Skip to content

Skip to content

How to spend US$2.3 trillion

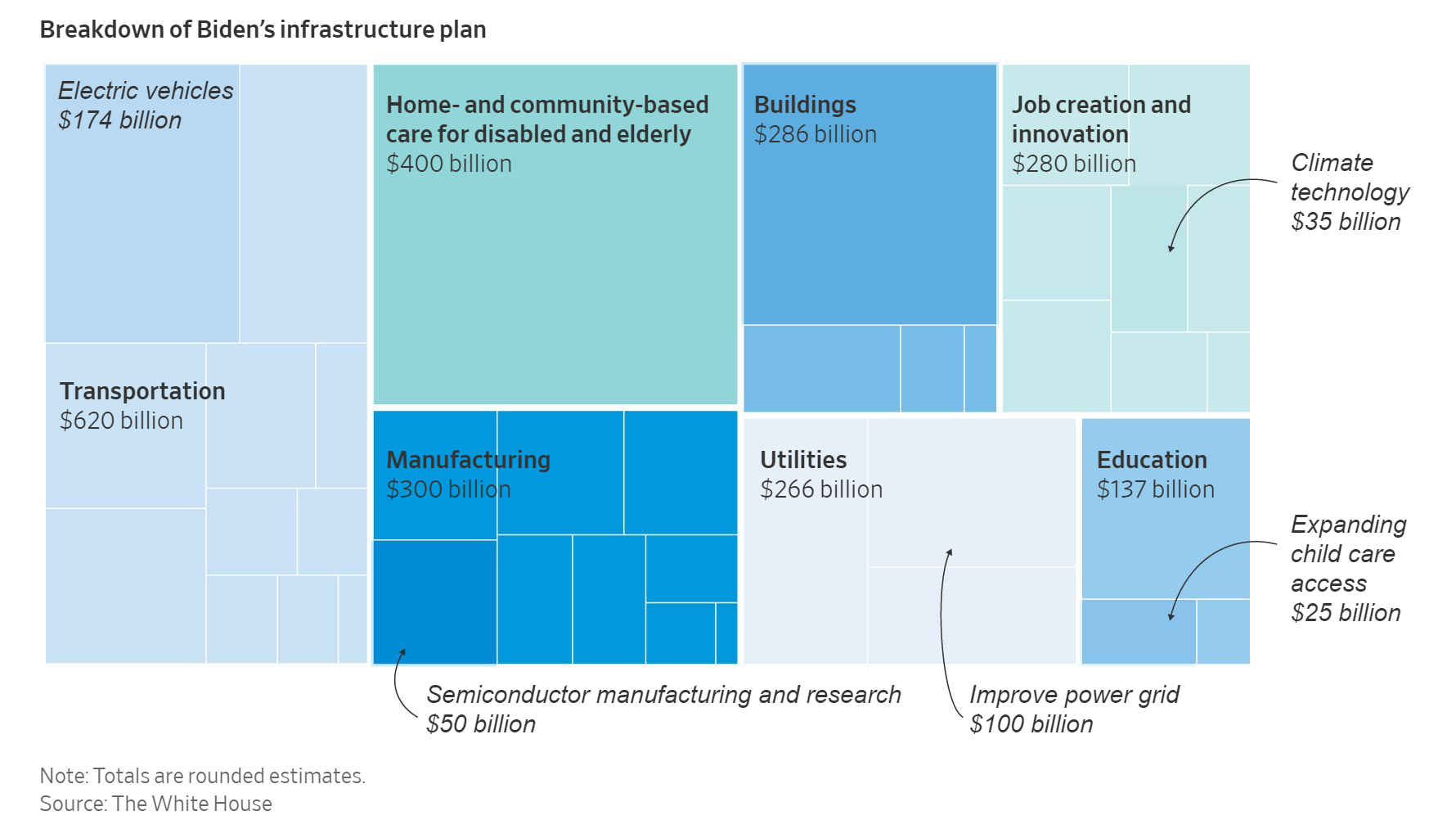

President Biden announced its long awaited massive infrastructure plan. The proposal is audacious. Here’s how he and his administration plan to allocate the US$2.3 trillion spending package (Figure 1):

Some key takeaways:

- One of the key focuses of the plan is investments in fighting climate change. A major part of this effort is US$174 billion in EV investments, which include tax incentives to reduce costs of buying EVs and build 500,000 charging stations by 2030.

