Skip to content

Skip to content

In our previous chapters, we introduced you to the world of P2P lending, sharing its foundational concepts and how you can think about adding it to your investment portfolio. But, P2P lending is not just about people lending and borrowing money. It’s an ecosystem where everyone has a role to play to make sure the system is efficient, transparent, and trustworthy. Within this ecosystem, one player stands tall as the guardian of order and fairness: the regulator.

In this chapter, we put the spotlight on this important player. As the overseer of the ecosystem, the regulator not only sets the rules of the game but also ensures that every participant plays fairly.

The need for regulation

Lending, at its core, is about trust and mutual benefit. At a very high level, it is similar to shopping but with added complexities. When we shop, we trust that the product we buy is genuine, safe, and worth our money. If there’s no regulation or oversight, we might end up with counterfeit or unsafe products. Similarly, lending without regulation can have detrimental effects on both borrowers and lenders.

Take this simpler example:

Imagine you’re shopping for a toy for a child. You spot a shiny, attractive toy labeled “Safe for Kids.” You trust this label and purchase it. Later, you find out that the toy has small parts that can be hazardous. You feel deceived, and there’s potential harm awaiting the child.

Translate this to the lending world:

Mr Verma, a hardworking individual, decides to take a loan from a local lender, attracted by its “No Extra Charges” promise. After taking the loan, he discovers multiple hidden fees. He struggles to repay the loan, leading to financial stress.

Both scenarios highlight the importance of oversight and the importance of establishing trust. Thus, the role of the regulator is quite important in ensuring the smooth functioning of P2P lending.

