Skip to content

Skip to content

Lending forms a vital part of any economy, and India is no exception. Lending helps businesses to expand, empowers individuals to achieve their aspirations, and contributes to the overall prosperity of the country. From the age-old practice of borrowing from money lenders or extended family members to obtaining loans from financial institutions, all of this is a form of lending.

However, in recent years, there has been a transformative evolution in the lending landscape, one such is the rise of P2P lending. Peer-to-Peer (P2P) lending has gained significant traction both globally and in India over the past decade. It presents an alternative option to both borrowers who are seeking money and lenders who are seeking investment opportunities. In this article, we will discuss what P2P lending is, how it works in India, and the benefits and risks associated with it.

What is P2P Lending?

Peer-to-peer (P2P) lending is an online lending model that allows individuals or businesses to borrow money directly from other individuals or investors through a platform. It eliminates the need for traditional financial intermediaries, such as banks or financial institutions, and enables direct interaction between borrowers and lenders. This type of lending is also referred to as “crowdlending” or “social lending.”

Originating in the UK over 18 years ago, P2P lending has rapidly expanded its presence across the globe, gaining widespread popularity. It has experienced remarkable growth at an annual rate (CAGR) of around 30% worldwide in the past few years, with an even more accelerated pace witnessed in India. The rise can be attributed to factors such as increasing internet penetration, the abundance of data, and the continuous evolution of technology, which have collectively contributed to the sophistication and efficiency of these lending platforms.