- As tensions with China escalate, so is the importance of semiconductor manufacturing. The US plans to invest US$50 billion to help bring back chip making to US shores (many of the most advanced fabs are in Taiwan and South Korea, which are close to the Chinese shores).

- The plan also hopes to modernize more than 20,000 miles of roads and repair 10,000 bridges.

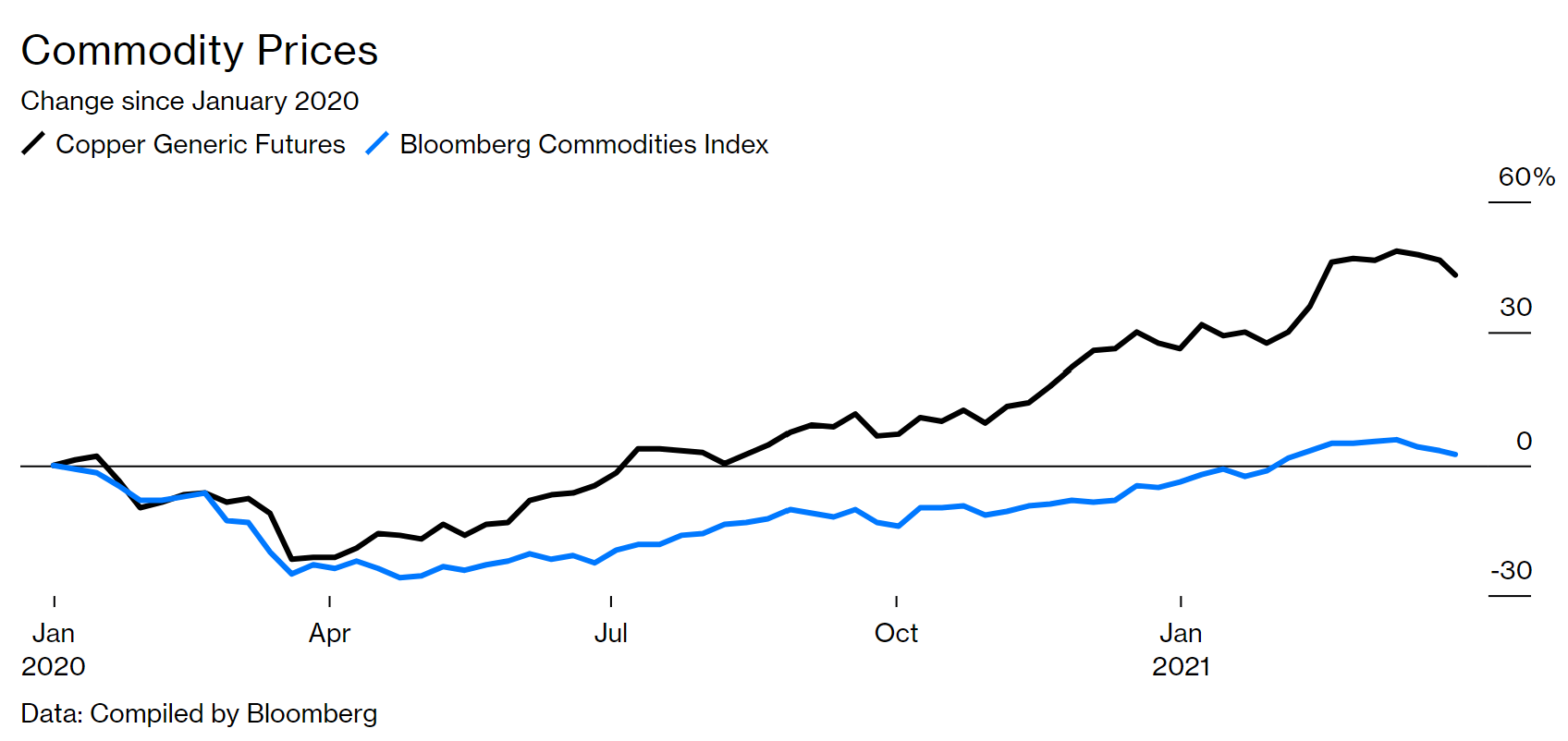

What does this all mean? Raw materials. And lots of it. Copper, nickel, aluminium, steel and others – raw ingredients that go into batteries, chips, roads, and buildings – likely pushing prices up. On this front, China is one-step ahead:

- In 2020, as the world was in a global lockdown, China took advantage of the price plunge in Copper and bought so much supply, that its year-over-year purchase increase was more than the US’ entire annual US consumption.

