Skip to content

Skip to content

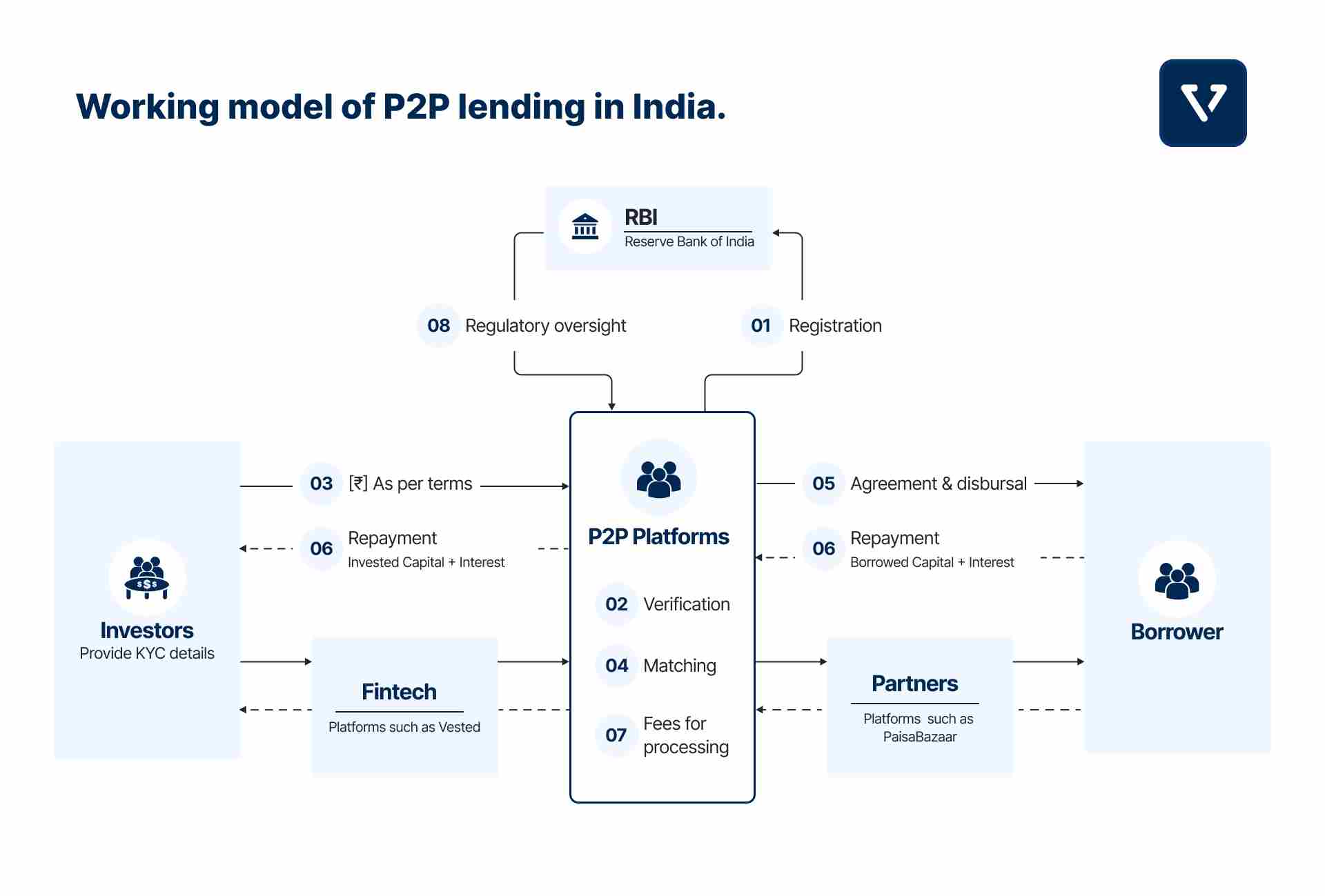

In our previous chapters, we dived into the world of Peer-to-Peer (P2P) lending and took a detailed look at the role of the big guardian in the room—Reserve Bank of India (RBI). Having understood those building blocks, let’s now focus on the glue that holds this ecosystem together: the P2P lending platforms themselves.

