Skip to content

Skip to content

The backstory:

Both Uber and Lyft (Uber’s primary competitor in the US) have submitted paperwork for their confidential US IPO filing this week. This means that both companies are likely to go public in the next three to four months, depending on market conditions (they can still cancel, but backing out of an IPO gives a negative signal to the market). Uber’s IPO is expected to be one of the biggest of all time hitting a valuation of US $120 billion. In this week’s post, we will dig a little deeper into Uber’s numbers and different business lines to see if the valuation is justified.

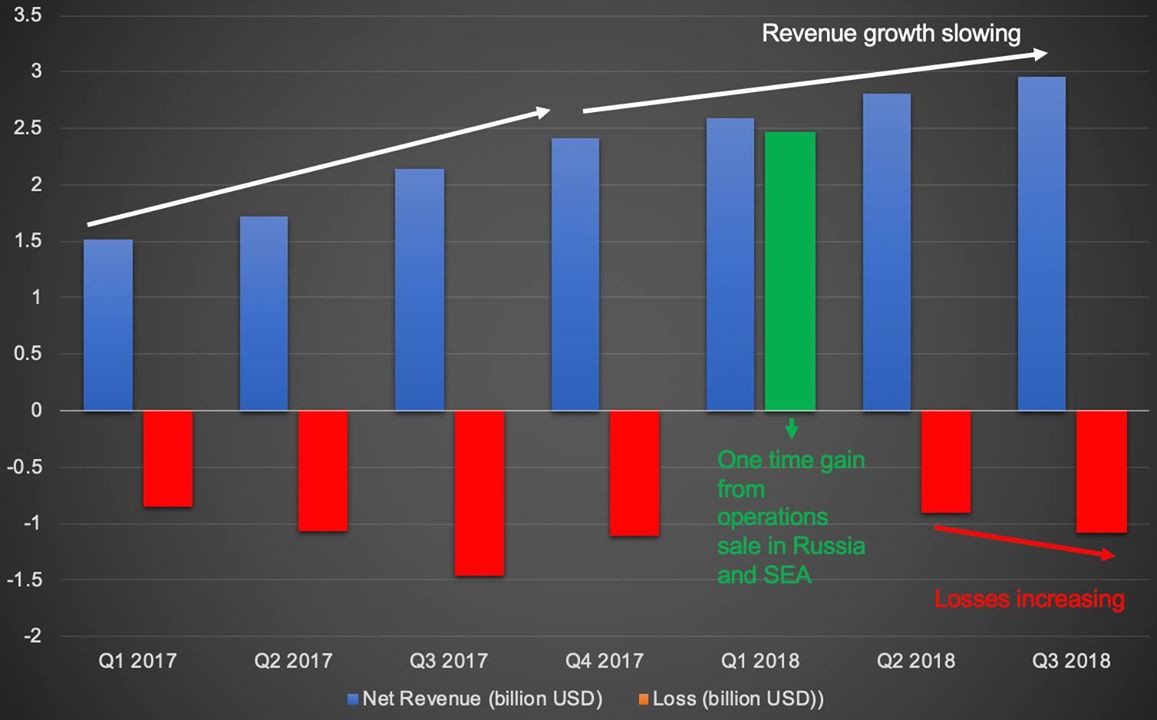

Figure 1: Uber’s financials adapted from WSJ

Uber by the numbers.

Unlike most private companies, Uber has been releasing (unaudited) financial numbers to its investors. As you can see in Figure 1 above, in Q3 2018, Uber made US $2.95 billion dollars in net revenue (Uber’s share of the income minus revenue sharing, costs and taxes). It is also evident from the plot that the rate of increase in revenue is slowing down. This is because the ride sharing market in the US is becoming saturated and due to the fact that Uber is retreating from unprofitable markets in other parts of the world (it sold its operations in Russia and Southeast Asia to local players netting US $2.5 billion positive cash flow in Q1 2018). Nonetheless, one key driver of Uber’s revenue growth is Uber Eats.

