a strong rebound in market activity. Despite earlier concerns, its trading desks are humming, and its investment banking unit has bounced back in a big way.

Net Interest Income: A Mixed Bag

On the lending side, JPMorgan’s net interest income (NII)—which is the difference between what the bank earns on loans and pays on deposits—came in at $23.47 billion, smashing estimates by nearly $400 million. That’s the good news. The bad news? In Q4, NII actually dropped by 3% year-over-year, marking the first decline since 2021. This decline highlights the growing pressure on banks as deposit rates rise and loan growth remains muted.

Despite the dip in NII, the bank’s overall performance in Q4 remained robust. Profit rose 50% to $14 billion, thanks to a significant drop in non-interest expenses (down 7% from last year). This drop was primarily attributed to the $2.9 billion FDIC assessment last year, which was tied to the regional banking crisis.

The First Republic Acquisition: A Smart Move?

JPMorgan made a strategic move amid the banking turmoil. The bank acquired First Republic Bank out of the FDIC’s receivership. This acquisition allowed JPMorgan to gain more deposits and assets, further strengthening its position. While it paid a hefty FDIC assessment last year to stabilize the deposit insurance fund, JPMorgan’s gamble has clearly paid off, allowing it to continue growing even as others struggled.

Looking Ahead: Risks & Opportunities

Looking into 2025, JPMorgan’s outlook remains strong, with the bank forecasting net interest income of $94 billion, above analysts’ expectations. However, the decline in NII in Q4 suggests that the road ahead may not be entirely smooth. If the Federal Reserve continues to ease rates, it could put further pressure on net interest income. On the plus side, JPMorgan’s diversified business lines, including trading and investment banking, should cushion the bank from rate-related headwinds.

Goldman Sachs: Banking on investment banking for a stellar comeback

Goldman Sachs has closed out 2024 with a bang, reporting its biggest quarterly profit in over three years. On Wednesday, the bank posted fourth-quarter earnings that exceeded expectations, riding on a wave of robust trading revenue and a strong performance across its investment banking division.

The Numbers at a Glance

Goldman’s earnings came in at $11.95 per share, way ahead of the estimated $8.22. Revenue, meanwhile, surged by 23%, reaching $13.87 billion, comfortably topping the forecast of $12.39 billion. This performance pushed the bank’s quarterly profit up to $4.11 billion, more than double its $2.01 billion profit from the same period last year.

Trading Takes the Lead

A standout in this quarter was trading revenue, which drove much of Goldman’s success. Equities trading brought in $3.45 billion, a $450 million beat on Wall Street estimates. But it was fixed income trading that truly stole the show, generating $2.74 billion, exceeding expectations by nearly $300 million. This uptick in trading was driven by a broader rally in equity and bond markets, particularly in the wake of lower interest rates and economic optimism following the U.S. election.

Goldman’s investment banking division also had a solid quarter. Its fees increased by 24% to reach $2.05 billion, primarily fueled by debt underwriting and a rebound in mergers and acquisitions. The bank continues to benefit from a strong recovery in dealmaking, which is helping offset the pressures from previous years.

Strength Across Divisions

Goldman’s asset and wealth management division also posted impressive results, with revenue climbing 8% to $4.72 billion, far exceeding expectations by over $500 million. The division’s strong showing was supported by growth in both asset management and private wealth businesses, signaling increasing investor confidence in Goldman’s ability to manage and grow client funds.

The broader global banking and markets division, which encompasses trading and investment banking, saw revenue spike by 33% to $8.48 billion, powered by both trading gains and a pickup in investment banking activity.

Goldman’s Strategic Shift and Leadership Changes

Goldman Sachs is refocusing resources by exiting unprofitable ventures and launching a private credit division for large deals. Its consumer finance business, however, remains a weak spot. The unit posted an $859 million loss in 2024, and its Apple credit-card partnership faces uncertainty.

