Skip to content

Skip to content

Let’s start with a little history

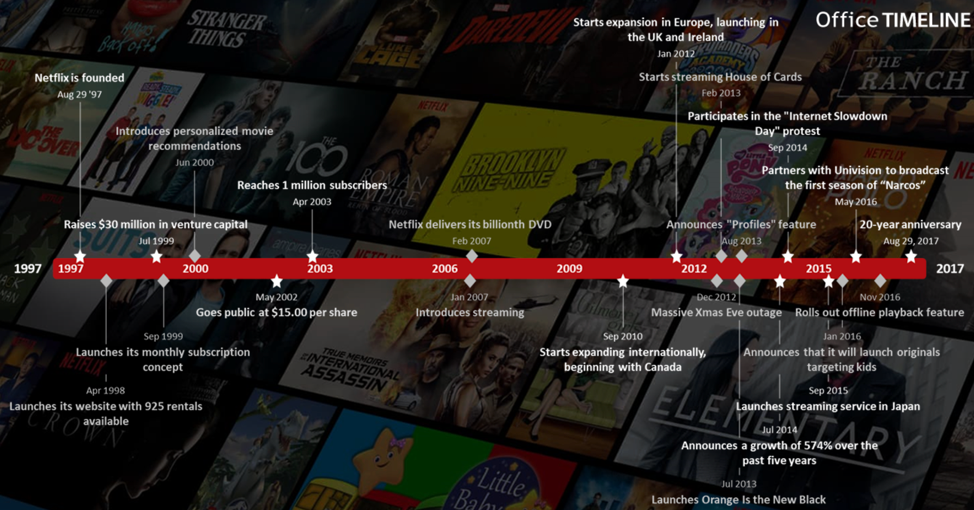

Before we delve into Netflix’s content acquisition strategy, it would be interesting to take a step back and look at the company’s journey. On August 29th 2017, Netflix marked its 20th anniversary. The media streaming giant currently has more than 137 million paid members and is available in 190 countries. The first global TV channel.

Figure 1: Netflix’s timeline

How did a DVD delivery company reinvent itself to become the first and most successful content streaming provider? And, why did its competitors, Blockbuster and Redbox, fail to make the same transition? In a 2016 interview, Reed Hastings, the CEO of Netflix, claimed that when they launched in 1998, the team saw DVD as a 5GB packet that you can mail for $0.32. Reed and the Netflix leadership team saw DVD-by-mail as a high latency digital distribution network, a temporary solution until the internet speed became good enough for streaming. With this vision of ‘delivering content by whatever pipe available’, it was only natural that Netflix made the leap into streaming they were just waiting for it to become technologically possible.

How Netflix first got its streaming off the ground:

In October 2008, Netflix inked a 4-year deal with Starz to stream previously released movies and TV shows for a reported estimated value of $20-30 million. At the time, Starz was trying to monetize content they were already licensing (from Disney). Little did they know that this action jump started the streaming service of its chief competitor, accelerating the fundamental shift from linear TV (regular TV channels where everyone watches the same thing at any one time) to an on-demand streaming service.

