Skip to content

Skip to content

Investing is a balancing act of striving for growth while ensuring capital preservation and maintaining access to liquid assets. Each investor has a unique financial situation, risk tolerance, and goal, leading to the bifurcation of investment objectives into primarily two categories: growth and safety.

Growth is the aim to increase the value of the principal amount over time. Investments targeting growth, like equities or real estate, typically come with higher risk but offer the potential for higher returns. They are often subject to market volatility, and while they can provide substantial gains, they can also result in losses.

On the other hand, the primary objective of safety is capital preservation, ensuring that the principal amount remains intact. This is where fixed-income instruments play a significant role. These instruments, which include government bonds, corporate bonds, P2P lending, fixed deposits (FDs), and treasury bills, provide a predetermined interest return over a specified period, offering stability to the portfolio. They are generally less volatile compared to growth assets.

Liquidity or the ease with which an asset can be converted into cash, is another essential consideration for investors. Having liquid assets ensures that funds are readily available for any unforeseen expenses or for capitalizing on new investment opportunities.

People often gravitate towards fixed-income instruments like FDs due to their perceived safety, stable returns, and potential for portfolio diversification. Additionally, their relative liquidity makes them a preferred choice for many conservative investors. However, from an inflation-beating returns perspective, FDs can sometimes be problematic. Their returns are not able to beat inflation, i.e. the increase in the cost of your expenses due to rising prices. Tax implications further erode the effective return in many cases.

In order to boost your fixed-income returns, you may need to complement your FDs with other fixed-income assets. In that situation, P2P lending emerges as a compelling complement to FDs, offering notably higher potential returns that can beat inflation. The platform’s flexibility, diversification opportunities, and the ability to choose plans to maintain liquidity make P2P lending a viable option. Yet, it’s essential to note that with the promise of higher returns, P2P lending carries higher risk than FDs and it should be viewed as a complement to FDs rather than a replacement.

Returns profile before inflation

Returns profile after inflation

Inflation Rate (CPI): Based on the 2022 Consumer Price Index by RBI.

P2P returns: Possible returns projected by Vested Edge for P2P lending.

FD returns: The return on a 1-year FD as quoted by ICICI Bank in June’23.

Factors work in favour of P2P lending

1. Low minimum investment

- Accessibility: P2P lending provides an accessible entry point for new investors. You can begin building your portfolio with an investment as low as Rs. 10,000 to 20,000.

- Gradual scaling: This flexibility allows investors to enter the market at a comfortable level and slowly increase their investments as they become more familiar with the landscape.

2. Regular income

- Early returns: P2P lending enables lenders to see returns quickly, often starting the consecutive month after the investment. Also, some P2P platforms offer liquid plans, where interest accumulates daily, and withdrawals can be made at any time.

- Predictable payments: The repayment schedule, including both the principal and interest, is structured in monthly installments, providing a steady income flow.Within this context, there are typically three types of plans that cater to the varied needs of investors.

- First, there are fixed-term plans where investors receive both the interest and the principal amount at the end of the investment term. This is particularly attractive for those who wish to lock in their investments and reap lump sum returns at maturity.

- Secondly, the monthly income plans offer a consistent cash flow, as investors are paid interest on a monthly basis, while the principal amount is returned at the end of the loan’s term. This is an appealing option for those seeking a regular income stream, similar to the returns from a rental property or dividend-paying stock.

- Lastly, liquid plans provide the utmost flexibility. In these plans, investors have the liberty to release their funds on demand. While this might not guarantee the highest returns, it gives investors the peace of mind knowing they can access their money whenever they need it, aligning closely with the convenience of traditional savings accounts.

3. Low volatility

- Stable returns: Unlike volatile market-linked investments such as mutual funds, the returns in P2P lending are pre-determined. Investors know the returns before the investment is done.

- Consistent performance: This leads to more predictable returns that are less subject to unexpected market shifts.

4. Ease of investment

- Digital process: From auto-selecting borrowers and executing legal agreements to receiving repayments, P2P lending platforms offer a completely digital experience.

- Escrow account: All transactions are secured through a third-party trusteeship, adding another layer of security.

- Real-time updates: Platforms provide regular performance updates, enabling you to track your investments in real-time.

5. Risk mitigation strategies

- By the P2P platform: Platforms implement thorough borrower selection processes, legal agreements, collection of security cheques, strategic collection and recovery mechanisms, and restrictions on funding to minimize risks.

- By the investor: You, as a lender, can further reduce risk by making small-ticket investments across multiple platforms, essentially distributing risk and potentially maximizing returns.

P2P lending vs. other asset classes: What are the risks and rewards?