Uber Eats is growing fast.

In Q2 2018, Uber’s food delivery business (Uber Eats) represented 10% of its gross bookings, or approximately US $1.2 billion; and in , it delivered US $2.1 billion in gross bookings (or 17% of total gross bookings). Net revenue contribution from Eats is unknown at this point.

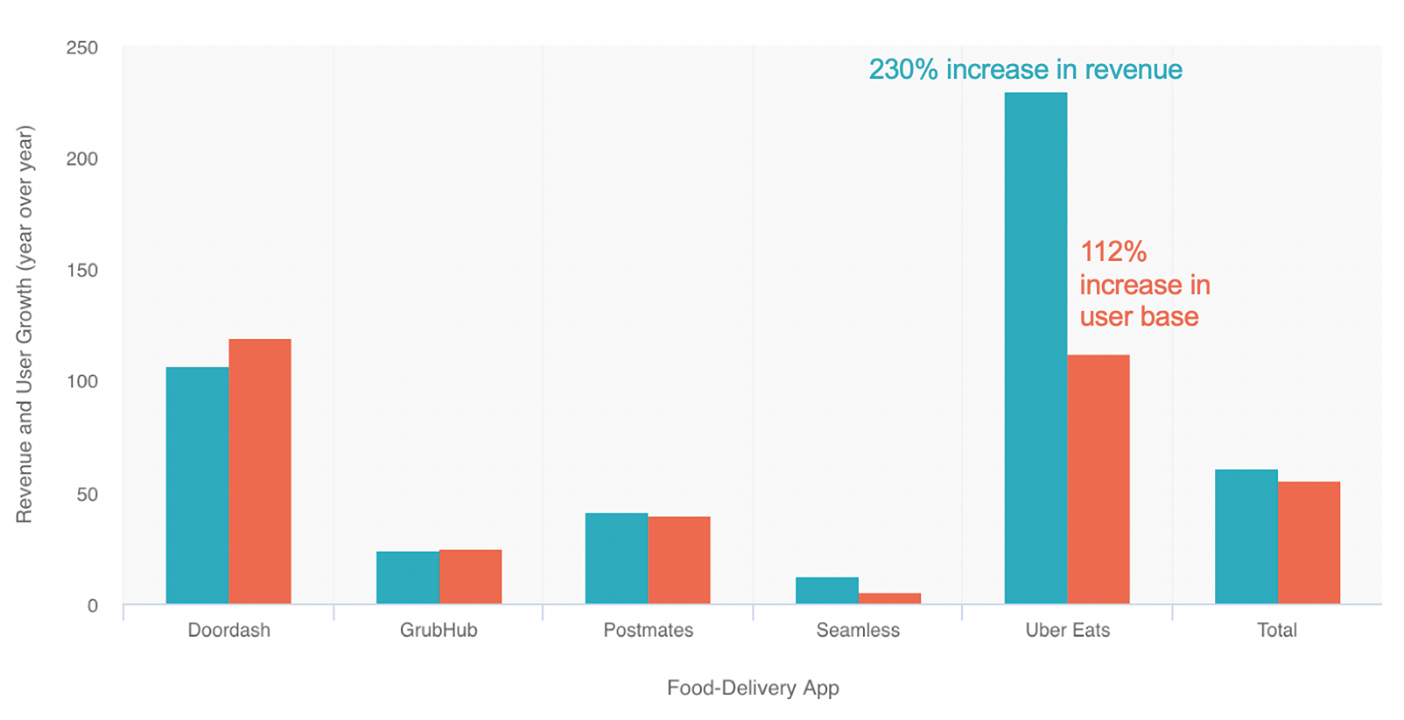

Figure 2: Uber Eats revenue vs. other food delivery services

The worry is that, although Uber Eats delivers top line revenue growth, the business is less profitable than the ride sharing business line. It is still too early to make this judgement however, as Uber Eats is still experiencing an uber (pun intended) growth phase fueled by generous subsidies. From April 2016 March 2017, Uber Eats experienced more than 230% growth in revenue and 112% increase in user base, outpacing the growth of other food delivery services in the US, with the average user spending US $220 per year on the service. See Figure 2 above for comparison of Uber Eats revenue with other food delivery services in the US. Data adapted from here.

