Skip to content

Skip to content

Learning from history 🙂

Centuries ago, in the heart of a small village, the act of borrowing and lending was simple and personal. When your neighbour’s roof leaked or his cow fell sick, you might offer a helping hand in the form of money. And in times of your own need, another neighbour might lend you grains or tools. This age-old system was built on trust, understanding, and community bonds, where transactions weren’t just about money, but about relationships and mutual support.

As societies evolved, this personalized system of borrowing and lending slowly started giving way to structured banks and large financial institutions. Yet, deep within our collective memories, the essence of community help and trust has remained.

Enter the age of the internet. The old ways of lending have been reimagined and brought back to life in a digital format, known as Peer-to-Peer (P2P) lending.

The idea of P2P lending

P2P lending bridges the gap between individuals with financial needs and those with financial resources to spare.

Picture this: Your friend, facing financial hurdles, needs funds for an unforeseen emergency. You, having saved up over the years, are looking to grow that money rather than let it gather dust in a bank account. In the past, your paths might never have crossed in this context. But in the digital age, P2P lending platforms allow you both to meet, eliminating the need for banks to act as middlemen.

Your friend, the borrower, can present their needs on the platform, while you, the lender, can scan through various borrowing requests and decide where you’d like to invest.

This creates a win-win: The person who needs money can get it without the usual paperwork that traditional banks require. Meanwhile, you might earn more from this than you would from a savings account or other typical investments.

So, in the P2P model:

- People who need money (borrowers) can get it without going to a bank.

- People with extra money (lenders) can lend it out and earn higher interest than what a typical bank fixed deposit provides.

How does P2P work?

P2P lending platforms connect borrowers and lenders, similar to how Uber connects riders and drivers or Flipkart connects buyers and sellers. The platforms manage both the supply (lenders) and the demand (borrowers). The supply side is responsible for handling the investors and onboarding partners, such as Vested, who bring in investors. The demand side works with loan/vendor partners or even borrowers directly.