- Over the years, China has also been securing supplies, buying mining rights from other countries. It has also invested heavily in processing capabilities: the country only mines about 23% of the world’s battery raw materials, but processes about 80% of the volume.

In the game of planned economy, China is one step ahead of the US.

It’s still very early days for Biden’s proposal. The final plan will undergo multiple revisions before it makes its way to congress in the coming months. But if passed, the plan can be a steroid shot to commodity prices, inflation, and the growth prospects of the companies in the sectors mentioned above.

UiPath IPO

It’s no secret that at Vested, we love software-as-a-service (SaaS) businesses. The SaaS vertical has been one of the fastest growing segments of the US stock market, as more and more manual business processes are being automated and replaced with software, spending in the SaaS category is expected to continue to increase.

In this section, we will be discussing a soon-to-be public company that automates manual computer tasks: UiPath.

What is UiPath?

Founded in Romania in 2015, the company has become synonymous with Robotic Process Automation (RPA).

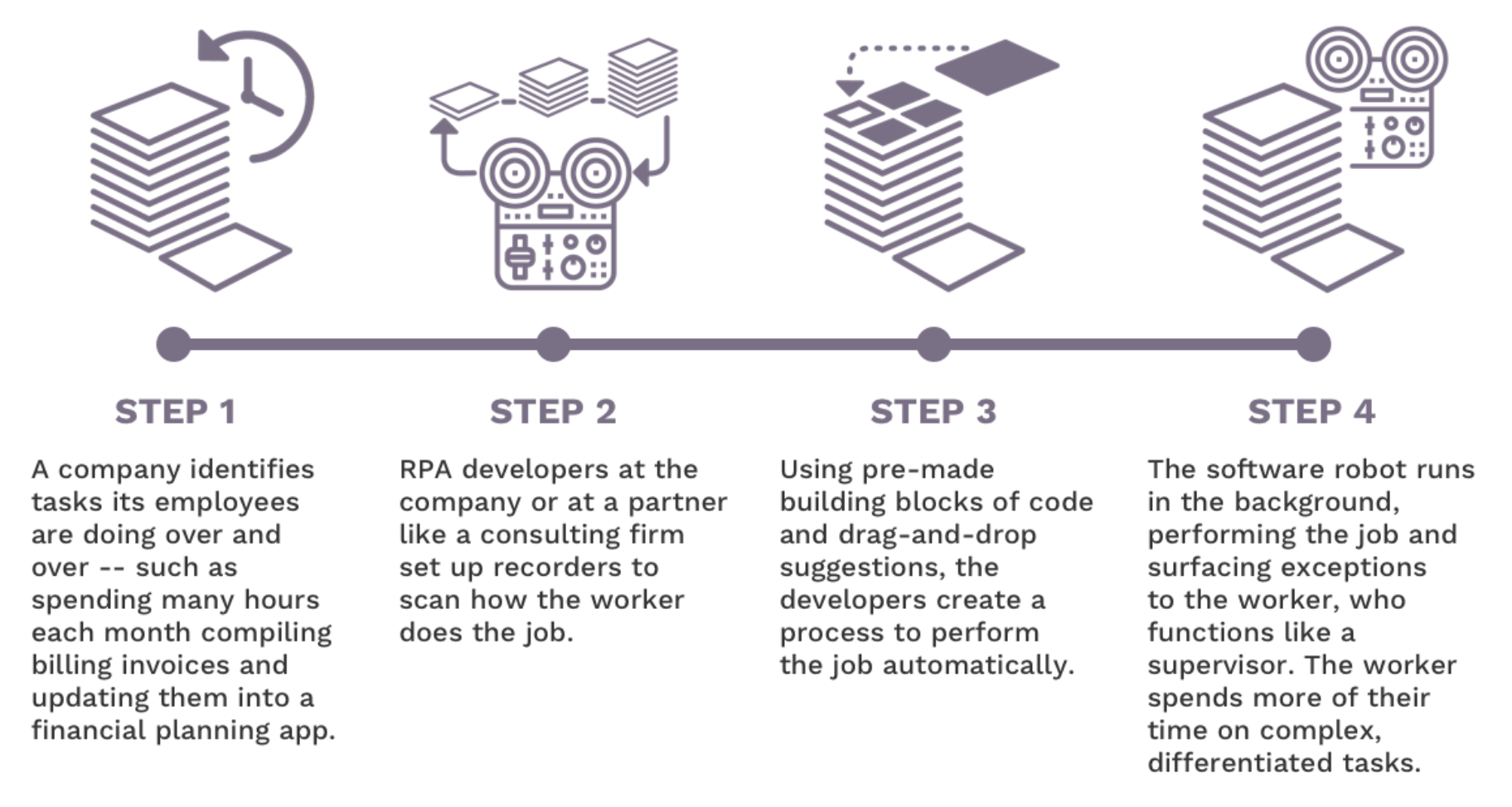

RPA is a suite of software tools that automates manual and repetitive computer tasks. RPA does this by leveraging computer vision, AI, and automation scripts (a combination UiPath would call a robot) to record and emulate tasks that a human would perform on a computer.

Companies typically use RPA to automate backoffice, human resource, finance, and operational tasks. For example, a user can use RPA tools to extract numbers from PDF invoices and transcribe to accounting software without human intervention.

