Skip to content

Skip to content

Executive Summary

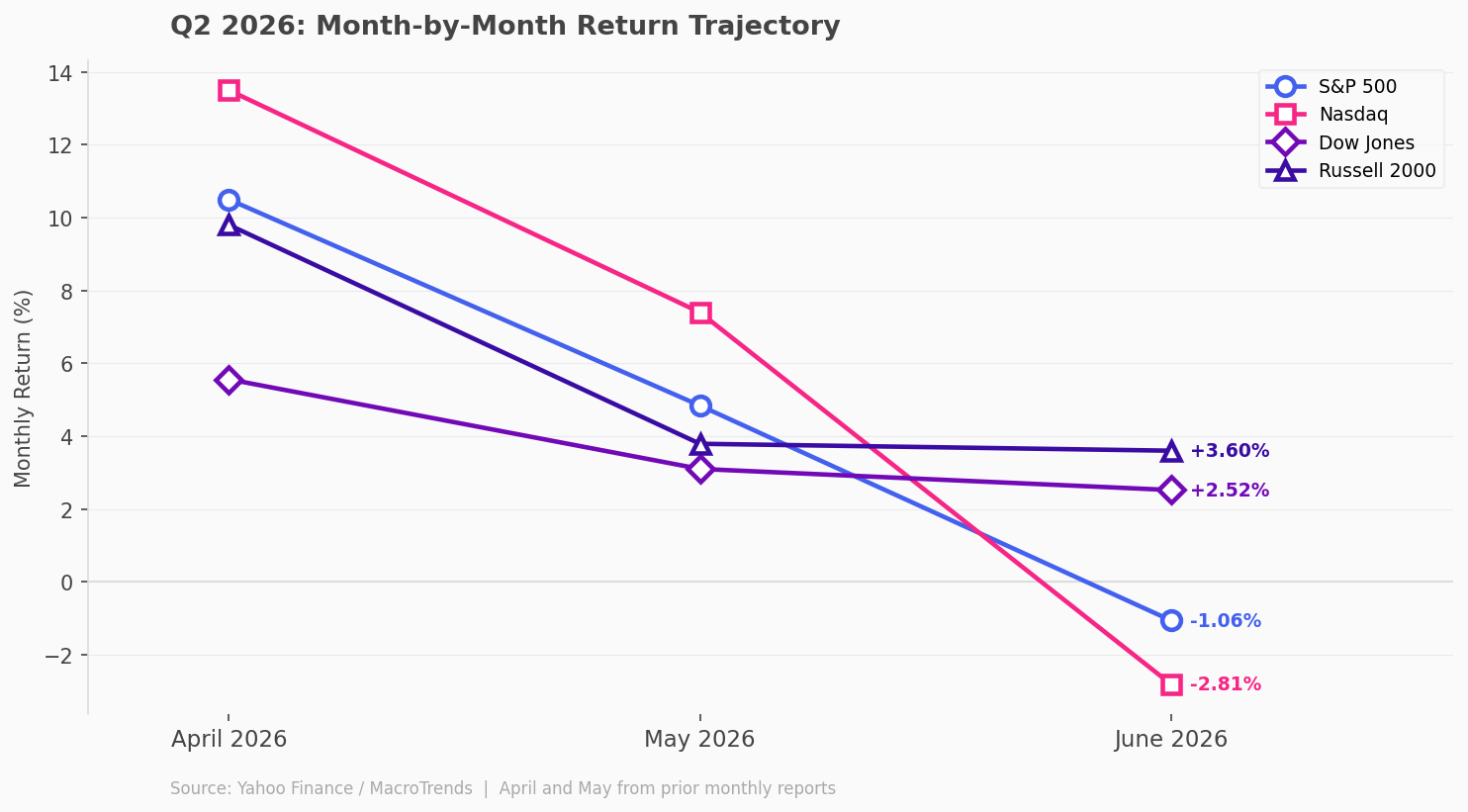

June 2026 did not follow May’s script.

After back-to-back months of double-digit gains in April and May, June brought a reset. The S&P 500 finished the month down 1.06%. The Nasdaq fell 2.81%. But beneath those modest headline declines sat an extraordinary sequence of events: the largest IPO in capital markets history, the Federal Reserve’s first policy meeting under a new chairman that sent the two-year yield spiking 16 basis points in a single day, a semiconductor correction that erased weeks of gains in days, and a US-Iran ceasefire that fractured repeatedly before barely holding.