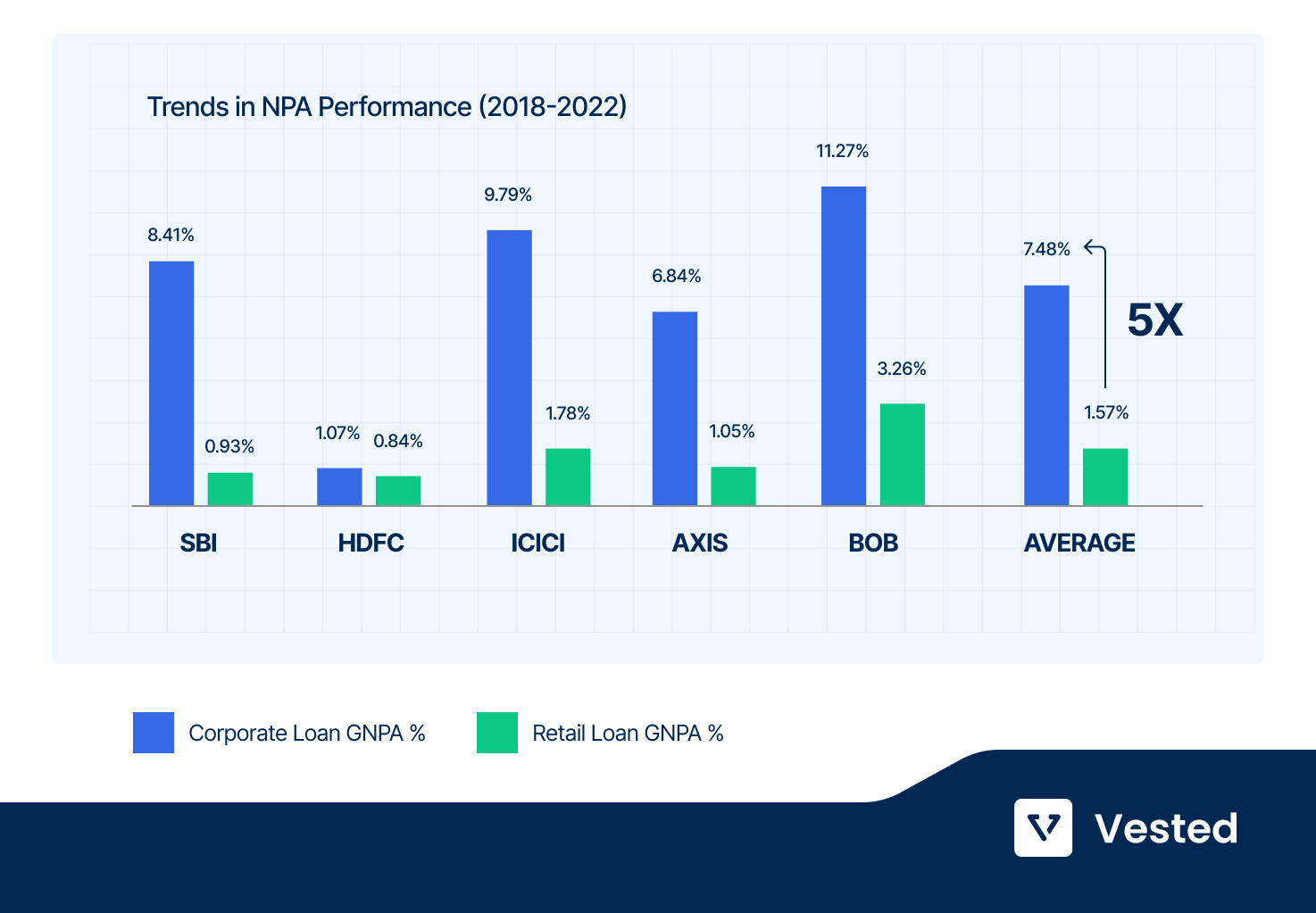

P2P platforms give out loans to retail individuals borrowers mostly. Historically, both globally and in India, retail debt has seen lower NPAs than corporate debt. Retail borrowers generally have a more direct and personal interest in repaying their loans, which often results in better repayment behavior. Moreover, retail borrowers are subject to more stringent credit assessments and due diligence, which helps to minimize the risk of defaults. Below is a graph that supports the statement:

Source: Annual Reports & Management Commentary of SBI, ICICI Bank, HDFC Bank, Axis Bank, Bank of Baroda

How does P2P lending work?

P2P lending platforms connect borrowers and lenders, similar to how Uber connects riders and drivers or Flipkart connects buyers and sellers. The platforms manage both the supply (investors) and the demand (borrowers). The supply side is responsible for handling the investors and onboarding partners, who bring in the investors. The demand side works with loan/vendor partners or even borrowers directly.

Here’s a simplified breakdown of the P2P lending process

- Lender registration: Investors need to register on the platform by providing basic personal information and KYC details

- Borrower registration: Borrowers must complete basic KYC and provide additional details such as credit history, income level, and employment status

- Loan application: Individuals or businesses seeking loans submit applications on the P2P platform, specifying the loan amount, purpose, and relevant information

- Credit evaluation: The platform performs comprehensive due diligence on borrowers, including identification, credit history, and financial capacity. They use various data points and credit assessment tools to evaluate creditworthiness and assign risk categories to borrowers.

- Lender selection: Investors, after registering on the platform, review borrower profiles and loan requests. They select borrowers based on their risk appetite and desired returns.

- Diversification feature:

- Some platforms offer an automatic diversification feature, where investors can allocate funds across multiple borrowers; which otherwise is not feasible manually

- This reduces NPA risks, as exposure to any single borrower is typically kept below 0.5% of the invested amount. Smart algorithms help achieve this diversification, allowing even small investments (such as INR 1,000) to be spread across many borrowers

- Diversification feature:

- Fund disbursement: Once the decision is made to invest in a borrower’s loan, the funds are disbursed to the borrower. In some cases, multiple lenders can collectively fund a single loan

- Loan repayment: Borrowers make periodic repayments, including both principal and interest. P2P platforms facilitate the collection and distribution of payments to lenders.

- Default management: In case of borrower default, P2P platforms have recovery mechanisms in place to mitigate losses for lenders. These may involve legal action or other recovery procedures.

P2P lending thrives on technology, providing efficient and accessible lending solutions to both borrowers and investors. By understanding this process, you can make a more informed decision to invest in P2P lending.

How is P2P Lending regulated in India? Is it legal in India?

P2P lending is legal and fully regulated by the Reserve Bank of India (RBI). The RBI issued a framework on Non-Banking Financial Company-Peer to Peer (NBFC-P2P) Lending Platforms in October 2017. This framework sets out the guidelines and standards that P2P platforms must follow to ensure a safe and transparent environment for both borrowers and lenders.

Here are some of the key regulations that P2P platforms must follow:

- Minimum net-owned fund: P2P platforms must maintain a minimum net-owned fund as specified by the RBI. This ensures that they have the financial resources to operate in a safe and sustainable manner

- Exposure limits: P2P platforms must limit the amount of exposure individual borrowers can receive or individual lenders can invest to mitigate the risks

- Credit assessment: P2P platforms are obligated to conduct thorough credit assessments of borrowers and disclose relevant information to lenders. This ensures that lenders are aware of the risks involved before they invest their money

- Escrow accounts: P2P platforms must maintain escrow accounts operated by bank-promoted trustees. The platforms should not touch the money from investors or borrowers

- Grievance redressal mechanisms: P2P platforms must follow fair practices and have grievance redressal mechanisms in place. This ensures that the interests of both borrowers and lenders are protected

What are the risks associated with P2P Lending?

