Skip to content

Skip to content

The Roblox IPO and the vertical gaming social media

Reed Hastings, CEO of Netflix once said that they compete with a broad set of competitors, from Facebook, Youtube to Disney and Fortnite, to get users’ screen time, and more often, they lose to gaming than to other streaming providers.

In the landscape of media consumption, gaming is often categorized as a separate segment. But, as we have written before, gaming is big business and competes directly with other media consumption for consumers’ time. In fact, most consumers under the age of 45 prefer to play video games than passively consume TV/Movies.

With the 2020 tailwind behind them, and after a pulled IPO (the company was supposed to go public last year), Roblox went public last week via direct listing.

What is Roblox?

Roblox is a very interesting company. It’s part gaming platform, part user generated social media, and part digital marketplace. Here’s a snippet about the company from its S-1 (bold areas emphasized by us).

“An average of 36.2 million people from around the world come to Roblox every day to connect with friends. Together they play, learn, communicate, explore, and expand their friendships, all in 3D digital worlds that are entirely user-generated, built by our community of nearly 7 million active developers. We call this emerging category “human co-experience,†which we consider to be the new form of social interaction we envisioned back in 2004. Our platform is powered by user-generated content and draws inspiration from gaming, entertainment, social media, and even toys.â€

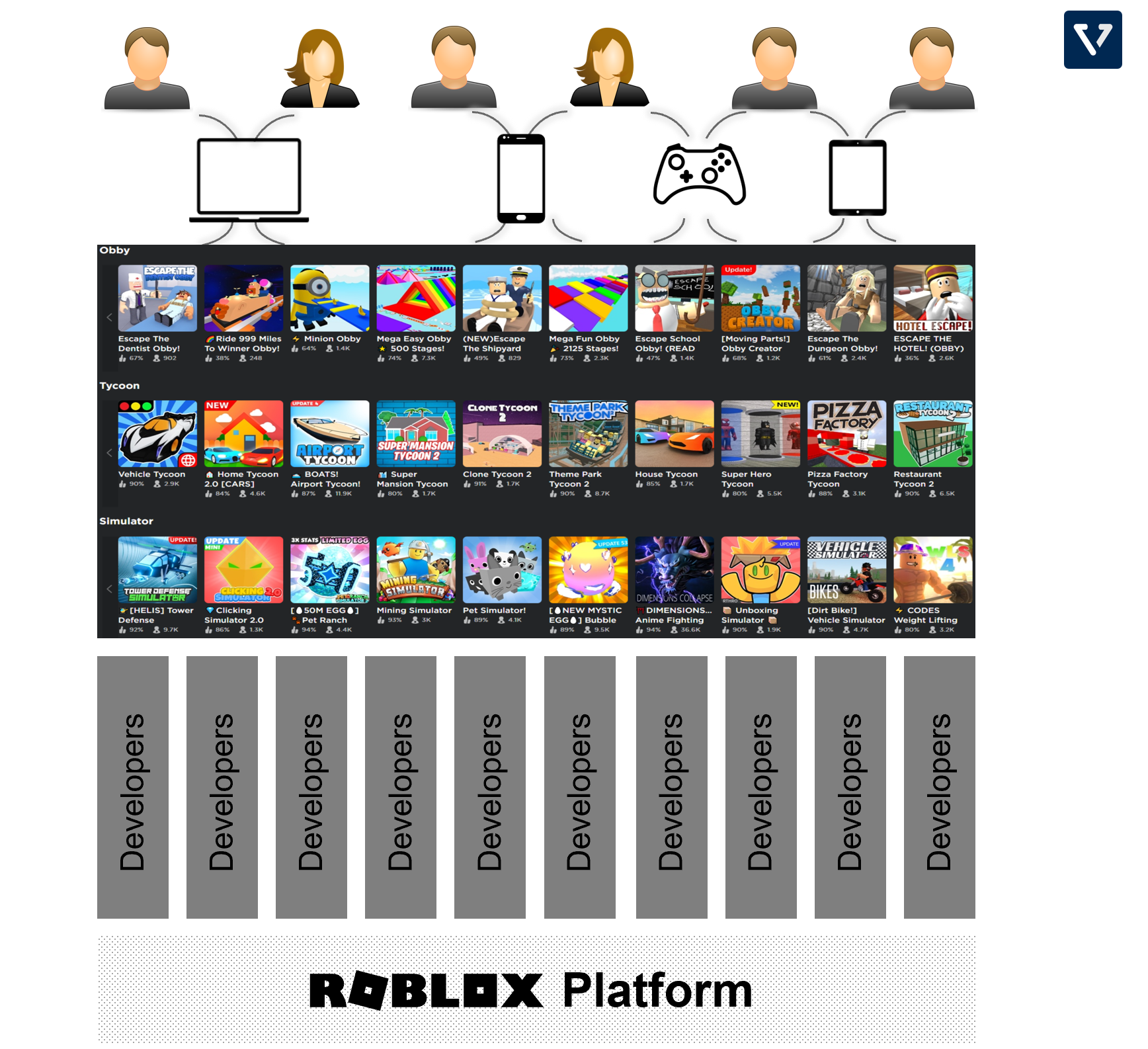

The ecosystem that Roblox is trying to build is often called the metaverse. It is a collection of persistent, shared, 3D virtual spaces in a virtual universe. Here’s an illustration of the Roblox metaverse:

- Players can access the Roblox metaverse from any device capable of running the Roblox client (although most players use it via their smartphone, which has profound impact on profitability – more on this later).

- Players can create their own digital avatars that they can equip with various digital accessories that persist throughout all the games (you can use the same avatar, wearing the same accessories, across multiple games).