Understanding risk in its various forms is crucial in money management. By breaking down risk into different types and employing appropriate strategies to manage them, investors can better navigate the uncertainties of the financial world. The goal is not to avoid risk altogether but to understand it, plan for it, and manage it effectively to achieve financial goals. Whether you are a seasoned investor or just starting, recognizing and mitigating risks can be key to successful money management.

Let’s delve deeper into understanding risk, expected returns, and the nuances of various investment instruments.

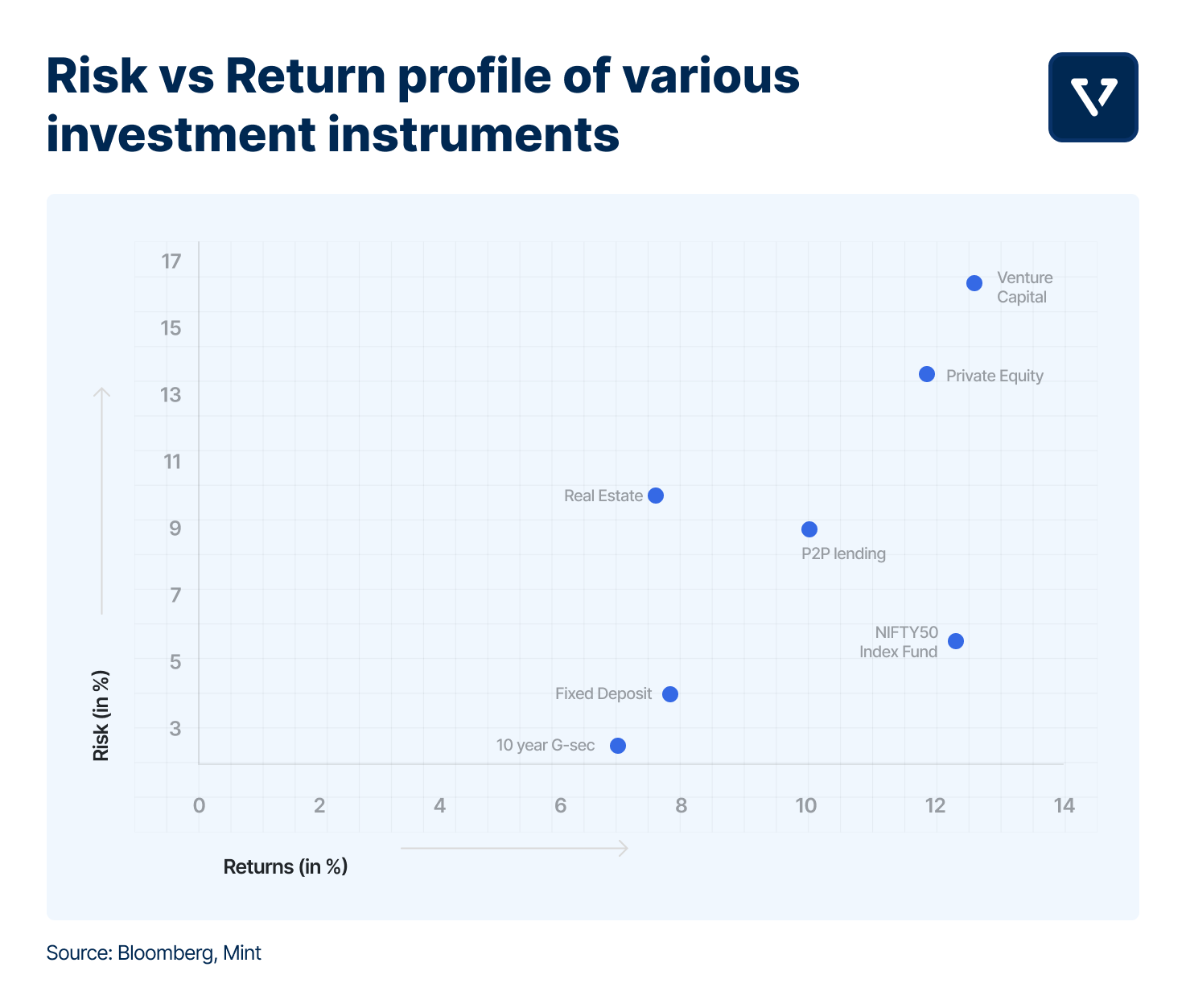

1. Fixed Deposits (FDs)

Risk: Low

Expected Returns: The average interest rate for FDs in India hovers between 3% to 6%, but this can change based on the bank, tenure, and the prevailing economic conditions.

Insight: FDs are like safety nets. They offer guaranteed returns, and your principal amount remains safe. However, with inflation, the real rate of return (after negating the effect of inflation) might be lower than what’s advertised. This means that the purchasing power of your money might reduce over time.