Two forces defined the month. The first was the SpaceX IPO, which raised $85.7 billion at a $1.75 trillion valuation and within days briefly pushed SpaceX above Amazon and Microsoft in market cap. The second was Kevin Warsh’s debut FOMC meeting on June 16-17, which stripped the easing bias from the Fed’s statement and formally reset market expectations from cuts to possible hikes by year-end.

The Dow and Russell 2000 told a different story, gaining 2.52% and 3.60% respectively, as value rotation and Alphabet’s addition to the Dow provided meaningful offset to the tech and semiconductor drag.

Q2 2026 closed as the best quarter for US equities since the pandemic recovery in 2020: S&P +14%, Nasdaq +20%, Dow +12%. June’s modest retreat did not undo those gains. It just reminded markets that what goes up on AI enthusiasm can come down on AI reality checks.

| -1.06% S&P 500 June Return | -2.81% Nasdaq June Return | +2.52% Dow Jones June Return | +3.60% Russell 2000 June Return |

| +14.0% Q2 2026 S&P Return | +20.0% Q2 2026 Nasdaq Return | $85.7B SpaceX IPO Raised | +346% Micron Revenue YoY |

Index Performance

| Index | June 30 Close | June Return | YTD Return |

|---|---|---|---|

| S&P 500 | 7,499.36 | -1.06% | +9.55% |

| Nasdaq | 26,213.72 | -2.81% | +12.79% |

| Dow Jones | 52,319.20 | +2.52% | +8.85% |

| Russell 2000 | 3,024.37 | +3.60% | +21.90% |

| VIX | 16.45 | +7.4% | N/A |

What Actually Happened in June: The Big Picture

The SpaceX IPO Rewrote the Record Books

On June 12, SpaceX began trading on the Nasdaq under the ticker SPCX, having priced at $135 per share the previous evening. The company raised $85.7 billion in total, surpassing Saudi Aramco’s 2019 record of $25.6 billion by $60 billion. Within days, SpaceX’s share price surged to as high as $225, briefly pushing its market cap above $3 trillion and making it the fourth-largest company in the world.

The IPO reshaped market conversations simultaneously: it triggered sympathy rallies in every space-adjacent name, raised questions about whether AI-adjacent euphoria had reached a speculative extreme, and set off debate about index inclusion. S&P Dow Jones Indices declined to fast-track SpaceX into the S&P 500, citing the requirement for four consecutive quarters of GAAP profitability. Nasdaq moved quickly to qualify SpaceX for the Nasdaq-100 under its updated fast-track framework, with inclusion effective July 7.

Warsh’s First FOMC: The Rate Calculus Flips

June 16-17 produced the most consequential monetary policy event of the year so far. The FOMC held rates unchanged at 3.50-3.75%, as universally expected. What was not expected was the totality of the hawkish pivot around the decision.

The committee removed its longstanding easing bias from the statement. The dot plot was retained but revised sharply, with the median FOMC participant now projecting at least one rate hike for 2026. Nine of 18 participants projected the year-end funds rate at or above 4.00%. Chair Warsh was the only participant who did not submit a dot.