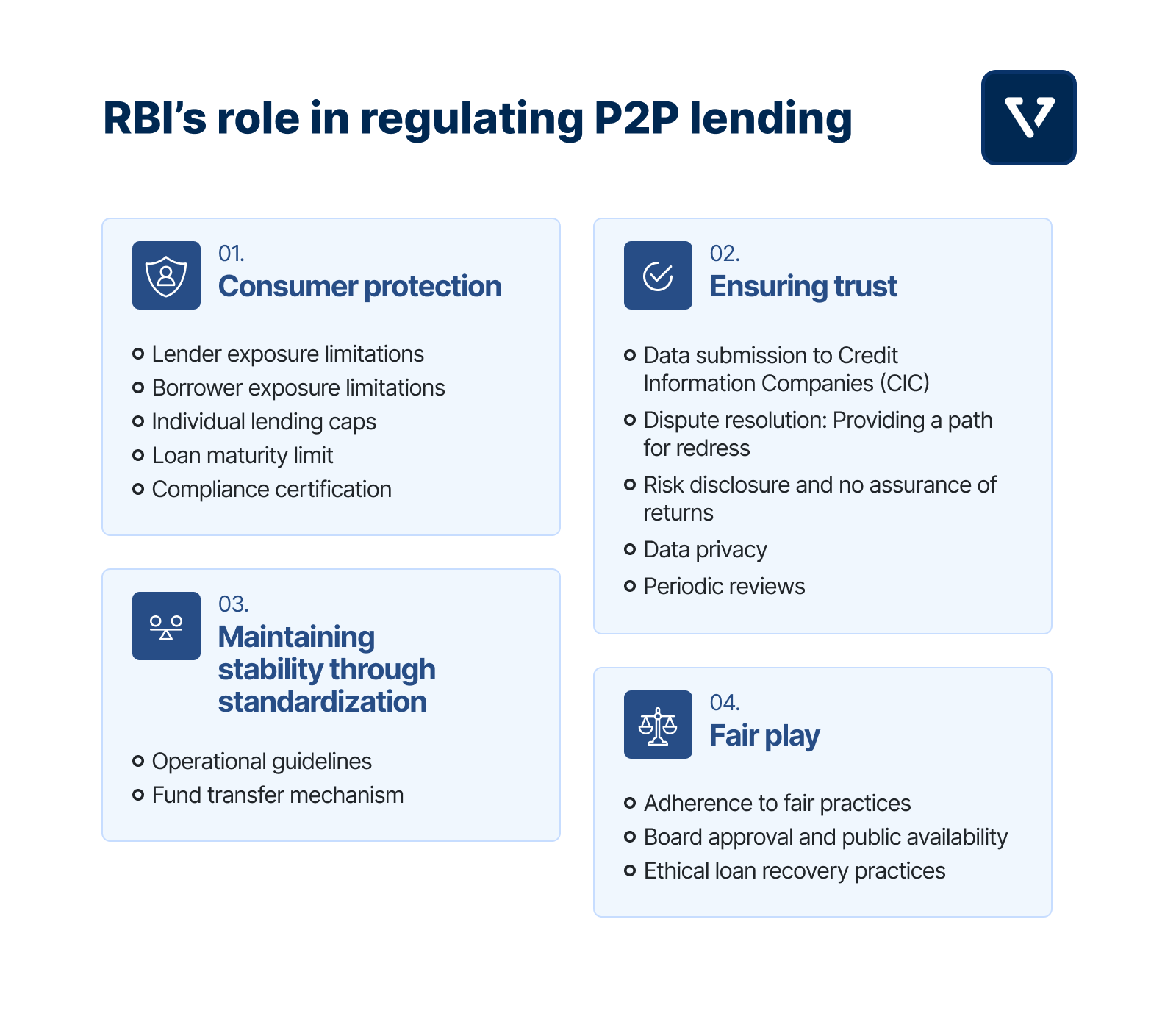

RBI’s role in regulating P2P lending

While P2P lending platforms have improved access to credit and investment opportunities, they have also opened up new avenues for risk. To help ensure that risk in P2P is controlled, the Reserve Bank of India (RBI) stepped in early and formulated regulations that have provided clarity and protection.

In general, RBI has four key roles:

1. Consumer protection

What RBI does: The Reserve Bank of India puts consumer interests at the forefront, setting various norms and conditions to safeguard both lenders and borrowers participating in P2P lending. By adhering to these norms and limits, NBFC-P2P platforms contribute to creating a balanced, secure, and resilient financial marketplace that protects the interests of both lenders and borrowers.

Lender exposure limitations

The maximum amount that a lender can lend across all P2P platforms is capped at ₹50,00,000. This limit is subject to the condition that such investments are aligned with the lender’s net worth.

For lenders investing more than ₹10,00,000 across P2P platforms, a certification from a practicing Chartered Accountant confirming a minimum net worth of ₹50,00,000.

Borrower exposure limitations

A borrower is restricted to aggregate loans not exceeding ₹10,00,000 across all P2P platforms at any given time.

Individual lending caps

The lending exposure from a single lender to the same borrower, across all P2P platforms, is capped at ₹50,000 to mitigate concentrated credit risk.

Loan maturity limit

Loans facilitated through P2P platforms should not have a maturity period exceeding 36 months, ensuring short-term, manageable borrowing.

Compliance certification

P2P platforms must obtain a declaration certificate from both borrowers and lenders, confirming that the aforementioned limits are adhered to.

2. Ensuring trust

What RBI does: To build trust within the P2P lending ecosystem, RBI mandates strict data management, ongoing due diligence, and a robust dispute resolution mechanism.

Data submission to Credit Information Companies (CIC)

In a data-driven world, accurate and timely credit information is crucial for effective financial decision-making. Non-Banking Financial Companies Peer-to-Peer (NBFC-P2P) platforms in India have a mandate to join all Credit Information Companies (CICs) and consistently furnish both historical and current data. This not only aids in evaluating borrower credibility but also ensures the integrity of the entire lending ecosystem.

Dispute resolution: Providing a path for redress

Consumer satisfaction is a cornerstone of any financial service, and NBFC-P2P (Non-Banking Financial Companies Peer-to-Peer) lending platforms are committed to ensuring a seamless experience for their participants. However, grievances are an inevitable part of any service industry, and how these are managed can significantly impact the reputation and effectiveness of the platform. To facilitate efficient grievance redressal, the Reserve Bank of India (RBI) has set forth specific norms for NBFC-P2P platforms. Below is a summary outlining these redressal guidelines.