- Players can choose various experiences (games) that are developed by multiple independent developers.

How does Roblox make money

Roblox operates a two sided marketplace:

- On one side, you have players, who spend USD and buy Robux (the platform’s digital currency. For US $0.01, players get 1 Robux), to buy everything from experiences (games), digital items (hats, clothes, accessories), to even emotes. Players can even subscribe to a premium membership, which generates recurring revenue for the company.

- On the other side, you have developers who earn Robux for creating games, digital items and even tools to sell to other developers. Developers also earn Robux based on engagement metrics. The Robux that these developers earn can be exchanged to USD at a rate of US $0.0035 per 1 Robux (or 2.9X lower than what the players get).

As you can see, Roblox generates revenue from USD to Robux conversion at a pretty large bid-ask spread. The company also takes a cut for every transaction that occurs on the platform:

- When a player buys experiences or digital items, for every Robux spent, the company takes a 30% cut. The developer receives the remaining 70%.

- When a player spends Robux in the Avatar Marketplace, the company takes 70% cut, giving the creator the remaining 30%.

In essence, Roblox operates a metaverse and generates revenue from two primary sources: (1) USD to Robux conversion and (2) the company takes a pretty hefty tax on the commerce that happens within.

So, here is what the network effect looks:

- The more people participating in the metaverse, and the higher their engagement, the more they spend.

- More players attract more developers to the platform.

- Which results in more experiences/games to attract more users.

- Which allows the company to further monetize via ads.

- All of the above translates to more transactions within the platform, generating more revenue.

Metrics that matter for Roblox

Because the activities in the platform are fundamental to strengthening its network effect, as is with a social media company, engagement is a metric that we need to follow closely.

