Skip to content

Skip to content

Welcome back to a new edition.

Mark Twain once put it simply:

“It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

This week, the AI trade had its most interesting week in months. Because everything that the market was certain about turned out to be wrong.

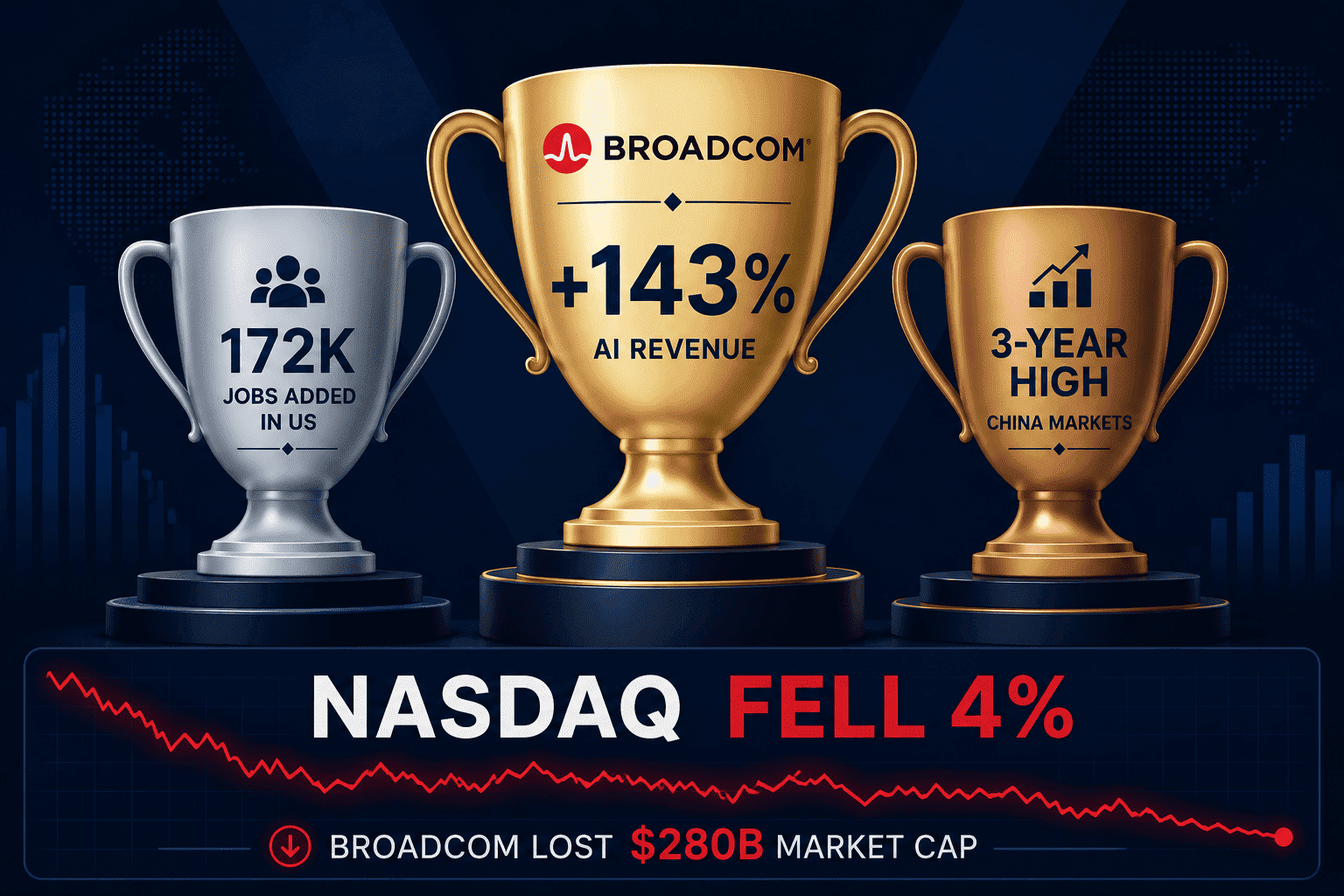

Broadcom posted record quarterly earnings. Yet, the stock fell for two days straight and lost $280 billion. The US had a record job addition. Markets fell anyway.