Board-approved redressal policy

Every NBFC-P2P platform must institute a Board-approved policy aimed at addressing grievances and complaints from participants. This policy must outline the procedures for handling and resolving complaints within a specified time frame.

Timely resolution

All complaints received should be resolved in a manner consistent with the Board-approved policy. In any event, the resolution should not take more than one month from the date the complaint was received.

Transparency at the operational level

To make the grievance redressal process more transparent and accessible, the following information should be prominently displayed on the NBFC-P2P platform’s website:

- Grievance redressal officer: The name and contact information (telephone or mobile numbers, as well as the email address) of the designated Grievance Redressal Officer, who can be contacted for complaint resolution, must be clearly stated.

- Higher authority for unresolved complaints: If the grievance is not resolved within a one-month period, participants should be informed that they have the option to escalate the issue to the Customer Education and Protection Department of the Reserve Bank of India.

Risk disclosure and no assurance of returns

Lenders participating on the platform must give an explicit declaration, acknowledging their understanding of the risks involved in lending transactions. They must be informed that the platform provides no guarantee for the return of principal or interest payments. Furthermore, a clear statement should be displayed, stating that the Reserve Bank of India does not bear responsibility for any claims or opinions expressed by the NBFC-P2P, nor does it assure loan repayments.

Data privacy

Confidential information pertaining to participants should never be disclosed to third parties without explicit consent from the participants involved.

Periodic reviews

The Board of Directors should conduct periodic reviews of the adherence to the Fair Practices Code, as well as the effectiveness of the grievance redressal mechanisms in place. A summary of these reviews should be submitted to the Board at regular intervals.

3. Maintaining stability through standardization

What RBI does: RBI works to stabilize the P2P lending landscape by enforcing financial and operational criteria that platforms must meet, including capital requirements and business monitoring.

In a sector as diverse as P2P lending, standardization is paramount. Without a common set of rules or benchmarks, there can be considerable variation in the level of risk and quality among different P2P platforms. A lack of standardization could lead to unfair practices and put both investors and borrowers at risk.

In order to ensure standardization for all P2P lending platforms, the RBI, published its Master Directions for NBFC (Peer-to-Peer Lending Platforms) in 2017. The guidelines permit various entities—including individuals, societies, HUFs, and firms—to participate in P2P lending. However, only an entity registered as an NBFC can operate a P2P lending intermediary connecting lenders and borrowers. Furthermore, the NBFC-P2P must have a net owned fund of at least ₹2 crore and must maintain a leverage ratio not exceeding 2.

Additionally, to receive a Certificate of Registration (CoR) from the RBI, a P2P lending company must fulfill the following conditions:

- Incorporation within India.

- Availability of adequate technological, entrepreneurial, and managerial resources.

- Submission of a comprehensive business plan for P2P lending activities.

- Possession of a sufficient capital structure and managerial capacity for conducting P2P lending.

Once these conditions are met, the RBI grants in-principle approval for initiating a P2P lending platform. This approval is valid for 12 months, during which the platform must establish its technological infrastructure and documentation. Upon satisfying the RBI’s conditions, the platform is granted a CoR as an NBFC-P2P, subject to additional stipulations as deemed necessary by the regulatory body.

Unlike traditional financial institutions, P2P platforms cannot raise deposits themselves. Instead, they perform a range of activities aimed at streamlining the lending process, risk assessment, and loan recovery using investor capital. Below is a summary of key guidelines provided to NBFC-P2P players in India.

Operational guidelines for NBFC-P2P

- Role as an intermediary: NBFC-P2Ps serve as online platforms that connect participants in the P2P lending space, facilitating the matching of lenders and borrowers.

- Deposit regulations: Platform entities are not permitted to raise deposits like the Banks do.

- Direct lending restrictions: An NBFC-P2P cannot lend its own money.

- No credit enhancements: Platforms are prohibited from offering or arranging credit enhancements or guarantees.

- Type of loans: Only unsecured loans, also known as clean loans, can be facilitated through the platform.