Despite challenges, the bank is optimistic about 2025, expecting strong M&A and equity deal pipelines fueled by rate cuts and market optimism. Goldman’s 48% stock surge reflects its success, but consumer finance struggles and macroeconomic hurdles remain key concerns.

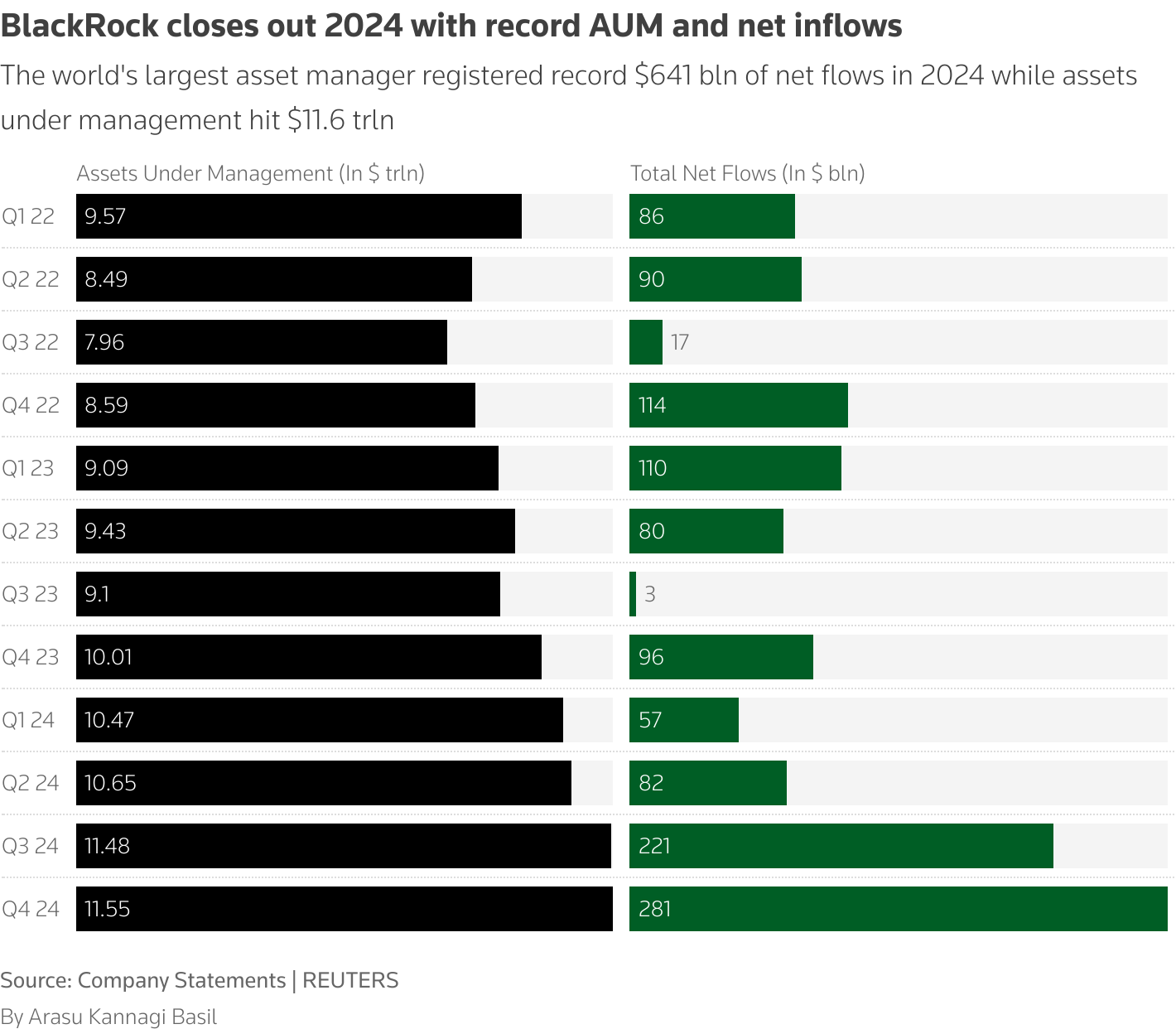

BlackRock’s Record-Breaking Q4: A Deep Dive Into Its Stellar Performance

In the final quarter of 2024, BlackRock, the world’s largest asset manager, hit a record high of $11.6 trillion in assets under management (AUM). This milestone wasn’t just about numbers; it marked a significant jump in profitability, with the firm reporting a 21% year-over-year increase. But what exactly drove this surge, and why does it matter in the broader financial landscape?