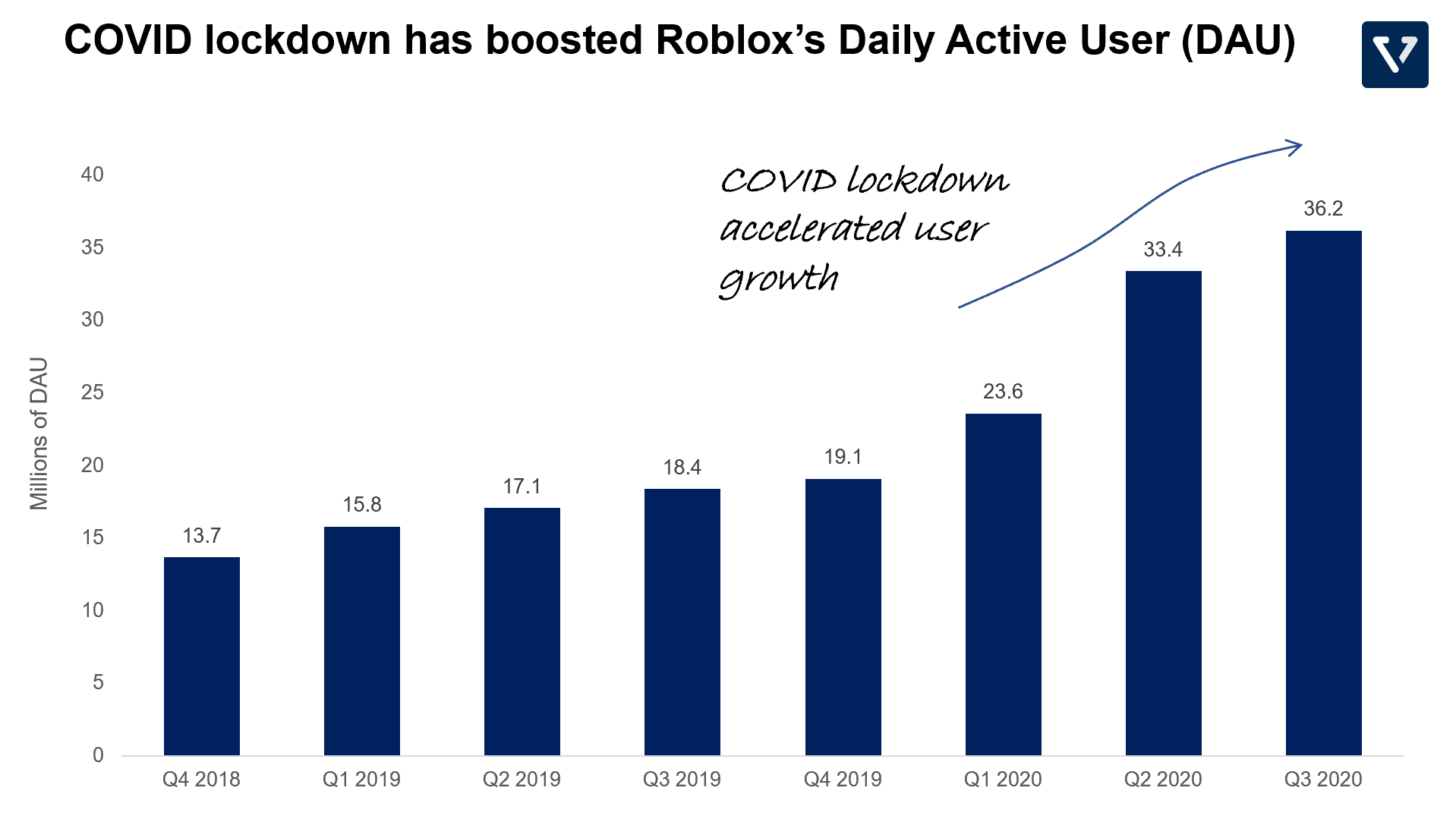

Number of users is growing rapidly. As is with many other digital platforms and social media companies, the number of Daily Active Users (DAU) grew rapidly in the second half of 2020 due to the global lockdown. The number of DAU increased by 97% in Q3 2020 from the same period in the preceding year (Figure 2). This is about 5X smaller in number of DAU than that of Twitter.

Nevertheless, Roblox has a higher engagement rate compared to other social media platforms. On average, the average user spends about 2.6 hours per day on Roblox, which is more than 2X higher than the average time spent on a typical social media platform. But Netflix is still king in terms of the number of hours users spent on the platform. On average, a Netflix user spends about four hours per day on the platform.