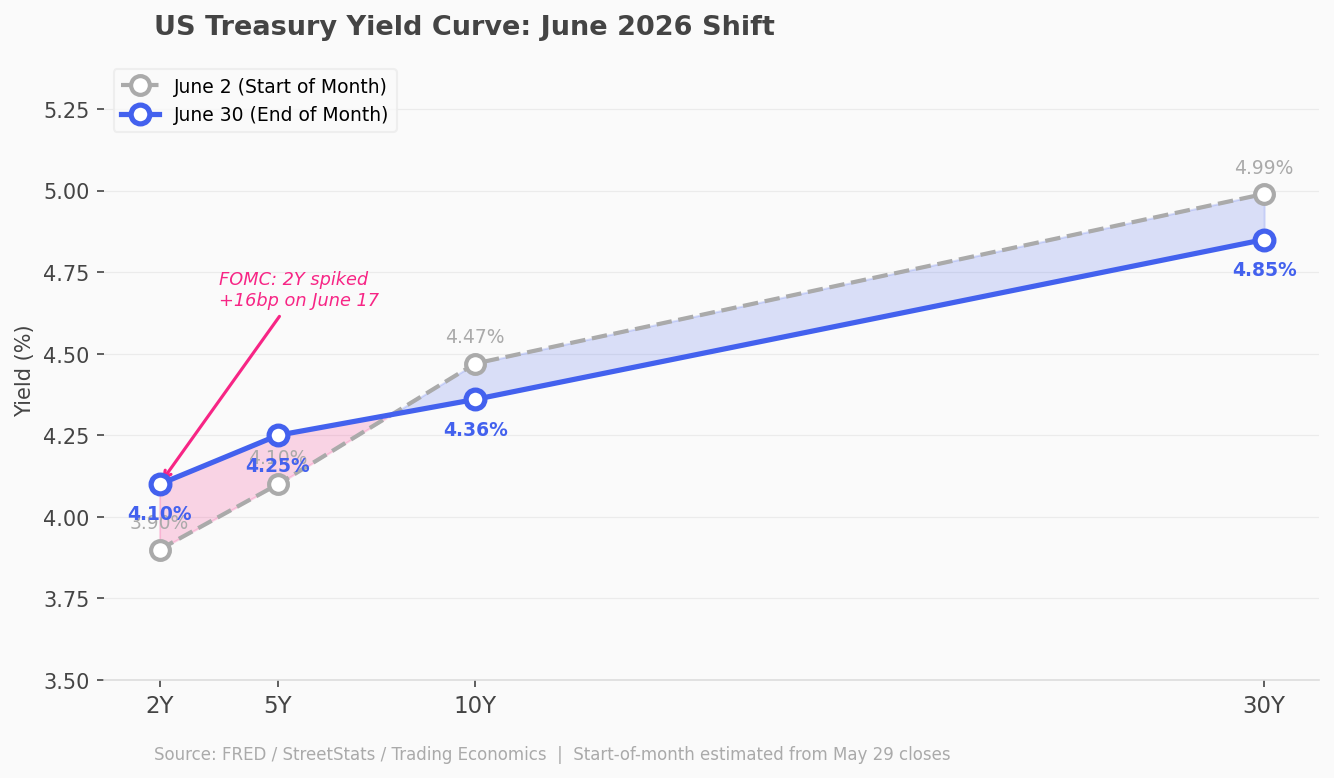

The two-year Treasury yield jumped 16 basis points on June 17 alone, the largest single-day move since March 2008 according to MUFG. By end of June, approximately 34 basis points of Fed tightening for 2026 were priced in.