- Funds management: Platforms are not allowed to hold any funds on their balance sheets, whether they come from lenders for disbursement or from borrowers for loan repayments.

- Cross-selling limitations: The only additional products platforms can offer are those directly related to the loan, like insurance products specifically designed for loan coverage.

- International transactions: NBFC-P2Ps are not allowed to facilitate any international flow of funds.

- Legal compliance: They are responsible for ensuring that all participants comply with the relevant legal requirements.

- Data storage: All data related to their activities and participants must be stored and processed on hardware located within India.

Fund transfer mechanism

Ensuring the secure and transparent movement of funds is a critical aspect of Peer-to-Peer (P2P) lending platforms. To this end, the platforms implement a robust escrow account mechanism managed by a bank-promoted trustee. This system is designed to safeguard the financial interests of both lenders and borrowers by creating distinct escrow accounts for incoming and outgoing funds. Below are some additional details that describe the fund transfer mechanism in greater detail.

Use of escrow accounts

Fund transfers between participants on the P2P lending platform will be facilitated through specialized escrow accounts that are operated under the supervision of a trustee endorsed by a bank.

Dual escrow account structure

At least two separate escrow accounts are maintained:

Lender’s escrow account: This account holds funds received from lenders that are yet to be disbursed to borrowers.

Borrower’s collection account: This account is designated for collecting repayments from borrowers.

Strictly bank-based transactions

All fund transfers must occur via these escrow accounts and only through formal banking channels. Cash transactions are expressly forbidden, adding an additional layer of transparency and accountability.

4. Fair play

What RBI does: RBI emphasizes fair and ethical practices in P2P lending, specifying codes and guidelines aimed at transparent and responsible functioning of these platforms.

Adherence to fair practices

Ensuring ethical operations and safeguarding participants’ interests are critical aspects of running an NBFC-P2P (Non-Banking Financial Companies Peer-to-Peer) lending platform in India.

To guide the actions of such platforms, a Fair Practices Code, governed by specific guidelines, must be instituted. This code serves as a transparent operational manual available to all stakeholders, outlining the platform’s commitment to ethical lending practices, risk disclosure, data privacy, and grievance redressal. Below are two key elements of the Fair Practices Code:

Board approval and public availability

An NBFC-P2P must establish a Fair Practices Code based on the prescribed guidelines, and this code should be approved by the organization’s Board of Directors. Once approved, it should be publicly accessible on the platform’s website for stakeholder reference.

Ethical loan recovery practices

In terms of loan recoveries, the platform should ensure that its staff are well-trained to interact appropriately with participants. Harassing tactics, such as repeated calls at unreasonable hours or using coercion, are strictly prohibited.

Key Takeaways

Alright, so in this chapter, we took a look at the role of regulators, specifically the Reserve Bank of India (RBI), in overseeing Peer-to-Peer (P2P) lending platforms in India. Here are the key takeaways:

- Regulation is essential in P2P lending for consumer protection, ensuring trust, maintaining stability, and promoting fair play. Without oversight, borrowers and lenders could be exposed to misleading terms, hidden fees, and unfair practices.

- The RBI requires P2P lending platforms to register as Non-Banking Financial Companies (NBFCs) and adhere to specific financial standards, including net owned funds and leverage ratios. These platforms must also meet conditions like having a business plan and sufficient technological infrastructure.

- P2P platforms only act as intermediaries without the ability to lend or raise deposits themselves. They are required to perform due diligence on participants, assist in loan disbursement and repayment, and faceseveral other operational limitations (e.g., type of loans allowed, no credit enhancements).

- Platforms must submit both historical and current transaction data to CICs, ensuring that the credit information in the system remains up-to-date and accurate, which in turn contributes to the integrity of the lending ecosystem.

- Strict limitations are set for both lenders and borrowers to prevent excessive exposure. Funds transfer is facilitated via escrow accounts, managed by a bank-promoted trustee, to ensure secure and transparent transactions.

- An ethical code must be established by each platform, outlining their commitment to transparent practices, ethical loan recovery, and data privacy. This must be reviewed periodically by the company’s Board of Directors.