The P2P lending ecosystem, at its core, is about connecting lenders and borrowers in an efficient and transparent manner. While the oversight and guidelines provided by the Reserve Bank of India (RBI) act as a protective shield, ensuring that operations within this space are safe and reliable, it’s the lending platforms themselves that drive the actual transactions.

P2P lending platforms form the interface between borrowers in need of funds and lenders looking for opportunities to invest their capital. Thus, understanding the nitty-gritties of these platforms is pivotal. Not only does it ensure that one navigates through this financial arena with confidence, but it also assures that the underlying transactions, right from lending to repayment, happen without hiccups.

Demand and supply generation

At the heart of the P2P lending ecosystem is the lending model, which determines how money flows from one entity to another. This model is characterized by two main participants: the suppliers of money (lenders) and the demanders of money (borrowers).

In Chapter 1, we explored the fundamental concepts of the model.

Demand: Who are the borrowers?

The demand for loans in the Indian P2P ecosystem primarily originates from three types of players: (See Figure 1)

Individual borrowers

- Salary earners: In the Indian P2P lending landscape, salaried professionals form a significant segment of borrowers. They often seek personal loans, funds for medical emergencies, or even finance for vacations.

- Self-employed professionals: Be it doctors, engineers, or freelancers, this group seeks business expansion loans, personal loans or working capital loans.

Institutional borrowers

- Small and medium-sized enterprises (SMEs): These are businesses that require capital to expand, buy inventory, or even for day-to-day operations. Example: Your neighborhood Kirana store

Platforms and ecosystem partners

- Financial marketplaces: Financial marketplaces are online platforms that aggregate and offer a variety of financial products and services, from loans and credit cards to insurance and investment products. They act as a one-stop shop for consumers looking for financial solutions.

When such platforms partner with P2P lending platforms, it means they are expanding their offerings to include peer-to-peer loan options. This provides consumers with even more choices when it comes to borrowing. For instance, platforms like BankBazaar or PaisaBazaar collaborate with multiple banks, NBFCs, and P2P lenders, allowing users to compare and choose the best loan product for their needs.

- Direct selling agents (DSAs): Direct Selling Agents, or DSAs, are intermediaries who play a crucial role in the distribution of loans in India. They act as representatives for banks or financial institutions and help in sourcing potential borrowers. In essence, DSAs bridge the gap between financial institutions and the public.

Historically, DSAs operated mainly through offline, on-ground networks. However, with the advent of technology and digital transformation, many DSAs have adapted and now utilize tech tools to source clients and manage relationships. Their strength lies in their deep-rooted network of clients and their ability to reach out to potential borrowers, thereby increasing the distribution reach of the financial products they represent.

