Skip to content

Skip to content

Tesla Strategy Analysis

If you’re looking for Tesla strategy analysis, you’ve come to the right place! Check Tesla’s latest share price

A brief history of Tesla

Tesla is a remarkable company. It is the first US car company to go public since 1956, the first electric car company that not only builds cars but also constructs a nationwide integrated charging network, and – arguably one of its greatest accomplishments – the company that changed the public perception of electric cars. Tesla made electric cars cool.

The company was founded in July 2003, and contrary to popular belief, was not originally founded by Elon Musk, but rather two entrepreneurs and engineers: Martin Eberhard and Marc Tarpenning. After a string of issues and multiple CEOs, Elon, who at the time was the primary financier of the company, stepped in as the CEO in October 2008.

Tesla’s mission is to accelerate the world’s transition to sustainable energy. Its master plan is outlined in a letter Elon wrote:

- Build sports car

- Use that money to build an affordable car

- Use that money to build an even more affordable car

- While doing above, also provide zero emission electric power generation options

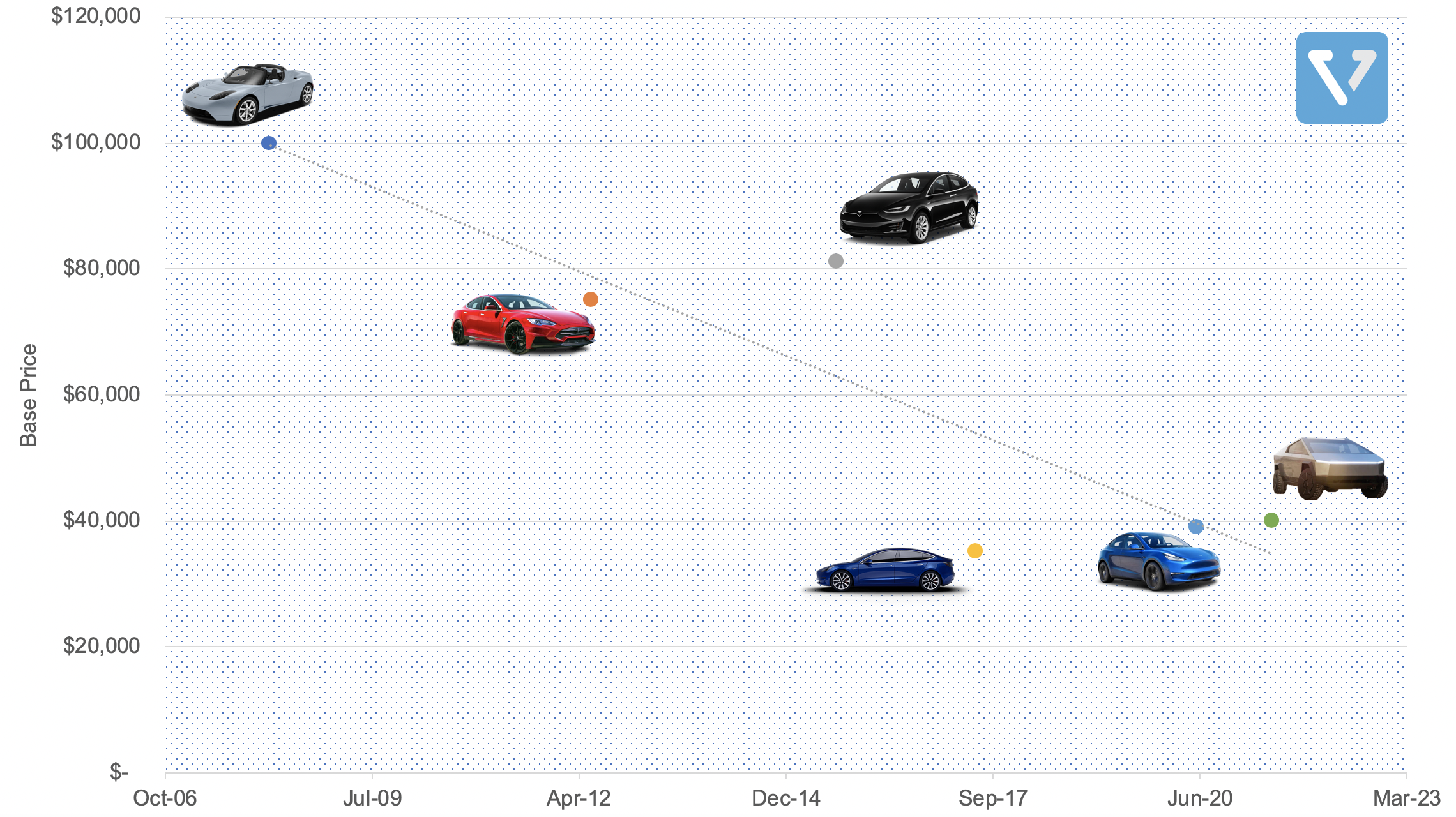

So far the company has stayed on this path (see Figure 1 for the historical journey of the company’s product). After building its first performance roadster, the company then released its first premium sedan – the Model S, followed by the premium SUV – the Model X, and the mass market sedan – the Model 3. In the upcoming years, Tesla plans to release the Model Y (mass market SUV based on the Model 3), the cybertruck, and the new generation roadster.

Fun fact: Tesla’s Models: S, 3, X. Y reads SEXY. The company chose the name ‘Model 3′ (instead of Model E) because it couldn’t get the rights, which is owned by Ford.

Figure 1: Tesla cars’ base price vs. release date

What Tesla has achieved so far cannot be trivialized. As mentioned before, Tesla is the first US car company to successfully IPO since 1956. One of the reasons the company was able to accomplish this is because of two key shifts in the automobile landscape: (1) with the exception of the engine, much of automobile parts manufacturing has been commoditized and can be acquired from 3rd party vendors (windshield, dashboard, suspension, etc), and (2) the electric motor is much simpler to develop than the internal combustion engine. The traditional gasoline power engine has more than 2000 moving parts, while the electric motor that propels an EV has about 20. This means a small startup such as Tesla could develop a powertrain that combined off-the-shelf parts (li-on battery from laptops, chassis from lotus, etc) without breaking the bank.

In this article, we will delve into three key reasons why Tesla has been successful, compare the company’s progress with its chief competitors, and discuss its financials.

Three reasons why Tesla has been successful

There are three reasons why Tesla has been successful thus far. It has (1) superior technology, (2) a supercharger network, and (3) vertical integration. These three factors create a virtuous cycle that continues to extend the company’s lead.