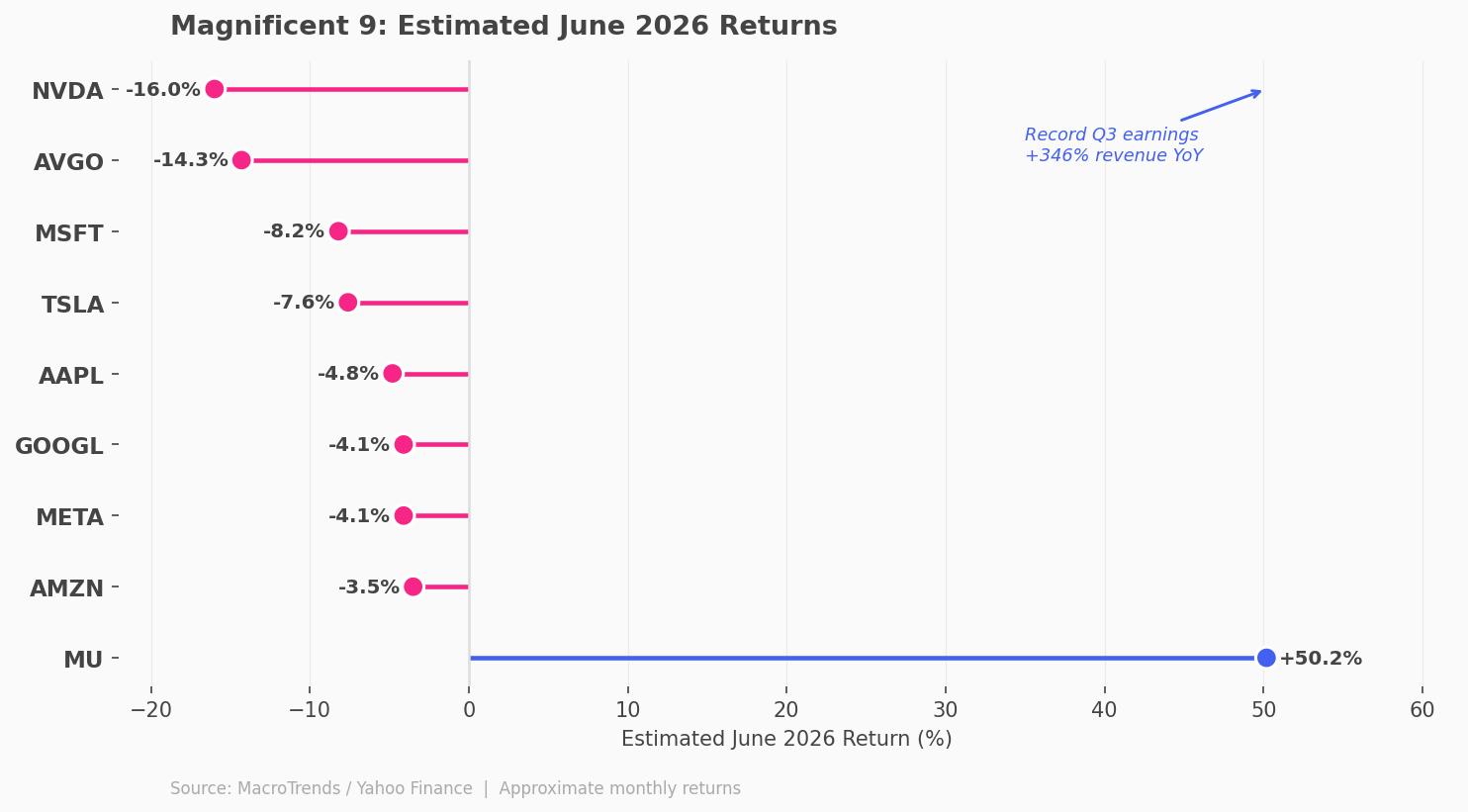

The AI Semiconductor Correction

The second half of June brought a sharp correction in AI-linked semiconductor names. Nvidia fell approximately 16% from its June 10 levels. Broadcom fell 14%. AMD gave back gains. Multiple triggers converged: stretched valuations after the SOXX index had gained more than 230% in 14 months, BofA’s June 23 note on rate hike risks and AI capex sustainability, and OpenAI’s reported decision to delay its IPO to 2027.

The correction was partially offset by Micron Technology’s record Q3 FY2026 earnings on June 25, which drove an 18.4% single-day surge and briefly took Micron’s market cap above $1.4 trillion. Revenue of $41.46 billion was up 346% year-over-year. Even Micron gave back 6.7% the following session as profit-taking set in.

Key Earnings That Shaped the Month

Micron Technology (MU), Q3 FY2026, June 25 after close

The defining earnings report of June. Revenue of $41.46 billion, up 346% year-over-year, broke virtually every record in Micron’s history. Adjusted EPS of $25.11 beat consensus. Q4 revenue guidance of approximately $50 billion was more than double analyst estimates. The stock surged 18.4% to briefly overtake Meta’s market capitalisation. Barclays subsequently raised its price target by 70%.

| Metric | Q3 FY2026 Actual | Consensus | YoY Change |

|---|---|---|---|

| Revenue | $41.46B | ~$20B est. | +346% |

| Adj. EPS | $25.11 | Beat | Record |

| Q4 Guidance | ~$50B | >2x est. | — |

Nike (NKE), Q4 FY2026, June 30 after close

Revenue of $10.972 billion beat the $10.859 billion consensus. GAAP EPS of $0.72 dramatically beat the $0.13 consensus, but included a 52-cent per share benefit from expected IEEPA tariff recovery. Stripping that item, adjusted EPS was approximately $0.20. Wholesale revenues rose 4% while Nike Direct fell 7%. The stock whipsawed after hours as the market parsed the quality of the beat. NKE was down approximately 35% year-to-date entering earnings, trading at 0.5% of the Dow, the same weighting that got Verizon removed.

Macro and Federal Reserve

The Inflation Picture

May CPI, released June 10, came in at 3.8% year-over-year for the headline and 3.3% for core. The May PCE report on June 26 showed headline at 4.1% year-over-year (highest since 2023), core at 3.4% year-over-year. The MoM headline reading came in at 0.4%, one tick below the 0.5% forecast.