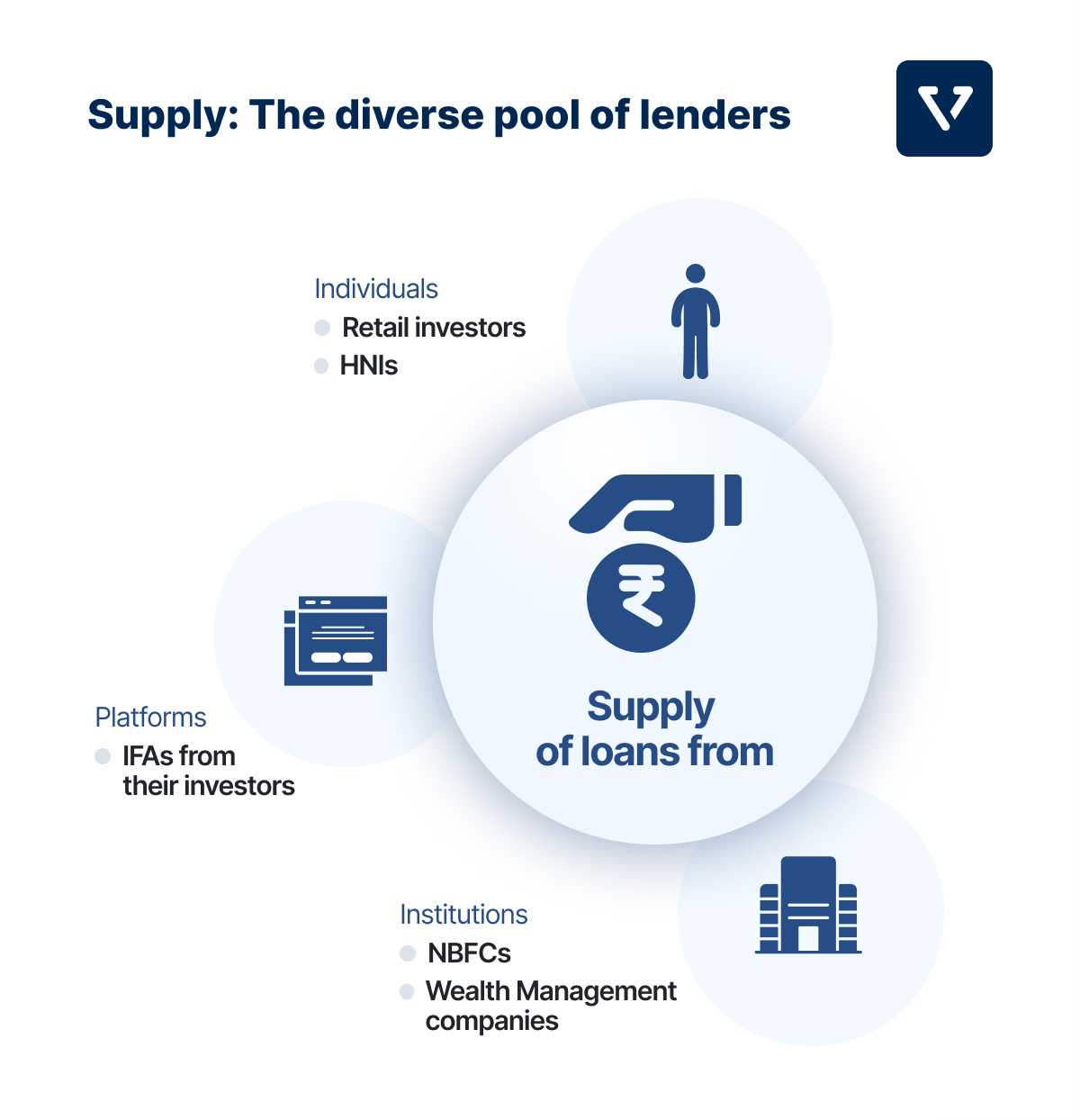

Supply: The diverse pool of lenders

To meet the increasing demand for loans, a substantial supply of capital is essential. Let’s explore the sources of this capital and understand where the supply originates from.

Individual investors

- Retail investors: This group typically comprises individuals who invest in small to medium-sized amounts, say Rs. 10,000 to Rs. 5 lakh.

- High net-worth individuals (HNIs): They usually invest larger amounts, diversifying across multiple P2P platforms. Typically, they invest upwards of Rs. 5 lakh in P2P lending as an asset class.Here are the limits that individual investors have:

- Overall limit: An investor can lend up to a total of Rs 50,00,000 across all P2P platforms. This is the maximum amount they can have lent out at any time.

- Certification for bigger investments: If an investor wants to lend more than Rs 10,00,000, they need a certificate. This is a note from a Chartered Accountant that says the investor has assets and wealth (net worth) worth at least Rs 50,00,000.

Financial platforms and agents

- Fintech platforms: These are technologically enabled platforms that facilitate various financial transactions and services. Example: Vested is a platform that allows investors to invest in the P2P lending along with investments in the US stock market.

- Independent financial advisors (IFAs): With a vast network of clients, IFAs distribute P2P lending as an investment product.

P2P platform for the borrower

The role of P2P platforms is very important. The platform-designed systems automate and streamline every single step of a customer’s journey, from initial onboarding to post-transaction operations. This digital journey is built upon a rule-based engine and system. (see Figure 4)

Let’s understand this in detail by first looking at the borrower journey followed by one of Vested Edge’s partner platforms, Faircent. Faircent has 41.81 lakh registered borrowers and enabled lending of Rs. 3,585 crores as of October 2023.

1. Loan request

Every P2P platform has a different type of borrower and a different strategy for sourcing them. Faircent has built their speciality in lending to small businesses and in sourcing these businesses via an offline Direct Selling Agent or DSA model.