1. Superior technology

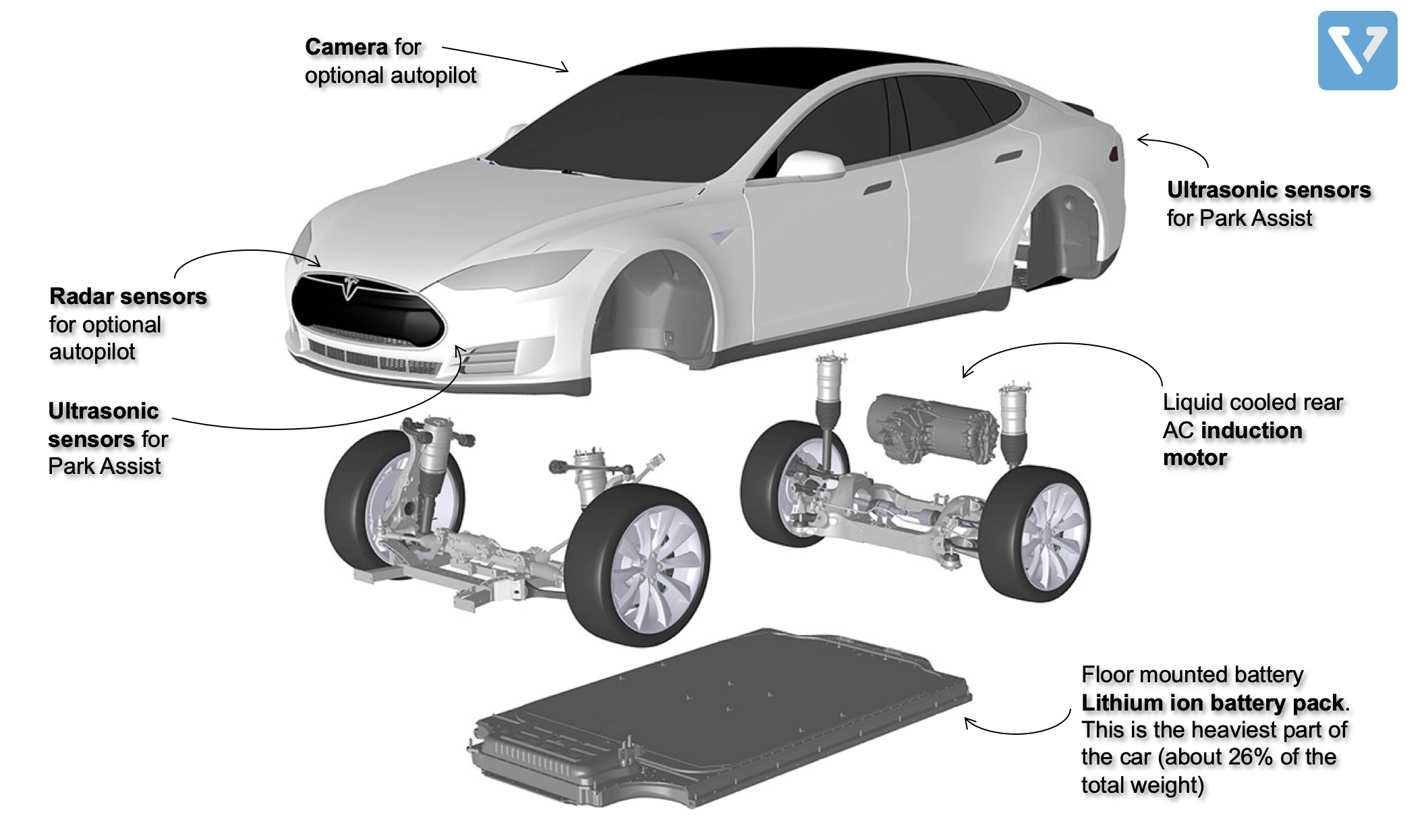

Figure 2: Anatomy of a Tesla

A typical Tesla car can be broken down into three core components:

Electric motor

Tesla’s electric motors are superior compared to the company’s competitors. Tesla motors are equipped with proprietary magnets, making them not only smaller, but also cheaper and more efficient than competitors’. For example, the Model 3’s motor is estimated to cost approximately US $754 (at 46.1 kg), while the BMW’s i3 and the Chevy Bolt, are estimated to cost US$ 841 (at 48.37 kg) and US $836 (at 51.49 kg) respectively. Furthermore, Tesla’s motor also has more torque and better performance.

Battery

Tesla’s energy storage system consists of thousands of individual lithium ion batteries arranged in series. This component is manufactured by Panasonic (ticker: PCRFY) and by far the heaviest part of the car – weighing more than 500 kg. This is why the energy storage system is placed at the bottom of the car to help with stability and handling. Experts in the field consider Tesla’s battery technology to be a couple of years ahead of competitors’. For example, the battery pack in the model 3 is estimated to have 14% better energy density.

Tesla’s superiority in battery does not stop on the technology aspect. The company also has access to the largest battery manufacturing capacity in the world. Since its early days, Tesla has had a close relationship with Panasonic. The Japanese company would produce batteries in Japan and export them to California for Model S and X cars. The two companies have since partnered to make batteries in the US at Gigafactory 1 in Nevada, USA (note that Tesla calls factories that combine battery manufacturing with electric car assembly “Gigafactoriesâ€).

Currently, Tesla has about 44 gigawatt hours (GWh – unit of energy output that represents 1 billion watt hours) of battery capacity. 35 GWh comes from the Nevada Gigafactory 1 (although only â…” of this capacity is currently operational) and 9 GWh is imported from Panasonic Japan. This 44 GWh figure almost exceeds the capacity of all other automakers combined, making Tesla’s production capacity far ahead of its competitors. This gap may increase even further as Tesla is nearing completion of Gigafactory 3 in China and recently announced Gigafactory 4 in Germany.