China’s stock market and currency hit a 3-year high. While Wall Street was panicking.

Oil started the year at $60, had a roller coaster ride, and is sitting at $93 today. And it is quietly making the most expensive technology buildout in history even more expensive.

All three stories, very intertwined and connected. So what is actually going on?

Before we get to that, an exciting update from us.

Your FY 2025-26 tax documents are now live on Vested! Get all tax documents for your entire Vested portfolio: Stocks, ETFs, Global Funds, Managed Portfolios and Private Markets, all in one place, and also a feature that allows you to file directly.

Just go to your Profile. Then click on Tax Documents.

View Tax Documents

Now, back to the markets.

But first, let’s see how the rest of the world held up this week.

The World in a Week: How Major Markets Moved

The week had all the ingredients for a milestone. The Dow hit a fresh record on Thursday. The S&P 500 was eyeing its tenth straight weekly gain.

Then Friday happened.

The US added 172,000 jobs in May, double of what economists expected. Normally, that is great news. But here is the problem: a strong job market means the economy does not need help, which means the Fed has no reason to cut interest rates. And markets had been hoping for cuts. So good economic news became bad market news.

Then Broadcom declined to lift its AI chip targets. That was all the market needed.

Semis went into freefall. The Nasdaq dropped 4.2%, its worst session since April 2025. The S&P lost 2.6%. Marvell and Micron fell double digits. The 10-year yield pushed above 4.5%. A week that nearly made history ended in a heap.

Asia felt the spillover. South Korea’s Kospi fell as much as 5%, triggering a circuit breaker. The Nikkei gave back part of a strong month. China’s Shanghai held firm near 4,066, insulated from the AI hardware selloff.

Europe was largely calm until the Friday wobble.

India was the quiet standout. Benchmarks finished roughly flat. The RBI held its repo rate at 5.25% despite the rupee being down about 5% since February. Media, PSU banks, and realty outperformed.

News Summaries

Broadcom Had a Record Quarter. Still Lost $280B Overnight.

On June 3, after US markets closed, Broadcom reported its Q2 FY2026 earnings. The stock had already closed at an all-time high that same day, at $479.23.

Then the numbers came out.

AI chip revenue: +143% year on year. Total revenue: $22.19 billion, up 48%. Profit per share: up 54%. Free cash flow: $10.3 billion, which is 46% of total revenue coming out as actual cash. Next quarter revenue guidance: $29.4 billion, beating the analyst estimate of $28.61 billion.

Every single number beat expectations.

But why did the stock fall 12% the next morning?

One number. AI chip revenue guidance for Q3: $16 billion. The whisper number was $17.2 billion.

That $1.2 billion gap erased $280 billion in market cap by June 4. Reportedly one of the three biggest single-day wipeouts in US megacap history since 2019.

On the same call, CEO Hock Tan announced Broadcom is narrowing to “chips only,” stepping back from an earlier plan to build complete integrated AI systems. A real strategic change. Getting less attention than it deserves.

Then on June 5, the pain continued. Broadcom fell another 3.8%. Micron dropped 6.3%, although it had zero news of its own this week. It fell just for being in the same sector.

Anyways, here is the part worth sitting with.

Broadcom already has its customers locked in. Google, Meta, OpenAI, and Anthropic are all signed up on multi-year contracts. Its confirmed order book sits at $73 billion.

So, the business is not in trouble. The stock fell because Wall Street had already priced in a future even better than the one Broadcom delivered.

The India-lens: The AI supply chain is one of the most important investment themes of this decade. A week like this is a reminder that how you own it matters as much as whether you own it. Managed Portfolios on Vested, like the Artificial Intelligence portfolio, are built and rebalanced across the full supply chain by the research team. You get the exposure without the single-stock noise.

Invest in Managed Portfolios

Chinese Markets and its Currency are Having a Moment.

On June 5, Bloomberg reported that the 40-day correlation between China’s main stock index CSI 300 and its currency Yuan hit a 3-year high. Both have risen together every single month of 2026. Five months in a row.