Faircent has partnered with 2,500+ DSAs to source the end borrower. These DSAs are essential, bringing in 4 out of every 5 loan seekers to the platform. But Faircent doesn’t just give loans to anyone. They’ve set up rules for these DSAs to follow (we cover this below), ensuring that they bring in only reliable and trustworthy individuals. This way, Faircent maintains its quality and reputation while helping small businesses grow.

2. Digital data capture

Once a potential borrower is identified by Faircent’s DSA, they collect different types of data to ascertain whether the borrower is worthy of a loan. In a bid to ensure efficiency and minimize paperwork, Faircent has introduced a digital data capture system. This system is designed to capture five essential data fields:

- Full Name

- Date of Birth (DOB)

- PAN Card Details

- Address/Pin Code

- Mobile Number

3. Authenticating identities

Step 3 is to verify the authenticity of the end borrower.

- Selected data points from the provided five, especially PAN card details, are subjected to verification through online PAN verification APIs connected to the Income Tax database.

- Authenticity is established when the data given by borrowers matches the records in the income tax repository.

4. The critical role of automated credit bureau checks

For a holistic understanding of a borrower’s credit profile, Faircent shares the captured five data points with the Credit Bureau. This initiates an automated check into the borrower’s credit history and behaviors.

- This check is essential to Faircent’s decision-making process, helping discern the feasibility of progressing with a specific borrower.

- During this stage, stringent exclusion criteria come into play. Borrowers may be excluded based on:

- New to credit (NTC)

- Past Defaults: Unpaid for 90 days or more.

- Current Delinquents: Over 90 days of payment delay.

- Recent Payment Delays: Delayed by more than 30 days in the last year.

- Short Bureau Vintage: Self-employed with a credit history of less than 3 years and salaried with less than 2 years.

- Excessive Credit Inquiries

Approximately 85% of applicants do not progress past this stage, ensuring that only the most eligible borrowers continue.

5. The rule engine

If the borrower survives the Bureau cuts, they’re directed to what they call a “Rule Engine.” This machine-learning-based engine has years’ worth of data and learning behind it. It decides how much money one can borrow, at what interest rate, and for how long. It’s super smart in terms of pricing risk: it rewards good borrowers with lower rates and increases rates for riskier profiles.

- The engine strategically segments customers based on risk range criteria. Embedded within this system is the pricing engine, responsible for rating and ranking borrowers based on their associated risks. Subsequently, the rate of interest is attributed.

- The tenure and amount considerations hinge on the customer’s FOIR (Fixed Obligation to Income Ratio).

- The engine thrives on extensive data, enhancing its predictive capabilities regarding borrowers’ repayment likelihood, leveraging a risk-based pricing model.

- Furthermore, Faircent’s Rule Engine incorporates machine learning. It continually refines itself using borrower performance data, improving pricing predictions and making informed decisions on borrower approvals or rejections.

6. Affordability Assessment

- Banking and GST checksSince Faircent focuses mainly on small businesses , it additionally uses banking records and GST details to determine if a business can repay a loan.

- Banking data, a vital component to gauge EMI affordability, is accessed via licensed Account Aggregators withcustomer consent. This process virtually eliminates any potential customer-initiated fraud.

- For businesses with substantial turnovers and loan requisites, GST data is retrievable from the government portal.

During this assessment phase, another 50% of the potential borrowers do not progress to the subsequent stages.

7. Personal interaction: Bridging the gap

A personal discussion is necessary to make sure the customer is legit and not a bot. It’s also a chance for experienced risk assessors to ask specific questions to gauge the authenticity and intent of the borrower.

An invaluable aspect of Faircent’s assessment is the personal telephonic interaction.

- This conversation, structured with specific queries, ensures genuine human interaction and ascertains the customer’s true intent for loan procurement.

- The underlying reason for the loan becomes pivotal during this discussion.

- Cases progress favorably when the provided reasons align with business requirements and meet the satisfaction of the risk officer. However, more than half of the potential borrowers are turned away during this phase due to inconsistencies or ambiguities in their loan rationale.

8. Credit decisions

Faircent’s comprehensive evaluation culminates in the final credit decision phase.

- A comprehensive internal credit policy check is conducted, facilitated by the internal loan management system.