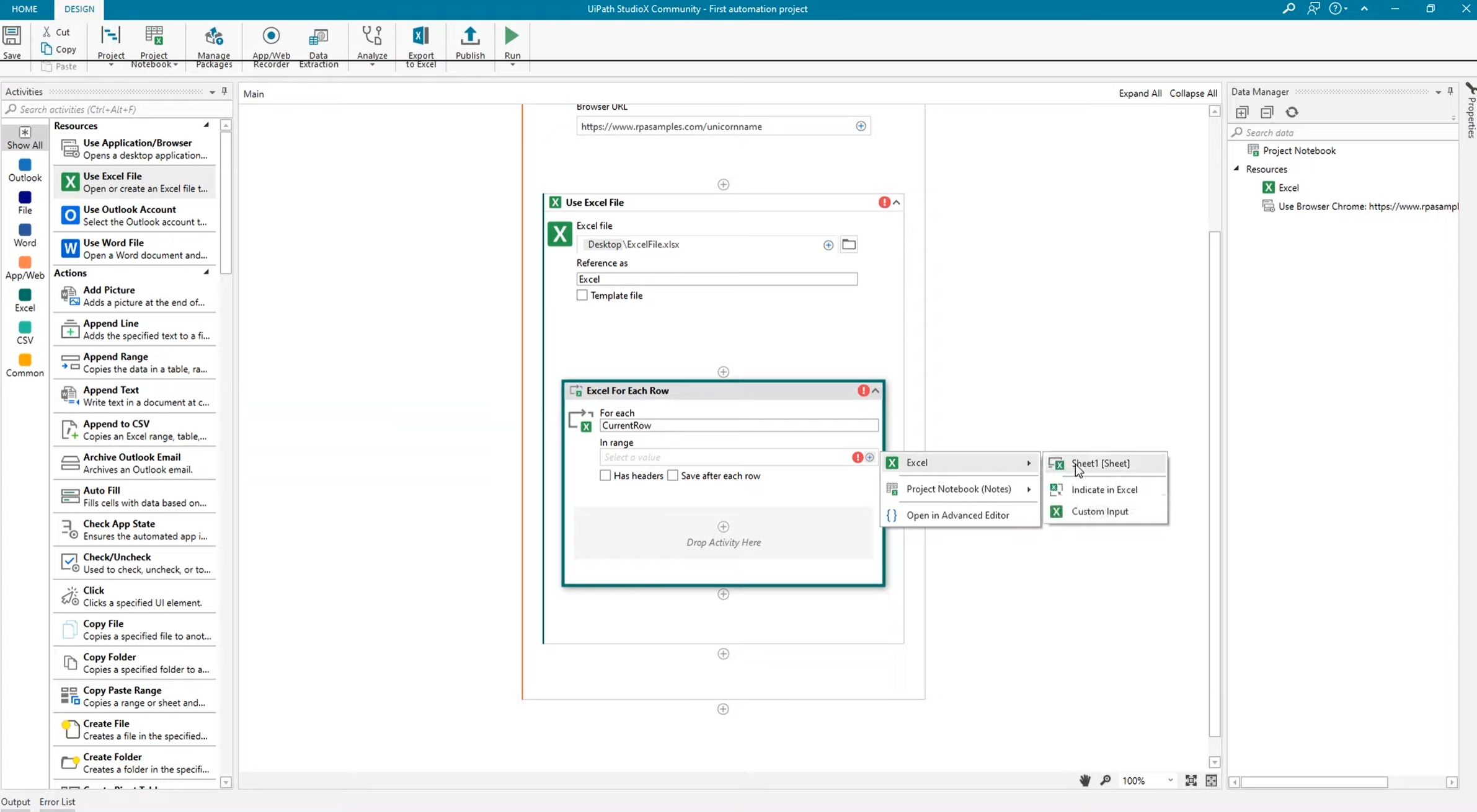

UiPath’s tool set allows its users to create their own workflows to be automated in a low-code manner. Users can record actions and combine different action blocks into a workflow that can then be run automatically (creating digital robots). See Figure 4.

Because the set-up can be done in a low-code environment, it is often faster than creating Excel macros or deploying engineering resources to build internal apps. As a result, non-technical employees are empowered to create their own solutions, enabling the UiPath’s usage to increase within its customers’ organizations, further expanding the company’s revenue (more on this later).

How does UiPath make money?

As of January 31, 2021, UiPath had 7,968 customers, including 80% of the Fortune 10 and 63% of the Fortune Global 500. It generates revenue from three segments:

- Licenses: It sells term licenses to other businesses to use its software (software-as-a-service).

- Maintenance and Support: It provides technical support to help customers adopt and maintain UiPath’s solutions.

- Services and Others: It also sells process automation, education, and training services.

The three segments provide gross margins that are very high (typical of a SaaS business) of 82% and 89% for FY 2020 and 2021 respectively.