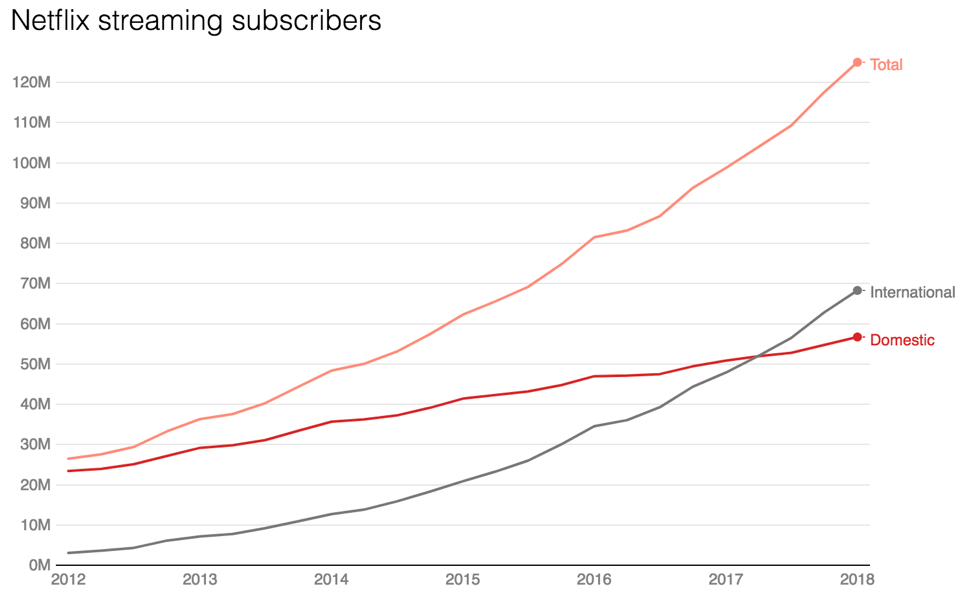

Netflix repeated this content acquisition strategy with other content providers such as AMC networks, Disney, NBC and other traditional content providers. It is likely that all these providers, like Starz, did not feel threatened by selling content old content to Netflix. However, all of these non-original content propelled the initial growth of the Netflix streaming service. Figure 2 below shows the growth of streaming subscribers.

Figure 2: Netflix streaming subscriber

Netflix did not have any original content until 2013 (when House of Cards was launched). Netflix outlined its content acquisition strategy in its the Q3 2017 letter to shareholder. In this letter, Reed Hasting emphasized that the future of Netflix was no longer in content of other networks, but in fact was dependent on creating its own exclusive content. He believed that this would allow Netflix to move up the value chain, from licensing second-run content to licensed originals, and then to Netflix produced exclusives.

Content Strategy

Make shows people want to watch!

Not having the constraints of an advertisement business model, Netflix could focus on creating content that increases customer delight. This sounds sounds obvious, but many US TV providers are constrained by their advertising business model and the limitation of linear TV, where they can only show one show at a time. Thus, the shows they air and produce are not always optimized for quality, but rather broad appeal. This is not the case with Netflix. Since it is a subscription-based streaming service, Netflix can make many shows that appeal to different audiences, however small. Netflix licenses and produces evergreen content (hence no live sports); and broadly, there are two types of shows that the company produces:

- Shows that have a broad audience. An example of this would be Bright, a Netflix original fantasy movie starring Will Smith that has broad global appeal. And as Netflix increases its focus on international market, it is spending more developing local movies and TV shows. Shows such as Sacred Games, a thriller made in India that is based on a best-selling novel.

- Niche prestige shows that create loyal subscribers. Shows such as The Crown, Master of None, etc. The company is also taking advantage of the current narrow, superhero focused, theatrical offerings, by offering a wider array of genres of independent and mid-budget movies of on its platform. Filling a market gap.