- If a potential borrower sails through the personal discussion phase and adheres to all risk parameters and internal credit checks, the risk officer gives the green light for a loan offering.

After traversing through this rigorous assessment journey, a staggering 92% of initial applicants do not reach the finishing line.

9. Video and physical verification

Once the borrower crosses the risk assessment stage, the operations team steps in.

- Every borrower who successfully navigates Faircent’s credit framework undergoes a video verification facilitated by the loan officer.

- Face-matching technology stands at the forefront of this process. How does it work? A selfie image of the borrower is compared to the PAN image data retrieved during the ‘identity establishment’ phase.

But precision is the keyword. The loan officer outrightly declines matches below 65%. Interestingly, even those matches that score above 95% are revisited for conversations to negate any iota of potential fraud.

10. E-KYC and E-NACH for seamless transactions

The second last step in Faircent’s process is to complete the E-KYC procedure and set up E-NACH mandates on the borrower’s account.

- The E-NACH setup, set up through the customer’s net banking, is designed for the automated collection of EMIs. This ensures timely payments and minimal hassles.

- But what’s the weight behind E-NACH? Well, it holds a stature equivalent to that of a cheque. Governed by the framework of the negotiable instrument, it even invokes a criminal offence under section 138 in instances of non-payment.

- The verification doesn’t stop here. The E-KYC procedure is intertwined with the validation of the customer’s physical presence. It’s made certain that the customer is unmistakably at the residence or office address provided during the ‘identity establishment’ phase, ensuring that the given addresses aren’t just words on paper but verifiable locations.

Because of the thorough checks Faircent employs, only 8% of the customers pass through and secure loans. This rigorous process ensures that only the most reliable borrowers receive loans, minimizing the risk of defaults or non-payments, commonly termed as NPA risk. We’ll dive deeper into this subject in Chapter 4.

11. Digital signature & E-Agreement

- Upon successful navigation through Faircent’s verification stages, borrowers are provided an e-agreement on their personal dashboard

- Faircent’s system autonomously triggers the e-agreement, beckoning the borrower to append their digital signature. To bolster the security of this action, the signing process is authenticated via a system-generated OTP (One-Time Password).

12. Instant disbursement

The penultimate moment in the loan journey—disbursement—is executed by Faircent.

- Before the final loan disbursement, there’s one last checkpoint. Known as the penny drop, this step might sound diminutive, but it plays a key role in ensuring the sanctity of the process.

- This ‘penny drop’ entails making a minuscule transfer to the borrower’s bank account. Why? Faircent verifies that the funds earmarked for the borrower are indeed channelled to the very individual who began their loan journey on the platform. It’s a final nod ensuring that the bridge between the platform and the borrower remains unbroken and genuine.