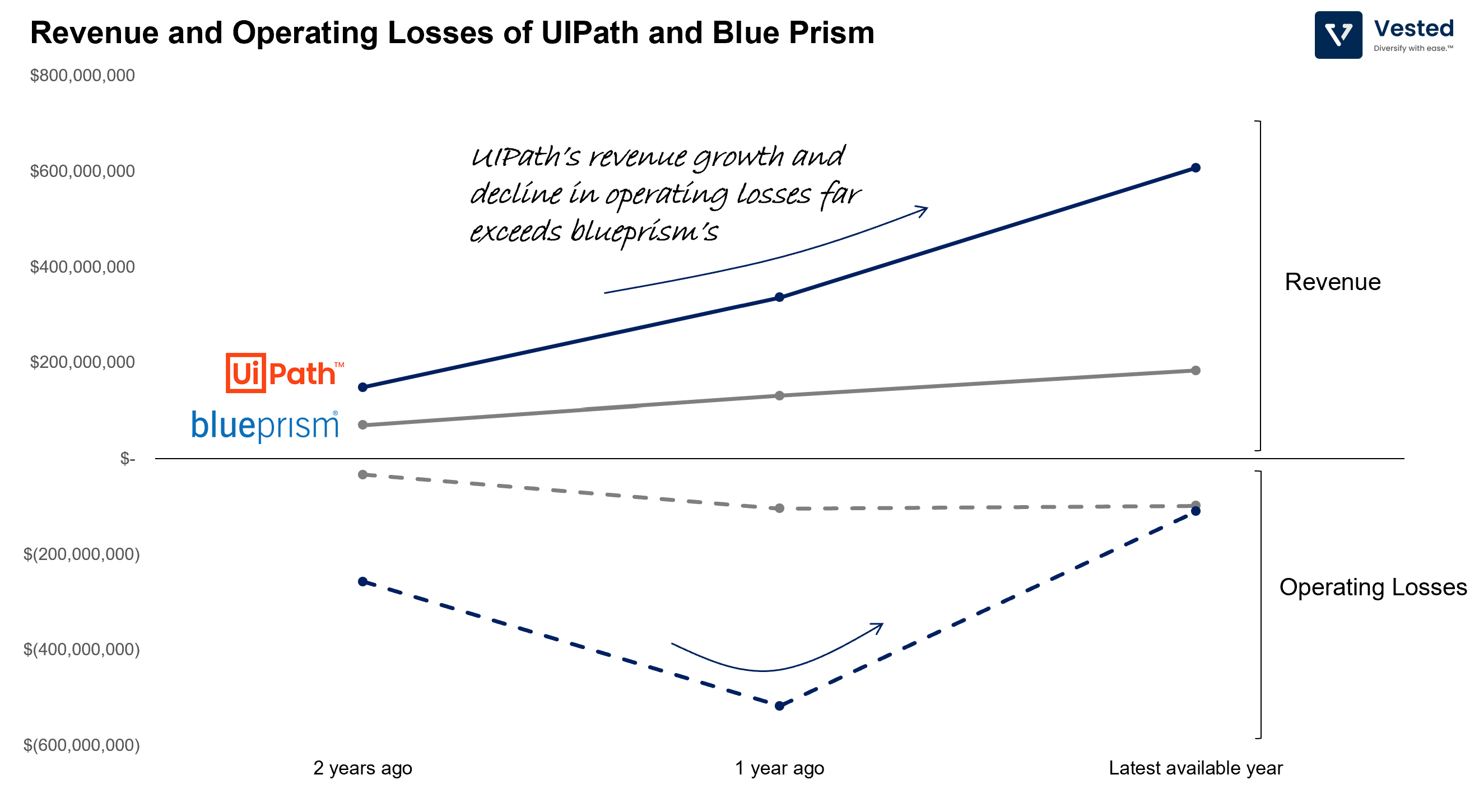

The RPA industry is relatively new. Most of UiPath’s peers are still private (thus we cannot do a financial comparison), with the exception of Blue Prism (a public company traded in the London Stock Exchange). Here’s a comparison of the revenue and operating losses (both companies are not profitable yet) between the two companies.

Despite being public, Blue Prism is actually much smaller than UiPath. Its market capitalization is currently US$1.7 billion. In contrast, UiPath was recently valued at US$35 billion.

The vast difference in valuation is not just because of the size of the earnings, but also the difference in revenue growth rate. Overall, Blue Prism is growing much slower than UiPath (Figure 5). Two years ago, UiPath’s revenue was 1.5x that of Blue Prism. As of the latest fiscal year, UiPath’s revenue is 3.5x that of Blue Prism.

Efficiency in UiPath’s growth

UiPath’s rapid growth is partly because it efficiently leverages in-house sales teams and external partnerships (the company partners with more than 3,700 global and regional system integrators, resellers, and business consultants). And partly because UiPath also has the ability to efficiently land-and-expand once it penetrates an organization. You can see this from its net-dollar retention numbers.

A side note on dollar-based net-retention: When evaluating a SaaS business, a useful metric is dollar-based net retention. This metric indicates how much more a typical customer spends one year after they become a customer. For example, if a customer joined in 2019 and spent US$100,000, a dollar-based net retention of 120% means that this customer in 2020 spends US$120,000. The customer spends more as they use more services.

The higher the dollar-based net retention, the more efficient the business is, as the company does not have to spend sales and marketing dollars to grow existing revenue.