The Q1 GDP final revision came in at +2.1% annualised, revised up from +1.6%. The combination of above-target inflation and resilient growth continues to generate a stagflationary undertone.

| Metric | Reading | vs. Prior / Target |

|---|---|---|

| May CPI (YoY) | 3.8% | Highest since May 2023 |

| May Core PCE (YoY) | 3.4% | Highest since Oct 2023 |

| May PCE Headline (YoY) | 4.1% | Highest since 2023 |

| Q1 GDP Final | +2.1% | Revised up from +1.6% |

| Univ. of Michigan (Jun) | 49.5 | Below 50.0 expected |

| Fed Funds Rate | 3.50-3.75% | Held at June 17 FOMC |

Treasury Yields: June Shift

| Maturity | June 2 (Start) | June 30 (End) | Move |

|---|---|---|---|

| 2-Year | ~3.90% | 4.10% | +20 bp (FOMC spike) |

| 10-Year | ~4.47% | ~4.36% | -11 bp (oil-driven relief) |

| 30-Year | ~4.99% | ~4.85% | -14 bp |

| DXY | ~100.5 | ~100.97 | +0.47 |

The Geopolitical Backdrop

US-Iran War: Ceasefire Architecture Under Stress

The Islamabad Memorandum of Understanding, signed remotely on June 17, established a 60-day extension of the original April 8 ceasefire, committing both sides to halt hostilities, reopen the Strait of Hormuz, and enter formal negotiations across four working groups. The framework fractured repeatedly almost immediately.

| Date | Event | Brent Impact |

|---|---|---|

| Jun 17 | Islamabad MoU signed, 60-day extension | Brent holds $78-80 |

| Jun 22 | Tensions resurface; AI correction starts | Brent drifts lower |

| Jun 25 | IRGC drones attack cargo ship Ever Lovely | Brent -2%, tankers kept moving |

| Jun 27-28 | US strikes Iran; Iran hits US bases in Kuwait/Bahrain | Brent +1.5%, then fades |

| Jun 29 | US-Iran stand-down; Doha talks announced | Brent retreats to ~$72 |

Major Corporate Activity

SpaceX IPO (SPCX, Nasdaq, June 12)

The largest IPO in capital markets history. Raised $85.7 billion at $135/share. Opened at $150, briefly traded above $225. Goldman Sachs led the syndicate. SpaceX joined the Russell 1000 effective June 26 post-close, with Nasdaq-100 inclusion confirmed for July 7. JPMorgan estimated $4.3 billion in passive inflows from the Nasdaq-100 addition alone.

Comcast NBCUniversal Spin-Off (announced June 29)

Comcast announced a tax-free spin-off of NBCUniversal and Sky into a separate publicly traded company. The new NBCUniversal will hold Universal studios, theme parks, NBC, Telemundo, Peacock, Bravo, and Sky. Comcast retains broadband and wireless connectivity. CMCSA gained 4.53% on announcement day and a further 17% the following session as the market applied sum-of-parts valuation.

Alphabet Joins the Dow Jones (effective June 29)

S&P Dow Jones Indices announced on June 23 that Alphabet (GOOGL) would replace Verizon (VZ) in the 30-stock index, effective June 29. Alphabet’s first session as a Dow component produced a 4.79% gain. Verizon fell 5.2% on mechanical index rebalancing.

Rocket Lab Acquires Iridium ($8 billion, announced June 29)

Rocket Lab (RKLB) will acquire Iridium (IRDM) in a cash-and-stock deal at $54 per share, a 24.1% premium. The deal gives Rocket Lab a 66-satellite LEO network, L-band spectrum, and 2.55+ million subscribers. Explicitly framed as a SpaceX-style vertical integration play to compete with Starlink. RKLB surged 15.9% and IRDM 25.5% on the announcement.

Honeywell Three-Way Separation (effective June 29)

Honeywell completed the spin-off of Honeywell Aerospace (HONA) effective June 29, alongside a 1-for-2 reverse stock split of the remaining Honeywell Technologies (HON). The breakup completes a multi-year transformation into three independent public companies.