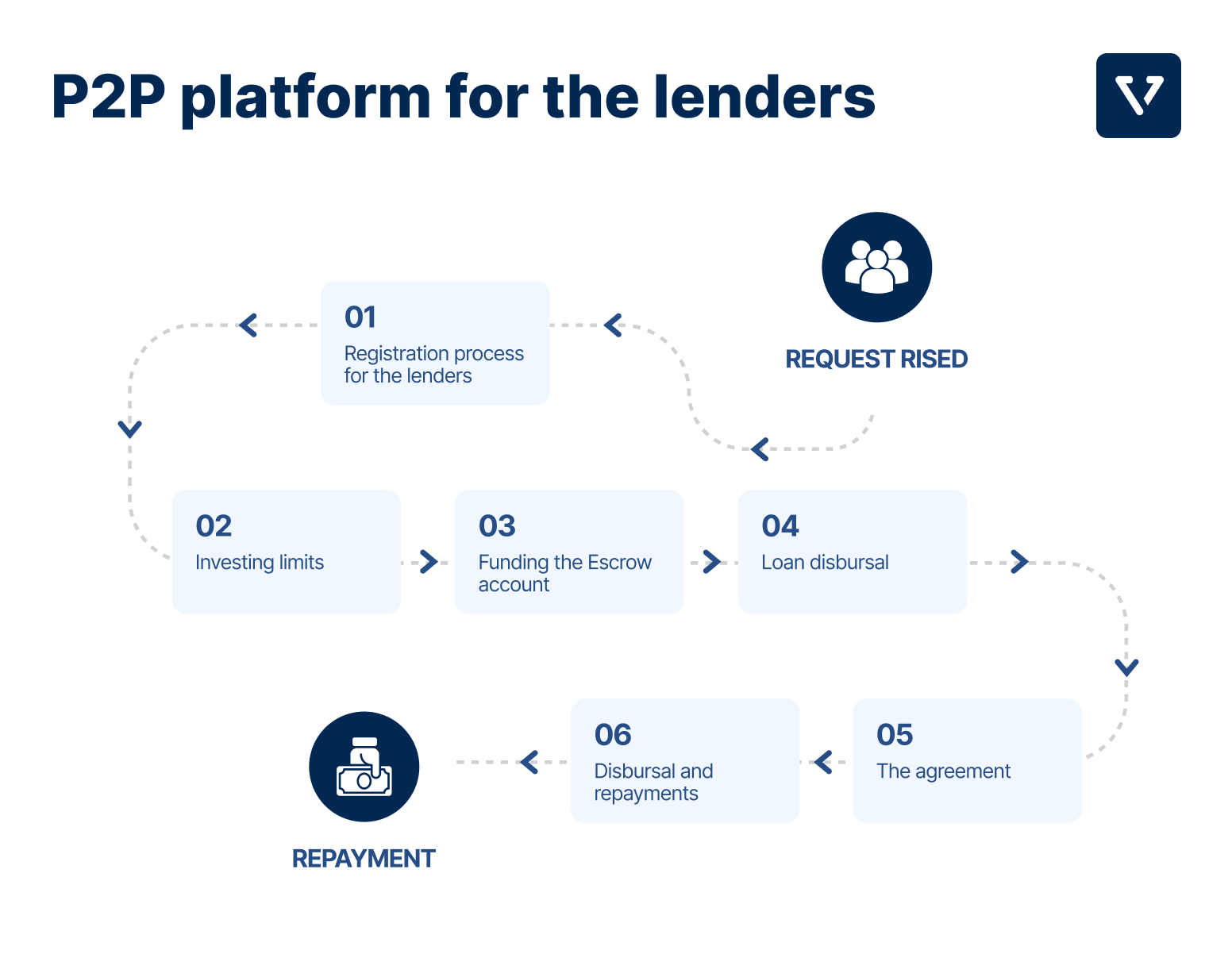

P2P platform for the lender (or investor)

Faircent acts as a bridge between lenders and borrowers. As a Peer-to-Peer (P2P) platform, it offers transparency and allows lenders to invest directly in potential borrowers. This setup provides an opportunity for potential returns while diversifying investments. (see Figure 5)

There are clear guidelines and eligibility criteria on who can become a lender (or investor)

Who can be a lender?

- Individual persons

- Groups of individuals

- HUFs (Hindu Undivided Families)

- Firms

- Societies

- Any other non-corporate entity

Basic Requirements for a Lender:

- An active bank account in India

- A PAN card

- Willingness to follow Faircent’s policies

- Commitment to the Lender Code of Conduct

For Institutional Lenders: Only financial companies listed by the RBI or those formed under the Indian Companies Act are eligible.

1. Registration process for the lenders

For anyone new to the platform, registration is the first step. Lenders simply click on the “Sign up Now” button, fill in their basic details, and upload any necessary documents. This process is designed to be swift, and once verified – typically within a day – the lender can begin their lending journey.

For Vested Edge users, this process will be done through the Vested platform, and they need not register through any other platform.

2. Investing limits

For lenders looking to diversify their investment portfolio, the platform allows an aggregate exposure of up to ₹50,00,000 across all P2P platforms. However, those keen on investing more than ₹10,00,000 need to provide a Net Worth certificate. This entire process is streamlined, and funds are channelled through a secure Lenders Escrow account under the oversight of ICICI Trusteeship Services Ltd.

3. Funding the Escrow account

An escrow account acts as a secure intermediary holding space for funds. Lenders make their first deposit. Subsequent deposits can have a lower limit. They can use a range of methods, including NEFT/RTGS, net banking, UPI, PayTM, or even cheques. Transaction fees, however, vary depending on the chosen method.