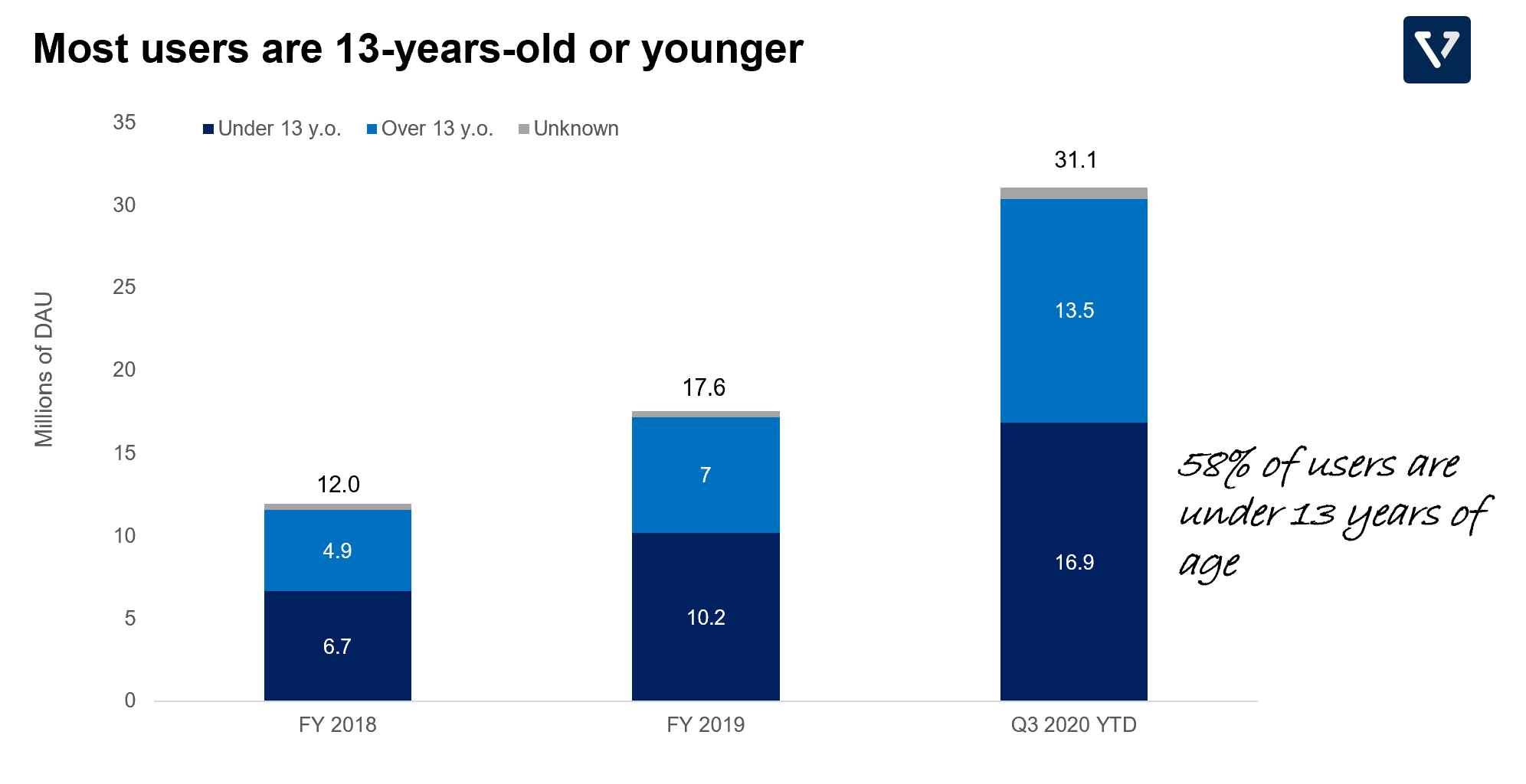

Most Roblox users are children. As of Q3 of 2020, 58% of its users are 13 years-old or younger (Figure 3). This means that they have lower purchasing ability. The company’s ability to continue its growth is predicated on its ability to expand to other demographics and potentially expand beyond gaming experiences.

High concentration of young users also means that the company must spend heavily on safety and content moderation (Infrastructure and trust & safety expenses are 32% of revenue).