2. Peer-to-Peer (P2P) Lending

Risk: Low to moderate

Expected Returns: Generally, P2P platforms in India have been seen to offer returns ranging from 8% to 12%, though this can fluctuate based on borrower profiles and platform credibility.

Insight: P2P has higher potential returns than FDs, but it also carries a higher risk. In FDs, your money is backed by the bank (up to Rs. 5 lakhs per depositor under DICGC), but in P2P, there’s a chance of default where borrowers might not repay. However, the higher returns might justify the risk for some. It’s crucial to spread investments across multiple platforms and multiple borrowers for diversification.

Comparing FDs vs P2P:

When looking purely at returns, P2P seems to have an edge over FDs. However, when factoring in risk, FDs are safer. A combination of both can help you build a better fixed income portfolio

3. Mutual Funds

Risk: Moderate to high (though it can vary based on the type of fund)

Expected Returns: Historically, equity mutual funds in India have given returns of anywhere between 10% to 15% over the long term. However, debt funds or liquid funds might offer lower returns, closer to FD rates.

Insight: Equities are a great long-term wealth building option and equity mutual funds provide diversification. Instead of putting all your money in one stock or bond, fund managers spread it across multiple assets. While the risk is higher than FDs and P2P, mutual funds add a different dynamic to your portfolio.

4. Direct stock investment:

Risk: High

Expected Returns: The stock market’s returns can be quite volatile. Historically, the Indian stock market (e.g., NSE Nifty 50) has provided average annual returns of around 12% to 15%, though individual stock performance can vary widely.

Insight: Investing directly in the stock market can offer high rewards, but it’s also quite risky. Market sentiment, global events, or company performance can drastically affect returns.

5. Real Estate

Risk: Moderate to high

Expected Returns: Real estate returns can be quite variable based on location, property type, and the time horizon. Historically, urban real estate in India has appreciated at an average rate of 6% to 10% annually, but this can be much higher in rapidly developing areas or much lower in stagnant markets.

Insight: Real estate offers tangible assets, but the high entry cost and potential liquidity issues (i.e., it might take time to sell a property) can be barriers. Returns can also be influenced by infrastructure developments, urbanization trends, and government policies. You can treat some real estate, like commercial properties, as a fixed income asset while others, like residential properties, can be for long-term appreciation.

6. Gold

Risk: Moderate

Expected Returns: Historically, gold has been a favored asset in India and has provided annual returns of around 7% to 9%. However, its price can be influenced by global economic conditions, geopolitical tensions, and supply-demand dynamics.

Insight: Gold has always held a special place in the Indian investment landscape, not just for its cultural and traditional significance but also as a hedge against inflation and economic downturns. The metal is often seen as a ‘safe haven’ during turbulent times. While its price can fluctuate in the short term, over longer periods, gold has proven to be a stable and reliable investment. It’s also liquid, meaning you can easily convert it to cash if needed.

7. Bonds and debentures

Risk: Varies (Government bonds are typically lower risk, while corporate bonds can range from low to high risk depending on the company’s credit rating.)

Expected Returns: The return on bonds and debentures depends on the issuer and the type. Government bonds (like the Indian government’s 10-year bond) have historically yielded between 5% to 7%. In contrast, corporate bonds can offer higher returns, depending on the company’s creditworthiness.

Insight: Bonds and debentures represent debt instruments. When you invest in them, you’re essentially lending money to the issuer, whether it’s the government or a corporation. In return, you receive periodic interest payments and get the principal amount back at maturity. They’re typically less volatile than stocks and can offer a predictable income stream. Bonds in combination with P2P lending and FDs can form your fixed income portfolio.

8. Start-up investments (Private equity and Venture capital)

Risk: Very high

Expected Returns: The returns on start-up investments are challenging to generalize because of their high variability. While many start-ups fail and investors may lose their entire investment, successful ones can offer returns many times the original investment. Some reports suggest that successful venture capital-backed companies can offer returns of 200% or more, but these figures should be taken with caution, considering the high failure rate of startups.

Insight: Investing in start-ups is akin to venturing into the unknown. The potential for high returns is undoubtedly there, especially if you back a future unicorn. However, the risks are also substantial. Many start-ups fail within their first few years, resulting in a complete loss for investors. Due diligence is crucial – understanding the business model, the industry landscape, the founders’ backgrounds, and the company’s financials can help make an informed decision. It’s also advisable to only allocate a small portion of your investment portfolio to start-ups to manage risk better.

How can investing in P2P lending help diversify an investment portfolio?

Diversification is a term that resonates with almost every financial planner, investment manager, and individual investor. But what exactly is diversification, and why is it considered one of the fundamental principles of investing?

Diversification is the strategy of allocating investments among various financial instruments, industries, and other categories to mitigate the impact of adverse market conditions. In simple terms, it means not putting all your eggs in one basket.