Idle funds management

One of the platform’s unique features is its approach to managing idle funds. If a lender has funds exceeding ₹500 that remain unutilised for more than a week, Faircent steps in to invest these into the Faircent Double Freedom plan automatically.

The objective is straightforward: allow the lender’s money to earn interest rather than lying dormant. Those who prefer not to opt for this feature can communicate their preferences to the platform.

4. Loan disbursal

Once the formalities are completed and the loan agreement is signed, the funds are disbursed from the Lender’s Escrow Account to the borrower. Monthly EMIs are then due, with penalties in place for any delays.

5. The agreement

To ensure legitimacy and trust, an online, legally binding contract is established between the lenders and borrowers. Both parties can view, understand, and digitally sign this agreement, which holds the same legal weight as a physical contract.

6. Disbursal and repayments

Upon successful agreement, loans are transferred to the borrower. Every month, lenders can expect EMIs, which are auto-debited from the borrower and credited to the Lender’s Escrow account, reflecting in the lender’s virtual account on the platform. We will discuss in detail about the checks and repayments in Chapter 4.

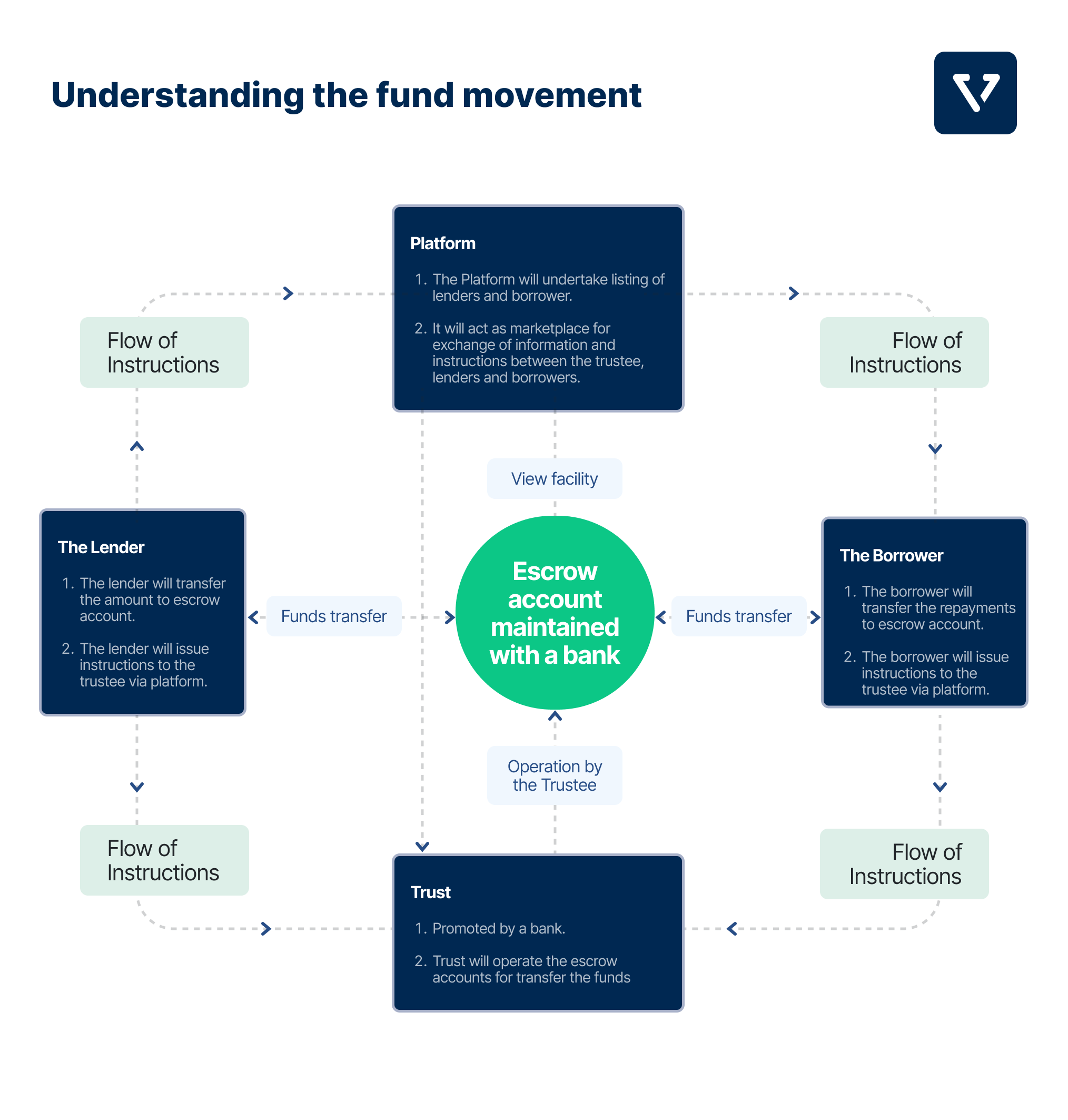

Understanding the fund movement

Role of Platform

The heart of Faircent’s system is the platform. It serves multiple essential functions: (see Figure 6)

Listing of participants: Faircent’s platform lists both lenders and borrowers, offering a comprehensive view of all active members.

Marketplace functionality: Beyond just a listing, the platform acts as a marketplace. Here, the exchange of information and instructions between the trustee, lenders, and borrowers takes place.

Monitoring Escrow Accounts: Faircent prioritizes transparency and accountability. To achieve this, while the platform itself does not directly interfere with the transactions, it retains ‘view only’ access to the escrow accounts. This approach empowers Faircent to meticulously monitor and accurately report all activities, ensuring that every rupee is accounted for and every transaction is transparent to all involved parties.

To optimize operations and ensure a smooth flow of funds between borrowers and lenders, Faircent employs not one, but two distinct escrow accounts:

- Lenders’ Escrow Account: This is specifically tailored for lenders. Whenever a lender commits funds for potential loans, these funds are securely stored in this account, awaiting the fulfillment of loan agreements and eventual disbursement to borrowers.

- Borrowers’ Collection Escrow Account: This account acts as the receiving end of the financial spectrum. Whenever borrowers make repayments, whether regular EMIs or any other financial settlements, the payments are routed into this account.