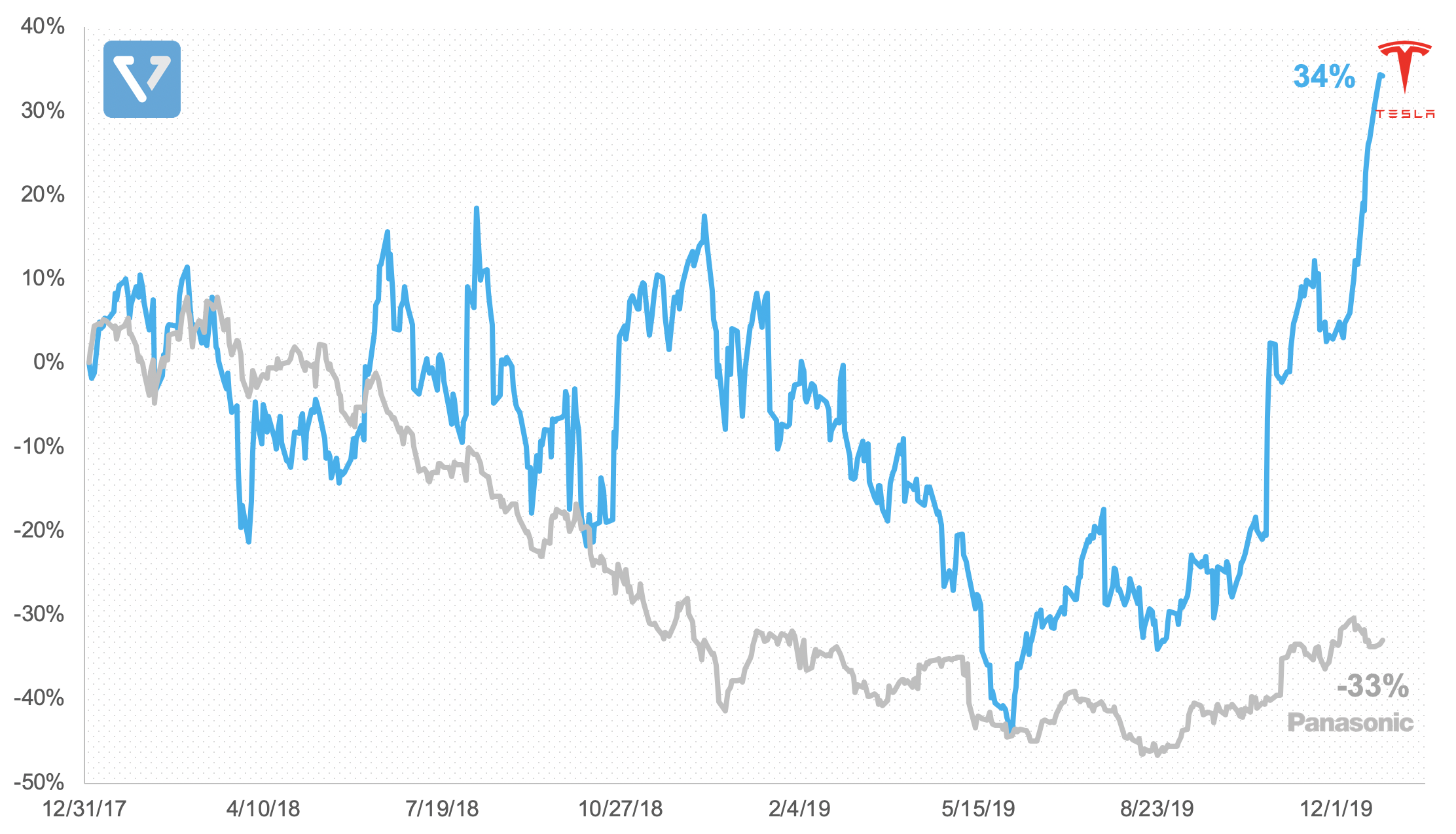

The partnership between Panasonic and Tesla has been rocky in recent months, however. Clashes over management style, engineering issues and battery prices have frayed the relationship. Panasonic’s share price has suffered due to the lack of profitability of the joint venture, dropping by 33% over the past two years, while Tesla’s has increased by 34%.

Figure 3: Tesla vs. Panasonic returns from the past 2 years

As a result of this tension, Panasonic is not participating in Tesla’s Gigafactory 3 construction in China (instead, Tesla has signed an agreement with LG Chem to supply battery for this new factory).

For its part, Tesla needs to continue to increase efficiency and lower manufacturing prices as it introduces new lower-priced vehicles for the mainstream. The company has expanded its partnership with other battery manufacturers, is looking into developing its own proprietary battery, made acquisitions to bolster battery manufacturing capabilities, and may even go into mining to be able to secure raw materials for battery production.

Autonomous driving technology (Autopilot)

Many pundits often discuss the upcoming electric vehicle (EV) revolution in the same vein as the self driving innovation. However, in reality, the two may not be compatible, at least in the medium term. Fully autonomous self driving technology may not be compatible with EVs as the computational power required to run an advanced self driving car (which corresponds to automated driving level 4 – 5) will sap too much energy and will significantly reduce the EV’s range. Currently, Tesla’s autopilot is at level 2.

Nonetheless, it is worth briefly discussing Tesla’s autonomous driving capabilities (when compared to other automakers). Self driving algorithms employ neural networks that require gobs of data to develop – the more data one has, the more robust and accurate the self driving algorithm will be. In terms of driving data, Tesla is only second to Waymo. With more than 10 million miles on the road and 7 billion simulated miles, Waymo has the most driving data. While Tesla, which relies on more than half a million cars using autopilot mode, has recorded 1.3 billion miles.

Despite the quantity of driving data, the quality of Tesla’s data may not be suitable for full autonomy. Tesla took a different approach in developing its autonomous capabilities. Unlike Waymo (and most other players in the autonomous vehicle (AV) industry), which employs high precision GPS, LiDAR and cameras to create a detailed map of the environment, Tesla relies on radar and cameras only. Tesla primarily uses cameras to map the 3D world into the 2D space. It is unclear if this approach will ever work to achieve full autonomy, as it is less accurate.

In a sense, Tesla had no choice. When it first launched in October 2015, the cost of LiDAR was about $75,000, which made the technology too expensive to be deployable in a production car. So Tesla took the only approach that was viable at the time: a camera and radar system, combined with software that can be updated via the internet.

The company has promised full autonomy capabilities by 2020. Take this with a grain of salt, however, as Tesla has a history of overpromising its autonomous capabilities.

2. Supercharger Network

The average American drives 29.8 miles (47.7 km) per day. At first glance, this range is sufficiently covered by an EV. But the average can be misleading. Despite the low average, there are circumstances where the driver drives very long distance – exceeding the range coverage of EVs. As such, about 95% of driving needs can be satisfied by an EV, but most consumers require 100% of their driving needs to be met (including long distance trips 1-2 times per year). The fear of not being able to drive long distance using an EV is called range anxiety, and is the number one reason consumers cite to be the barrier to adopting EVs on a wider scale.

Recognizing this, Tesla has developed a network of superchargers. Superchargers are electric charging stations that can fast charge (50% charge in about 20 minutes) Teslas. They use a proprietary connector, which means other EVs cannot use Tesla’s network.

Although requiring significant capital investment, Tesla’s supercharger network provides the company a competitive advantage. No other EV makers have a charging network. While Tesla has floated the possibility of opening its supercharging network to other car makers, no specific plans have been announced.