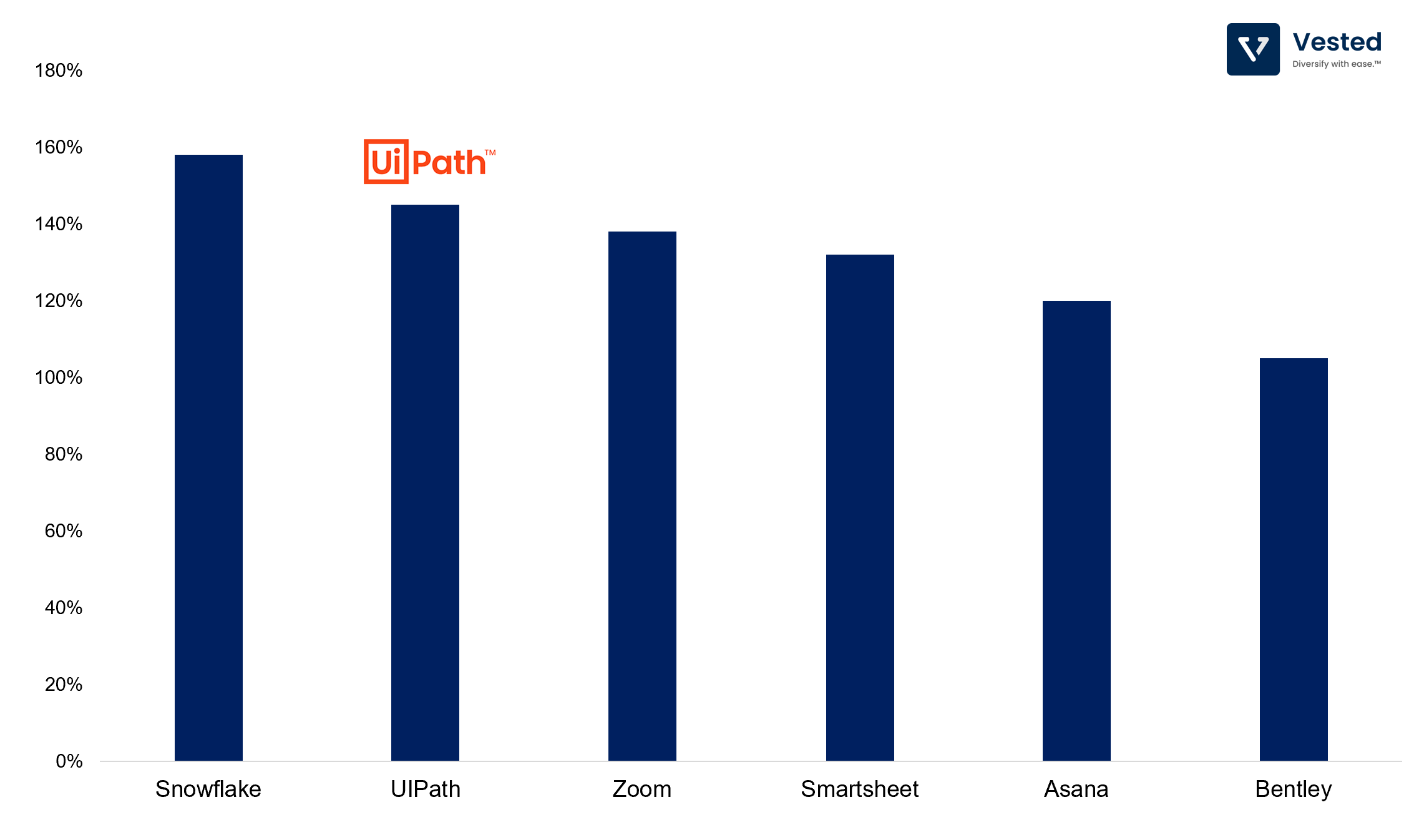

Below is a comparison of the net-dollar retention rates of UiPath vs. other recent public SaaS companies (values are taken from publicly available data – typically around when these companies are going public). As you can see, UiPath is only second to Snowflake.

Valuation will be high

It’s likely that UiPath’s valuation will be high. As recently as a month ago, the company was valued at US$35 billion in the private market, which is 20x higher than that of Blue Prism.

While high net-dollar retention indicates efficiency in growth, it may not translate to share price returns in the short term, especially if valuations are overly high. Take Snowflake, for example. Its share price is currently trading near US$240 per share, which is about the close price of its public debut, 39% lower than its peak in November 2020.

The elephant in the room

Microsoft is a late entrant to this space, but has been making investments in its own automation platform, Power Automate. Microsoft might present a difficult challenge for UiPath.

Why?

- Because Microsoft has similarly extensive sales teams which have already established relationships with all the major enterprises.

- Because Microsoft creates Windows, and therefore can possibly create deeper integration for its own RPA software.

- And lastly, because Microsoft can bundle Power Automate along with Office 365 in a similar manner which it bundled Teams (its chat service that competes with Slack), which had the effect of capping Slack’s growth.