By distinguishing between these accounts, Faircent ensures a meticulous and organized management of funds, further solidifying the platform’s reputation for transparency, security, and reliability.

Role of the trustee

The operation of the escrow accounts is overseen by a trustee, ensuring that funds are handled with the utmost care and integrity.

An interesting facet of this arrangement is that the trustee is mandatorily promoted by the very bank maintaining the escrow accounts. This ensures an added layer of oversight and accountability, ensuring that both parties’ interests are safeguarded at all times.

Faircent has opened a Lenders Escrow account under the trusteeship of ICICI Trusteeship Services Ltd.

Promotion by a bank: To ensure accountability, the trust is always promoted by a bank, acting as a stamp of credibility.

Operation of Escrow Accounts: Based on the instructions it receives from P2P platforms, the trust operates the escrow accounts. This ensures the fluid movement of funds with meticulous attention to detail.

Banishing cash transactions

In line with global best practices and to ensure traceability and transparency, Faircent’s platform strictly prohibits cash transactions.

Every single fund transfer associated with the platform, be it to or from a bank account, adheres to this principle. This policy not only ensures the legitimacy of each transaction but also fortifies the platform against potential fraudulent activities.

Key Takeaways

In this chapter, we delve into the intricacies of Peer-to-Peer (P2P) lending platforms, illustrating their role in the modern financial ecosystem. Using the case study of Faircent, a P2P lending platform, we dissect the complex interplay of technology, data, and human judgment that drives these platforms.

- P2P lending platforms play a pivotal role in connecting borrowers with lenders, with technology underpinning the entire process.

- Modern P2P platforms rely on automated, rule-based engines and machine learning for efficient customer appraisal, risk assessment, and operational streamlining.

- Multiple layers of checks, both automated and human-driven, are essential in the loan approval process to ensure the credibility, authenticity, and intent of the borrowers.

- Accurate data capture, from personal details to financial health indicators, is crucial for decision-making. Platforms often integrate with external systems like tax databases and credit bureaus to validate this information.

- Despite automation, personal interactions remain invaluable to the loan approval process, providing an extra layer of verification and trust.

- Digital processes, like e-KYC, e-agreements, and digital signatures, not only streamline operations but also enhance user experience, ensuring that transactions are transparent, efficient, and secure.