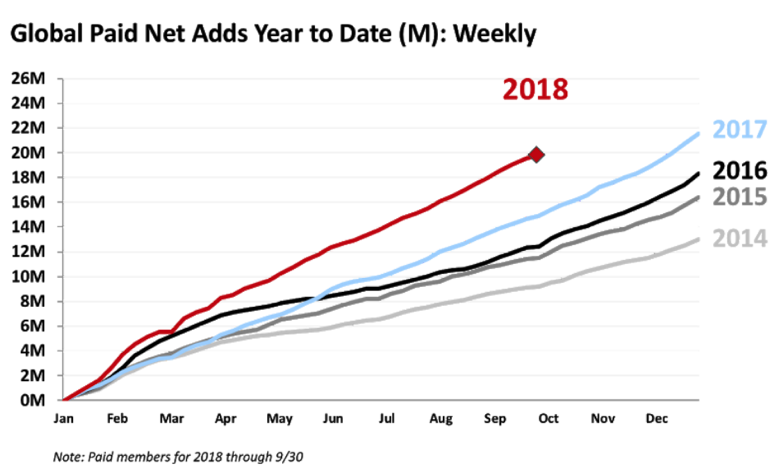

Not surprisingly, making shows that people want to watch leads to lower churn (customers leaving) and higher user growth. As seen in the Figure 3, Netflix’s year over year paid user growth is accelerating. This accelerating user growth is driven by geographical expansion and introduction of new original content. Since Netflix does not release ratings for its shows, we have to rely on third party measurements and quotes from press releases to determine content popularity. Take Bright for example: although critically panned, the movie attracted 11 million viewers in its first three days of release. Similarly, Stranger Things, another Netflix original, drew 16 million viewers within the first three days.

Figure 3: Global paid net add by year

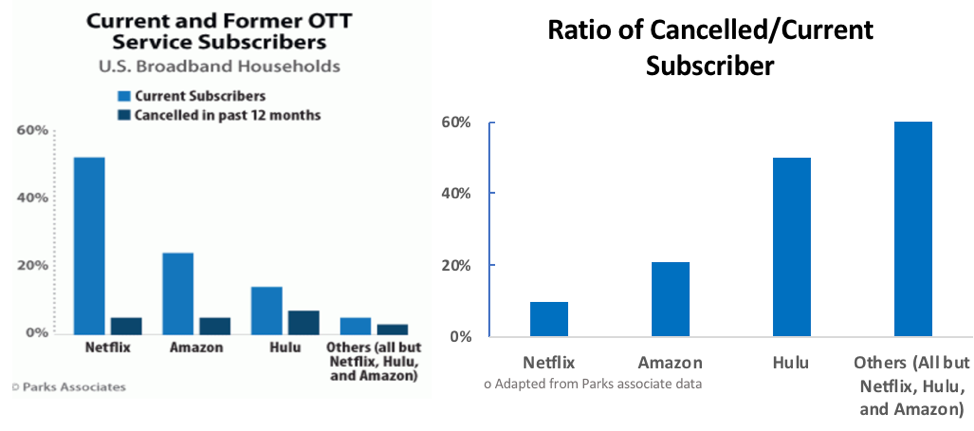

In addition to driving user growth, creating original content that delights customers reduces churn. According to a 2016 study performed by Parks Associate, lack of long-run ongoing perceived value is the primary driver of churn. Therefore, Netflix must continue to provide users reasons to return to the service. The Parks Associate research showed that Netflix is not only the leader in streaming services, but also has the lowest churn as a percentage of customer base. Figure 4(A) summarizes Netflix’s user base and cancellation rate as a portion of broadband households in the US, while Figure 4(B) summarizes the churn rates of Netflix vs. its competitors, calculated using data shown in Figure 4(A). Note that churn rate is defined as the ratio of cancellations/current subscribers.

As of early 2016, Netflix is the Over the Top (OTT) leader with 52% of all household subscribing to its service. It also has the lowest churn rate, with only 5% of all US broadband user cancelling their service in 2015. These numbers mean that Netflix has an 9% annual churn rate. This means the average customer will stay with the service for 11 years, giving Netflix a lifetime value of roughly $1210 [with a projected revenue of $16 billion dollar, and an expected 146 million subscriber by end of 2018, estimated revenue/user is ~$110/year/user, over 11 years, this equals to $1210].

Figure 4: (A) Current and Former Over the Top (OTT) subscriber as a percentage of US broadband customer from Park’s Associate research. (B) Ratio of Cancelled/Current Subscriber, adapted from (A).