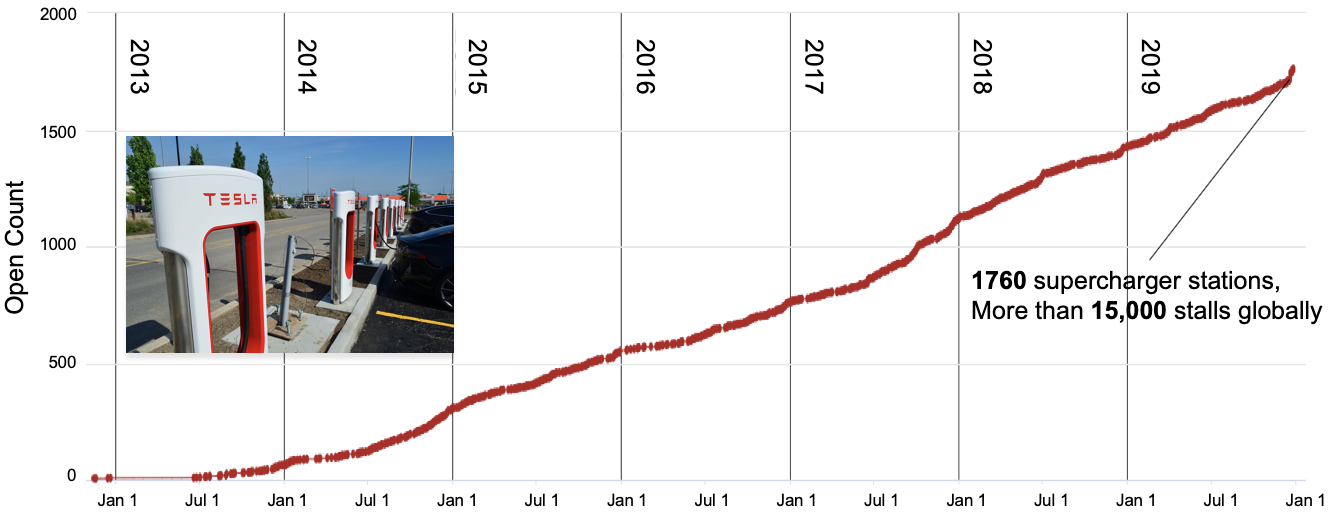

Since 2012, Tesla’s supercharger capabilities have increased from just a handful in large US cities, to more than 1760 stations (Figure 4), with more than 15,000 stalls in 37 countries (59% of these are located in the US and China).

Figure 4: Tesla’s global supercharger network. Data is taken from here source

It costs Tesla an estimated US $270,000 per station (costs may vary depending on various circumstances). At close to 1800 stations, this suggests that Tesla has invested approximately US $486 million on its supercharger network thus far. Although a large amount, this represents a small portion of the company’s capital expenditure. In 2019 alone, Tesla expects to spend US $1.5 billion in capital expenditure for R&D, manufacturing expansion and building out its Supercharger network.

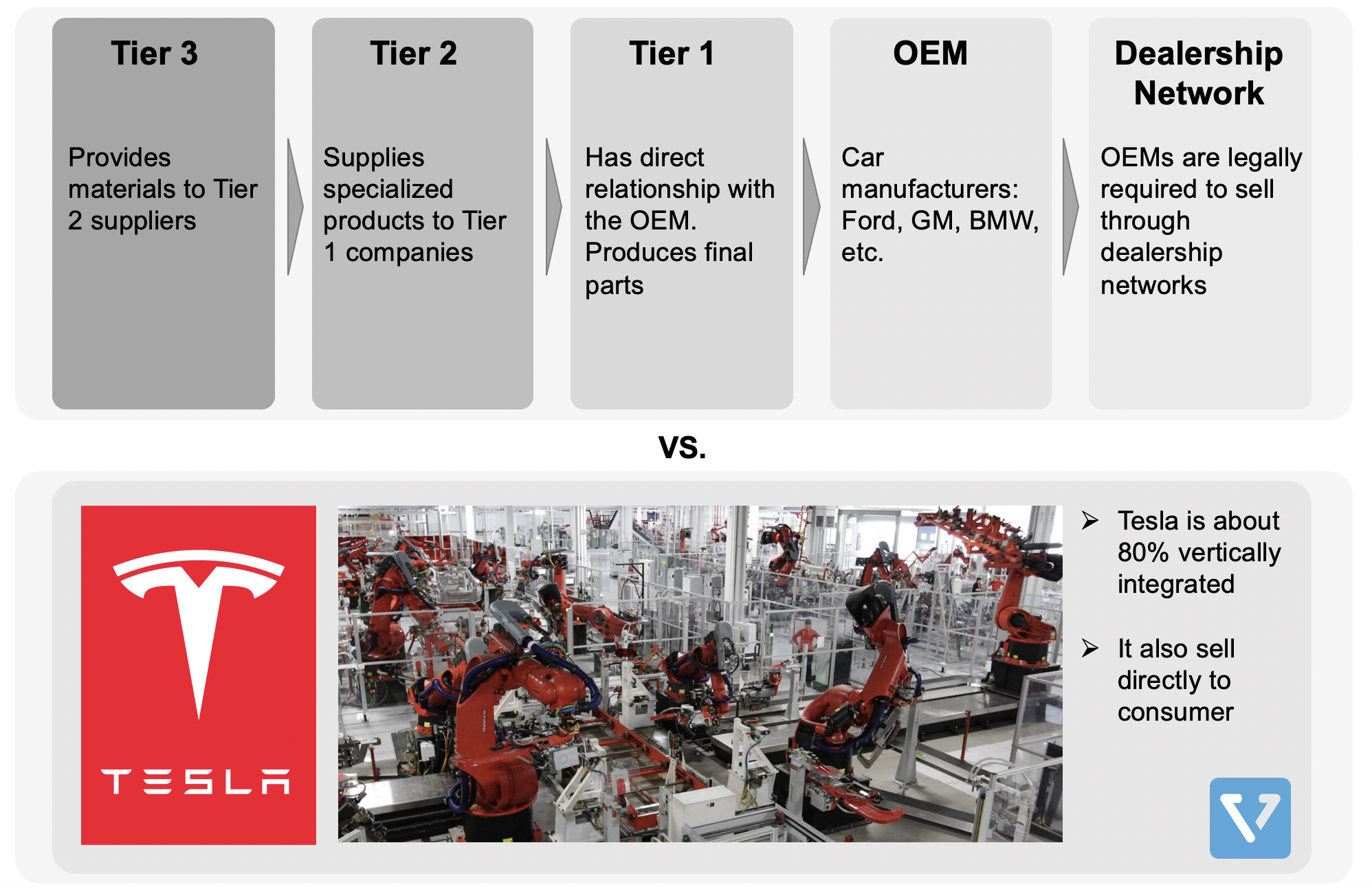

3. Vertical Integration

Tesla’s organizational structure and its approach to vertically integrate where possible are what make its technology superior. Unlike other car companies, Tesla develops and produces most of the core components in-house. In contrast, established car companies (OEMs) such as Ford, GM and others have an ecosystem of third party suppliers that comprise of three tiers (Figure 5). This makes fast technology innovation and iteration difficult.

Figure 5: The multi-tiered supply chain of the traditional car maker (OEM) vs. Tesla’s vertically integrated structure

A recent report by Goldman Sachs estimates that Tesla has achieved about 80% vertical integration in its manufacturing supply chain. The company’s innovations range from its supercharger network and custom software, to novel methods to produce the frame of the car.

The primary benefit of vertical integration is not to profit from the margin you would otherwise pay your suppliers, but rather to enable a much faster rate of innovation and technology development.