To understand BlackRock’s remarkable performance, it’s important to break down the key factors at play. First, the company benefited from strong movements in global equity markets. The U.S. stock market, in particular, saw a significant rally, which was partly spurred by investor optimism following the results of the 2024 presidential election. Lower corporate taxes and deregulation were seen as key drivers for this optimism, translating to higher stock prices and, consequently, more money flowing into the market. BlackRock, with its vast portfolio of equity funds, reaped the rewards.

But it wasn’t just about equities. BlackRock’s strategy to diversify its investments into private markets has also paid off. In 2024, the firm made substantial acquisitions, including the $25 billion purchase of Global Infrastructure Partners and HPS Investment Partners. This move was a clear signal of BlackRock’s intent to strengthen its position in the rapidly growing private investment space.

Net Inflows: A Closer Look at the Numbers

Another standout feature of BlackRock’s Q4 was its impressive net inflows. The company reported a whopping $281.4 billion in total net inflows for the quarter, a substantial increase from the previous year’s $95.6 billion. Of this total, $201 billion came from long-term net inflows, with exchange-traded funds (ETFs) capturing a lion’s share of $142.6 billion. This reflects an ongoing trend where investors are increasingly flocking to passive investment products like ETFs, which BlackRock has expertly capitalized on.

Strong Revenue Growth

BlackRock’s revenue also saw a substantial increase, with the firm posting $5.68 billion for the quarter, up 22.6% from the previous year. This surge in revenue was primarily driven by higher fee income, which came as a direct result of the strong equity market performance and the growing demand for BlackRock’s investment products. The company’s investment advisory, performance fees, and securities lending revenue also grew by 22.5%, reaching $4.42 billion.

The firm’s ability to increase its fee income highlights the strength of its platform—BlackRock has built a vast infrastructure that allows it to generate consistent revenue, even in volatile markets.