P2P lending is an innovative and promising form of lending. However, it comes with certain inherent risks that potential investors and borrowers should consider. Here are some of the key risks associated with P2P lending in India:

Credit risk: The most significant risk in P2P lending is credit risk. This is the risk that borrowers may fail to repay their loans, leading to potential losses for lenders. In case of a default, P2P platforms may use a combination of soft and hard collections to collect missed payments on the lender’s behalf. Soft collections may include contacting the borrower to remind them of their payment due date or sending them a letter or email. Hard collections may include taking legal action against the borrower or working with a collection agency to recover the debt.

- To mitigate this risk, diversifying investments across multiple borrowers can help spread the exposure and minimize the impact of defaults on overall returns

Platform risk: There is a risk that some P2P platforms may be fraudulent or poorly managed, resulting in potential loss of investments or compromise of personal information.

- You should carefully research and invest in multiple well-established and regulated platforms to minimize platform-related risks

Illiquidity Risk: P2P lending typically has fixed tenures, and you may not be able to access your invested funds until the loan matures. In case of urgent cash needs, this illiquidity can be a drawback.

- You can park or invest the emergency funds in a liquid plan offered by some of the platforms

Regulatory risk: Although P2P lending is regulated in India, changes in regulatory policies or the introduction of new regulations could affect the functioning of P2P platforms or the returns expected by investors.

- Opting for platforms that strictly adhere to regulatory guidelines can help mitigate regulatory risks

Macro-Economic Factors: Economic downturns or financial crises can impact borrowers’ ability to repay loans, increasing the likelihood of defaults.

- Diversifying your investments across different asset classes and industries can reduce the impact of such macroeconomic events

What happens when the P2P platform shuts down?

P2P lending platforms are regulated by the Reserve Bank of India (RBI) to ensure that they operate in a safe and transparent manner. In the event that a P2P platform shuts down, there are a number of measures in place to protect the interests of lenders and borrowers.

- Escrow accounts: All transactions on P2P platforms are processed through an escrow account operated by a bank-promoted trustee. This ensures that the funds of lenders are held in a safe and secure manner. In the event that a platform shuts down, the escrow account will be used to distribute the funds to lenders. This provides a layer of security for lenders’ investments

- Loan contract enforceability: Each loan facilitated through the P2P platform is backed by a legally enforceable loan contract signed by the individual borrower. In the event of platform closure, the loan contract remains valid, and borrowers are still obligated to fulfil their repayment commitments to lenders

- Deposit requirement: As part of the licensing process, the RBI requires P2P platforms to maintain a deposit of INR 2 crores or as specified. This amount will be used to set up a recovery measure, and a committee will utilise this for completing the transaction process and in, recovering the money from the borrowers and providing it to the lenders

- Business continuity plan: RBI guidelines mandate that P2P platforms have a Business Continuity Plan (BCP) in place in the event of platform closure. The BCP outlines measures to safeguard lenders’ and borrowers’ information and ensures data protection during the transition or closure process.

While the regulatory measures help provide some level of protection, there may still be uncertainties and risks involved when a P2P platform shuts down. It is essential for investors to be aware of this possibility and to diversify their investments across multiple platforms to minimize potential losses. Furthermore, selecting well-established and regulated platforms with a proven track record of quality risk management can add an extra layer of security to P2P lending investments.

How do taxes work in P2P Lending?

Interest income earned from P2P lending is taxed under “Income from Other Sources” as per your current tax slab just like your savings/FD interest. There will be no TDS (Tax Deducted at Source) deducted when you withdraw your money or receive any interest.

Conclusion

By understanding the intricacies of P2P lending and being aware of the associated risks, you can make well-informed decisions and leverage the potential benefits offered by this product. P2P lending is a relatively new product, and as such, there are still some risks involved. However, it can be a great way to diversify your portfolio and earn returns up to 12% that can beat inflation as well as fixed deposits. Finally, it is also important to understand that even though the returns are higher in P2P lending, they are not guaranteed.