This is not normal. When stocks and a currency rise together consistently, it means foreign capital is buying both simultaneously. Local investors do not move currency. Foreign investors do, when they buy both assets at once. A 3-year high here means the conviction is the strongest it has been since 2023.

The numbers back it up.

China’s main stock index, the CSI 300, is at its highest since early 2022. Up 26% over the past year. The Hang Seng Tech Index is up 42% this year alone.

Goldman Sachs raised its China earnings growth forecast from 4% last year to 14% for 2026 and 2027. BofA says global investment flows are now split 50-50 between the US and the rest of the world for the first time in five years.

The valuation gap makes this harder to ignore. Chinese stocks trade at 15.1x earnings. US stocks at roughly 22x. A similar AI story, meaningfully cheaper.

And there is one more reason China is winning right now that connects directly to the oil story. We will get to that later.

Anyways, risks are real and policy can shift quickly. Geopolitical tensions with the US remain. This is a rotation story, not exactly a “China has won” story.

The India-lens: Global capital flows are shifting. For five years, almost everything went to the US. In 2026, that is changing, and an investor building a genuinely global portfolio would want to be part of that shift, not watching it from the sidelines. Global Funds on Vested give you access to international markets and this broader diversification without having to pick individual stocks or markets yourself.

Invest in Global Funds

Iran Suspended Talks. Oil Jumped 4.3%. The Fed Did Not Blink.

On June 1, Iran walked away from peace talks. Brent jumped 4.3% in a single session. On June 3, a US strike hit an oil tanker bound for Iran. Iran responded with attacks on US naval bases in Bahrain and Kuwait.

By June 5, Trump signalled diplomatic progress and Chinese crude imports fell to a 10-year low, pulling Brent back to $93.

To understand why this matters, you need the backstory. In late February, the US and Israel struck Iran. The Strait of Hormuz, through which 20% of the world’s daily oil flows, effectively closed. By April 7, Brent had hit $138 intraday. The IEA called it the “largest supply disruption in history,” 2 to 3 times the scale of the 1973 oil crisis. A ceasefire in May brought it down 19% in a single month.

That is the world Brent at $93 is coming from. Still 43% higher than where it started the year.

Source: Trading Economics

The strait remains effectively closed to Western tankers. But here is what almost nobody is talking about.

Here is what is actually happening. Iran did not close Hormuz for everyone. Chinese ships pass freely. Most western tankers wait or are turned back. Essentially, China gets cheap oil while the West pays a war premium.

That is one reason Chinese stocks and the yuan are both rising while Western markets deal with expensive energy.

Now add another layer. The US central bank has not cut rates since late 2024. Borrowing costs have sat at 3.5–3.75% all year. At their April meeting, almost every member voted to hold. Markets now price a near 50-50 chance of zero cuts in all of 2026.

And yet the AI companies are still spending. Meta $125–145 billion this year. Alphabet $180–190 billion. Amazon roughly $200 billion. Over $650 billion across five hyperscalers, all being built at the highest borrowing costs in years.

High rates do not stop the spending. They just make the future returns harder to achieve. And with oil still 43% above where it started the year, the cost of running the world is not coming down anytime soon either.

Goldman Sachs sees Brent averaging $100+ if Hormuz stays this way for another month.

The India-lens: India imports roughly 85% of its oil. At $93 Brent, the cost flows through to petrol prices, inflation, and the Reserve Bank’s rate decisions. A wider oil import bill puts pressure on the rupee, which quietly compresses the real returns on rupee-denominated savings over time. This week is a reminder that global events shape Indian portfolios even when you feel insulated in domestic stocks. We covered exactly why in this video at Global Markets by Vested.

Watch on YouTube

Now step back and look at all three together.

Broadcom did everything right and got punished for not doing it better. A jobs report came in strong and markets fell anyway. China picked up the capital that quietly left US tech. And oil is costing everyone more, including the AI companies spending $650 billion to build the future, at exactly the moment when high borrowing costs are making that future more expensive to fund.

The week had a single thread running through all of it. Good news is bad news. Strong earnings are not enough. Strong jobs are not enough.

The market is not rewarding what happened. It is punishing what might not happen next.

Interesting to see how it turns out.