For diversification, one must understand three parameters.

How much to invest?: You don’t want your entire portfolio to be concentrated in one asset. A balanced approach means allocating a certain percentage of your portfolio to an asset.

- Portfolio allocation: As a rule of thumbP2P lending, which is considered an alternative investment, should not constitute a very high portion of your overall portfolio. Financial advisors might recommend allocating anywhere from 5% to 25% of your total investment portfolio to P2P lending, depending on individual circumstances and risk tolerance.

- Diversification within P2P: Even within your investments in P2P, diversify by lending small amounts to multiple borrowers rather than a large sum to one or a few borrowers. This will help mitigate the risk of default. (read the next section on hyper diversification within P2P)

When to invest?: P2P lending can be particularly attractive when traditional investments like the stock market are highly volatile. Since P2P returns are generally independent of market trends, it might add stability to your portfolio.

Also,

What to invest in?: P2P platforms in India provide exposure to various borrower profiles, like small businesses, individual borrowers, etc. Each category has its risk and return profile. When evaluating platforms, it’s important to understand which type of customers they lend to and what is the purpose of the loan. Each platform has a unique approach. For example, some lend to small businesses, whereas some lend to salaried individuals.

Now, to understand how P2P lending would fit into your portfolio, imagine that you have ₹10,00,000 to invest.

Traditionally, you might put:

- 60% in stocks: ₹6,00,000

- 30% in FDs: ₹3,00,000

- 10% in gold: ₹1,00,000

Now, let’s say you decide to diversify further with P2P. You might adjust your holdings as:

- 50% in stocks: ₹5,00,000

- 25% in FDs: ₹2,50,000

- 10% in gold: ₹1,00,000

- 15% in P2P: ₹1,50,000

P2P is not correlated with traditional stock or bond markets. Hence, when there’s a downturn in stock markets, your investments in P2P lending will likely remain unaffected or even prosper. Historically, P2P lending has shown to offer stable and attractive returns, making it a good choice for those looking for a balance of risk and reward.

Hyper diversification within P2P

Hyper diversification is a strategy within the investment world that refers to an extreme spread of investments across various assets, sectors, or instruments. In the context of peer-to-peer (P2P) lending, hyper diversification takes on a specific meaning. Let’s explore it in more detail.

In traditional investing, diversification often means spreading your money across different asset classes like stocks, bonds, real estate, etc. Hyper diversification within P2P lending goes a step further and implies spreading your investment across many different loans, borrowers, and risk profiles within the P2P space itself.

Here’s an example to understand the concept:

Imagine you have INR 1,00,000 that you want to invest in P2P lending in India. If you lend the entire amount to one borrower, you’re heavily reliant on that single borrower’s ability to repay the loan. If that person defaults, you could lose the entire investment. But with hyper diversification, you can spread that INR 1,00,000 across 50 borrowers and give INR 2,000 to each borrower. Now with each borrower, you only risk 2% of your capital vs. 100% with one borrower earlier.

Way to achieve Hyper Diversification

- Spread across many loans: Instead of putting all your money into one loan, you could spread it across 100 different loans, each of INR 1,000. This way, even if one borrower defaults, you only lose 1% of your investments.

- Diversification across risk profiles: Within those 100 loans, you could further diversify by lending to different types of borrowers. Some might be low-risk with lower returns, while others might be higher risk with the potential for greater returns. This way, you’re not only spreading the risk but also potentially creating a more balanced return profile.

- Platform diversification: You could also diversify across different P2P lending platforms. Choosing multiple platforms not only minimizes platform-specific risks but also allows you to tap into diverse risk profiles, enhancing overall portfolio resilience.

Benefits of Hyper Diversification in P2P

- Reduces risk: By spreading the investment thinly across many loans, you reduce the impact of any single default.

- Potential for balanced returns: By carefully selecting a mix of risk profiles, you can tailor the return potential to your specific preferences and risk tolerance.

- More stability: Hyper diversification may lead to more stable returns, as it’s unlikely that all segments of the portfolio would perform poorly simultaneously.

Key Takeaways

- P2P lending is an attractive investment avenue due to its low entry cost, regular monthly income, low volatility, ease of investment, higher control over investment, and potential risk mitigation strategies.

- We can compare investing in P2P lending to fixed deposits, mutual funds, the stock market, and real estate to get an understanding of its relative risk and reward in comparison to traditional investment opportunities. P2P is seen as offering potentially higher returns than fixed deposits and less volatility than stock markets.

- Diversification of your portfolio through P2P is possible. One can consider allocating 5-15% of one’s portfolio in P2P loans.

- We also covered a specific and effective strategy within P2P lending called hyper diversification. It involves spreading investment across many different loans, borrowers, and risk profiles within the P2P space itself, significantly reducing the impact of a single default.