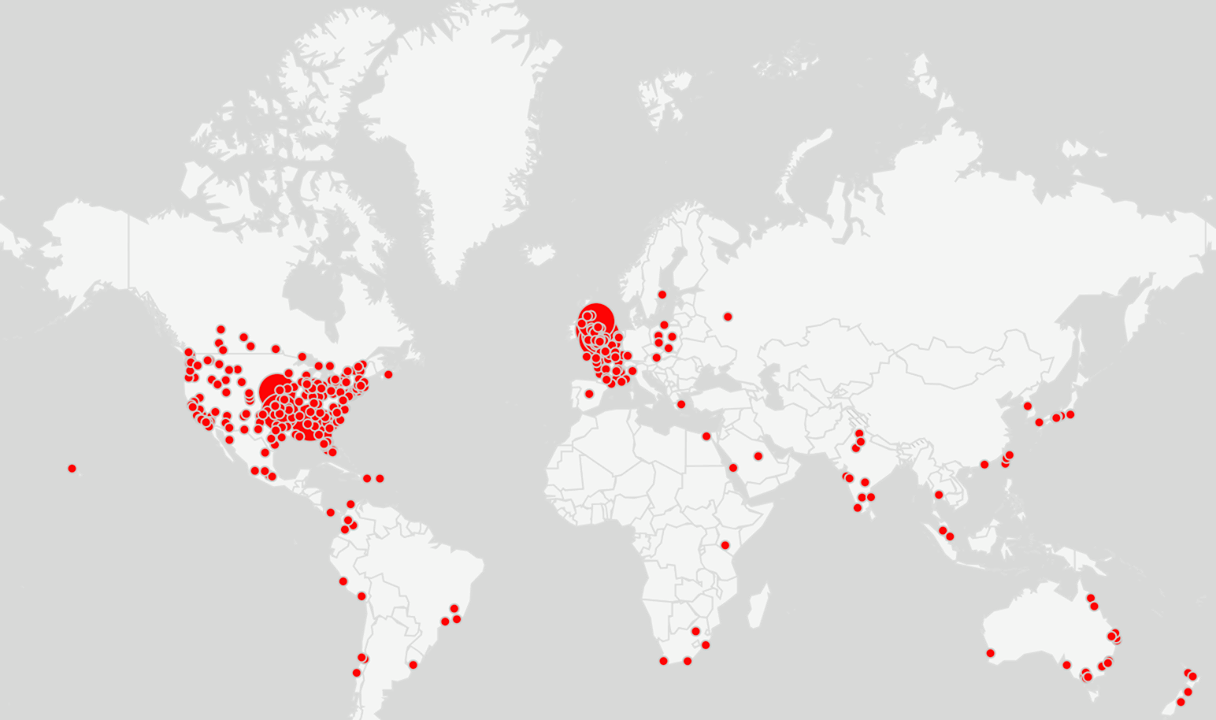

Figure 3: Area coverage of Uber Eats

The service is now global, operating in 378 cities in five continents and is valued at US $20 billion (See Figure 3).

Uber is also expected to enjoy valuation growth due to its ownership stakes in other giant ride hailing companies. The company acquired these stakes when it sold its operations in China, SEA and Russia:

- China: In August 2016, Uber retreated from the country and sold its operations to its chief competitor Didi. As a result, Uber acquired 17.7% of economic interest in Didi. As of July 2018, Didi is valued at US $56 billion, giving Uber’s stake a value of almost US $10 billion (and likely growing fast as Didi has recently expanded internationally).