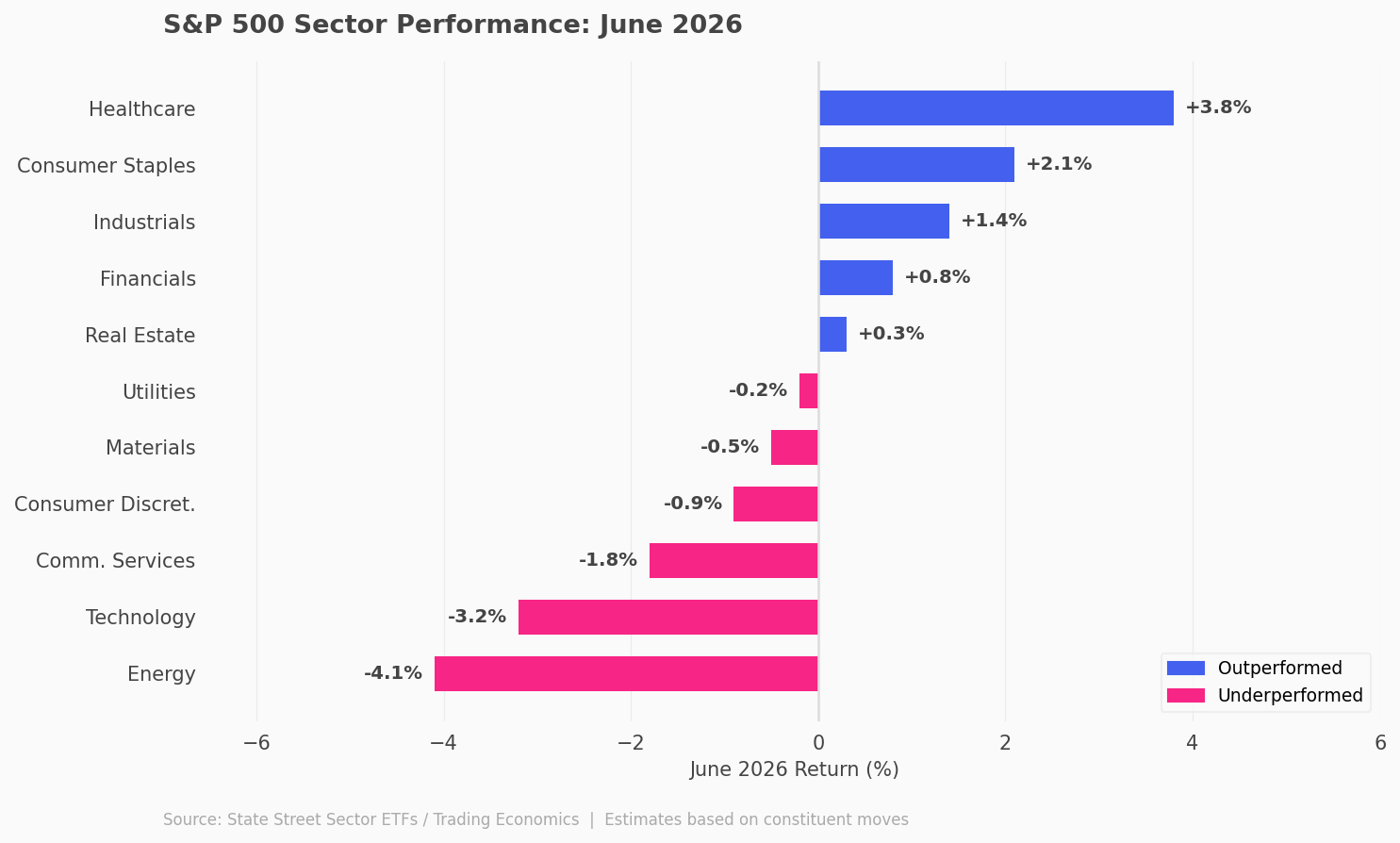

S&P 500 Sector Performance: June 2026

Healthcare led the month on Eli Lilly’s EU leukemia therapy approval. Energy and Technology were the primary drags, with the semiconductor correction and oil price declines creating a double headwind for AI infrastructure names. The Dow’s value rotation played out in the industrial and financial components.

Key Themes That Shaped the Markets in June

June was a strong month for the Genomics Portfolio. More companies in this space are getting better at reading DNA quickly and cheaply, and demand for that kind of testing keeps growing. A few names also bought smaller companies to add new capabilities, and investors liked that.

The bigger shift here is that genomic testing is moving from labs into everyday doctor visits. That is a big deal, because it means this is turning into a real, growing business, not just science that sounds promising.

Deglobalization kept climbing in June as tariffs stopped being a scary headline and became something companies just plan around now. Countries have also started signing trade deals that skip the US entirely, which shows this trend is bigger than just American policy.

Companies are shifting where they manufacture and who they buy from, not because they have to for now, but because it has become the smarter long term move. That shift is what is driving this portfolio.