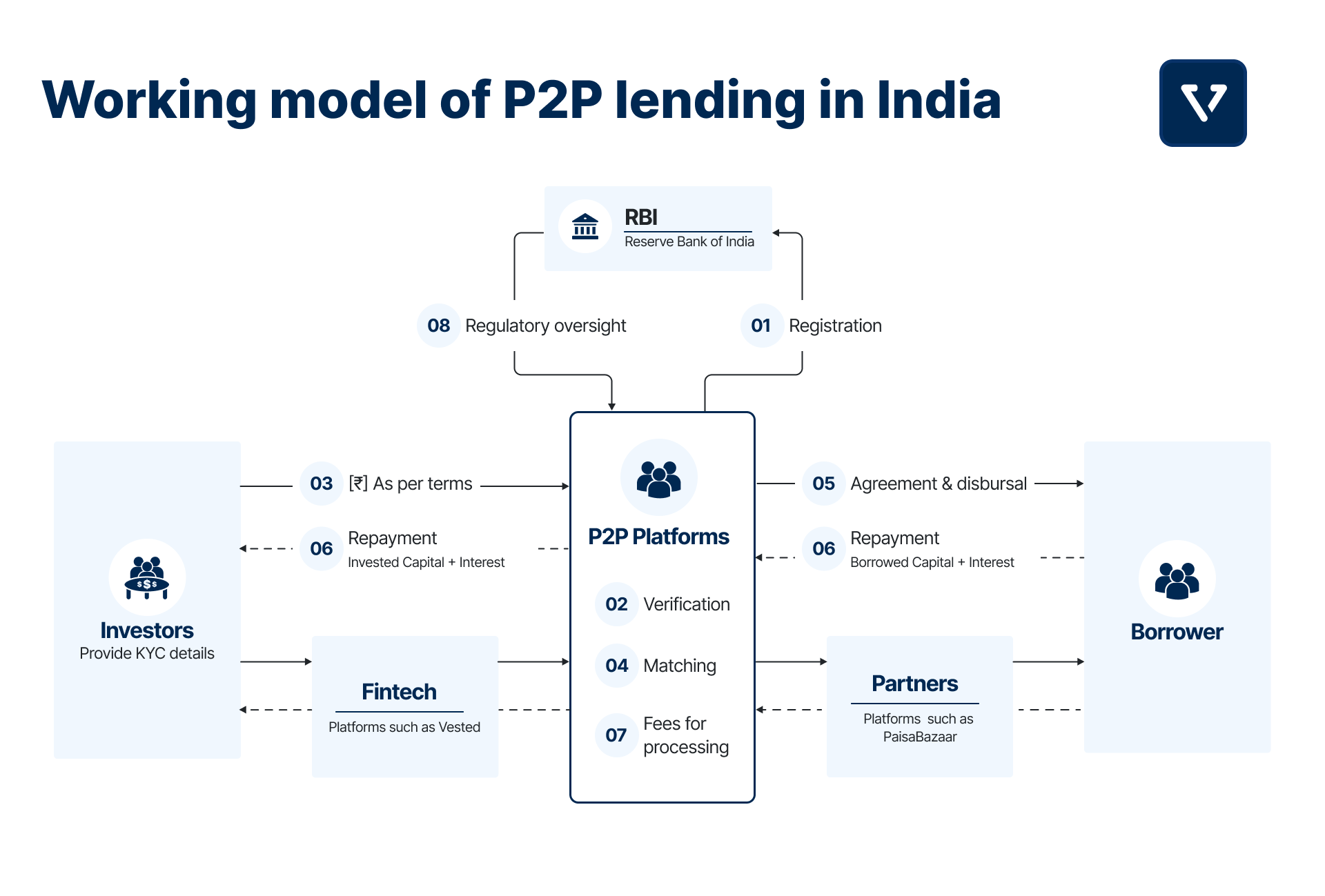

Here’s an illustration of the multiple steps involved in P2P lending in India (see Figure 1)

- Platform Registration: There are various P2P lending platforms in India where lenders and borrowers can register. Since October 2017, the Reserve Bank of India (RBI) has regulated these platforms by requiring them to obtain a license to operate as an NBFC-P2P (Non-Banking Financial Company – Peer to Peer).

- Verification of lenders and borrowers: Both lenders and borrowers may need to register on a P2P lending platform. The platform performs the Know Your Customer (KYC) process. They may verify identity, address, and bank details and assess the borrower’s credit risk. Sometimes, borrowers and lenders are introduced via partners who undertake the KYC on their end and pass it on to the platform.

- Setting terms for lenders: With the help of technology, P2P platforms have made the selection of borrowers by lenders much easier. They use automated systems to match borrowers with the selection criteria of the lenders. As an investor, once you sign up and give the platform your preference of interest rate, duration and amount of the borrowers, the system automatically allocates your funds based on the guidelines you have provided.

- Matching lenders and borrowers:

- Listing: Borrowers create a listing for their loan requirement, mentioning the purpose, amount, and other details.

- Selection: Lenders browse through these listings and choose whom to lend to based on their risk appetite and return expectations.

- Automated matching: Leading P2P platforms offer automated matching, where algorithms pair lenders and borrowers based on compatibility.

- Hyper-diversified matching: Nowadays platforms not only match you automatically, but they spread your investment across multiple borrowers in what is called hyper-diversification (more details later in the Chapter)

- Agreement and disbursement:

- Loan agreement: Both parties agree to a legal contract outlining the terms and conditions.

- Disbursement: Once agreed, the lender’s amount is transferred to the borrower’s account.

- Repayment:

- EMIs: Borrowers repay the loan in Equated Monthly Installments (EMIs), which include principal and interest.

- Collection: P2P platforms often handle the collection process, making it easier for both parties.

- Missed payments: In case of default, the P2P platform might initiate legal action or work with a collection agency.

- Fees and Charges:

- Platform fees: P2P platforms usually charge a fee for their services, which could be a percentage of the loan amount or a fixed charge.

- Regulation:

- RBI guidelines: In India, P2P lending platforms are regulated by the Reserve Bank of India (RBI). Platforms must adhere to guidelines such as maintaining minimum net-owned funds, implementing proper grievance redressal mechanisms, and adhering to caps on the amount one can lend or borrow. We’ll dive deeper into the rules and regulations in Chapter 2.

- Safeguards: Investors are exposed to the risk of default. Unlike bank deposits, there’s no insurance on the funds lent through P2P platforms. However, P2P platforms carefully assess risks. They also spread an investor’s money across many borrowers to reduce risks. We’ll talk more about these safety measures in upcoming chapters.

Key Takeaways

- Peer-to-Peer lending modernizes traditional community-based borrowing through digital platforms, connecting individual borrowers with lenders.

- P2P platforms in India is regulated by the RBI, facilitate the entire lending process, from user verification to loan repayment, and manage borrower-lender matching.

- P2P lending platforms use algorithms for matching lenders and borrowers and employ strategies like hyper-diversification to spread investment risks.

- Loans are typically repaid in EMIs, and the platforms handle collections and defaults. While there’s no insurance for lent funds, risk is managed by careful borrower assessment and investment diversification.

- P2P lending in India adheres to RBI guidelines, ensuring a structured and secure environment for both lenders and borrowers.