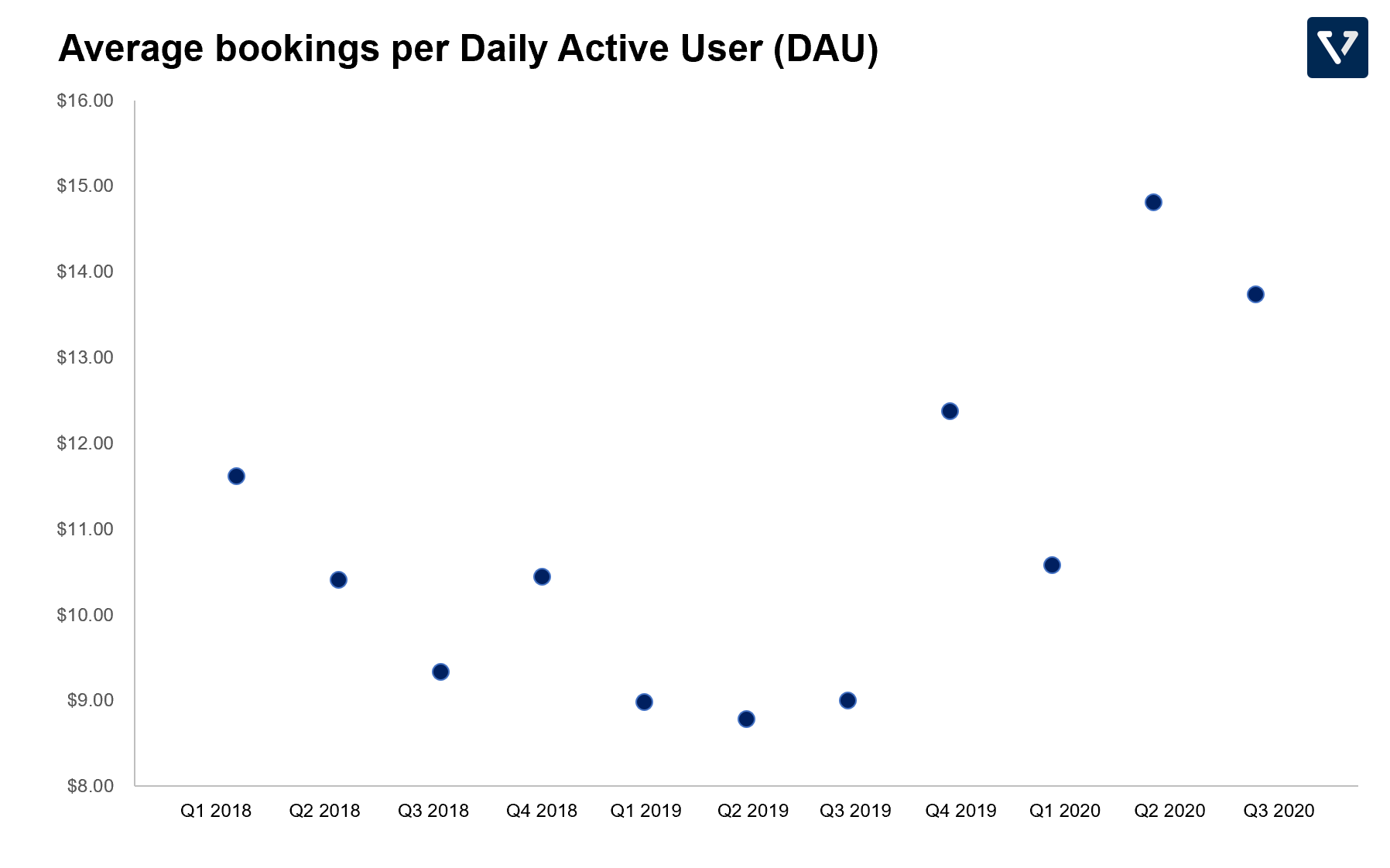

Revenue per user is trending up. Because of the pandemic, the number of users and their engagement increased. As a result, the average revenue that Roblox extracts from the average player increases (to be clear, this does not include the revenue Roblox generates from the developers). In Figure 4, we plot the Average bookings per DAU (ABPDAU – sorry lots of acronyms – but this is just the amount of money the average player in the ecosystem spends. Each data point is for the quarter).

In the first 3 quarters of 2020, Roblox was able to extract a total of US $39/user, which puts the company on track to exceed more than US $50/user for the entire 2020 (Q4 revenue is typically the highest for the company).

How does that compare to other subscription services or social media platforms over the first three quarters of 2020?

- Facebook: US $160/user (mainly from advertising)

- Snap: US $25.6/user (mainly from advertising)

- Netflix: US $96.4/user

All in all, not bad, considering the Roblox is still relatively early in its expansion. It can extract more revenue per active user than Snap and is only 2.5X smaller than that of Netflix.

To improve the revenue per DAU, it is important that Roblox can expand its core user demographic to an older audience. In order to do that, the company will need to continue to enhance its graphical capabilities to attract an order audience and expand beyond its core gaming experience.

At the moment, Roblox’s graphics are optimized for playability over a wide array of devices (from a low powered smartphone to a state of the art PC). And therefore, the company imposes constraints on the quality and fidelity of the games. Over time however, the graphical capabilities will improve (see Figure 5).