- Russia: In July 2017, Uber merged its operations in Russia and several other countries in the region with Yandex. As part of the deal, Uber gained 36.6% ownership stake of the new entity. The stake was valued at more than US $1.4 billion at the time of the transaction.

- Southeast Asia: In March 2018, Uber retreated from the region and sold its operations to Grab. In exchange, Uber acquired 27.5% ownership stake of Grab. At the time of the deal, Grab was valued at US $6 billion. This gave Uber’s stake a value of US $1.7 billion. Grab’s valuation is sure to grow, as it is the leader in ride sharing in the region and also a provider of financial services, insurance and micro loans.

In addition to its B2C businesses above, Uber is expanding into B2B (business to business) as well:

- Uber for Business: An all in one integrated solution to manage billing, expensing, reporting, and real time tracking of rides. Uber sells this service to businesses to help manage their own transportation needs. For example, a hotel can use Uber for Business to manage its shuttle service to the airport, or an insurance agency can use the platform to manage travel of its employees.

- Uber Freight: Uber Freight leverages Uber’s platform to match truck drivers with shippers. With this new business line, the company is expanding into the long distance truck delivery business.

- Uber Health: Similar to Uber for business, Uber Health is a transportation solution that Uber has created specifically for health providers/clinics to provide non emergency patient transportation. It allows for future ride scheduling and is HIPAA compliant (protects privacy of the patient).

The company is transforming itself to go beyond car sharing. It wants to be your integrated transportation solution. To that end, it is also investing in scooter and bike sharing, self-driving vehicles, flying cars, and is partnering with transit networks (trains and buses so that you can purchase your fare through the app):

- Uber bought an electric bike sharing company (Jump) for about US $200 million. At the time of the acquisition, Jump had an average of four trips per day per bike, at an average distance of 2.6 miles (4.2 km). This would cost the user approximately US $2/ride. As such, electric bikes fill in the gap of short distance travel that may cannibalize Uber car rides. Additionally, the company is in talks to potentially acquire either Lime or Bird. Both are leading scooter and bike sharing platforms.

- Through its partnership with Masabi, Uber now allows users to buy public transit tickets through the app.

- The company also invests in self-driving car technology. Over the last 18 months, Uber has invested anywhere between US $125 US $200 million in autonomous vehicle research, and the company has recently hired a former federal US auto safety officer to its self driving team.

- On top of all the above, Uber is also developing a flying car platform, called Elevate.

Ok, phew. That was longer than I intended. It is clear that Uber has global ambitions and is expanding beyond its core car-based ride sharing business. But is the US $120 billion justified?

Currently, Uber is on a ~US $12 billion net revenue run rate in 2018, and is valued at US $72 billion (as of early 2018) giving it a 6X net revenue multiple. If Uber can increase its revenue by 40% in 2019 (which should be a reasonable number since it increased its net revenue by 50% in 2018), then the company can hit close to US $16.8 billion net revenue, or a US $100.8 billion dollar valuation (applying the same 6X multiple), giving a total of 100.8 + 10 (from Didi) + 1.4 (from Yandex) + 1.7 (from Grab) = US $114 billion valuation. Note that this back of the envelope math does not include the increase in value of its stake in other global ride sharing companies. Looking at it this way, it does not seem that the US $120 billion dollar valuation is too far fetched.

Note that the numbers and valuations presented here, at best are rough approximations, as Uber and its subsidiaries are private companies they do not report audited numbers, and valuation of private companies is difficult to accurately assess. Nonetheless, Uber’s is the IPO to watch in 2019. Final valuation determination will be made by public investors, after assessment of the company’s financials is performed, which can only happen a couple of weeks before the official IPO date.

At Vested, we enable you to invest in US-listed companies. Once Uber is publicly listed, you can invest in the company through our platform. Sign up at https://vestedfinance.com to get the latest updates regarding our platform launch.