This is why the company decided to open source its technology patents. Tesla did not do this for altruistic reasons (despite what its PR department would say) – the move is strategic in nature.

To grow even faster, Tesla needs to move electric vehicles to the mainstream (as of 2018, EV penetration in the US is at about 3.4%) – and the fastest way to do this is to have other car manufacturers produce electric cars as well, so that when consumers are shopping for EVs, they compare others’ electric cars with Tesla’s, which the company believes is best in class.

With its ability to innovate faster, Tesla has the confidence that it can out innovate its competitors.The company also has the largest automotive battery manufacturing capacity along with the most extensive charging network.

Tesla’s vertical integration is not limited to technology development – but also to the manner it sells to customers. In the US, all other car companies rely on a franchise distribution model, but Tesla never opted into this model. When selling through a franchise model, a car maker sells its cars through a 3rd party that then sells to the end consumer. In almost every state in the US, there are laws that prohibit car makers from selling directly to consumers once they have established the franchise model. The goal of this law is two-fold: (1) protect the franchise owner from unfair competition from the car makers, and (2) protect the public from unfair practices by the car makers.

Although the laws were established to protect the consumer and the public, it has been used to protect the rights of the dealers/franchise owners and block direct car sales to consumers. Once a car maker opts into the dealership model, they cannot bypass the franchise. For the car maker to go directly to the consumer, they have to repurchase the rights from the franchise owners; and for established car makers, this is prohibitively expensive.

Because Tesla has never gone this route, it can go directly to the consumer. This means that (1) Tesla can capture more of the profit margin as there is less middlemen in the distribution network, (2) Tesla has control on the customer purchasing experience, an important fact considering 87% of Americans dislike the traditional car buying experience, and (3) Tesla can sell its cars online.

Tesla’s direct path to the consumer is not without its controversies, however. The company has faced multiple legal disputes in multiple US states. Some states have not only banned Tesla from selling directly in stores, but also banned Tesla service centers. To circumvent this in states that have strict dealership laws, Tesla has established showrooms – store fronts that showcase Tesla cars where transactions cannot occur and employees are not allowed to talk about pricing or financing options.

Tesla’s progress compared to competitors

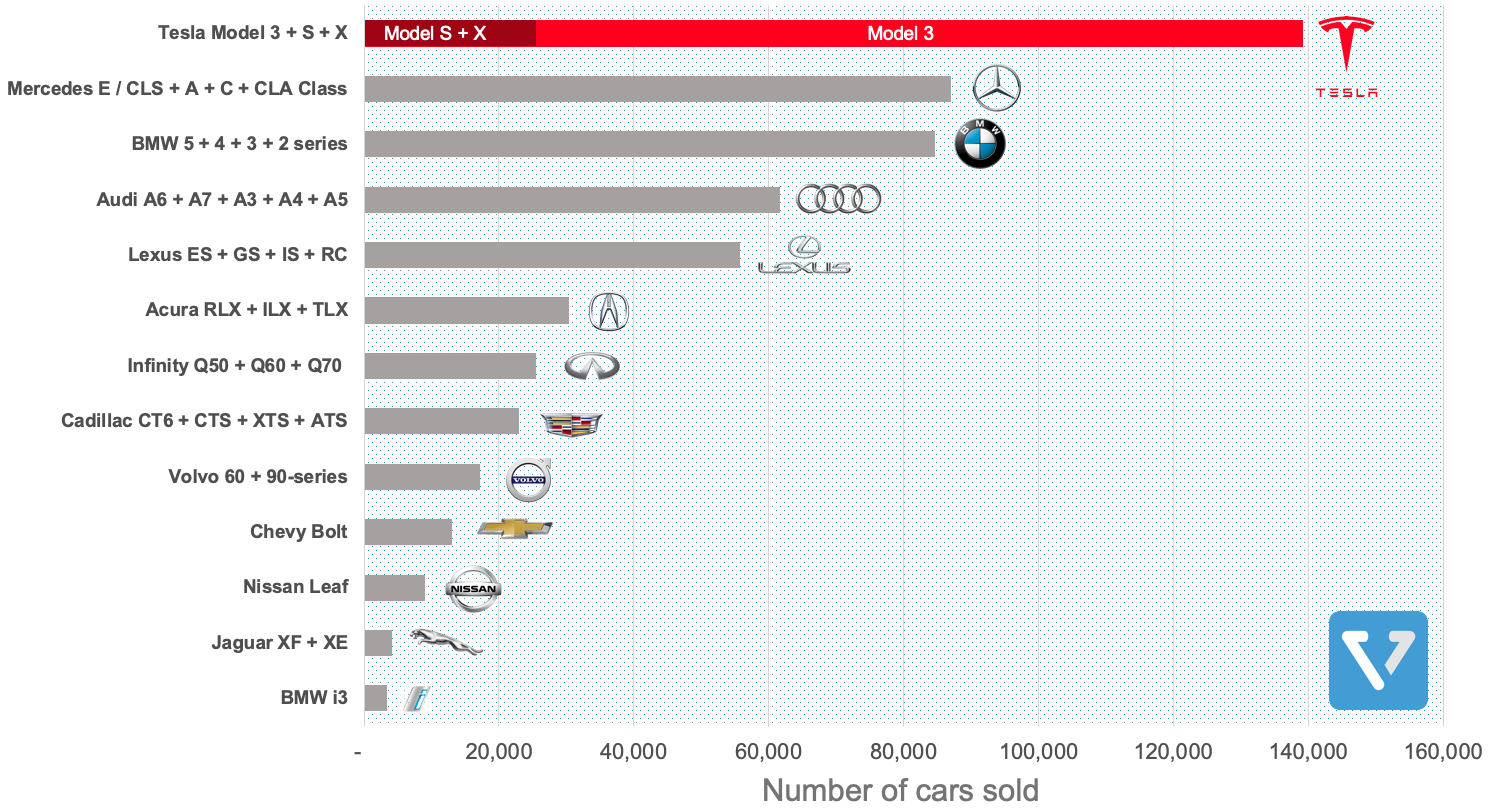

Figure 6 shows the number of cars Tesla has sold (delivered) in the US from January to September 2019, compared to that of other small to midsize luxury cars and electric cars made by other car makers.

Figure 6: Total number of small and midsize luxury cars sold in the US from January to September 2019. Midsize premium car sales data. Small premium car sales data . Tesla’s car deliveries data are taken from the company.

Between Q1 to Q3 2019, Tesla sold almost 140,000 cars in the US. That is more than the venerable Mercedes, and 10x more cars than GM’s Chevrolet Bolt (the second best selling EV in the US in 2019). Tesla is not only outselling other EVs, but other premium cars by a significant margin. Tesla claims that the Model 3 is addressing a market larger than initially thought. More than 60% of Model 3 trade-ins are non-premium brands. This seems to be backed by a survey from Bloomberg that shows that most buyers traded in vehicles in the price range between US $20,000 – 40,000 (vs. average Model 3 selling price of US $50,528).