Defense had a slower month compared to earlier this year, but demand is still there under the surface. Late in June, the Pentagon asked Congress for 87.6 billion dollars to restock weapons used during the Iran conflict, and Lockheed landed a 35.3 billion dollar missile defense contract in that same window.

This is how defense spending usually works. Weapons get used, stockpiles run low, and new orders follow a few months later. June was that in-between waiting period.

Looking Ahead: What to Watch in July

July 2: June Nonfarm Payrolls (moved from July 4 holiday)

The single most important data point of the week. Markets are pricing meaningful Fed tightening for September. A print above 200,000 with wage acceleration hardens those odds substantially. Markets are closed July 3 and July 4 (observed).

July 7: SpaceX Joins Nasdaq-100

Passive funds tracking the index begin purchasing after July 6 close. JPMorgan estimates $4.3 billion in forced passive inflows. The stock is trading approximately 30% below its post-IPO high, meaning institutional buying arrives at a discounted price. Watch SPCX behaviour as a signal for broader risk appetite in high-valuation technology names.

US-Iran: Doha Talks and Ceasefire Durability

The 60-day MoU runs through mid-August. Both sides have already exchanged strikes twice since signing. Any failure to make progress on the Strait navigation and nuclear working groups raises the probability of renewed escalation and an oil spike that directly re-ignites the inflation math the Fed is navigating.

Q2 Earnings Season Preview: The Memory Cost Test

Q1 earnings were largely insulated from the oil and memory cost shock. Q2 results, beginning mid-July, will show whether companies absorbed those costs, passed them through, or lost volume. Apple, Microsoft, and their consumer hardware supply chains will be the first test. Gross margin trajectories for industrials, consumer goods, and transport names will define whether the AI-driven earnings growth narrative can survive a real cost cycle.

Conclusion

June 2026 contained everything at once. The largest IPO in history. The most hawkish Fed pivot in a decade. A semiconductor correction that questioned the AI infrastructure thesis. A Middle East ceasefire that fractured repeatedly but somehow held at the margins. And a quarter-end that closed out Q2 as the best three months for equity markets since the pandemic recovery.

What June said most clearly is that the market is no longer willing to simply look past macro uncertainty on the strength of AI earnings momentum. The final two weeks of the month demonstrated that even exceptional fundamental results can trigger corrections when the price paid for those results was already exceptional.

The Q3 setup is more complex than Q2’s was. The fundamentals remain supportive. The positioning is less certain. Going into July, investors face a shortened trading week, a payrolls report that will define rate-path expectations, a $4 billion passive buying event for a stock that has halved from its high, and a ceasefire that requires active maintenance rather than passive holding.

The Key Numbers for June

| Metric | Value |

|---|---|

| S&P 500 June Return | -1.06% |

| Nasdaq June Return | -2.81% |

| Dow Jones June Return | +2.52% |

| Russell 2000 June Return | +3.60% |

| Q2 2026 S&P 500 Return | +14.0% |

| Q2 2026 Nasdaq Return | +20.0% |

| SpaceX IPO Raise | $85.7 billion |

| 2Y Treasury Yield Move (June 17) | +16 bp in one day |

| Micron Q3 Revenue | $41.46B (+346% YoY) |

| Brent Crude (Month End) | ~$72/barrel |

| Fed Funds Rate | 3.50-3.75% (unchanged) |

This article draws from sources such as the Financial Times, Bloomberg, and other reputed media

houses. Please note, this blog post is intended for general educational purposes only and does not

serve as an offer, recommendation, or solicitation to buy or sell any securities. It may contain

forward-looking statements, and actual outcomes can vary due to numerous factors. Past performance

of any security does not guarantee future results. This blog is for informational purposes only.

Neither the information contained herein, nor any opinion expressed, should be construed or deemed

to be construed as solicitation or as offering advice for the purposes of the purchase or sale of

any security, investment, or derivatives. The information and opinions contained in the report were

considered by VF Securities, Inc. to be valid when published. Any person placing reliance on the

blog does so entirely at his or her own risk, and does not accept any liability as a result.

Securities markets may be subject to rapid and unexpected price movements, and past performance is

not necessarily an indication of future performance. Investors must undertake independent analysis

with their own legal, tax, and financial advisors and reach their own conclusions regarding

investment in securities markets. Past performance is not a guarantee of future results.