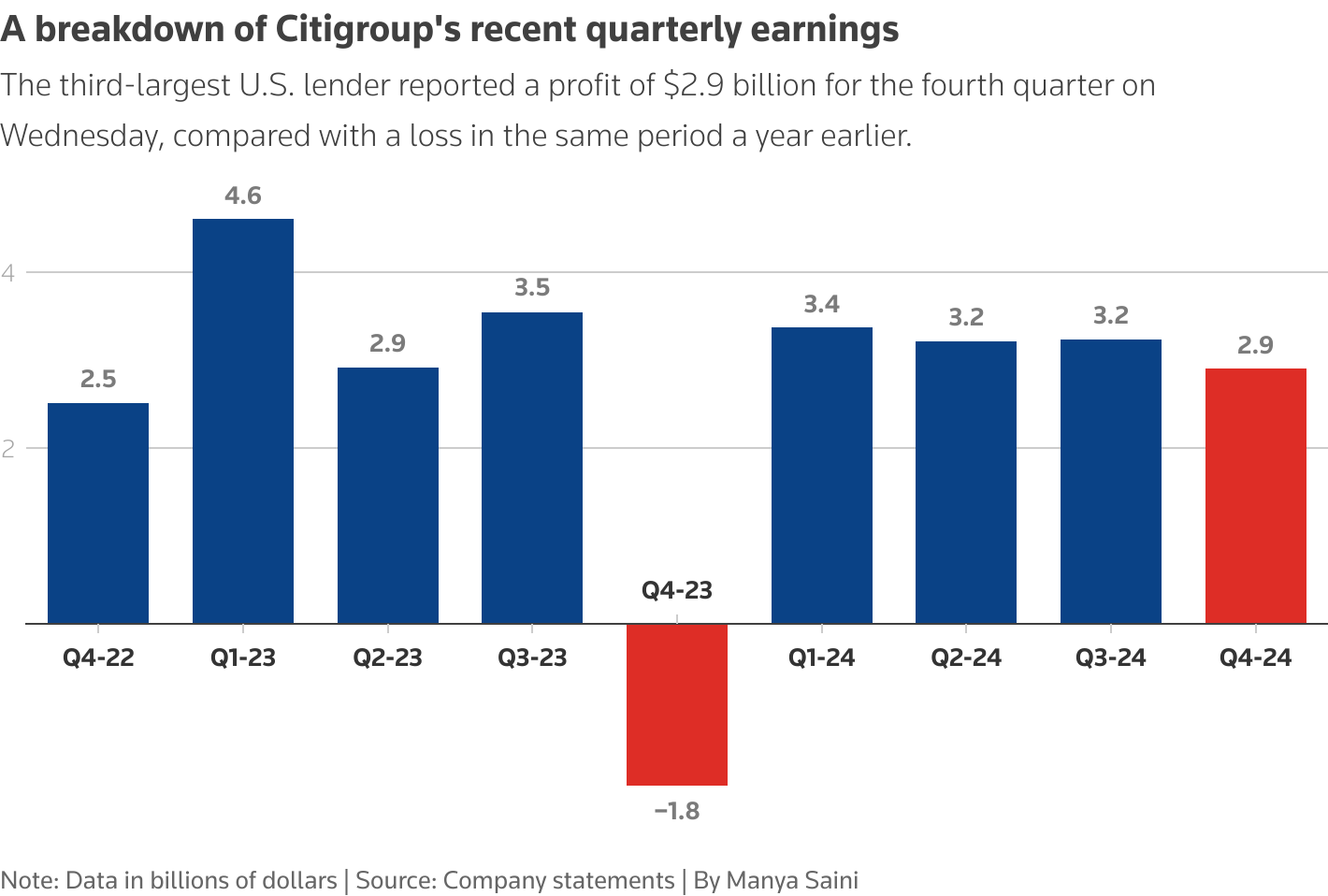

Citigroup’s Strong Q4 Results and Strategic Shifts for 2026

Citigroup’s fourth-quarter results came out stronger than expected, with the bank posting a 6.3% jump in shares. The numbers told a compelling story—net income surged to $2.86 billion from a loss of $1.84 billion the previous year, while revenue rose 12% year-over-year to $19.58 billion.

Source: Reuters

The surge in earnings was fueled by broad-based strength across its business units, with trading and investment banking playing a pivotal role. Trading revenue soared 36%, hitting $4.58 billion, driven by a jump in both fixed income and equity markets. The investment banking division also saw a 35% rise, thanks to a flurry of corporate debt issuances and a rebound in M&A activity.

Citi’s wealth management division, a key piece of CEO Jane Fraser’s strategy, saw a healthy 20% rise in revenue, reflecting strong performance in services for high-net-worth individuals.

However, the bank didn’t stop at just good results—it also lowered its profitability target for 2026. Citigroup now expects its return on tangible common equity (ROTCE) to land between 10% and 11%, down from its earlier target of 11% to 12%. This marks a shift, but Fraser reassured that this is a “waypoint, not a destination,” implying the bank’s long-term focus remains intact.

The ongoing transformation, however, isn’t without its costs. Citigroup has been under regulatory scrutiny in recent years for issues related to risk management and data governance, resulting in fines. To address this, the bank is investing more heavily in technology and compliance improvements. These efforts are expected to pay off, but they are also part of the reason why the bank has adjusted its profitability targets.

In a show of strength, Citigroup also announced a $20 billion stock buyback program. The first $1.5 billion of that will be repurchased in the first quarter of 2025. This move is seen as a reflection of the bank’s confidence in its financial health and growth prospects.