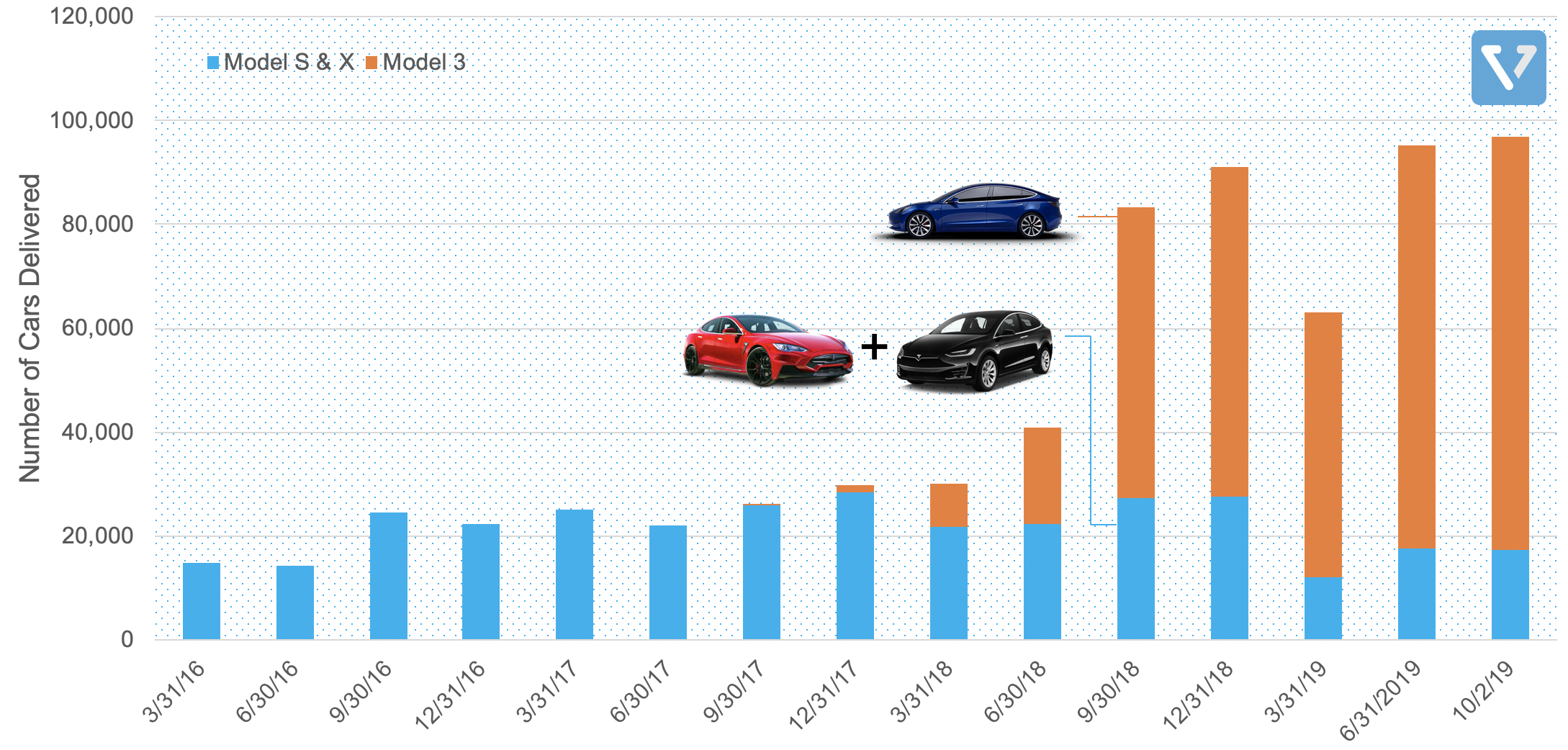

In Figure 7 you can see Tesla’s quarterly car delivery numbers. The number of delivered cars is an important metric for Tesla, as it is a leading indicator for revenue. After the launch of the Model 3, the company’s car delivery numbers increased significantly, while sales of the premium models, Models S and X, have decreased in 2019. This might be because Model 3 is cannibalizing sales of the more expensive models. In Q3 2019, Tesla’s product mix comprised of 80% Model 3 and 20% Model S and X.

Figure 7: Tesla global car delivery numbers by the quarter

Note: There was a significant dip in vehicle deliveries in Q1 2019 as Tesla was experiencing production issues that hampered its ability to produce cars at a sufficient pace.

To maintain profitability, Tesla must continuously increase efficiency and reduce costs. As part of this effort, Tesla is expanding its manufacturing capacity. The company is near completion of Gigafactory 3 in Shanghai (which will produce cars that are 50% cheaper per unit capacity than existing production lines). The factory was completed in record time, and Tesla plans to begin delivery in China in January 2020. Tesla expects China to be the largest market of its Model 3, as the market for premium mid-size sedan in China is far larger than that of US.

Building 1,000 cars is hard. Building 100,000 cars is exponentially harder. Despite all its successes, the company has stumbled time and time again mastering the operational complexities of manufacturing at a large scale.

- Quality issues: In Q3 2019, Consumer Report (a non profit dedicated to unbiased product testing) no longer recommended Tesla’s cars due to production quality issues. The quality issues seemed to be worse during periods when the company’s production capacity was stretched thin due to commencement of overseas exports. Surprisingly, despite the problems, Tesla Model 3 still receives very high consumer satisfaction ratings. It seems the company is making progress on fixing these issues.

- Service issues: Amid a significant increase in vehicle sales, Tesla’s sales and services suffered as they were unable to meet deliveries or complete services in a timely manner. Unlike Ford, which has more than 5000 dealerships (and many more independent mechanics that can service a Ford vehicle), Tesla only has 413 service centers worldwide.

- Manufacturing stumbles: Tesla has a history of missteps when designing its production line architecture. One example of this was when it tried to over-automate the assembly process of Model 3. These missteps are not only costly, but have caused the company to miss vehicle delivery deadlines and as a result, their share price to tumble.