Risks

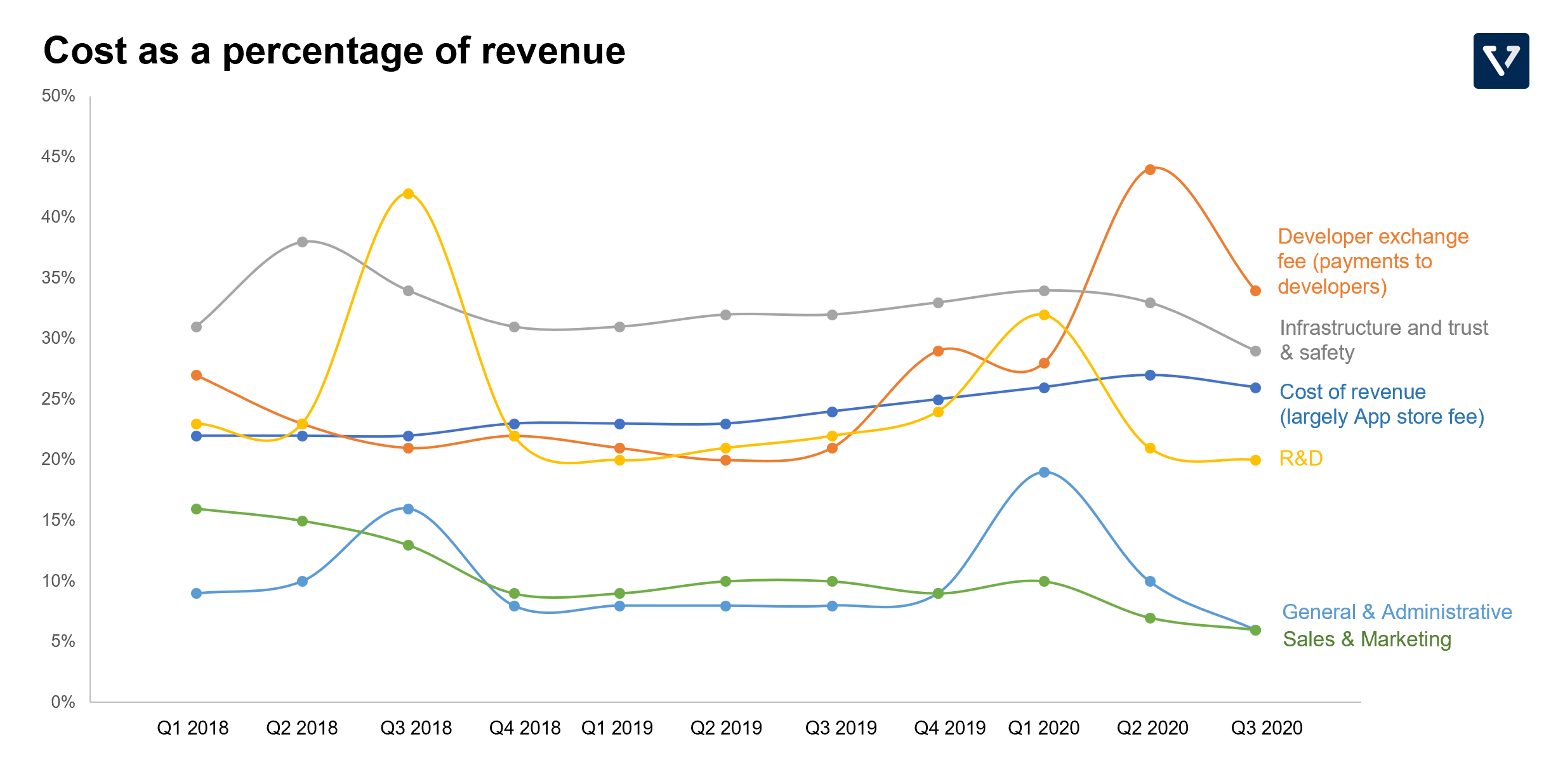

Costs are high. Will Roblox have the profitability margin of a software company? The breakdown of the company’s expenses as a percentage of revenue is shown in Figure 6. Here are key takeaways:

- The top three expenses are (1) Develop exchange fee (payment to developers), (2) Infrastructure and trust & safety, and (3) Cost of revenue (largely the 30% cut that Apple and Google take as part of the app store fee).

- For 2020, these three expenses sum up 94% of total revenue. It is unlikely that these numbers will go down in the future. Payments to developers will not go down in the future if the ecosystem continues to thrive. App store cut is unlikely to go down either (this is testament to the duopoly of Apple and Google and their respective App Stores). And in the near term, as long as the core audience is children, it is unlikely that trust & safety expenses will meaningfully decline.

- What this means is that, despite the software nature of the business, Roblox might not be as profitable as other social media/software companies.

- The good thing though, is that the company barely spends money on sales & marketing. Its growth appears to be largely organic.