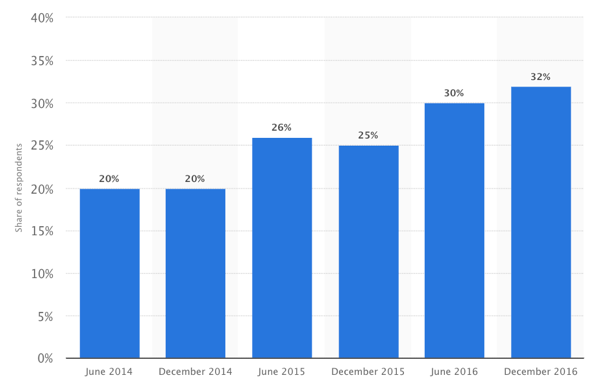

In addition to churn measurements, we can also measure Netflix’s stickiness by surveying consumers’ viewing habits. With the proliferation of original content, the viewing habits of Netflix’s customer has shifted over the years. Figure 5 shows that the share of Netflix customers that primarily watch original content has increased from 20% in 2014, to 32% at end of 2016. This shift reduces Netflix’s dependency on licensed content from 3rd party providers.

Figure 5: Share of Netflix customers who watch original content most often in the United States from 2014 to 2016

Own your content!

As Netflix grew, it had to reduce content dependency from external providers. Figure 6 below illustrates the value chain where Netflix only licenses 2nd run content (licensing content from 3rd party). Netflix would pay content providers a sum of money for a limited distribution license (limited in both time and region). This also means Netflix is effectively funding the development of competitor’s internet TV. Fortunately, since Netflix is an aggregator, it has the data advantage. It collects users viewing behaviors to understand customers’ preferences, which in turn helps inform the production of its original content.

Figure 6: Value chain of Netflix’s content without original content

With original content, Netflix subsumes the role of the content provider and collaborates directly with content creators. This direct collaboration allows for a greater share of the profit to the creators. It has been reported that Netflix is coming to multimillion dollar agreements with comedians and show runners to produce exclusives. This direct relationship also allows for more artistic freedom for creators, attracting more creators to work with Netflix. But most importantly, this arrangement gives Netflix exclusive content that is less restrictive, has longer lifetime in the Netflix library, and can be simultaneously released globally. This vertical integration also means that Netflix will require more capital to deploy, as it must continue to invest in production capacity (as indicated by a recent $1 billion dollar investment in a new studio in Albuquerque, New Mexico), and to develop new capabilities around production planning, crew, vendor management and visual effects.

Figure 7: Value chain of Netflix’s content with original content

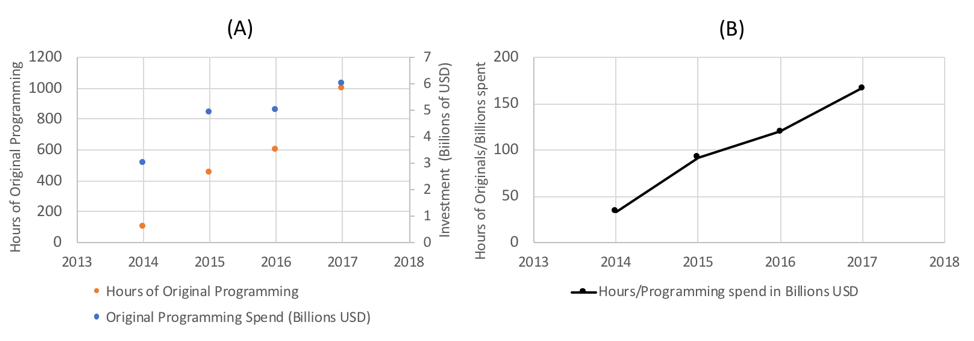

Since the launch of House of Cards in 2013, Netflix has only accelerated its investment in original programming. Figure 8(A) shows that since 2014, Netflix has increasedits investment in original content by more than $1B year over year, growing its content from less than 200 hours in 2014 to more than a 1000 hours by the end of 2017. In Figure 8(B), we can see that the efficiency of capital has increased over time, as the content output per USD invested has more than tripled in 3 years. Please note that this is a qualitative comparison as there is a 1–3 years lag between investment to viewing and revenue impact in the P&L.

Figure 8: (A) Increase of amount of Original programming and Total Investment Spend by year. (B) Effectiveness of investment: Hours of Programming/Investment in billions USD

[mc4wp_form id=”1064″]