Tesla’s Financials

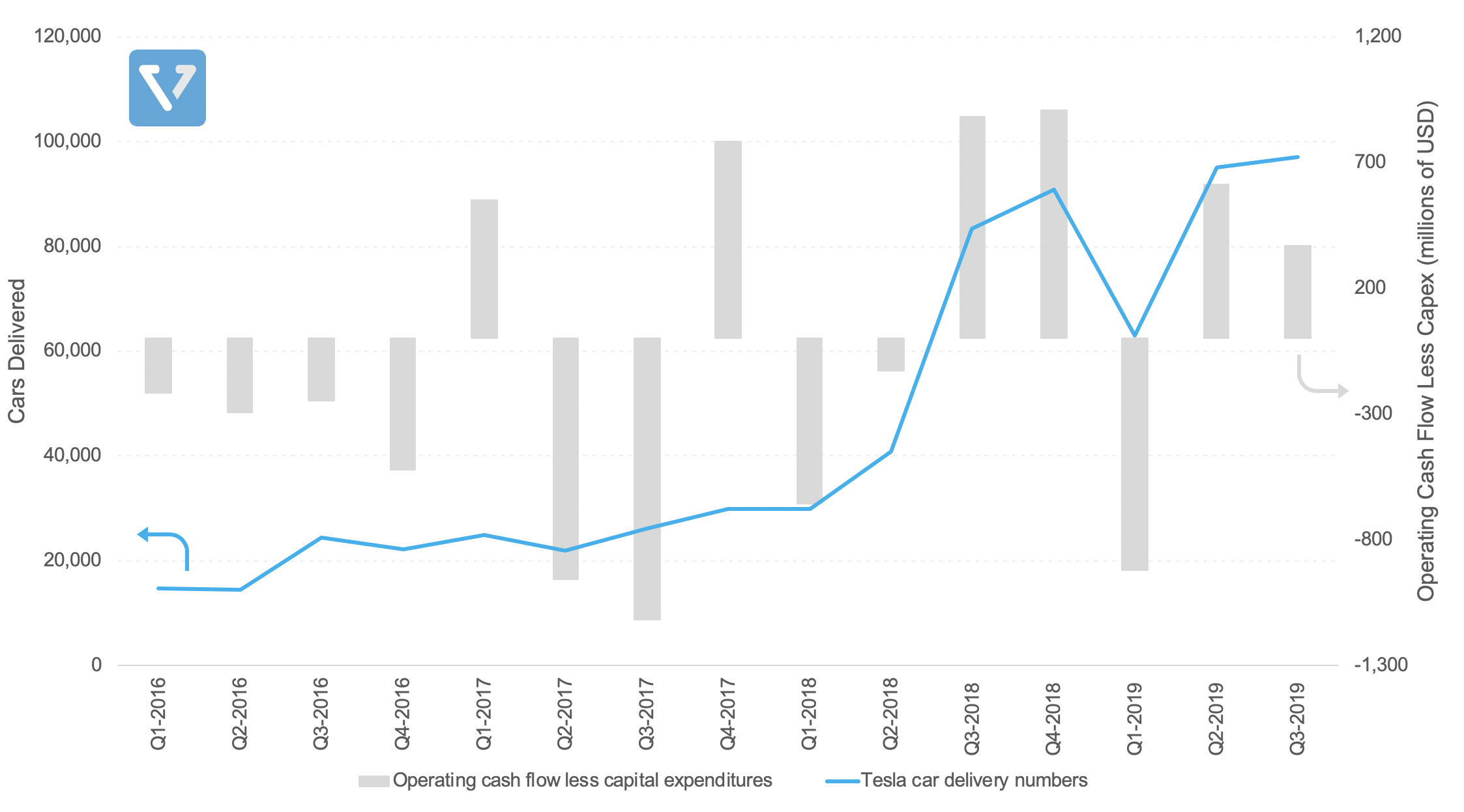

Making the cars is one problem, being able to execute in a timely manner while maintaining liquidity is another. Currently, Tesla’s largest risk is likely execution risk. Can the company overcome production issues and deliver cars in a timely manner to generate cash and recoup its large capital expenditures?

In Figure 8 below, Tesla’s quarterly car delivery numbers are plotted vs. free cash flow (quarterly operating cash flow less capital expenditures). As you can see, the car delivery numbers can significantly affect Tesla’s cash reserve. Liquidity is an important factor for Tesla as it prepares to ramp up production facilities in Shanghai and Germany and launch new lineups (Model Y).

This is the reason why car delivery numbers are closely watched by investors. In Q1 2019, Tesla missed its delivery target by a large margin, and the share price tumbled.

Figure 8: Quarterly Car Deliveries (blue line) vs. Operating Cash Flow Less Capex (millions of USD)