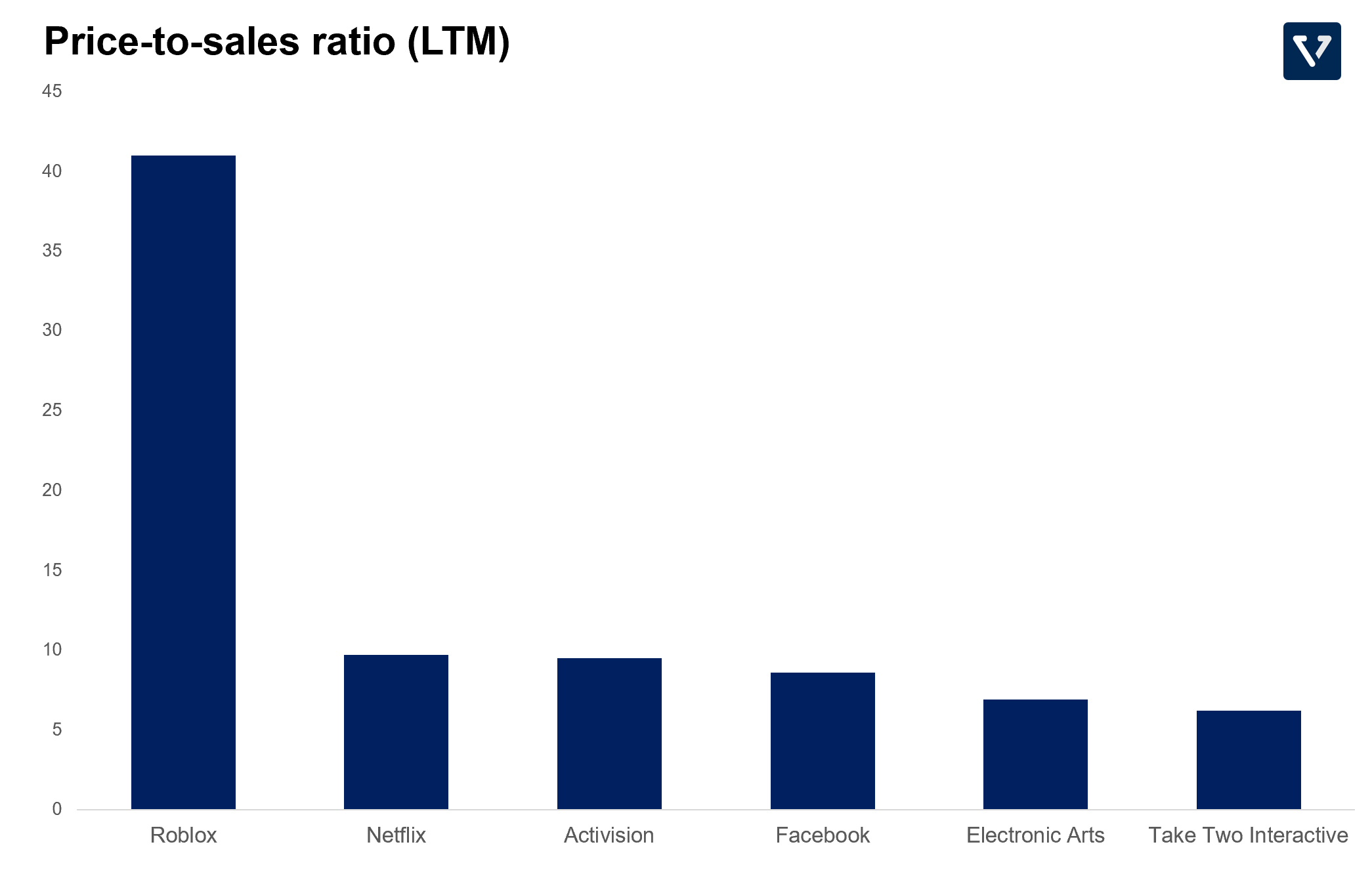

As is true for a lot of recent hot IPOs, Roblox’s valuation does not seem to make sense. Since the company is not profitable yet, we look at the Price-to-sales ratio from the last twelve month (P/S LTM). The P/S ratio indicates how much investors are willing to pay for every dollar or Roblox’s revenue.

Roblox’s P/S at this writing is 41X. That is almost double that of the richly valued Tesla (at 21X) and more than four times higher than that of Netflix and Activision Blizzard.