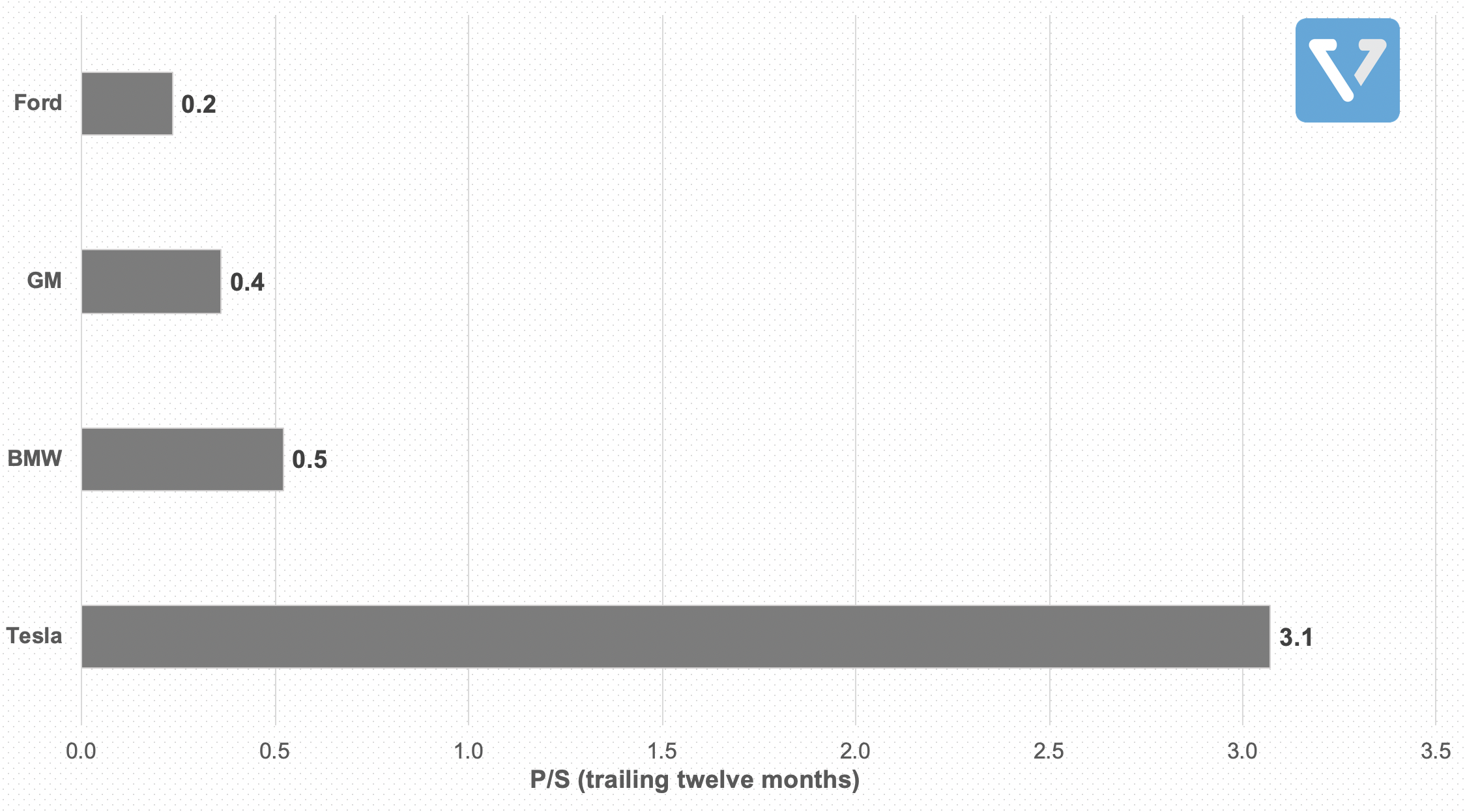

When compared to other car companies, Tesla’s valuation is much higher. You can see the company’s trailing twelve months Price to Sales ratio in Figure 9 (we use the P/S ratio – market cap over revenue – instead of P/E ratio since Tesla has not consistently generated profits yet). Tesla leads the pack at 3.1, while established car companies such as BMW, GM, and Ford are significantly lower.

Figure 9: Tesla’s P/S (TTM) compared to other car makers

The market is evaluating Tesla as a growing tech company, rather than a traditional auto maker. In the past 3 years, Tesla shares have returned 81%, higher than BMW, GM and Ford that have returned -15%, 1.3%, and -20% respectively. In fact, the company’s returns beat the Nasdaq composite, which returned 62% over the same period.

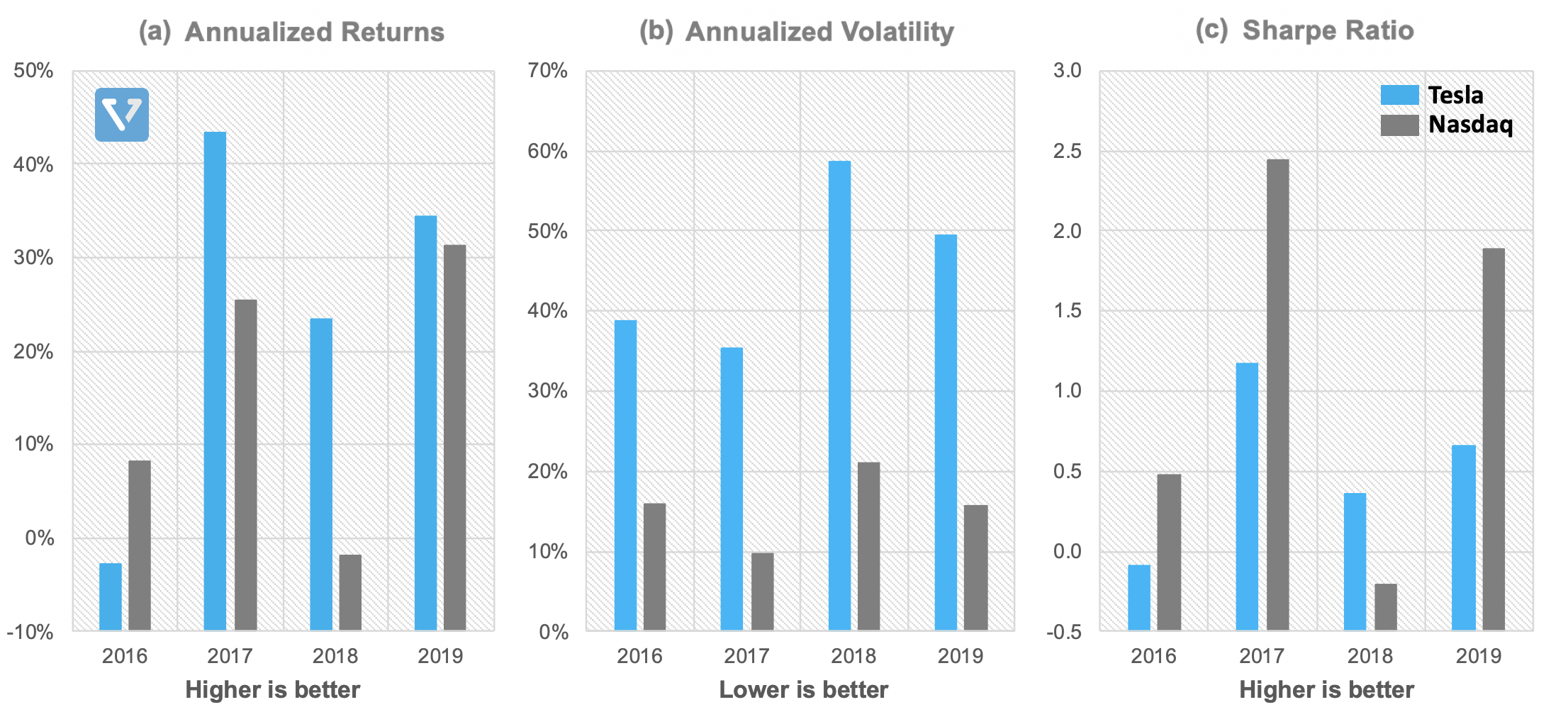

However, high growth is accompanied by high volatility. Figure 10 summarizes Tesla’s annualized returns, annualized profitability, and Sharpe ratio, and compares them to the broader Nasdaq index over the same time period. As you can see, Tesla’s return outperformed that of Nasdaq (Figure 10 (a)) in the last 3 out of 4 years, but Tesla’s volatility (Figure 10 (b)) is much higher, ranging from 2 – 4X more volatile than the Nasdaq depending on the year. As a result, Tesla’s risk adjusted return (Sharpe ratio) is generally much lower than Nasdaq (Figure 10 (c)).

Figure 10: Annualized return (a), annualized profitability (b) and Sharpe ratio (c) of Tesla over the last four years vs. Nasdaq’s. The 6 month T-bill at the end of each year was used as the risk free return when calculating the Sharpe ratio.

Investing in Tesla is not for the faint of heart. Thus far, the company has beaten the odds and built superior technologies, created an organization that out-innovates incumbents, all while building large scale manufacturing capabilities. And yes, the EV market is projected to increase exponentially in the upcoming decades, as we transition away from internal combustion technology. However, the margin for error for Tesla is small. Currently, the expectation for the company is so high that it propels the share price to record highs. Any problems in production, issues with car deliveries, or missed sales estimates will result in significant drop of the share price. This is why often times Tesla’s share is very popular among short sellers (investors who bet that the company will underperform).

Now that you have a good overview of Tesla’s differentiated strategy. Read more about how to easily invest in Tesla from India.

[mc4wp_form id=”1064″]